It seems that an announcement about who will be appointed as Fed Chairman after Janet Yellen’s terms expires early next year is imminent. Although there are sources in the Administration, e.g., the President, indicating that Janet Yellen may be reappointed, the betting odds strongly favor Jerome Powell, a Republican currently serving as a member of the Board of Governors, over the better-known contender, John Taylor, who has earned a considerable reputation as an academic economist, largely as author of the so-called Taylor Rule, and has also served as a member of the Council of Economic Advisers and the Treasury in previous Republican administrations.

Taylor’s support seems to be drawn from the more militant ideological factions within the Republican Party owing to his past criticism of Fed’s quantitative-easing policy after the financial crisis and little depression, having famously predicted that quantitative easing would revive dormant inflationary pressures, presaging a return to the stagflation of the 1970s, while Powell, who has supported the Fed’s policies under Bernanke and Yellen, is widely suspect in the eyes of the Republican base as a just another elitist establishmentarian inhabiting the swamp that the new administration was elected to drain. Nevertheless, Taylor’s academic background, his prior government service, and his long-standing ties to the US and international banking and financial institutions make him a less than ideal torch bearer for the true-blue (or true-red) swamp drainers whose ostensible goal is less to take control of the Fed than to abolish it. To accommodate both the base and the establishment, it is possible that, as reported by Breitbart, both Powell and Taylor will be appointed, one replacing Yellen as chairman, the other replacing Stanley Fischer as vice-chairman.

Seeing no evidence that Taylor has a sufficient following for his appointment to provide any political benefit, I have little doubt that it will be Powell who replaces Yellen, possibly along with Taylor as Vice-Chairman, if Taylor, at the age of 71, is willing to accept a big pay cut, just to take the vice-chairmanship with little prospect of eventually gaining the top spot he has long coveted.

Although I think it unlikely that Taylor will be the next Fed Chairman, the recent flurry of speculation about his possible appointment prompted me to look at a recent talk that he gave at the Federal Reserve Bank of Boston Conference on the subject: Are Rules Made to be Broken? Discretion and Monetary Policy. The title of his talk “Rules versus Discretion: Assessing the Debate over Monetary Policy” is typical of Taylor’s very low-key style, a style that, to his credit, is certainly not calculated to curry favor with the Fed-bashers who make up a large share of a Republican base that demands constant attention and large and frequently dispensed servings of red meat.

I found several things in Taylor’s talk notable. First, and again to his credit, Taylor does, on occasion, acknowledge the possibility that other interpretations of events from his own are possible. Thus, in arguing that the good macroeconomic performance (“the Great Moderation”) from about 1985 to 2003, was the result of the widespread adoption of “rules-based” monetary policy, and that the subsequent financial crisis and deep recession were the results of the FOMC’s having shifted, after the 2001 recession, from that rules-based policy to a discretionary policy, by keeping interest rates too low for too long, Taylor did at least recognize the possibility that the reason that the path of interest rates after 2003 departed from the path that, he claims, had been followed during the Great Moderation was that the economy was entering a period of inherently greater instability in the early 2000s than in the previous two decades because of external conditions unrelated to actions taken by the Fed.

The other view is that the onset of poor economic performance was not caused by a deviation from policy rules that were working, but rather to other factors. For example, Carney (2013) argues that the deterioration of performance in recent years occurred because “… the disruptive potential of financial instability—absent effective macroprudential policies—leads to a less favourable Taylor frontier.” Carney (2013) illustrated his argument with a shift in the tradeoff frontier as did King (2012). The view I offer here is that the deterioration was due more to a move off the efficient policy frontier due to a change in policy. That would suggest moving back toward the type of policy rule that described policy decisions during the Great Moderation period. (p. 9)

But despite acknowledging the possibility of another view, Taylor offers not a single argument against it. He merely reiterates his own unsupported opinion that the policy post-2003 became less rule-based than it had been from 1985 to 2003. However, later in his talk in a different context, Taylor does return to the argument that the Fed’s policy after 2003 was not fundamentally different from its policy before 2003. Here Taylor is assuming that Bernanke is acknowledging that there was a shift in from the rules-based monetary policy of 1985 to 2003, but that the post-2003 monetary policy, though not rule-based as in the way that it had been in 1985 to 2003, was rule-based in a different sense. I don’t believe that Bernanke would accept that there was a fundamental change in the nature of monetary policy after 2003, but that is not really my concern here.

