Commenter TravisV kindly referred me to a review article by David Frum in the current issue of the Atlantic Monthly of The Deluge by Adam Tooze, an economic history of the First World War, its aftermath, and the rise of America as the first global superpower since the Roman Empire. Frum draws an interesting contrast between Tooze’s understanding of the 1920-21 depression and the analysis of that episode presented in James Grant’s recent paean to the Greatest Depression.

But in thinking about Frum’s article, and especially his comments on Grant, I realized that my own discussion of the 1920-21 depression was not fully satisfactory, and so I have been puzzling for a couple of weeks about my own explanation for the good depression of 1920-21. What follows is a progress report on my thinking.

Here is what Frum says about Grant:

Periodically, attempts have been made to rehabilitate the American leaders of the 1920s. The most recent version, James Grant’s The Forgotten Depression, 1921: The Crash That Cured Itself, was released just two days before The Deluge: Grant, an influential financial journalist and historian, holds views so old-fashioned that they have become almost retro-hip again. He believes in thrift, balanced budgets, and the gold standard; he abhors government debt and Keynesian economics. The Forgotten Depression is a polemic embedded within a narrative, an argument against the Obama stimulus joined to an account of the depression of 1920-21.

As Grant correctly observes, that depression was one of the sharpest and most painful in American history. Total industrial production may have dropped by 30 percent. [According to Industrial Production Index of the Federal Reserve, industrial production dropped by almost 40%, DG] Unemployment spiked at perhaps close to 12 percent (accurate joblessness statistics don’t exist for this period). Overall, prices plummeted at the steepest rate ever recorded—steeper than in 1929-33. Then, after 18 months of extremely hard times, the economy lurched into recovery. By 1923, the U.S. had returned to full employment.

Grant presents this story as a laissez-faire triumph. Wartime inflation was halted. . . . Recovery then occurred naturally, without any need for government stimulus. “The hero of my narrative is the price mechanism, Adam Smith’s invisible hand,” he notes. “In a market economy, prices coordinate human effort. They channel investment, saving and work. High prices encourage production but discourage consumption; low prices do the opposite. The depression of 1920-21 was marked by plunging prices, the malignity we call deflation. But prices and wages fell only so far. They stopped falling when they become low enough to entice consumers into shopping, investors into committing capital and employers into hiring. Through the agency of falling prices and wages, the American economy righted itself.” Reader, draw your own comparisons!

. . .

Grant rightly points out that wars are usually followed by economic downturns. Such a downturn occurred in late 1918-early 1919. “Within four weeks of the … Armistice, the [U.S.] War Department had canceled $2.5 billion of its then outstanding $6 billion in contracts; for perspective, $2.5 billion represented 3.3 percent of the 1918 gross national product,” he observes. Even this understates the shock, because it counts only Army contracts, not Navy ones. The postwar recession checked wartime inflation, and by March 1919, the U.S. economy was growing again.

Here is where the argument needs further clarity and elaboration. But first let me comment parenthetically that there are two distinct kinds of post-war downturns. First, there is an inevitable adjustment whereby productive resources are shifted to accommodate the shift in demand from armaments to civilian products. The reallocation entails the temporary unemployment that is described in familiar search and matching models. Because of the magnitude of the adjustment, these sectoral-adjustment downturns can last for some time, typically two to four quarters. But there is a second and more serious kind of downturn; it can be associated either with an attempt to restore a debased currency to its legal parity, or with the cessation of money printing to finance military expenditures by the government. Either the deflationary adjustment associated with restoring a suspended monetary standard or the disinflationary adjustment associated with the end of a monetary expansion tends to exacerbate and compound the pure resource reallocation problem that is taking place simultaneously.

What I have been mainly puzzling over is how to think about the World War I monetary expansion and inflation, especially in the US. From the beginning of World War I in 1914 till the US entered the war in April 1917, the dollar remained fully convertible into gold at the legal gold price of $20.67 an ounce. Nevertheless, there was a huge price inflation in the US prior to April 1917. How was this possible while the US was on the gold standard? It’s not enough to say that a huge influx of gold into the US caused the US money supply to expand, which is the essence of the typical quantity-theoretic explanation of what happened, an explanation that you will find not just in Friedman and Schwartz, but in most other accounts as well.

Why not? Because, as long as the dollar was still redeemable at the official gold price, people could redeem their excess dollars for gold to avoid the inflationary losses incurred by holding dollars. Why didn’t they? In my previous post on the subject, I suggested that it was because gold, too, was depreciating, so that rapid US inflation from 1915 to 1917 before entering the war was a reflection of the underlying depreciation of gold.

