Without searching through my old posts, I’m confident that I’ve already made this point many times in passing, but I just want to restate this point up front — highlighted and underscored. Any economic model must satisfy the following rational-expectations condition:

If the agents in the model expect the equilibrium outcome of the model (or, if there are multiple equilibrium outcomes, they all expect the same one of those equilibrium outcomes), that expected equilibrium outcome will be realized.

When the agents in an economic model all expect the equilibrium outcome of the model, the agents may be said to have rational expectations, and those rational expectations are self-fulfilling. Any economic model that lacks this contingent RATEX property is incoherent. But unless an economic model provides a theory of expectation formation whereby the agents all form correct expectations of the equilibrium outcome of the model, RATEX is a merely contingent, not an essential, property of the model.

Although an actual expectation-formation theory of rational expectations has never, to my knowledge, been derived from plausible assumptions, the RATEX assumption is disingenuously insisted upon as a property of rational decision-making implied by neoclassical theory. Such tyrannizing methodological intimidation is groundless and entails the reductio ad absurdum of the Milgrom and Stokey No-Trade Theorem.

This post started out as a short Twitter thread discussing the role of supply shocks in our current burst of inflation. The thread was triggered by Skanda Aramanth’s tweet arguing that, within a traditional aggregate-demand/aggregate-supply framework, a negative supply shock would have an effect sufficiently inflationary to cause the rate of NGDP growth to rise even with an unchanged monetary policy if the aggregate-demand curve is highly inelastic.

Skanda received some pushback on his contention from those, e.g., George Selgin, who dismissed the assumption of an inelastic aggregate demand as an implausible explanation of recent experience.

Here are the tweets by Skanda and George.

I find this attempt to put the burden on those who are not convinced that that an adverse AS shock will raise NGDP unconvincing. The question is, under what circumstances will the AD schedule be inelastic in fact; and it can be so only if either M or V somehow rises as AS falls.

Without weighing in on the plausibility of the inelastic aggregate demand curve assumption, not being very enamored of the aggregate demand/aggregate supply paradigm, which strikes me as a mishmash of inconsistent partial-equilibrium and general-equilibrium reasoning based on a static model with inflationary expectations uneasily attached, I offered the following alternative account of our recent inflationary experience.

There were two supply shocks. The first was the pandemic, in 2020-21. That was followed in late 2021 by the prelude to Putin’s war which sent oil prices up from $50/barrel in early 2021 to nearly $100/barrel by the end of 2021.

The first supply shock required income support for basic consumption during the pandemic resulting in a buildup of purchasing power in the form of cash balances or other liquid assets for which there was no immediate outlet during the pandemic.

The buildup of unused purchasing power implied that the end of the pandemic would involve a positive but transitory shock to aggregate demand when the economy (production and consumption patterns) returned to normal as the limitations imposed by the pandemic began to ease.

The alternative to allowing the positive but transitory shock to aggregate demand would have been to adopt a restrictive policy as the pandemic was easing, which made neither economic or political sense. The optimal policy was to accept temporary inflation during the recovery, rather than impose a deflationary policy to suppress transitory inflation.

The transitory inflation was exacerbated by various supply bottlenecks and shortages of workers and other productive resources, which were reflected the difficulties of ramping up production quickly after lengthy production shutdowns or curtailments during the height of the pandemic.

These transitory difficulties would have likely worked themselves out by the end of 2021 had it not been for the second supply shock associated with the months long buildup to Putin’s war which was anticipated for months before it actually started in February 2022, causing a second increase in inflation just when the first burst of inflation in the second half of 2021 would have tapered off.

No doubt, it would have been better for the Fed to have started tightening earlier so keep the NGDP from increasing so rapidly at the end of 2021 and the start of 2022, but the scare talk about unanchoring inflation expectations has been overdone.

Financial markets clearly reflect expectations that the Fed is going to rein in aggregate demand so that the excess growth in NGDP in 2021 will have little long-term effect. Even with the continuing potential that Putin’s War will cause further supply disruptions with short-term inflationary effects, the current and likely future conditions seem far better than result than that would have produced by the Volcker 2.0 policy for which Larry Summers et al. are still pining.

Nearly 14 years ago, in the summer of 2008, as a recession that started late in 2007 was rapidly deepening and unemployment rapidly rising, the Fed, mainly concerned about rising headline inflation fueled by record-breaking oil prices, kept its Fed Funds target at the 2% level set in May (slightly reduced from the 2.25% target set in March), lest inflation expectations become unanchored.

Let’s look at what happened after the Fed Funds target was reduced to 2.25% in March 2008. The price of crude oil (West Texas Intermediate) rose by nearly 50% between March and July, causing CPI inflation (year over year) between March and August to increase from 4% to 5.5%, even as unemployment rose from 5.1% in March to 5.8% in July. The PCE index, closely watched by the Fed as more indicative of underlying inflation than the CPI, showed inflation rising even faster than did the CPI.

Not only did the Fed refuse to counter rising unemployment and declining income and output by reducing its Fed Funds target, it made clear that reducing inflation was a more urgent goal than countering economic contraction and rising unemployment. An unchanged Fed Funds target while income and employment are falling, in effect, tightens monetary policy, a point underscored by the Fed as it emphasized its intent, despite the uptick in inflation caused by rising oil prices, to keep inflation expectations anchored.

The passive tightening of monetary policy associated with an unchanged Federal Funds target while income and employment were falling and the price of oil was rising led to a nearly 15% decline in the price of between mid-July and the end of August, and to a concurrent 10% increase in the dollar exchange rate against the euro, a deflationary trend also refelcted in an increase in the unemployment rate to 6.1% in August.

Evidently pleased with the deflationary impact of its passive tightening of monetary policy, the Fed viewed the falling price of oil and the appreciation of the dollar as an implicit endorsement by the markets, notwithstanding a deepening recession in a financially fragile economy, of its hard line on inflation. With major financial institutions weakened by the aftereffects of bad and sometimes fraudulent investments made in the expectation of rising home prices that then began falling, many debtors (both households and businesses) had neither sufficient cash flow nor sufficient credit to meet their debt obligations. Perhaps emboldened by the perceived market endorsement of its hard line on inflation, When the Lehman Brothers investment bank, heavily invested in subprime mortgages, was on the verge of collapse in the second week of September, the Fed, perhaps emboldened by the perceived approval of its anti-inflation hard line by the markets, refused to provide, or arrange for, emergency financing to enable Lehman to meet obligations coming due, triggering a financial panic stoked by fears that other institutions were at risk, causing an almost immediate freeze up of credit facilities in financial centers in the US and around the world. The rest is history.

Why bring up this history now? I do so, because I see troubling parallels between what happened in 2008 and what is happening now, parallels that make me concerned that a too narrow focus on preventing inflation expectations from being unanchored could lead to unpleasant and unnecessary consequences.

First, in 2008, the WTI price of oil rose by nearly 50% between March and July, while in 2021-22 the WTI oil price rose by over 75% between December 2021 and April 2022. Both episodes of rising oil prices clearly depressed real GDP growth. Second, in both 2008 and 2021-22, the rising oil price caused actual, and, very likely, expected rates of inflation to rise. Third, in 2008, the dollar appreciated from $1.59/euro on July 15 to $1.39/euro on September 12, while, in 2022, the dollar has appreciated from $1.14/euro on February 11 to $1.05/euro on April 29.

In 2008, an inflationary burst, fed in part by rapidly rising oil prices, led to a passive tightening of monetary policy, manifested in dollar appreciation in forex markets, plunging an economy, burdened with a fragile financial system carrying overvalued assets, and already in recession, into a financial crisis. This time, even steeper increases in oil prices, having fueled an initial burst of inflation during the recovery from a pandemic/supply-side recession, were later reinforced by further negative supply shocks stemming from Russia’s invasion of Ukraine. The complex effects of both negative supply-shocks and excess aggregate demand have caused monetary policy to shift from ease to restraint, once again manifested in dollar appreciation in foreign-exchange markets.