At a recent Brookings conference, Ben Bernanke argued that the Fed had been following a policy rule—including in the “too low for too long” period. But the rule that Bernanke had in mind is not a rule in the sense that I have used it in this discussion, or that many others have used it.

Rather it is a concept that all you really need for effective policy making is a goal, such as an inflation target and an employment target. In medicine, it would be the goal of a healthy patient. The rest of policymaking is doing whatever you as an expert, or you as an expert with models, thinks needs to be done with the instruments. You do not need to articulate or describe a strategy, a decision rule, or a contingency plan for the instruments. If you want to hold the interest rate well below the rule-based strategy that worked well during the Great Moderation, as the Fed did in 2003-2005, then it’s ok, if you can justify it in terms of the goal.

Bernanke and others have argued that this approach is a form of “constrained discretion.” It is an appealing term, and it may be constraining discretion in some sense, but it is not inducing or encouraging a rule as the language would have you believe. Simply having a specific numerical goal or objective function is not a rule for the instruments of policy; it is not a strategy; in my view, it ends up being all tactics. I think there is evidence that relying solely on constrained discretion has not worked for monetary policy. (pp. 16-17)

Taylor has made this argument against constrained discretion before in an op-ed in the Wall Street Journal (May 2, 2015). Responding to that argument I wrote a post (“Cluelessness about Strategy, Tactics and Discretion”) which I think exposed how thoroughly confused Taylor is about what a monetary rule can accomplish and what the difference is between a monetary rule that specifies targets for an instrument and a monetary rule that specifies targets for policy goals. At an even deeper level, I believe I also showed that Taylor doesn’t understand the difference between strategy and tactics or the meaning of discretion. Here is an excerpt from my post of almost two and a half years ago.

Taylor denies that his steady refrain calling for a “rules-based policy” (i.e., the implementation of some version of his beloved Taylor Rule) is intended “to chain the Fed to an algebraic formula;” he just thinks that the Fed needs “an explicit strategy for setting the instruments” of monetary policy. Now I agree that one ought not to set a policy goal without a strategy for achieving the goal, but Taylor is saying that he wants to go far beyond a strategy for achieving a policy goal; he wants a strategy for setting instruments of monetary policy, which seems like an obvious confusion between strategy and tactics, ends and means.

Instruments are the means by which a policy is implemented. Setting a policy goal can be considered a strategic decision; setting a policy instrument a tactical decision. But Taylor is saying that the Fed should have a strategy for setting the instruments with which it implements its strategic policy. (OED, “instrument – 1. A thing used in or for performing an action: a means. . . . 5. A tool, an implement, esp. one used for delicate or scientific work.”) This is very confused.

Let’s be very specific. The Fed, for better or for worse – I think for worse — has made a strategic decision to set a 2% inflation target. Taylor does not say whether he supports the 2% target; his criticism is that the Fed is not setting the instrument – the Fed Funds rate – that it uses to hit the 2% target in accordance with the Taylor rule. He regards the failure to set the Fed Funds rate in accordance with the Taylor rule as a departure from a rules-based policy. But the Fed has continually undershot its 2% inflation target for the past three [now almost six] years. So the question naturally arises: if the Fed had raised the Fed Funds rate to the level prescribed by the Taylor rule, would the Fed have succeeded in hitting its inflation target? If Taylor thinks that a higher Fed Funds rate than has prevailed since 2012 would have led to higher inflation than we experienced, then there is something very wrong with the Taylor rule, because, under the Taylor rule, the Fed Funds rate is positively related to the difference between the actual inflation rate and the target rate. If a Fed Funds rate higher than the rate set for the past three years would have led, as the Taylor rule implies, to lower inflation than we experienced, following the Taylor rule would have meant disregarding the Fed’s own inflation target. How is that consistent with a rules-based policy?

This is such an obvious point – and I am hardly the only one to have made it – that Taylor’s continuing failure to respond to it is simply inexcusable. In his apologetics for the Taylor rule and for legislation introduced (no doubt with his blessing and active assistance) by various Republican critics of Fed policy in the House of Representatives, Taylor repeatedly insists that the point of the legislation is just to require the Fed to state a rule that it will follow in setting its instrument with no requirement that Fed actually abide by its stated rule. The purpose of the legislation is not to obligate the Fed to follow the rule, but to merely to require the Fed, when deviating from its own stated rule, to provide Congress with a rationale for such a deviation. I don’t endorse the legislation that Taylor supports, but I do agree that it would be desirable for the Fed to be more forthcoming than it has been in explaining the reasoning about its monetary-policy decisions, which tend to be either platitudinous or obfuscatory rather than informative. But if Taylor wants the Fed to be more candid and transparent in defending its own decisions about monetary policy, it would be only fitting and proper for Taylor, as an aspiring Fed Chairman, to be more forthcoming than he has yet been about the obvious, and rather scary, implications of following the Taylor Rule during the period since 2003.