But why was gold depreciating? What happened to make gold less valuable? There are two answers. First, a lot of gold was being withdrawn from circulation, as belligerent governments were replacing their gold coins with paper or base metallic coins. But there was a second reason: the private demand for gold was being actively suppressed by governments. Gold could no longer be freely imported or exported. Without easy import and export of gold, the international gold market, a necessary condition for the gold standard, ceased to function. If you lived in the US and were concerned about dollar depreciation, you could redeem your dollars for gold, but you could not easily find anyone else in the world that would pay you more than the official price of $20.67 an ounce, even though there were probably people out there willing to pay you more than that price if you could only find them and circumvent the export and import embargoes to ship the gold to them. After the US entered the war in April 1917, an embargo was imposed on the export of gold from the US, but that was largely just a precaution. Even without an embargo, little gold would have been exported.

So it was at best an oversimplification for me to say in my previous post that the dollar depreciated along with gold during World War I, because there was no market mechanism that reflected or measured the value of gold during World War I. Insofar as the dollar was still being used as a medium of exchange, albeit with many restrictions, it was more correct to say that the value of gold reflected the value of the dollar, than that the value of the dollar reflected the value of gold.

In my previous post, I posited that, owing to the gold-export embargo imposed after US entry into World War I, the dollar actually depreciated by less than gold between April 1917 and the end of the war. I then argued that after full dollar convertibility into gold was restored after the war, the dollar had to depreciate further to match the value of gold. That was an elegant explanation for the anomalous postwar US inflation, but that explanation has a problem: gold was flowing out of the US during the inflation, but if my explanation of the postwar inflation were right, gold should have been flowing into the US as the trade balance turned in favor of the US.

So, much to my regret, I have to admit that my simple explanation, however elegant, of the post-World War I inflation, as an equilibration of the dollar price level with the gold price level, was too simple. So here are some provisional thoughts, buttressed by a bit of empirical research and evidence drawn mainly from two books by W. A. Brown England and the New Gold Standard and The International Gold Standard Reinterpreted 1914-34.

The gold standard ceased to function as an economic system during World War I, because a free market in gold ceased to exist. Nearly two-thirds of all the gold in the world was mined in territories under the partial or complete control of the British Empire (South Africa, Rhodesia, Australia, Canada, and India). Another 15% of the world’s output was mined in the US or its territories. Thus, Britain was in a position, with US support and approval, to completely dominate the world gold market. When the war ended, a gold standard could not begin to function again until a free market in gold was restored. Here is how Brown describes the state of the world gold market (or non-market) immediately after the War.

In March 1919 when the sterling-dollar rate was freed from control, the export of gold was for the first time legally [my emphasis] prohibited. It was therefore still impossible to measure the appreciation or depreciation of any currency in terms of a world price of gold. The price of gold was nowhere determined by world-wide forces. The gold of the European continent was completely shut out of the world’s trade by export embargoes. There was an embargo upon the export of gold from Australia. All the gold exported from the Union of South Africa had still to be sold to the Bank of England at its statutory price. Gold could not be exported from the United States except under government license. All the avenues of approach by which gold from abroad could reach the public in India were effectually closed. The possessors of gold in the United States, South Africa, India, or in England, Spain, or France, could not offer their gold to prospective buyers in competition with one another. The purchasers of gold in these countries did not have access to the world’s supplies, but on the other hand, they were not exposed to foreign competition for the supplies in their own countries, or in the sphere of influence of their own countries.

Ten months after the war ended, on September 12, 1919, many wartime controls over gold having been eliminated, a free market in gold was reestablished in London.

No longer propped up by the elaborate wartime apparatus of controls and supports, the official dollar-sterling exchange rate of $4.76 per pound gave way in April 1919, falling gradually to less than $4 by the end of 1919. With the dollar-sterling exchange rate set free and the dollar was pegged to gold at the prewar parity of $20.67 an ounce, the sterling price of gold and the dollar-sterling exchange rate varied inversely. The US wholesale price index (in current parlance the producer price index) stood at 23.5 in November 1918 when the war ended (compared to 11.6 in July 1914 just before the war began). Between November 1918 and June 1919 the wholesale price index was roughly stable, falling to 23.4, a drop of just 0.4% in seven months. However, the existence of wartime price controls, largely dismantled in the months after the war ended, introduces some noise into the price indices, making price-level estimates and comparisons in the latter stages of the War and its immediate aftermath problematic.