In September 2008, the Fed, focused narrowly on inflation, was oblivious to the looming financial crisis as deflationary forces, amplified by the passive monetary tightening of the preceding two months, were gathering. This time, although monetary tightening to reign in excess aggregate demand is undoubtedly appropriate, signs of ebbing inflationary pressure are multiplying, and many forecasters are predicting that inflation will subside to 4% or less by year’s end. Modest further tightening to reduce aggregate demand to a level consistent with a 2% inflation rate might be appropriate, but the watchword for policymakers now should be caution.

While there is little reason to think that the US economy and financial system are now in as precarious a state as they were in the summer of 2008, a decision to raise the target Fed Funds rate by more than 50 basis points as a demonstration of the Fed’s resolve to hold the line on inflation would certainly be ill-advised, and an increase of more than 25 basis points would now be imprudent.

The preliminary report on first-quarter 2022 GDP, presented a mixed picture of the economy. A small drop in real GDP seems like an artefact of technical factors, and an upward revision seems likely with no evidence yet of declining employment or slack in the labor market. While noiminal GDP growth declined substantially in the first quarter from the double-digit growth rate in 2021, it is above the rate consistent with the 2% inflation rate that remains the Fed’s policy target. However, given the continuing risks of further negative supply-side shocks while the war in Ukraine continues, the Fed should not allow the nominal growth rate of GDP to fall below the 5% rate that ought to remain the short-term target under current conditions.

If the Fed is committed to a policy target of 2% average inflation over a suitably long time horizon, the rate of nominal GDP growth need not fall below 5% before normal peacetime economic conditions have been restored. Until a return to normalcy, avoiding the risk of reducing nominal GDP growth below a 5% rate should have priority over quickly reducing inflation to the targeted long-run average rate. To do otherwise would increase the risk that inadvertent policy mistakes in an uncertain economic environment might cause sufficient financial distress to tip the economy into recession and even another financial crisis. Better safe than sorry.

I’ve written three recent blogposts explaining why the inflation that began accelerating in the second half of 2021 was likely to be transitory (High Inflation Anxiety, Sic Transit Inflatio del Mundi, and Wherein I Try to Calm Professor Blanchard’s Nerves). I didn’t deny that inflation was accelerating and likely required a policy adjustment, but I also didn’t accept that the inflation threat was (or is) as urgent as some, notably Larry Summers, were suggesting.

In my two posts in late 2021, I argued that Summers’s concerns were overblown, because the burst of inflation in the second half of 2021 was caused mainly by increased consumer spending as consumers began drawing down cash and liquid assets accumulated when spending outlets had been unavailable, and was exacerbated by supply bottlenecks that kept output from accommodating increased consumer demand. Beyond that, despite rising expectations at the short-end, I minimized concerns about the unanchoring of inflation expectations owing to the inflationary burst in the second half of 2021, in the absence of any signs of rising inflation expectations in longer-term (5 years or more) bond prices.

Aside from criticizing excessive concern with what I viewed as a transitory burst of inflation not entirely caused by expansive monetary policy, I cautioned against reacting to inflation caused by negative supply shocks. In contrast to Summers’s warnings about the lessons of the 1970s when high inflation became entrenched before finally being broken — at the cost of the worst recession since the Great Depression, by Volcker’s anti-inflation policy — I explained that much of 1970s inflation was caused by supply-side oil shocks, which triggered an unnecessarily severe monetary tightening in 1974-75 and a deep recession that only modestly reduced inflation. Most of the decline in inflation following the oil shock occurred during the 1976 expansion when inflation fell to 5%. But, rather than allow a strong recovery to proceed on its own, the incoming Carter Administration and a compliant Fed, attempting to accelerate the restoration of full employment, increased monetary expansion. (It’s noteworthy that much of the high unemployment at the time reflected the entry of baby-boomers and women into the labor force, one of the few occasions in which an increased natural rate of unemployment can be easily identified.)

The 1977-79 monetary expansion caused inflation to accelerate to the high single digits even before the oil-shocks of 1979-80 led to double-digit inflation, setting the stage for Volcker’s brutal disinflationary campaign in 1981-82. But the mistake of tightening of monetary policy to suppress inflation resulting from negative supply shocks (usually associated with rising oil prices) went unacknowledged, the only lesson being learned, albeit mistakenly, was that high inflation can be reduced only by a monetary tightening sufficient to cause a deep recession.

Because of that mistaken lesson, the Fed, focused solely on the danger of unanchored inflation expectations, resisted pleas in the summer of 2008 to ease monetary policy as the economy was contracting and unemployment rising rapidly until October, a month after the start of the financial crisis. That disastrous misjudgment made me doubt that the arguments of Larry Summers et al. that tight money is required to counter inflation and prevent the unanchoring of inflation expectations, recent inflation being largely attributable, like the inflation blip in 2008, to negative supply shocks, with little evidence that inflation expectations had, or were likely to, become unanchored.

My first two responses to inflation hawks occurred before release of the fourth quarter 2021 GDP report. In the first three quarters, nominal GDP grew by 10.9%, 13.4% and 8.4%. My hope was that the Q4 rate of increase in nominal GDP would show a further decline from the Q3 rate, or at least show no increase. The rising trend of inflation in the final months of 2021, with no evidence of a slowdown in economic activity, made it unlikely that nominal GDP growth in Q4 had not accelerated. In the event, the acceleration of nominal GDP growth to 14.5% in Q4 showed that a tightening of monetary policy had become necessary.

Although a tightening of policy was clearly required to reduce the rate of nominal GDP growth, there was still reason for optimism that the negative supply-side shocks that had amplified inflationary pressure would recede, thereby allowing nominal GDP growth to slow down with no contraction in output and employment. Unfortunately, the economic environment deteriorated drastically in the latter part of 2021 as Russia began the buildup to its invasion of Ukraine, and deteriorated even more once the invasion started.

The price of Brent crude, just over $50/barrel in January 2021, rose to over $80/barrel in November of 2021. Tensions between Russia and Ukraine rose steadily during 2021, so it is not easy to determine the extent to which those increasing tensions were causing oil prices to rise and to what extent they rose because of increasing economic activity and inflationary pressure on oil prices. Brent crude fell to $70 in December before rising to $100/barrel in February on the eve of the invasion, briefly reaching $130/barrel shortly thereafter, before falling back to $100/barrel. Aside from the effect on energy prices, generalized uncertainty and potential effects on wheat prices and the federal budget from a drawn-out conflict in Ukraine have caused inflation expectations to increase.

Under these circumstances, it makes little sense to tighten policy suddenly. The appropriate policy strategy is to lean toward restraint and announce that the aim of policy is to reduce the rate of GDP growth gradually until a sustainable 4-5% rate of nominal GDP growth consistent with an inflation rate of about 2-3% a year is reached. The overnight rate of interest being the primary instrument whereby the Fed can either increase or decrease the rate of nominal GDP growth, it is unnecessary, and probably unwise, for the Fed to announce in advance a path of interest-rate increases. Instead, the Fed should communicate its target range for nominal GDP growth and condition the size and frequency of future rate increases on the deviations of the economy from that targeted growth path of nominal GDP.

Previous monetary policy mistakes that caused either recessions or excessive inflation have for more than half a century resulted from using interest rates or some other policy instrument to control inflation or unemployment rather than to moderate deviations from a stable growth rate in nominal GDP. Attempts to reduce inflation by maintaining or increasing already high interest rates until inflation actually fell needlessly and perversely prolonged and deepened recessions. Monetary conditions ought be eased as soon as nominal GDP growth falls below the target range for nominal GDP growth. Inflation automatically tends to fall in the early stages of recovery from a recession, and nothing is gained, and much harm is done, by maintaining a tight-money policy after nominal GDP growth has fallen below the target range. That’s the great, and still unlearned, lesson of monetary policy.

