Scott Sumner had a terrific post today. The title said it all, but the rest of it wasn’t bad either.

The stock market wants fast economic growth, and they want the Fed to think economic growth is slow

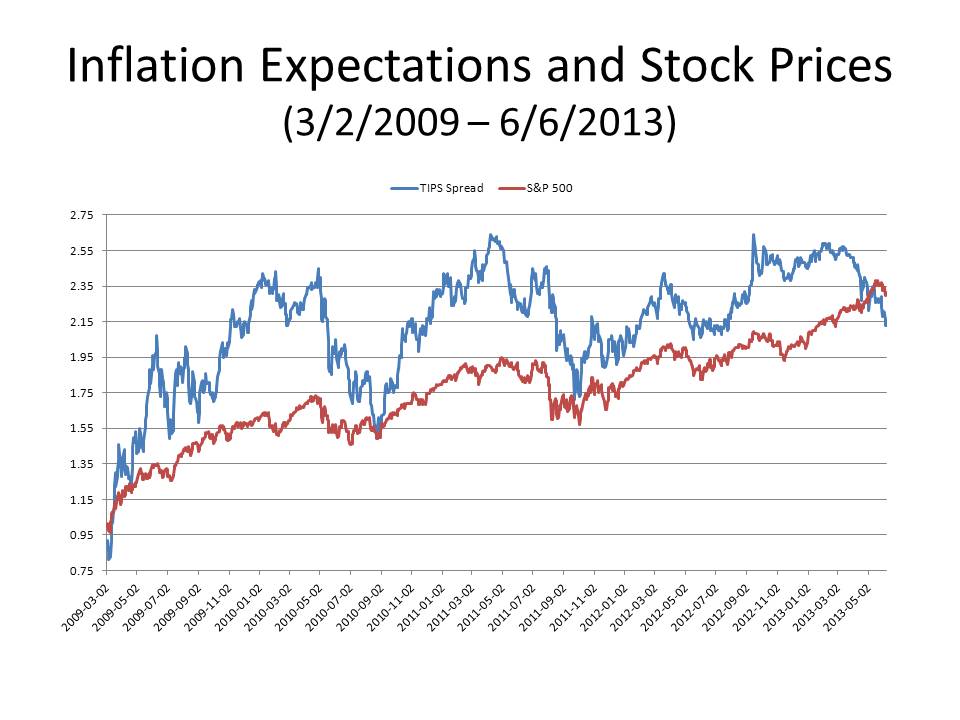

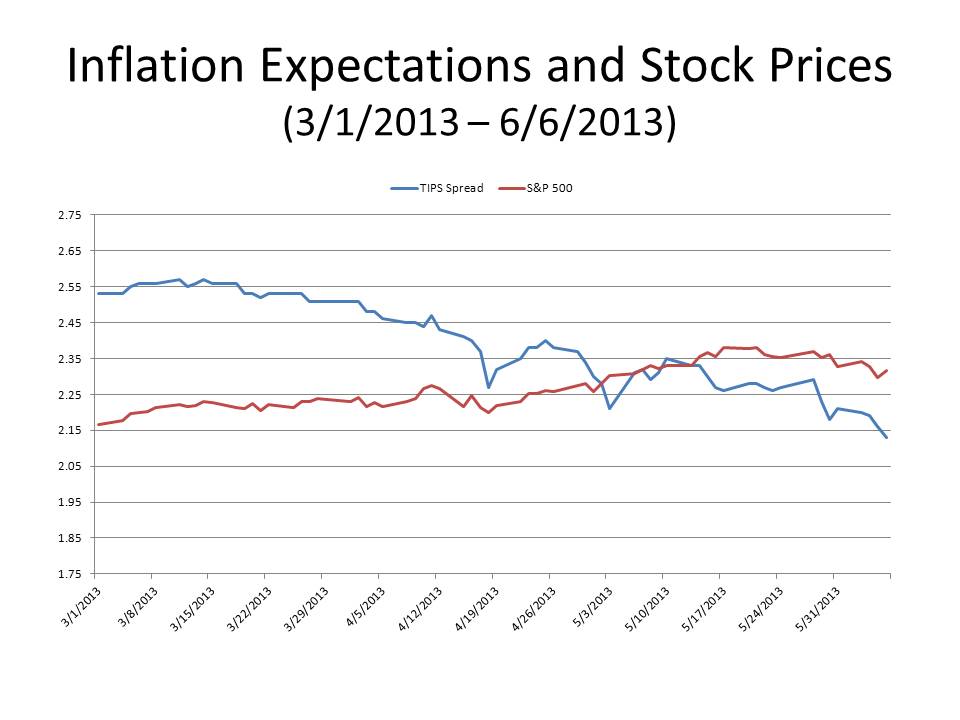

Eureka! Today we found out that NGDP (which the Fed looks at) grew at a 2.19% rate over the past 6 months and the more accurate NGDI grew by 5.06%.

And shhhh! Don’t anyone tell the Fed about NGDI!

Scott hit it right on the nose with that one.

It reminded me of something, so I went an looked it up in a book I happen to have at home.

Here’s what it says about Fed policy coming out of the 1981-82 recession.

