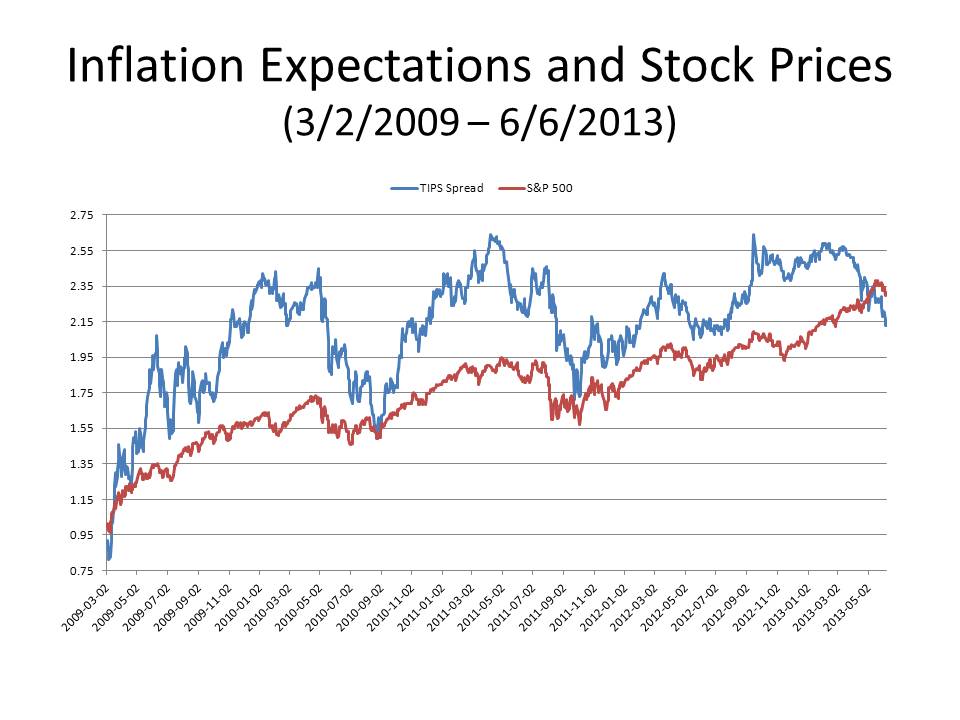

Possibly responding to hints by ECB president Mario Draghi of monetary stimulus, stocks around the world are up today; the S&P 500 over 1900 (about 2% above yesterday’s close). Anyone who wants to understand why stock markets have been swooning since the end of 2015 should take a look at this chart showing  the breakeven TIPS spread on 10-year Treasuries over the past 10 years.

the breakeven TIPS spread on 10-year Treasuries over the past 10 years.

Let’s look at the peak spread (2.56%) reached in early July 2008, a couple of months before the onset of the financial crisis in September. Despite mounting evidence that the economy was contracting and unemployment rising, the Fed, transfixed by the threat of Inflation (manifested in rising energy prices) and a supposed loss of Fed credibility (manifested in rising inflation expectations), refused to continue reducing its interest-rate target lest the markets conclude that the Fed was not serious about fighting inflation. That’s when all hell started to break loose. By September 14, the Friday before the Lehman bankruptcy, the breakeven TIPS spread had fallen to 1.95%. It was not till October that the Fed finally relented and reduced its target rate, but nullified whatever stimulus the lower target rate might have provided by initiating the payment of interest on reserves. As you can see the breakeven spread continued to fall almost without interruption till reaching lows of about 0.10% by the end of 2008.

There were three other episodes of falling inflation expectations which are evident on the graph, in 2010, 2011 and 2012, each episode precipitating a monetary response (so-called quantitative easing) by the Fed to reverse the fall in inflation expectations, thereby avoiding an untimely end to the weak recovery from the financial crisis and the subsequent Little Depression.

Despite falling inflation expectations during the second half of 2014, the lackluster expansion continued, a possible sign of normalization insofar as the momentum of recovery was sustained despite falling inflation expectations (due in part to a positive oil-supply shock). But after a brief pickup in the first half of 2015, inflation expectations have been falling further in the second half of 2015, and the drop has steepened over the past month, with the breakeven TIPS spread falling from 1.56% on January 5 to 1.28% yesterday, a steeper decline than in July 2008, when the TIPS spread on July 3 stood at 2.56% and did not fall to 2.30% until August 5.

I am not saying that the market turmoil of the past three weeks is totally attributable to falling inflation expectations; it seems very plausible that the bursting of the oil bubble has been a major factor in the decline of stock prices. Falling oil prices could affect stock prices in at least two different ways: 1) the decline in energy prices itself being deflationary – at least if monetary policy is not specifically aimed at reversing those deflationary effects – and 2) oil and energy assets being on the books of many financial institutions, a decline in their value may impair the solvency of those institutions, causing a deflationary increase in the demand for currency and reserves. But even if falling oil prices are an independent cause of market turmoil, they interact with and reinforce deflationary pressures; the only way to counteract those deflationary pressures is monetary expansion.

And with inflation expectations now lower than they have been since early 2009, further reductions in inflation expectations could put us back into a situation in which the expected yield from holding cash exceeds the expected yield from holding real capital. In such situations, with nominal interest rates at or near the zero lower bound, a perverse Fisher effect takes hold and asset prices have to fall sufficiently to make people willing to hold assets rather than cash. (I explained this perverse adjustment process in this paper, and used it to explain the 2008 financial crisis and its aftermath.) The result is a crash in asset prices. We haven’t reached that point yet, but I am afraid that we are getting too close for comfort.

The 2008 crisis. was caused by an FOMC that was so focused on the threat of inflation that they ignored ample and obvious signs of a rapidly deteriorating economy and falling inflation expectations, foolishly interpreting the plunge in TIPS spreads and the appreciation of the dollar relative to other currencies as an expression by the markets of confidence in Fed policy rather than as a cry for help.

In 2008, the Fed at least had the excuse of rising energy prices and headline inflation above its then informal 2% target for not cutting interest rates to provide serious monetary stimulus to a collapsing economy. This time, despite failing for over three years to meet its now official 2% inflation target, Dr. Yellen and her FOMC colleagues show no sign of thinking about anything other than when they can show their mettle as central bankers by raising interest rates again. Now is not the time to worry about raising interest rates. Dr. Yellen’s problem is now to show that her top – indeed her only – priority is to ensure that the Fed’s 2% inflation target will be met, or, if need be, exceeded, in 2016 and that the growth in nominal income in 2016 will be at least as large as it was in 2015. Those are goals that are eminently achievable, and if the FOMC has any credibility left after its recent failures, providing such assurance will prevent another unnecessary and destructive financial crisis.

The 2008 financial crisis ensured the election of Barak Obama as President. I shudder to think of who might be elected if we have another crisis this year.