The bread and butter of economics is demand and supply. The basic idea of a demand function (or a demand curve) is to describe a relationship between the price at which a given product, commodity or service can be bought and the quantity that will bought by some individual. The standard assumption is that the quantity demanded increases as the price falls, so that the demand curve is downward-sloping, but not much more can be said about the shape of a demand curve unless special assumptions are made about the individual’s preferences.

Demand curves aren’t natural phenomena with concrete existence; they are hypothetical or notional constructs pertaining to individual preferences. To pass from individual demands to a market demand for a product, commodity or service requires another conceptual process summing the quantities demanded by each individual at any given price. The conceptual process is never actually performed, so the downward-sloping market demand curve is just presumed, not observed as a fact of nature.

The summation process required to pass from individual demands to a market demand implies that the quantity demanded at any price is the quantity demanded when each individual pays exactly the same price that every other demander pays. At a price of $10/widget, the widget demand curve tells us how many widgets would be purchased if every purchaser in the market can buy as much as desired at $10/widget. If some customers can buy at $10/widget while others have to pay $20/widget or some can’t buy any widgets at any price, then the quantity of widgets actually bought will not equal the quantity on the hypothetical widget demand curve corresponding to $10/widget.

Similar reasoning underlies the supply function or supply curve for any product, commodity or service. The market supply curve is built up from the preferences and costs of individuals and firms and represents the amount of a product, commodity or service that would be willing to offer for sale at different prices. The market supply curve is the result of a conceptual summation process that adds up the amounts that would be hypothetically be offered for sale by every agent at different prices.

The point of this pedantry is to emphasize the that the demand and supply curves we use are drawn on the assumption that a single uniform market price prevails in every market and that all demanders and suppliers can trade without limit at those prices and their trading plans are fully executed. This is the equilibrium paradigm underlying the supply-demand analysis of econ 101.

Economists quite unself-consciously deploy supply-demand concepts to analyze labor markets in a variety of settings. Sometimes, if the labor market under analysis is limited to a particular trade or a particular skill or a particular geographic area, the supply-demand framework is reasonable and appropriate. But when applied to the aggregate labor market of the whole economy, the supply-demand framework is inappropriate, because the ceteris-paribus proviso (all prices other than the price of the product, commodity or service in question are held constant) attached to every supply-demand model is obviously violated.

Thoughtlessly applying a simple supply-demand model to analyze the labor market of an entire economy leads to the conclusion that widespread unemployment, when some workers are unemployed, but would have accepted employment offers at wages that comparably skilled workers are actually receiving, implies that wages are above the market-clearing wage level consistent with full employment.

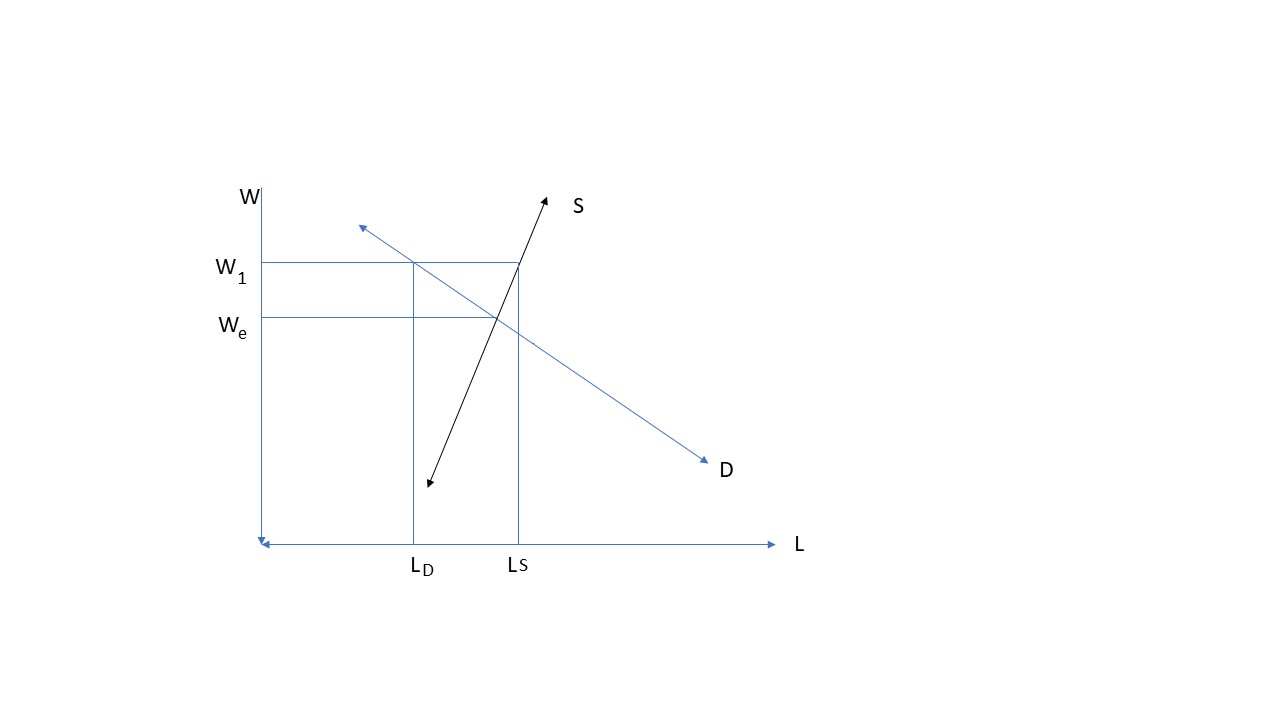

The attached diagram for simplest version of this analysis. The market wage (W1) is higher than the equilibrium wage (We) at which all workers willing to accept that wage could be employed. The difference between the number of workers seeking employment at the market wage (LS) and the number of workers that employers seek to hire (LD) measures the amount of unemployment. According to this analysis, unemployment would be eliminated if the market wage fell from W1 to We.

Applying supply-demand analysis to aggregate unemployment fails on two levels. First, workers clearly are unable to execute their plans to offer their labor services at the wage at which other workers are employed, so individual workers are off their supply curves. Second, it is impossible to assume, supply-demand analysis requires, that all other prices and incomes remain constant so that the demand and supply curves do not move as wages and employment change. When multiple variables are mutually interdependent and simultaneously determined, the analysis of just two variables (wages and employment) cannot be isolated from the rest of the system. Focusing on the wage as the variable that needs to change to restore full employment is an example of the tunnel vision.

Keynes rejected the idea that economy-wide unemployment could be eliminated by cutting wages. Although Keynes’s argument against wage cuts as a cure for unemployment was flawed, he did have at least an intuitive grasp of the basic weakness in the argument for wage cuts: that high aggregate unemployment is not usefully analyzed as a symptom of excessive wages. To explain why wage cuts aren’t the cure for high unemployment, Keynes introduced a distinction between voluntary and involuntary unemployment.

Forty years later, Robert Lucas began his effort — not the first such effort, but by far the most successful — to discredit the concept of involuntary unemployment. Here’s an early example:

Keynes [hypothesized] that measured unemployment can be decomposed into two distinct components: ‘voluntary’ (or frictional) and ‘involuntary’, with full employment then identified as the level prevailing when involuntary employment equals zero. It seems appropriate, then, to begin by reviewing Keynes’ reasons for introducing this distinction in the first place. . . .

Accepting the necessity of a distinction between explanations for normal and cyclical unemployment does not, however, compel one to identify the first as voluntary and the second as involuntary, as Keynes goes on to do. This terminology suggests that the key to the distinction lies in some difference in the way two different types of unemployment are perceived by workers. Now in the first place, the distinction we are after concerns sources of unemployment, not differentiated types. . . .[O]ne may classify motives for holding money without imagining that anyone can subdivide his own cash holdings into “transactions balances,” “precautionary balances”, and so forth. The recognition that one needs to distinguish among sources of unemployment does not in any way imply that one needs to distinguish among types.