If Taylor is nominated to be Chairman or Vice-Chairman of the Fed, I hope that, during his confirmation hearings, he will be asked to explain what the implications of following the Taylor Rule would have been in the post-2003 period.

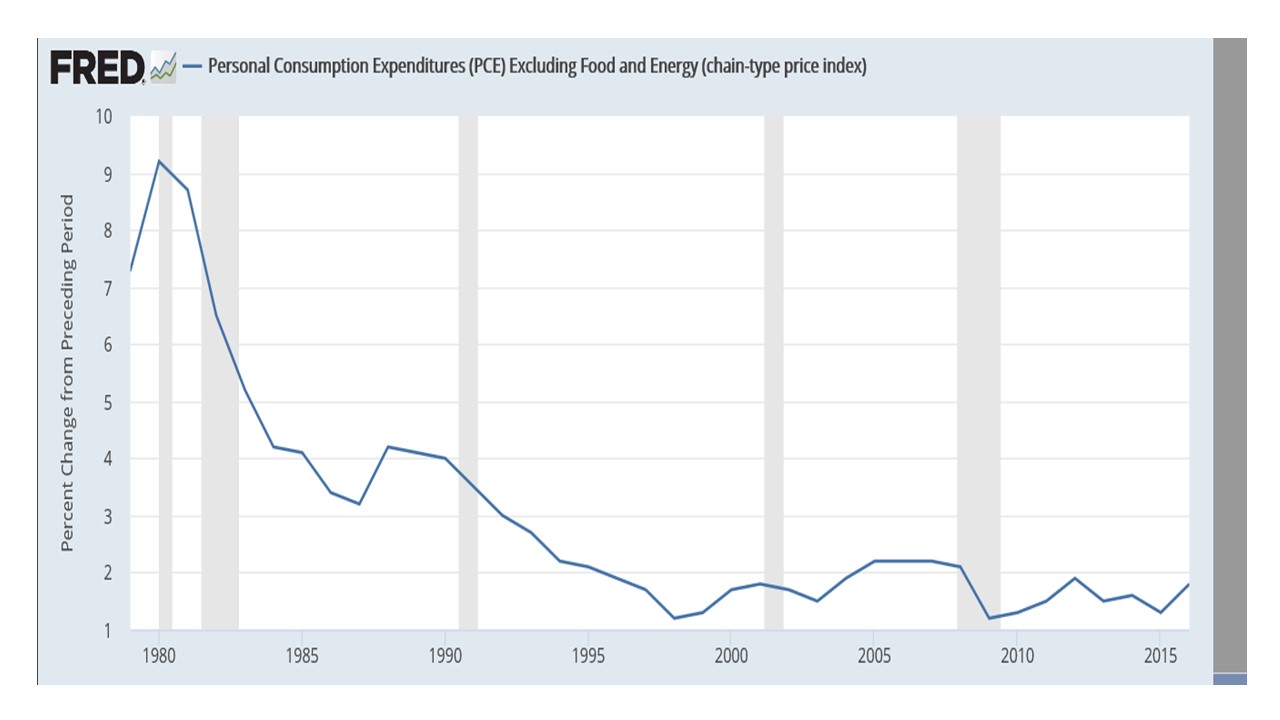

As the attached figure shows PCE inflation (excluding food and energy prices) was 1.9 percent in 2004. If inflation in 2004 was less than the 2% inflation target assumed by the Taylor Rule, why does Taylor think that raising interest rates in 2004 would have been appropriate? And if inflation in 2005 was merely 2.2%, just barely above the 2% target, what rate should the Fed Funds rate have reached in 2005, and how would that rate have affected the fairly weak recovery from the 2001 recession? And what is the basis for Taylor’s assessment that raising the Fed Funds rate in 2005 to a higher level than it was raised to would have prevented the subsequent financial crisis?