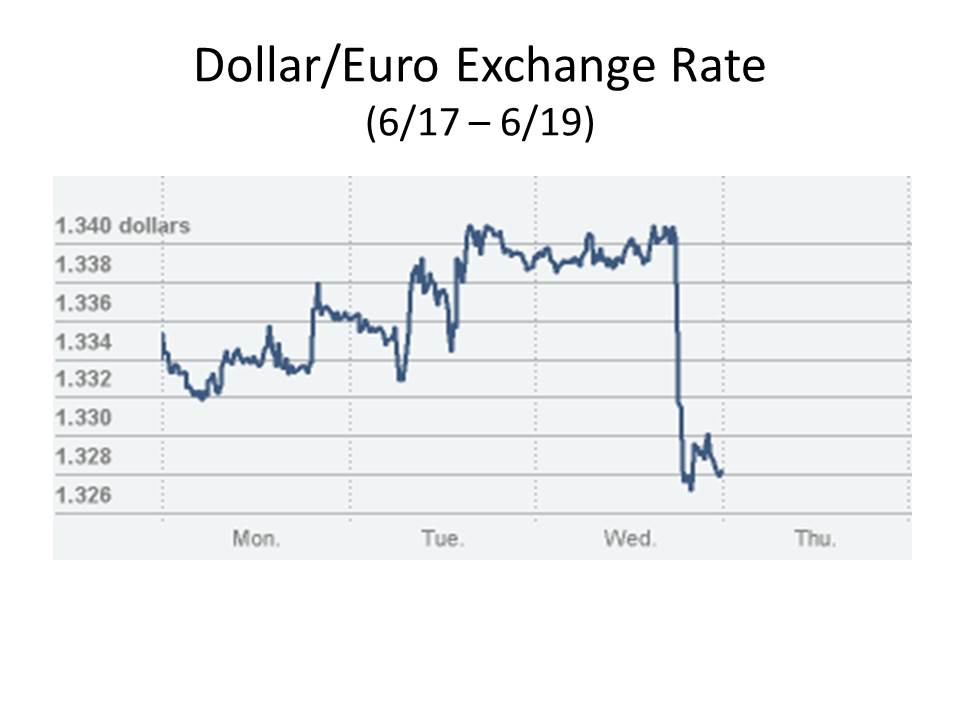

The renewed stringency forced interest rates to rise slightly while driving the dollare ever higher and commodities prices ever lower. Yet the recovery, once under way, was too powerful to be slowed down perceptibly by the monetary pressure. . . .

The recovery continued in the first half of 1984. But the amazing strength of the recovery pulled the growth of M-1 above its targets, reviving fears that the Fed would have to tighten. Instead of being welcomed, each bit of favorable economic news – strong growth in real GNP, reduced unemployment, higher factory orders – was greeted with fear and trepidation in the financial markets, because such reports were viewed as portents of future tightening by the Fed. Those fears generated continuing increases in interest rates, appreciation of the dollar, and falling commodities prices. In the summer of 1984, monetary stringency and fears that the Fed would clamp down even more tightly to bring the growth of M-1 back within its targets were threatening to produce a credit crunch and abort the recovery.

With interest rates and the dollar’s exchange rate again starting to rise rapidly, and with commodity prices losing the modest gains they had made in the previous year, the recovery was indeed threatened. In late July of 1984, two years after the Fed had given up its earlier effort to meet its monetary targets, the conditions for a credit crunch, if not a full scale panic, were again developing. The most widely reported monetary aggregate, M-1, was above the upper limit of the Fed’s growth target, and economic growth in the second quarter of 1984 was reported to have been an unexpectedly strong 7.5%. Commodities prices were practically in free fall and the dollar was soaring.

Once again, however, a timely intervention by Mr. Volcker calmed the markets and put to rest fears that the Fed would strive to keep monetary growth within the announced target ranges. Appearing before Congress, he announced that he expected inflation to remain low [around 4%!!!] and that the Fed would maintain its policy without seeking any further tightening to bring monetary growth within the target range. This assurance stopped, at least for a brief spell, the dollar’s rise in foreign exchange markets and permitted a slight rebound in commodities prices. Mr. Volcker’s assurance that monetary policy would not be tightened encouraged the public to stop trying to build up precautionary balances. As a consequence, M-1 growth leveled off even as interest rates fell back somewhat.

All the while Monetarist were loudly protesting the conduct of monetary policy. Before the Fed abandoned its attempt to target M-1, Monetarists criticized the Fed for not keeping monetary growth steady enough. For a time, they even attributed the failure of interest rates to fall as rapidly as the rate of inflation in 1981, or to fall at all in the first half of 1982, to uncertainty created by too much variability in the rate of monetary growth. Later, when the Fed abandoned, at any rate deemphasized, monetary targets, they warned that inflation would soon start to rise again. In late 1982, just as the economy was hitting bottom, Milton Friedman was predicting the return of double-digit inflation [sound familiar?] before the next election.

What book did I get that from? OK, I admit it. It’s from my book Free Banking and Monetary Reform, pp. 220-21. So we’ve been through this before. When the Fed adopts a crazy reaction function in which it won’t tolerate real growth above a certain threshold, which is what the Fed seems to have done, with the threshold at 3% or less, funny things start to happen.

How come no one is laughing?

PS I apologize again for not replying to comments lately. I am still trying to cope with my workload.