Nor is there any evident reason why one would want to draw this distinction. Certainly the more one thinks about the decision problem facing individual workers and firms the less sense this distinction makes. The worker who loses a good job in prosperous time does not volunteer to be in this situation: he has suffered a capital loss. Similarly, the firm which loses an experienced employee in depressed times suffers an undesirable capital loss. Nevertheless, the unemployed worker at any time can always find some job at once, and a firm can always fill a vacancy instantaneously. That neither typically does so by choice is not difficult to understand given the quality of the jobs and the employees which are easiest to find. Thus there is an involuntary element in all unemployment, in the sense that no one chooses bad luck over good; there is also a voluntary element in all unemployment, in the sense that however miserable one’s current work options, one can always choose to accept them.

Lucas, Studies in Business Cycle Theory, pp. 241-43

Consider this revision of Lucas’s argument:

The expressway driver who is slowed down in a traffic jam does not volunteer to be in this situation; he has suffered a waste of his time. Nevertheless, the driver can get off the expressway at the next exit to find an alternate route. Thus, there is an involuntary element in every traffic jam, in the sense that no one chooses to waste time; there is also a voluntary element in all traffic jams, in the sense that however stuck one is in traffic, one can always take the next exit on the expressway.

What is lost on Lucas is that, for an individual worker, taking a wage cut to avoid being laid off by the employer accomplishes nothing, because the willingness of a single worker to accept a wage cut would not induce the employer to increase output and employment. Unless all workers agreed to take wage cuts, a wage cut to one employee would have not cause the employer to reconsider its plan to reduce in the face of declining demand for its product. Only the collective offer of all workers to accept a wage cut would induce an output response by the employer and a decision not to lay off part of its work force.

But even a collective offer by all workers to accept a wage cut would be unlikely to avoid an output reduction and layoffs. Consider a simple case in which the demand for the employer’s output declines by a third. Suppose the employer’s marginal cost of output is half the selling price (implying a demand elasticity of -2). Assume that demand is linear. With no change in its marginal cost, the firm would reduce output by a third, presumably laying off up to a third of its employees. Could workers avoid the layoffs by accepting lower wages to enable the firm to reduce its price? Or asked in another way, how much would marginal cost have to fall for the firm not to reduce output after the demand reduction?

Working out the algebra, one finds that for the firm to keep producing as much after a one-third reduction in demand, the firm’s marginal cost would have to fall by two-thirds, a decline that could only be achieved by a radical reduction in labor costs. This is surely an oversimplified view of the alternatives available to workers and employers, but the point is that workers facing a layoff after the demand for the product they produce have almost no ability to remain employed even by collectively accepting a wage cut.

That conclusion applies a fortiori when decisions whether to accept a wage cut are left to individual workers, because the willingness of workers individually to accept a wage cut is irrelevant to their chances of retaining their jobs. Being laid off because of decline in the demand for the product a worker is producing is a much different situation from being laid off, because a worker’s employer is shifting to a new technology for which the workers lack the requisite skills, and can remain employed only by accepting re-assignment to a lower-paying job.

Let’s follow Lucas a bit further:

Keynes, in chapter 2, deals with the situation facing an individual unemployed worker by evasion and wordplay only. Sentences like “more labor would, as a rule, be forthcoming at the existing money wage if it were demanded” are used again and again as though, from the point of view of a jobless worker, it is unambiguous what is meant by “the existing money wage.” Unless we define an individual’s wage rate as the price someone else is willing to pay him for his labor (in which case Keynes’s assertion is defined to be false to be false), what is it?

Lucas, Id.

I must admit that, reading this passage again perhaps 30 or more years after my first reading, I’m astonished that I could have once read it without astonishment. Lucas gives the game away by accusing Keynes of engaging in evasion and wordplay before embarking himself on sustained evasion and wordplay. The meaning of the “existing money wage” is hardly ambiguous, it is the money wage the unemployed worker was receiving before losing his job and the wage that his fellow workers, who remain employed, continue to receive.

Is Lucas suggesting that the reason that the worker lost his job while his fellow workers who did not lose theirs is that the value of his marginal product fell but the value of his co-workers’ marginal product did not? Perhaps, but that would only add to my astonishment. At the current wage, employers had to reduce the number of workers until their marginal product was high enough for the employer to continue employing them. That was not necessarily, and certainly not primarily, because some workers were more capable than those that were laid off.

The fact is, I think, that Keynes wanted to get labor markets out of the way in chapter 2 so that he could get on to the demand theory which really interested him.

More wordplay. Is it fact or opinion? Well, he says that thinks it’s a fact. In other words, it’s really an opinion.

This is surely understandable, but what is the excuse for letting his carelessly drawn distinction between voluntary and involuntary unemployment dominate aggregative thinking on labor markets for the forty years following?

Mr. Keynes, really, what is your excuse for being such an awful human being?

[I]nvoluntary unemployment is not a fact or a phenomenon which it is the task of theorists to explain. It is, on the contrary, a theoretical construct which Keynes introduced in the hope it would be helpful in discovering a correct explanation for a genuine phenomenon: large-scale fluctuations in measured, total unemployment. Is it the task of modern theoretical economics to ‘explain’ the theoretical constructs of our predecessor, whether or not they have proved fruitful? I hope not, for a surer route to sterility could scarcely be imagined.

Lucas, Id.

Let’s rewrite this paragraph with a few strategic word substitutions:

Heliocentrism is not a fact or phenomenon which it is the task of theorists to explain. It is, on the contrary, a theoretical construct which Copernicus introduced in the hope it would be helpful in discovering a correct explanation for a genuine phenomenon the observed movement of the planets in the heavens. Is it the task of modern theoretical physics to “explain” the theoretical constructs of our predecessors, whether or not they have proved fruitful? I hope not, for a surer route to sterility could scarcely be imagined.

Copernicus died in 1542 shortly before his work on heliocentrism was published. Galileo’s works on heliocentrism were not published until 1610 almost 70 years after Copernicus published his work. So, under Lucas’s forty-year time limit, Galileo had no business trying to explain Copernican heliocentrism which had still not yet proven fruitful. Moreover, even after Galileo had published his works, geocentric models were providing predictions of planetary motion as good as, if not better than, the heliocentric models, so decisive empirical evidence in favor of heliocentrism was still lacking. Not until Newton published his great work 70 years after Galileo, and 140 years after Copernicus, was heliocentrism finally accepted as fact.

In summary, it does not appear possible, even in principle, to classify individual unemployed people as either voluntarily or involuntarily unemployed depending on the characteristics of the decision problem they face. One cannot, even conceptually, arrive at a usable definition of full employment

Lucas, Id.

Belying his claim to be introducing scientific rigor into macroeocnomics, Lucas restorts to an extended scholastic inquiry into whether an unemployed worker can really ever be unemployed involuntarily. Based on his scholastic inquiry into the nature of volunatriness, Lucas declares that Keynes was mistaken because would not accept the discipline of optimization and equilibrium. But Lucas’s insistence on the discipline of optimization and equilibrium is misplaced unless he can provide an actual mechanism whereby the notional optimization of a single agent can be reconciled with notional optimization of other individuals.

It was his inability to provide any explanation of the mechanism whereby the notional optimization of individual agents can be reconciled with the notional optimizations of other individual agents that led Lucas to resort to rational expectations to circumvent the need for such a mechanism. He successfully persuaded the economics profession that evading the need to explain such a reconciliation mechanism, the profession would not be shirking their explanatory duty, but would merely be fulfilling their methodological obligation to uphold the neoclassical axioms of rationality and optimization neatly subsumed under the heading of microfoundations.