When the US embargo on gold exports was lifted in June 1919, causing a big jump in gold exports in July 1919, wholesale prices shot up nearly 4% to 24.3, and to 24.9 in August, suggesting that lifting the gold export embargo tended to reduce the international value of gold to which the dollar corresponded. Prices dropped somewhat in September when the London gold market was reestablished, perhaps reflecting the impact of pent-up demand for gold suddenly becoming effective. Prices remained stable in October before rising almost 2% in November. Price increases accelerated in December and January, leveled off in February and March, before jumping up in April, the PPI reaching its postwar peak (28.8, a level not reached again till November 1950!) in May 1920.

My contention is that the US price level after World War I largely reflected the state of the world gold market, and the state of the world gold market was mainly determined by the direction and magnitude of gold flows into or out of the US. From the War’s end in November 1918 till the embargo on US gold exports was lifted the following July, the gold market was insulated from the US. The wartime controls imposed on the world gold market were gradually being dismantled, but until the London gold market reopened in September 1919, allowing gold to move to where it was most highly valued, there was no such thing as a uniform international value of gold to which the dollar had to correspond.

My understanding of the postwar US inflation and the subsequent deflation is based on the close relationship between monetary policy and the direction and magnitude of gold flows. Under a gold standard, and given the demand to hold the liabilities of a central bank, a central bank typically controlled the amount of gold reserves it held by choosing the interest rate at which it would lend. The relationship between the central-bank lending rate and its holdings of reserves is complex, but the reserve position of a central bank was reliably correlated with the central-bank lending rate, as Hawtrey explained and documented in his Century of Bank Rate. So the central bank lending rate can be thought of as the means by which a central bank operating under a gold standard made its demand for gold reserves effective.

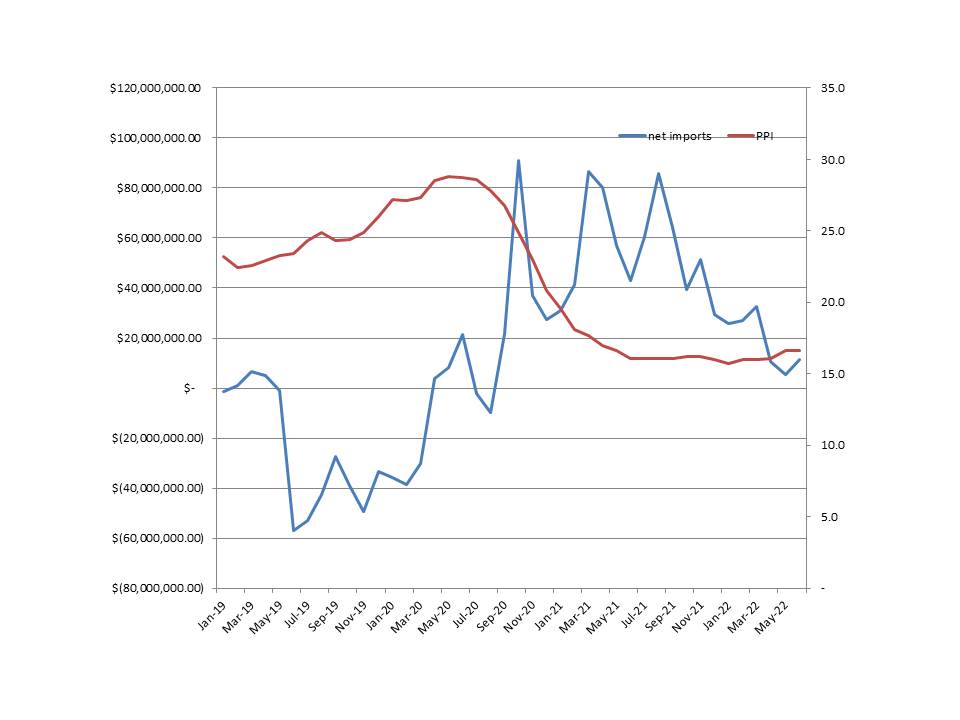

The chart below shows monthly net gold flows into the US from January 1919 through June 1922. Inflows (outflows) correspond to positive (negative) magnitudes measured on left vertical axis; the PPI is measured on the right vertical axis. From January 1919 to June 1920, prices were relatively high and rising, while gold was generally flowing out of the US. From July 1920 till June 1921, prices fell sharply while huge amounts of gold were flowing into the US. Prices hit bottom in June, and gold inflows gradually tapered off in the second half of 1921.