As the attached figure shows PCE inflation (excluding food and energy prices) was 1.9 percent in 2004. If inflation in 2004 was less than the 2% inflation target assumed by the Taylor Rule, why does Taylor think that raising interest rates in 2004 would have been appropriate? And if inflation in 2005 was merely 2.2%, just barely above the 2% target, what rate should the Fed Funds rate have reached in 2005, and how would that rate have affected the fairly weak recovery from the 2001 recession? And what is the basis for Taylor’s assessment that raising the Fed Funds rate in 2005 to a higher level than it was raised to would have prevented the subsequent financial crisis?

Taylor’s implicit argument is that by not raising interest rates as rapidly as the Taylor rule required, the Fed created additional uncertainty that was damaging to the economy. But what was the nature of the uncertainty created? The Federal Funds rate is merely the instrument of policy, not the goal of policy. To argue that the Fed was creating additional uncertainty by not changing its interest rate in line with the Taylor rule would only make sense if the economic agents care about how the instrument is set, but if it is an instrument the importance of the Fed Funds rate is derived entirely from its usefulness in achieving the policy goal of the Fed and the policy goal was the 2% inflation rate, which the Fed came extremely close to hitting in the 2004-06 period, during which Taylor alleges that the Fed’s monetary policy went off the rails and became random, unpredictable and chaotic.

If you calculate the absolute difference between the observed yearly PCE inflation rate (excluding food and energy prices) and the 2% target from 1985 to 2003 (Taylor’s golden age of monetary policy) the average yearly deviation was 0.932%. From 2004 to 2015, the period of chaotic monetary policy in Taylor’s view, the average yearly deviation between PCE inflation and the 2% target was just 0.375%. So when was monetary policy more predictable? Even if you just look at the last 12 years of the golden age (1992 to 2003), the average annual deviation was 0.425%.

The name Larry Summers is in the title of this post, but I haven’t mentioned him yet, so let me explain where Larry Summers comes into the picture. In his talk, Taylor mentions a debate about rules versus discretion that he and Summers had at the 2013 American Economic Association meetings and proceeds to give the following account of the key interchange in that debate.

Summers started off by saying: “John Taylor and I have, it will not surprise you . . . a fundamental philosophical difference, and I would put it in this way. I think about my doctor. Which would I prefer: for my doctor’s advice, to be consistently predictable, or for my doctor’s advice to be responsive to the medical condition with which I present? Me, I’d rather have a doctor who most of the time didn’t tell me to take some stuff, and every once in a while said I needed to ingest some stuff into my body in response to the particular problem that I had. That would be a doctor who’s [sic] [advice], believe me, would be less predictable.” Thus, Summers argues in favor of relying on an all-knowing expert, a doctor who does not perceive the need for, and does not use, a set of guidelines, but who once in a while in an unpredictable way says to ingest some stuff. But as in economics, there has been progress in medicine over the years. And much progress has been due to doctors using checklists, as described by Atul Gawande.

Of course, doctors need to exercise judgement in implementing checklists, but if they start winging it or skipping steps the patients usually suffer. Experience and empirical studies show that checklist-free medicine is wrought with dangers just as rules-free, strategy-free monetary policy is. (pp. 15-16)

Taylor’s citation of Atul Gawande, author of The Checklist Manifesto, is pure obfuscation. To see how off-point it is, have a look at this review published in the Seattle Times.

“The Checklist Manifesto” is about how to prevent highly trained, specialized workers from making dumb mistakes. Gawande — who appears in Seattle several times early next week — is a surgeon, and much of his book is about surgery. But he also talks to a construction manager, a master chef, a venture capitalist and the man at The Boeing Co. who writes checklists for airline pilots.

Commercial pilots have been using checklists for decades. Gawande traces this back to a fly-off at Wright Field, Ohio, in 1935, when the Army Air Force was choosing its new bomber. Boeing’s entry, the B-17, would later be built by the thousands, but on that first flight it took off, stalled, crashed and burned. The new airplane was complicated, and the pilot, who was highly experienced, had forgotten a routine step.

For pilots, checklists are part of the culture. For surgical teams they have not been. That began to change when a colleague of Gawande’s tried using a checklist to reduce infections when using a central venous catheter, a tube to deliver drugs to the bloodstream.

The original checklist: wash hands; clean patient’s skin with antiseptic; use sterile drapes; wear sterile mask, hat, gown and gloves; use a sterile dressing after inserting the line. These are all things every surgical team knows. After putting them in a checklist, the number of central-line infections in that hospital fell dramatically.