Rational expectations and microfoundations provided the pretext that could justify or at least excuse the absence of any explanation of how an equilibrium is reached and maintained by assuming that the rational expectations assumption is an adequate substitute for the Walrasian auctioneer, so that each and every agent, using the common knowledge (and only the common knowledge) available to all agents, would reliably anticipate the equilibrium price vector prevailing throughout their infinite lives, thereby guaranteeing continuous equilibrium and consistency of all optimal plans. That feat having been securely accomplished, it was but a small and convenient step to collapse the multitude of individual agents into a single representative agent, so that the virtue of submitting to the discipline of optimization could find its just and fitting reward.

The standard neoclassical models of economics textbooks typically assume full information and perfect competition. But these assumptions are, or ought to be, just the starting point, not the end, of analysis. Recognizing when and why these assumptions need to be relaxed and what empirical implications follow from relaxing those assumptions is how economists gain practical insight into, and understanding of, complex economic phenomena.

Since the late eighteenth or early nineteenth century, much, if not most, of the financial instruments actually used as media of exchange (money) have been produced by private financial institutions (usually commercial banks); the amount of money that is privately produced is governed by the revenue generated and the cost incurred by creating money.

The standard textbook model of international monetary adjustment under the gold standard (or any fixed-exchange rate system), the price-specie-flow mechanism, introduced by David Hume mischaracterized the adjustment mechanism by overlooking that the prices of tradable goods in any country are constrained by the prices of those tradable goods in other countries. That arbitrage constraint on the prices of tradable goods in any country prevents price levels in different currency areas from deviating, regardless of local changes in the quantity of money, from a common international level.

The Great Depression was caused by a rapid appreciation of gold resulting from the increasing monetary demand for gold occasioned by the restoration of the international gold standard in the 1920s after the demonetization of gold in World War I.

If the expected rate of deflation exceeds the real rate of interest, real-asset prices crash and economies collapse.

The primary concern of macroeconomics as a field of economics is to explain systemic failures of coordination that lead to significant lapses from full employment.

Lapses from full employment result from substantial and widespread disappointment of agents’ expectations of future prices.

The only – or at least the best — systematic analytical approach to the study of such lapses is the temporary-equilibrium approach introduced by Hicks in Value and Capital.

F. A. Hayek entitled his 1974 Nobel Lecture whose principal theme was to attack the simple notion that the long-observed correlation between aggregate demand and employment was a reliable basis for conducting macroeconomic policy, “The Pretence of Knowledge.” Reiterating an argument that he had made over 40 years earlier about the transitory stimulus provided to profits and production by monetary expansion, Hayek was informally anticipating the argument that Robert Lucas famously repackaged two years later in his famous critique of econometric policy evaluation. Hayek’s argument hinged on a distinction between “phenomena of unorganized complexity” and phenomena of organized complexity.” Statistical relationships or correlations between phenomena of disorganized complexity may be relied upon to persist, but observed statistical correlations displayed by phenomena of organized complexity cannot be relied upon without detailed knowledge of the individual elements that constitute the system. It was the facile assumption that observed statistical correlations in systems of organized complexity can be uncritically relied upon in making policy decisions that Hayek dismissed as merely the pretense of knowledge.

Adopting many of Hayek’s complaints about macroeconomic theory, Lucas founded his New Classical approach to macroeconomics on a methodological principle that all macroeconomic models be grounded in the axioms of neoclassical economic theory as articulated in the canonical Arrow-Debreu-McKenzie models of general equilibrium models. Without such grounding in neoclassical axioms and explicit formal derivations of theorems from those axioms, Lucas maintained that macroeconomics could not be considered truly scientific. Forty years of Keynesian macroeconomics were, in Lucas’s view, largely pre-scientific or pseudo-scientific, because they lacked satisfactory microfoundations.

Lucas’s methodological program for macroeconomics was thus based on two basic principles: reductionism and formalism. First, all macroeconomic models not only had to be consistent with rational individual decisions, they had to be reduced to those choices. Second, all the propositions of macroeconomic models had to be explicitly derived from the formal definitions and axioms of neoclassical theory. Lucas demanded nothing less than the explicit assumption individual rationality in every macroeconomic model and that all decisions by agents in a macroeconomic model be individually rational.

In practice, implementing Lucasian methodological principles required that in any macroeconomic model all agents’ decisions be derived within an explicit optimization problem. However, as Hayek had himself shown in his early studies of business cycles and intertemporal equilibrium, individual optimization in the standard Walrasian framework, within which Lucas wished to embed macroeconomic theory, is possible only if all agents are optimizing simultaneously, all individual decisions being conditional on the decisions of other agents. Individual optimization can only be solved simultaneously for all agents, not individually in isolation.

The difficulty of solving a macroeconomic equilibrium model for the simultaneous optimal decisions of all the agents in the model led Lucas and his associates and followers to a strategic simplification: reducing the entire model to a representative agent. The optimal choices of a single agent would then embody the consumption and production decisions of all agents in the model.

The staggering simplification involved in reducing a purported macroeconomic model to a representative agent is obvious on its face, but the sleight of hand being performed deserves explicit attention. The existence of an equilibrium solution to the neoclassical system of equations was assumed, based on faulty reasoning by Walras, Fisher and Pareto who simply counted equations and unknowns. A rigorous proof of existence was only provided by Abraham Wald in 1936 and subsequently in more general form by Arrow, Debreu and McKenzie, working independently, in the 1950s. But proving the existence of a solution to the system of equations does not establish that an actual neoclassical economy would, in fact, converge on such an equilibrium.

Neoclassical theory was and remains silent about the process whereby equilibrium is, or could be, reached. The Marshallian branch of neoclassical theory, focusing on equilibrium in individual markets rather than the systemic equilibrium, is often thought to provide an account of how equilibrium is arrived at, but the Marshallian partial-equilibrium analysis presumes that all markets and prices except the price in the single market under analysis, are in a state of equilibrium. So the Marshallian approach provides no more explanation of a process by which a set of equilibrium prices for an entire economy is, or could be, reached than the Walrasian approach.

Lucasian methodology has thus led to substituting a single-agent model for an actual macroeconomic model. It does so on the premise that an economic system operates as if it were in a state of general equilibrium. The factual basis for this premise apparently that it is possible, using versions of a suitable model with calibrated coefficients, to account for observed aggregate time series of consumption, investment, national income, and employment. But the time series derived from these models are derived by attributing all observed variations in national income to unexplained shocks in productivity, so that the explanation provided is in fact an ex-post rationalization of the observed variations not an explanation of those variations.

Nor did Lucasian methodology have a theoretical basis in received neoclassical theory. In a famous 1960 paper “Towards a Theory of Price Adjustment,” Kenneth Arrow identified the explanatory gap in neoclassical theory: the absence of a theory of price change in competitive markets in which every agent is a price taker. The existence of an equilibrium does not entail that the equilibrium will be, or is even likely to be, found. The notion that price flexibility is somehow a guarantee that market adjustments reliably lead to an equilibrium outcome is a presumption or a preconception, not the result of rigorous analysis.

However, Lucas used the concept of rational expectations, which originally meant no more than that agents try to use all available information to anticipate future prices, to make the concept of equilibrium, notwithstanding its inherent implausibility, a methodological necessity. A rational-expectations equilibrium was methodologically necessary and ruthlessly enforced on researchers, because it was presumed to be entailed by the neoclassical assumption of rationality. Lucasian methodology transformed rational expectations into the proposition that all agents form identical, and correct, expectations of future prices based on the same available information (common knowledge). Because all agents reach the same, correct expectations of future prices, general equilibrium is continuously achieved, except at intermittent moments when new information arrives and is used by agents to revise their expectations.

In his Nobel Lecture, Hayek decried a pretense of knowledge about correlations between macroeconomic time series that lack a foundation in the deeper structural relationships between those related time series. Without an understanding of the deeper structural relationships between those time series, observed correlations cannot be relied on when formulating economic policies. Lucas’s own famous critique echoed the message of Hayek’s lecture.