The correlation is obviously very far from perfect; I have done a number of regressions trying to explain movements in the PPI from January 1919 to June 1922, and the net monthly inflow of gold into the US consistently accounts for roughly 25% of the monthly variation in the PPI, and I have yet to find any other variable that is reliably correlated with the PPI over that period. Of course, I would be happy to receive suggestions about other variables that might be correlated with price level changes. Here’s the simplest regression result.

The correlation is obviously very far from perfect; I have done a number of regressions trying to explain movements in the PPI from January 1919 to June 1922, and the net monthly inflow of gold into the US consistently accounts for roughly 25% of the monthly variation in the PPI, and I have yet to find any other variable that is reliably correlated with the PPI over that period. Of course, I would be happy to receive suggestions about other variables that might be correlated with price level changes. Here’s the simplest regression result.

y = -4.41e-10 NGOLDIMP, 41 observations, t = -3.99, r-squared = .285, where y is the monthly percentage change in the PPI, and NGOLDIMP is net monthly gold imports into the US.

The one part of the story that still really puzzles me is that deflation bottomed out in June 1921, even though monthly gold inflows remained strong throughout the spring and summer of 1921 before tapering off in the autumn. Perhaps there was a complicated lag structure in the effects of gold inflows on prices that might be teased out of the data, but I don’t see it. And adding lagged variables does little if anything to improve the fit of the regression.

I want to make two further points about the dearly beloved 1920-21 depression. Let me go to the source and quote from James Grant himself waxing eloquent in the Wall Street Journal about the beguiling charms of the wonderful 1920-21 experience.

In the absence of anything resembling government stimulus, a modern economist may wonder how the depression of 1920-21 ever ended. Oddly enough, deflation turned out to be a tonic. Prices—and, critically, wages too—were allowed to fall, and they fell far enough to entice consumers, employers and investors to part with their money. Europeans, noticing that America was on the bargain counter, shipped their gold across the Atlantic, where it swelled the depression-shrunken U.S. money supply. Shares of profitable and well-financed American companies changed hands at giveaway valuations.

The first point to make is that Grant has the causation backwards; it was the flow of gold into the US that caused deflation by driving up the international value of gold and forcing down prices in terms of gold. The second point to make is that Grant completely ignores the brutal fact that the US exported its deflation to Europe and most of the rest of the world. Indeed, because Europe and much of the rest of the world were aiming to rejoin the gold standard, which effectively meant going on a dollar standard at the prewar dollar parity, and because, by 1920, almost every other currency was at a discount relative to the prewar dollar parity, the rest of the world had to endure a far steeper deflation than the US did in order to bring their currencies back to the prewar parity against the dollar. So the notion that US deflation lured eager bargain-hunting Europeans to flock to the US to spend their excess cash would be laughable, if it weren’t so pathetic. Even when the US recovery began in the summer of 1921, almost everywhere else prices were still falling, and output and employment contractin.

This can be seen by looking at the exchange rates of European countries against the dollar, normalizing the February 1920 exchange rates as 100. In February 1921, here are the exchange rates. (Source W. A. Brown The International Gold Standard Reinterpreted 1914-34, Table 29)

UK 114.6

France 101.8

Switzerland 99.3

Denmark 124.4

Belgium 103.6

Sweden 119.6

Holland 94.9

Italy 81.6

Norway 102.8

Spain 84.9

And in 1922, the exchange rates for every country had risen against the dollar (peak month noted in parentheses), implying steeper deflation in each of those countries in 1921 than in the US.

UK (June) 134.3

France (April) 131.1

Switzerland (February) 118.5

Denmark (June) 145.4

Belgium (April) 117.7

Sweden (March) 140.6

Holland (April) 105.2

Italy (April) 119.6

Norway (May) 106.8

Spain (February) 94.9

As David Frum emphasizes, the damage inflicted by the bright and shining depression of 1920-21 was not confined to the US, it exacted an even greater price on the already devastated European continent, thereby setting the stage, in conjunction with the draconian reparations imposed by the Treaty of Versailles and the war debts that the US insisted on collecting, preferably in gold, not imports, from its allies, first for the great German hyperinflation and then the Great Depression. And we all know what followed.

So, yes, by all means, let us all raise our glasses and toast the dearly beloved, bright and shining, depression of 1920-21, of blessed memory, the greatest depression ever. May we never see its like again.