Just two days before the 50th anniversary of the assassination of John Kennedy, George Selgin offered an ironic endorsement of raising the inflation target, as happened during the Kennedy Administration, in order to reduce unemployment.

[T]his isn’t the first time that we’ve been in a situation like the present one. There was at least one other occasion when the U.S. economy, having been humming along nicely with the inflation rate of 2% and an unemployment rate between 5% and 6%, slid into a recession. Eventually the unemployment rate was 7%, the inflation rate was only 1%, and the federal funds rate was within a percentage point of the zero lower bound. Fortunately for the American public, some well-placed (mostly Keynesian) economists came to the rescue, by arguing that the way to get unemployment back down was to aim for a higher inflation rate: a rate of about 4% a year, they figured, should suffice to get the unemployment rate down to 4%–a much lower rate than anyone dares to hope for today.

I’m puzzled and frustrated because, that time around, the Fed took the experts’ advice and it worked like a charm. The federal funds rate quickly achieved lift-off (within a year it had risen almost 100 basis points, from 1.17% to 2.15%). Before you could say “investment multiplier” the inflation and unemployment numbers were improving steadily. Within a few years inflation had reached 4%, and unemployment had declined to 4%–just as those (mostly Keynesian) experts had predicted.

So why are these crazy inflation hawks trying to prevent us from resorting again to a policy that worked such wonders in the past? Do they just love seeing all those millions of workers without jobs? Or is it simply that they don’t care about job

Oh: I forgot to say what past recession I’ve been referring to. It was the recession of 1960-61. The desired numbers were achieved by 1967. I can’t remember exactly what happened after that, though I’m sure it all went exactly as those clever theorists intended.

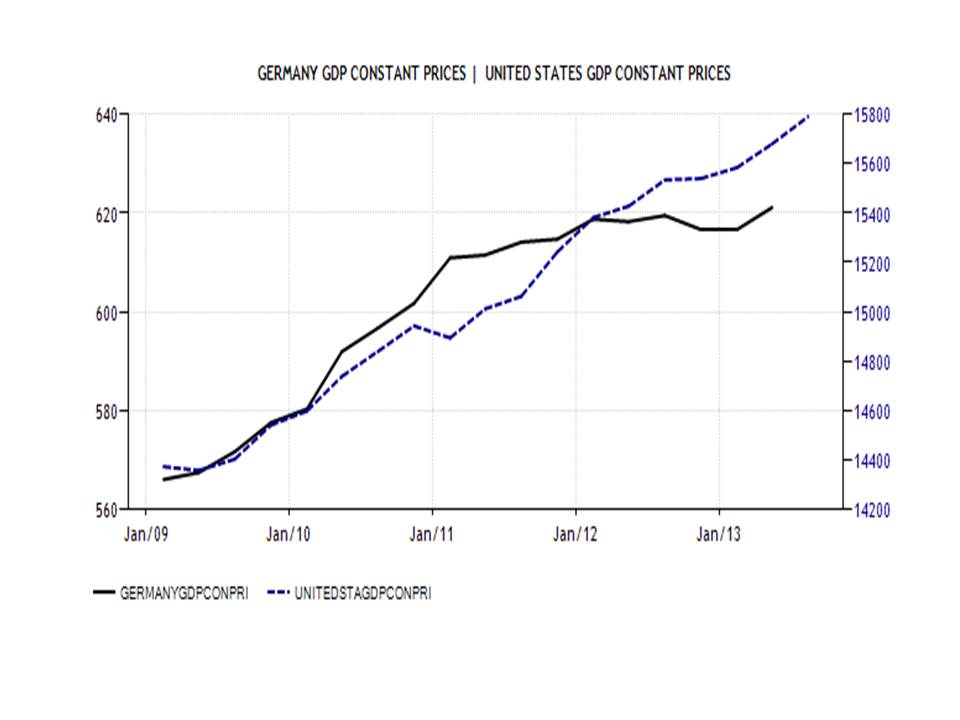

George has the general trajectory of the story more or less right, but the details and the timing are a bit off. Unemployment rose to 7% in the first half of 1961, and inflation was 1% or less. So reducing the Fed funds rate certainly worked, real GDP rising at not less than a 6.8% annual rate for four consecutive quarters starting with the second quarter of 1961, unemployment falling to 5.5 in the first quarter of 1962. In the following 11 quarters till the end of 1964, there were only three quarters in which the annual growth of GDP was less than 3.9%. The unemployment rate at the end of 1964 had fallen just below 5 percent and inflation was still well below 2%. It was only in 1965, that we see the beginings of an inflationary boom, real GDP growing at about a 10% annual rate in three of the next five quarters, and 8.4% and 5.6% in the other two quarters, unemployment falling to 3.8% by the second quarter of 1966, and inflation reaching 3% in 1966. Real GDP growth did not exceed 4% in any quarter after the first quarter of 1966, which suggests that the US economy had reached or exceeded its potential output, and unemployment had fallen below its natural rate.

In fact, recognizing the inflationary implications of the situation, the Fed shifted toward tighter money late in 1965, the Fed funds rate rising from 4% in late 1965 to nearly 6% in the summer of 1966. But the combination of tighter money and regulation-Q ceilings on deposit interest rates caused banks to lose deposits, producing a credit crunch in August 1966 and a slowdown in both real GDP growth in the second half of 1966 and the first half of 1967. With the economy already operating at capacity, subsequent increases in aggregate demand were reflected in rising inflation, which reached 5% in the annus horribilis 1968.

Cleverly suggesting that the decision to use monetary expansion, and an implied higher tolerance for inflation, to reduce unemployment from the 7% rate to which it had risen in 1961 was the ultimate cause of the high inflation of the late 1960s and early 1970s, and, presumably, the stagflation of the mid- and late-1970s, George is inviting his readers to conclude that raising the inflation target today would have similarly disastrous results.

Well, that strikes me as quite an overreach. Certainly one should not ignore the history to which George is drawing our attention, but I think it is possible (and plausible) to imagine a far more benign course of events than the one that played itself out in the 1960s and 1970s. The key difference is that the ceilings on deposit interest rates that caused a tightening of monetary policy in 1966 to produce a mini-financial crisis, forcing the 1966 Fed to abandon its sensible monetary tightening to counter inflationary pressure, are no longer in place.

Nor should we forget that some of the inflation of the 1970s was the result of supply-side shocks for which some monetary expansion (and some incremental price inflation) was an optimal policy response. The disastrous long-term consequences of Nixon’s wage and price controls should not be attributed to the expansionary monetary policy of the early 1960s.

As Mark Twain put it so well:

We should be careful to get out of an experience only the wisdom that is in it and stop there lest we be like the cat that sits down on a hot stove lid. She will never sit down on a hot stove lid again and that is well but also she will never sit down on a cold one anymore.