The search for microfoundations was always a natural and commendable endeavor. Scientists naturally try to reduce higher-level theories to deeper and more fundamental principles. But the endeavor ought to be conducted as a theoretical and empirical endeavor. If successful, the reduction of the higher-level theory to a deeper theory will provide insight and disclose new empirical implications to both the higher-level and the deeper theories. But reduction by methodological fiat accomplishes neither and discourages the research that might actually achieve a theoretical reduction of a higher-level theory to a deeper one. Similarly, formalism can provide important insights into the structure of theories and disclose gaps or mistakes the reasoning underlying the theories. But most important theories, even in pure mathematics, start out as informal theories that only gradually become axiomatized as logical gaps and ambiguities in the theories are discovered and filled or refined.

The resort to the reductionist and formalist methodological imperatives with which Lucas and his followers have justified their pretentions to scientific prestige and authority, and have used that authority to compel compliance with those imperatives, only belie their pretensions.

[[Update 8/15/2021: I’m about to post a new post on the decision to close the gold window rather than the effects of the decision to freeze wages and prices. The new post is longer than this one and covers a different set of issues, but the two are complementary and readers may find both of interest]

[Update 8/15/2019: It seems appropriate to republish this post originally published about 40 days after I started blogging. I have made a few small changes and inserted a few comments to reflect my improved understanding of certain concepts like “sterilization” that I was uncritically accepting. I actually have learned a thing or two in the eight plus years that I’ve been blogging. I am grateful to all my readers — both those who agreed and those who disagreed — for challenging me and inspiring me to keep thinking critically. It wasn’t easy, but we did survive August 15, 1971. Let’s hope we survive August 15, 2019.]

August 15, 1971 may not exactly be a day that will live in infamy, but it is hardly a day to celebrate 40 years later. It was the day on which one of the most cynical Presidents in American history committed one of his most cynical acts: violating solemn promises undertaken many times previously, both before and after his election as President, Richard Nixon declared a 90-day freeze on wages and prices. Nixon also announced the closing of the gold window at the US Treasury, severing the last shred of a link between gold and the dollar. Interestingly, the current (August 13th, 2011) Economist (Buttonwood column) and Forbes (Charles Kadlec op-ed) and today’s Wall Street Journal (Lewis Lehrman op-ed) mark the anniversary with critical commentaries on Nixon’s action ruefully focusing on the baleful consequences of breaking the link to gold, while barely mentioning the 90-day freeze that became the prelude to the comprehensive wage and price controls imposed after the freeze expired.

Of the two events, the wage and price freeze and subsequent controls had by far the more adverse consequences, the closing of the gold window merely ratifying the demise of a gold standard that long since had ceased to function as it had for much of the 19th and early 20th centuries. In contrast to the final break with gold, no economic necessity or even a coherent economic argument on the merits lay behind the decision to impose a wage and price freeze, notwithstanding the ex-post rationalizations offered by Nixon’s economic advisers, including such estimable figures as Herbert Stein, Paul McKracken, and George Schultz, who surely knew better, but somehow were persuaded to fall into line behind a policy of massive, breathtaking, intervention into private market transactions.

The argument for closing the gold window was that the official gold peg of $35 an ounce was probably at least 10-20% below any realistic estimate of the true market value of gold at the time, making it impossible to reestablish the old parity as an economically meaningful price without imposing an intolerable deflation on the world economy. An alternative response might have been to officially devalue the dollar to something like the market value of gold $40-42 an ounce. But to have done so would merely have demonstrated that the official price of gold was a policy instrument subject to the whims of the US monetary authorities, undermining faith in the viability of a gold standard. In the event, an attempt to patch together the Bretton Woods System (the Smithsonian Agreement of December 1971) based on an official $38 an ounce peg was made, but it quickly became obvious that a new monetary system based on any form of gold convertibility could no longer survive.

How did the $35 an ounce price became unsustainable barely 25 years after the Bretton Woods System was created? The problem that emerged within a few years of its inception was that the main trading partners of the US systematically kept their own currencies undervalued in terms of the dollar, promoting their exports while sterilizing the consequent dollar inflow, allowing neither sufficient domestic inflation nor sufficient exchange-rate appreciation to eliminate the overvaluation of their currencies against the dollar. [DG 8/15/19: “sterilization” is a misleading term because it implies that persistent gold or dollar inflows just happen randomly; the persistent inflow occur only because they are induced by a persistent increased demand for reserves or insufficient creation of cash.] After a burst of inflation in the Korean War, the Fed’s tight monetary policy and a persistently overvalued exchange rate kept US inflation low at the cost of sluggish growth and three recessions between 1953 and 1960. It was not until the Kennedy administration came into office on a pledge to get the country moving again that the Fed was pressured to loosen monetary policy, initiating the long boom of the 1960s some three years before the Kennedy tax cuts were posthumously enacted in 1964.

Monetary expansion by the Fed reduced the relative overvaluation of the dollar in terms of other currencies, but the increasing export of dollars left the $35 an ounce peg increasingly dependent on the willingness of foreign government to hold dollars. However, President Charles de Gaulle of France, having overcome domestic opposition to his rule, felt secure enough to assert [his conception of] French interests against the US, resuming the traditional French policy of accumulating physical gold reserves rather than mere claims on gold physically held elsewhere. By 1967 the London gold pool, a central bank cartel acting to control the price of gold in the London gold market, was collapsing, as France withdrew from the cartel, demanding that gold be shipped to Paris from New York. In 1968, unable to hold down the market price of gold any longer, the US and other central banks let the gold price rise above the official price, but agreed to conduct official transactions among themselves at the official price of $35 an ounce. As market prices for gold, driven by US monetary expansion, inched steadily higher, the incentives for central banks to demand gold from the US at the official price became too strong to contain, so that the system was on the verge of collapse when Nixon acknowledged the inevitable and closed the gold window rather than allow depletion of US gold holdings.

Assertions that the Bretton Woods system could somehow have been saved simply ignore the economic reality that by 1971 the Bretton Woods System was broken beyond repair, or at least beyond any repair that could have been effected at a tolerable cost.

But Nixon clearly had another motivation in his August 15 announcement, less than 15 months before the next Presidential election. It was in effect the opening shot of his reelection campaign. Remembering all too well that he lost the 1960 election to John Kennedy because the Fed had not provided enough monetary stimulus to cut short the 1960-61 recession, Nixon had appointed his long-time economic adviser, Arthur Burns to replace William McChesney Martin as chairman of the Fed in 1970. A mild tightening of monetary policy in 1969 as inflation was rising above a 5% annual rate, had produced a recession in late 1969 and early 1970, without providing much relief from inflation. Burns eased policy enough to allow a mild recovery, but the economy seemed to be suffering the worst of both worlds — inflation still near 4 percent and unemployment at what then seemed an unacceptably high level of almost 6 percent. [For more on Burns and his deplorable role in all of this see this post.]

With an election looming ever closer on the horizon, Nixon in the summer of 1971 became consumed by the political imperative of speeding up the recovery. Meanwhile a Democratic Congress, assuming that Nixon really did mean his promises never to impose wage and price controls to stop inflation, began clamoring for controls as the way to stop inflation without the pain of a recession, even authorizing the President to impose controls, a dare they never dreamed he would accept. Arthur Burns, himself, perhaps unwittingly [I was being too kind], provided support for such a step by voicing frustration that inflation persisted in the face of a recession and high unemployment, suggesting that the old rules of economics were no longer operating as they once had. He even offered vague support for what was then called an incomes policy, generally understood as an informal attempt to bring down inflation by announcing a target for wage increases corresponding to productivity gains, thereby eliminating the need for businesses to raise prices to compensate for increased labor costs. What such proposals usually ignored was the necessity for a monetary policy that would limit the growth of total spending sufficiently to limit the growth of wage incomes to the desired target. [On incomes policies and how they might work if they were properly understood see this post.]