Then came the big study, the use of a surgical checklist in eight hospitals around the world. One was in rural Tanzania, in Africa. One was in the Kingdom of Jordan. One was the University of Washington Medical Center in Seattle. They were hugely different hospitals with much different rates of infection.

Use of the checklist lowered infection rates significantly in all of them.

Gawande describes the key things about a checklist, much of it learned from Boeing. It has to be short, limited to critical steps only. Generally the checking is not done by the top person. In the cockpit, the checklist is read by the copilot; in an operating room, Gawande discovered, it is done best by a nurse.

Gawande wondered whether surgeons would accept control by a subordinate. Which was stronger, the culture of hierarchy or the culture of precision? He found reason for optimism in the following dialogue he heard in the hospital in Amman, Jordan, after a nurse saw a surgeon touch a nonsterile surface:

Nurse: “You have to change your glove.”

Surgeon: “It’s fine.”

Nurse: “No, it’s not. Don’t be stupid.”

In other words, the basic rule underlying the checklist is simply: don’t be stupid. It has nothing to do with whether doctors should exercise judgment, or “winging it,” or “skipping steps.” What was Taylor even thinking? For a monetary authority not to follow a Taylor rule is not analogous to a doctor practicing checklist-free medicine.

As it happens, I have a story of my own about whether following numerical rules without exercising independent judgment makes sense in practicing medicine. Fourteen years ago, on the Friday before Labor Day, I was exercising at home and began to feeling chest pains. After ignoring the pain for a few minutes, I stopped and took a shower and then told my wife that I thought I needed to go to the hospital, because I was feeling chest pains – I was still in semi-denial about what I was feeling – my wife asked me if she should call 911, and I said that that might be a good idea. So she called 911, and told the operator that I was feeling chest pains. Within a couple of minutes, two ambulances arrived, and I was given an aspirin to chew and a nitroglycerine tablet to put under my tongue. I was taken to the emergency room at the hospital nearest to my home. After calling 911, my wife also called our family doctor to let him know what was happening and which hospital I was being taken to. He then placed a call to a cardiologist who had privileges at that hospital who happened to be making rounds there that morning.

When I got to the hospital, I was given an electrocardiogram, and my blood was taken. I was also asked to rate my pain level on a scale of zero to ten. The aspirin and nitroglycerine had reduced the pain level slightly, but I probably said it was at eight or nine. However, the ER doc looked at the electrocardiogram results and the enzyme levels in my blood, and told me that there was no indication that I was having a heart attack, but that they would keep me in the ER for observation. Luckily, the cardiologist who had been called by my internist came to the ER, and after talking to the ER doc, looking at the test results, came over to me and started asking me questions about what had happened and how I was feeling. Although the test results did not indicate that I was having heart attack, the cardiologist quickly concluded that what I was experiencing likely was a heart attack. He, therefore, hinted to me that I should request to be transferred to another nearby hospital, which not only had a cath lab, as the one I was then at did, but also had an operating room in which open heart surgery could be performed, if that would be necessary. It took a couple of tries on his part before I caught on to what he was hinting at, but as soon as I requested to be transferred to the other hospital, he got me onto an ambulance ASAP so that he could meet me at the hospital and perform an angiogram in the cath lab, cancelling an already scheduled angiogram.

The angiogram showed that my left anterior descending artery was completely blocked, so open-heart surgery was not necessary; angioplasty would be sufficient to clear the artery, which the cardiologist performed, also implanting two stents to prevent future blockage. I remained in the cardiac ICU for two days, and was back home on Monday, when my rehab started. I was back at work two weeks later.

The willingness of my cardiologist to use his judgment, experience and intuition to ignore the test results indicating that I was not having a heart attack saved my life. If the ER doctor, following the test results, had kept me in the ER for observation, I would have been dead within a few hours. Following the test results and ignoring what the patient was feeling would have been stupid. Luckily, I was saved by a really good cardiologist. He was not stupid; he could tell that the numbers were not telling the real story about what was happening to me.

We now know that, in the summer of 2008, the FOMC, being in the thrall of headline inflation numbers allowed a recession that had already started at the end of 2007 to deteriorate rapidly, pr0viding little or no monetary stimulus, to an economy when nominal income was falling so fast that debts coming due could no longer be serviced. The financial crisis and subsequent Little Depression were caused by the failure of the FOMC to provide stimulus to a failing economy, not by interest rates having been kept too low for too long after 2003. If John Taylor still hasn’t figured that out – and he obviously hasn’t — he should not be allowed anywhere near the Federal Reserve Board.