Having been persuaded that there was no acceptable alternative to closing the gold window — from Nixon’s perspective and from that of most conventional politicians, a painfully unpleasant admission of US weakness in the face of its enemies (all this was occurring at the height of the Vietnam War and the antiwar protests) – Nixon decided that he could now combine that decision, sugar-coated with an aggressive attack on international currency speculators and a protectionist 10% duty on imports into the United States, with the even more radical measure of a wage-price freeze to be followed by a longer-lasting program to control price increases, thereby snatching the most powerful and popular economic proposal of the Democrats right from under their noses. Meanwhile, with the inflation threat neutralized, Arthur Burns could be pressured mercilessly to increase the rate of monetary expansion, ensuring that Nixon could stand for reelection in the middle of an economic boom.

But just as Nixon’s electoral triumph fell apart because of his Watergate fiasco, his economic success fell apart when an inflationary monetary policy combined with wage-and-price controls to produce increasing dislocations, shortages and inefficiencies, gradually sapping the strength of an economic recovery fueled by excess demand rather than increasing productivity. Because broad based, as opposed to narrowly targeted, price controls tend to be more popular before they are imposed than after (as too many expectations about favorable regulatory treatment are disappointed), the vast majority of controls were allowed to lapse when the original grant of Congressional authority to control prices expired in April 1974.

Already by the summer of 1973, shortages of gasoline and other petroleum products were becoming commonplace, and shortages of heating oil and natural gas had been widely predicted for the winter of 1973-74. But in October 1973 in the wake of the Yom Kippur War and the imposition of an Arab Oil Embargo against the United States and other Western countries sympathetic to Israel, the shortages turned into the first “Energy Crisis.” A Democratic Congress and the Nixon Administration sprang into action, enacting special legislation to allow controls to be kept on petroleum products of all sorts together with emergency authority to authorize the government to allocate products in short supply.

It still amazes me that almost all the dislocations manifested after the embargo and the associated energy crisis were attributed to excessive consumption of oil and petroleum products in general or to excessive dependence on imports, as if any of the shortages and dislocations would have occurred in the absence of price controls. And hardly anyone realizes that price controls tend to drive the prices of whatever portion of the supply is exempt from control even higher than they would have risen in the absence of any controls.

About ten years after the first energy crisis, I published a book in which I tried to explain how all the dislocations that emerged from the Arab oil embargo and the 1978-79 crisis following the Iranian Revolution were attributable to the price controls first imposed by Richard Nixon on August 15, 1971. But the connection between the energy crisis in all its ramifications and the Nixonian price controls unfortunately remains largely overlooked and ignored to this day. If there is reason to reflect on what happened forty years ago on this date, it surely is for that reason and not because Nixon pulled the plug on a gold standard that had not been functioning for years.

UPDATE: Re-upping this slightly revised post from July 11, 2011

Paul Krugman recently gave a lecture “Mr. Keynes and the Moderns” (a play on the title of the most influential article ever written about The General Theory, “Mr. Keynes and the Classics,” by another Nobel laureate J. R. Hicks) at a conference in Cambridge, England commemorating the publication of Keynes’s General Theory 75 years ago. Scott Sumner and Nick Rowe, among others, have already commented on his lecture. Coincidentally, in my previous posting, I discussed the views of Sumner and Krugman on the zero-interest lower bound, a topic that figures heavily in Krugman’s discussion of Keynes and his relevance for our current difficulties. (I note in passing that Krugman credits Brad Delong for applying the term “Little Depression” to those difficulties, a term that I thought I had invented, but, oh well, I am happy to share the credit with Brad).

In my earlier posting, I mentioned that Keynes’s, slightly older, colleague A. C. Pigou responded to the zero-interest lower bound in his review of The General Theory. In a way, the response enhanced Pigou’s reputation, attaching his name to one of the most famous “effects” in the history of economics, but it made no dent in the Keynesian Revolution. I also referred to “the layers upon layers of interesting personal and historical dynamics lying beneath the surface of Pigou’s review of Keynes.” One large element of those dynamics was that Keynes chose to make, not Hayek or Robbins, not French devotees of the gold standard, not American laissez-faire ideologues, but Pigou, a left-of-center social reformer, who in the early 1930s had co-authored with Keynes a famous letter advocating increased public-works spending to combat unemployment, the main target of his immense rhetorical powers and polemical invective. The first paragraph of Pigou’s review reveals just how deeply Keynes’s onslaught had wounded Pigou.

When in 1919, he wrote The Economic Consequences of the Peace, Mr. Keynes did a good day’s work for the world, in helping it back towards sanity. But he did a bad day’s work for himself as an economist. For he discovered then, and his sub-conscious mind has not been able to forget since, that the best way to win attention for one’s own ideas is to present them in a matrix of sarcastic comment upon other people. This method has long been a routine one among political pamphleteers. It is less appropriate, and fortunately less common, in scientific discussion. Einstein actually did for Physics what Mr. Keynes believes himself to have done for Economics. He developed a far-reaching generalization, under which Newton’s results can be subsumed as a special case. But he did not, in announcing his discovery, insinuate, through carefully barbed sentences, that Newton and those who had hitherto followed his lead were a gang of incompetent bunglers. The example is illustrious: but Mr. Keynes has not followed it. The general tone de haut en bas and the patronage extended to his old master Marshall are particularly to be regretted. It is not by this manner of writing that his desire to convince his fellow economists is best promoted.

Krugman acknowledges Keynes’s shady scholarship (“I know that there’s dispute about whether Keynes was fair in characterizing the classical economists in this way”), only to absolve him of blame. He then uses Keynes’s example to attack “modern economists” who deny that a failure of aggregate demand can cause of mass unemployment, offering up John Cochrane and Niall Ferguson as examples, even though Ferguson is a historian not an economist.

Krugman also addresses Robert Barro’s assertion that Keynes’s explanation for high unemployment was that wages and prices were stuck at levels too high to allow full employment, a problem easily solvable, in Barro’s view, by monetary expansion. Although plainly annoyed by Barro’s attempt to trivialize Keynes’s contribution, Krugman never addresses the point squarely, preferring instead to justify Keynes’s frustration with those (conveniently nameless) “classical economists.”

Keynes’s critique of the classical economists was that they had failed to grasp how everything changes when you allow for the fact that output may be demand-constrained.

Not so, as I pointed out in my first post. Frederick Lavington, an even more orthodox disciple than Pigou of Marshall, had no trouble understanding that “the inactivity of all is the cause of the inactivity of each.” It was Keynes who failed to see that the failure of demand was equally a failure of supply.

They mistook accounting identities for causal relationships, believing in particular that because spending must equal income, supply creates its own demand and desired savings are automatically invested.

Supply does create its own demand when economic agents succeed in executing their plans to supply; it is when, owing to their incorrect and inconsistent expectations about future prices, economic agents fail to execute their plans to supply, that both supply and demand start to contract. Lavington understood that; Pigou understood that. Keynes understood it, too, but believing that his new way of understanding how contractions are caused was superior to that of his predecessors, he felt justified in misrepresenting their views, and attributing to them a caricature of Say’s Law that they would never have taken seriously.

And to praise Keynes for understanding the difference between accounting identities and causal relationships that befuddled his predecessors is almost perverse, as Keynes’s notorious confusion about whether the equality of savings and investment is an equilibrium condition or an accounting identity was pointed out by Dennis Robertson, Ralph Hawtrey and Gottfried Haberler within a year after The General Theory was published. To quote Robertson:

(Mr. Keynes’s critics) have merely maintained that he has so framed his definition that Amount Saved and Amount Invested are identical; that it therefore makes no sense even to inquire what the force is which “ensures equality” between them; and that since the identity holds whether money income is constant or changing, and, if it is changing, whether real income is changing proportionately, or not at all, this way of putting things does not seem to be a very suitable instrument for the analysis of economic change.

It just so happens that in 1925, Keynes, in one of his greatest pieces of sustained, and almost crushing sarcasm, The Economic Consequences of Mr. Churchill, offered an explanation of high unemployment exactly the same as that attributed to Keynes by Barro. Churchill’s decision to restore the convertibility of sterling to gold at the prewar parity meant that a further deflation of at least 10 percent in wages and prices would be necessary to restore equilibrium. Keynes felt that the human cost of that deflation would be intolerable, and held Churchill responsible for it.

Of course Keynes in 1925 was not yet the Keynes of The General Theory. But what historical facts of the 10 years following Britain’s restoration of the gold standard in 1925 at the prewar parity cannot be explained with the theoretical resources available in 1925? The deflation that began in England in 1925 had been predicted by Keynes. The even worse deflation that began in 1929 had been predicted by Ralph Hawtrey and Gustav Cassel soon after World War I ended, if a way could not be found to limit the demand for gold by countries, rejoining the gold standard in aftermath of the war. The United States, holding 40 percent of the world’s monetary gold reserves, might have accommodated that demand by allowing some of its reserves to be exported. But obsession with breaking a supposed stock-market bubble in 1928-29 led the Fed to tighten its policy even as the international demand for gold was increasing rapidly, as Germany, France and many other countries went back on the gold standard, producing the international credit crisis and deflation of 1929-31. Recovery came not from Keynesian policies, but from abandoning the gold standard, thereby eliminating the deflationary pressure implicit in a rapidly rising demand for gold with a more or less fixed total supply.

Keynesian stories about liquidity traps and Monetarist stories about bank failures are epiphenomena obscuring rather than illuminating the true picture of what was happening. The story of the Little Depression is similar in many ways, except the source of monetary tightness was not the gold standard, but a monetary regime that focused attention on rising price inflation in 2008 when the appropriate indicator, wage inflation, had already started to decline.

I indicated in my first posting on Tuesday that I was going to comment on some recent comparisons between the current anemic recovery and earlier more robust recoveries since World War II. The comparison that I want to perform involves some simple econometrics, and it is taking longer than anticipated to iron out the little kinks that I keep finding. So I will have to put off that discussion a while longer. As a diversion, I will follow up on a point that Scott Sumner made in discussing Paul Krugman’s reasoning for having favored fiscal policy over monetary policy to lead us out of the recession.

Scott’s focus is on the factual question whether it is really true, as Krugman and Michael Woodford have claimed, that a monetary authority, like, say, the Bank of Japan, may simply be unable to create the inflation expectations necessary to achieve equilibrium, given the zero-interest-rate lower bound, when the equilibrium real interest rate is less than zero. Scott counters that a more plausible explanation for the inability of the Bank of Japan to escape from a liquidity trap is that its aversion to inflation is so well-known that it becomes rational for the public to expect that the Bank of Japan would not permit the inflation necessary for equilibrium.

It seems that a lot of people have trouble understanding the idea that there can be conditions in which inflation — or, to be more precise, expected inflation — is necessary for a recovery from a depression. We have become so used to thinking of inflation as a costly and disruptive aspect of economic life, that the notion that inflation may be an integral element of an economic equilibrium goes very deeply against the grain of our intuition.

The theoretical background of this point actually goes back to A. C. Pigou (another famous Cambridge economist, Alfred Marshall’s successor) who, in his 1936 review of Keynes’s General Theory, referred to what he called Mr. Keynes’s vision of the day of judgment, namely, a situation in which, because of depressed entrepreneurial profit expectations or a high propensity to save, macro-equilibrium (the equality of savings and investment) would correspond to a level of income and output below the level consistent with full employment.

The “classical” or “orthodox” remedy to such a situation was to reduce the rate of interest, or, as the British say “Bank Rate” (as in “Magna Carta” with no definite article) at which the Bank of England lends to its customers (mainly banks). But if entrepreneurs are so pessimistic, or households so determined to save rather than consume, an equilibrium corresponding to a level of income and output consistent with full employment could, in Keynes’s ghastly vision, only come about with a negative interest rate. Now a zero interest rate in economics is a little bit like the speed of light in physics; all kinds of crazy things start to happen if you posit a negative interest rate and it seems inconsistent with the assumptions of rational behavior to assume that people would lend for a negative interest when they could simply hold the money already in their pockets. That’s why Pigou’s metaphor was so powerful. There are layers upon layers of interesting personal and historical dynamics lying beneath the surface of Pigou’s review of Keynes, but I won’t pursue that tangent here, tempting though it would be to go in that direction.

The conclusion that Keynes drew from his model is the one that we all were taught in our first course in macro and that Paul Krugman holds close to his heart, the government can come to the rescue by increasing its spending on whatever, thereby increasing aggregate demand, raising income and output up to the level consistent with full employment. But Pigou, whose own policy recommendations were not much different from those of Keynes, felt that Keynes had left out an important element of the model in his discussion. As a matter of logic, which to Pigou was as, or more important than, policy, an economy confronting Keynes’s day of judgment would not forever be stuck in “underemployment equilibrium” just because the rate of interest could not fall to the (negative) level required for full employment.

Rather, Pigou insisted, at least in theory, though not necessarily in practice, deflation, resulting from unemployed workers bidding down wages to gain employment, would raise the real value of the money supply (fixed in nominal terms in Keynes’s model) thereby generating a windfall to holders of money, inducing them to increase consumption, raising aggregate demand and eventually restoring full employment. Discussion of the theoretical validity and policy relevance of what came to be known as the Pigou effect (or, occasionally, as the Pigou-Haberler Effect, or even the Pigou-Haberler-Scitovsky effect) became a really big deal in macroeconomics in the 1940s and 1950s and was still being taught in the 1960s and 1970s.

What seems remarkable to me now about that whole episode is that the analysis simply left out the possibility that the zero-interest-rate lower bound becomes irrelevant if the expected rate of inflation exceeds the putative negative equilibrium real interest rate that would hypothetically generate a macro-equilibrium at a level of income and output consistent with full employment.

If only Pigou had corrected the logic of Keynes’s model by positing an expected rate of inflation greater than the negative real interest rate rather than positing a process of deflation to increase the real value of the money stock, how different would the course of history and the development of macroeconomics and monetary theory have been.

One economist who did think about the expected rate of inflation as an equilibrating variable in a macroeconomic model was one of my teachers, the late, great Earl Thompson, who introduced the idea of an equilibrium rate of inflation in his remarkable unpublished paper, “A Reformulation of Macreconomic Theory.” If inflation is an equilibrating variable, then it cannot make sense for monetary authorities to commit themselves to a single unvarying target for the rate of inflation. Under certain circumstances, macroeconomic equilibrium may be incompatible with a rate of inflation below some minimum level. Has it occurred to the inflation hawks on the FOMC and their supporters that the minimum rate of inflation consistent with equilibrium is above the 2 percent rate that Fed has now set as its policy goal?

One final point, which I am still trying to work out more coherently, is that it really may not be appropriate to think of the real rate of interest and the expected rate of inflation as being determined independently of each other. They clearly interact. As I point out in my paper “The Fisher Effect Under Deflationary Expectations,” increasing the expected rate of inflation when the real rate of interest is very low or negative tends to increase not just the nominal rate, but the real rate as well, by generating the positive feedback effects on income and employment that result when a depressed economy starts to expand.

I am an economist in the Washington DC area. My research and writing has been mostly on monetary economics and policy and the history of economics. In my book Free Banking and Monetary Reform, I argued for a non-Monetarist non-Keynesian approach to monetary policy, based on a theory of a competitive supply of money. Over the years, I have become increasingly impressed by the similarities between my approach and that of R. G. Hawtrey and hope to bring Hawtrey’s unduly neglected contributions to the attention of a wider audience.