A couple of days ago, I wrote post gently (I hope) chiding Olivier Blanchard for what seemed to me to be a muddled attempt to attribute inflation to conflicts between various interest groups (labor, capital, creditors, debtors) that the political system is unable, or unwilling, to resolve,leavin, those conflicts to be addressed, albeit implicitly, by the monetary authority. In those circumstances, groups seek to protect, or even advance their interests, by seeking prices increases for their goods or services, triggering a continuing cycle of price and wage increases, aka a wage-price spiral.

My criticism of Blanchard wasn’t that the distributional conflicts that worry him don’t exist — they obviously do — or are irrelevant — they clearly aren’t, but that focusing attention on those conflicts tells us very little about the mechanisms that generate inflation: the macroeconomic policies (monetary or fiscal) under the control of governments and central banks. We live in complex societies consisting of many diverse and independent, yett deeply interrelated and interdependent, agents. Macroeconomic polilcies are adopted and implemented in an economic and social environment shaped by the various, and possibly conflicting, interests of these agents, so it would be absurd to argue that the conflicts and tensions that inevitably arise between those agents do not influence, or even dictate, the policy choices of governments and monetary authorities responsible for adopting and implementing macroeconomic policies.

Because distributional conflicts are inherent in any economy composed of a diverse set of agents pursuing their own inconsistent self-interests, so it seems quixotic to suppose or even imagine that distributional conflicts can be resolved by a formal negotiating process in the way that Blanchard seems to be suggesting. There are too many interests at play, too many conflicts to reconcile, too many terms to negotiate, too many uncertain conditions and too many unforeseen events requiring previously reached agreements to be renegotiated for these deep-seated conflicts to be resolved by any conceivable negotiation process.

The point that I tried to make is that, because it is unrealistic to think that the fundamental conflicts of interest characteristic of any modern economy can be reconciled by negotiation, the monetary authority should aim to adopt a policy on which economic agents can rely on in forming their expectations about the future. The best policy that the monetary authority can hope to achieve is one that aims for total nominal spending and total nominal income to increase at a predictable rate consistent with an inflation rate low enough to be politically uncontroversial. If such a policy is implemented, with nominal spending and income increasing at roughly the target rate, private expectations would likely converge toward that targeted rate, thereby contributing to the mutual consistency of private expectaions that would allow inflation to remain at an acceptably low rate.

Brad Delong kindly noticed my comment about Blanchard on his substack blog and on Twitter, opining that Blanchard and I were not really disagreeing but were talking past each other.

I don’t necessarily disagree with Brad’s take, but I’m not sure that I agree either, because I’m not sure that I understand what Blanchard is actually saying. I actually tried to hint at my uncertainty about what Blanchard’s argument actually is (and whether I disagree with it) by borrowing (with slight modification) the lyric of George and Ira Gershwin’s standard “Let’s Call the Whole Thing Off.” (Or, try out this version.)

Paul Krugman also weighed in, defending Blanchard’s analysis against the argument which he attributes to John Cochrane and to me that inflation is always the result of excessive demand.

Although Blanchard is nobody’s idea of a leftist (OK, Republicans seem to consider anyone more liberal than Attila the Hun a Marxist, but still), he nonetheless got immediate pushback from economists who insisted that inflation is always the result of excessive demand, of too much money chasing too few goods or, what is roughly the same thing, the consequence of an excessively hot economy.

I’m always grateful to be noticed by Krugman, but I’ll just note in passing that he’s not quite correct in attributing to me the view that inflation is always the consequence of an excessively hot economy; I was simply working with Blanchard’s own framing in his original Twitter thread.

But the point in Krugman’s post that I want to comment on is his football metaphor.

At one level, of course Blanchard is right. Companies that charge higher prices and workers who demand higher wages aren’t doing so because the money supply has increased; they’re trying to increase their incomes (or offset declines in their incomes caused by, say, rising energy prices). And inflation happens when the attempts of firms and workers to claim a bigger share of the economic pie are inconsistent, when the additional purchasing power being demanded exceeds what the economy can deliver.

Reading the discussion, I found myself remembering a remark made way back in the 1970s by William Nordhaus, another eminent economist (and Nobel laureate) who happens to have been my first mentor in the field. Nordhaus compared inflation to what happens in a football stadium when the action on the field is especially exciting. (If you don’t find American football exciting, think of it as a soccer match.) Everyone stands up to get a better view, but this is collectively self-defeating — your view doesn’t improve because the people in front of you are also standing, and you’re less comfortable besides.

Nordhaus’s football metaphor is very apt as far as it goes. You can imagine that inflation starts as the result of an attempt by agents to increase their prices (wages) that turns out to be self-defeating because everyone’s attempt to increase his price or wage relative to everyone else’s turns out to be self-defeating when everyone else does the same thing, so that no one really improves his position compared to everyone else.

I will just observe parenthetically that it is not strictly true that no one improves his view of the field, because people who are taller than average likely will improve their view of the field, especially if they are sitting behind short people. But that is likely a second-order effect. Similarly, some people raising their prices may be well-positioned to increase their prices more than average, so that they may be net gainers from the process. But again those are likely second-order effects.

But here is where the football metaphor breaks down. Blanchard is not worried about a once and for all increase in the price level, which is what the football metaphor translates into. People standing up in a football game do not keep growing taller once they stand up. The process comes to an end, and is eventually reversed after people sit down again.

But inflation is unpopular because it supposedly is a continuing process of increasing prices. Larry Summers and Blanchard have been invoking the experience of the 1970s in which there was supposedly a self-generating or self-reinforcing wage-price spiral that could only be stopped by a brutal monetary tightening administered by Paul Volcker causing a severe recession with double-digit unemployment. To avoid another such catastrophic recession, Blanchard is urging everyone to be reasonable and not to try to increase prices or wages in a likely futile attempt to gain at the expense of others.

The problem with football metaphor is that it can’t explain how the inflation process can continue if it is not enabled by macroeconomic policies that cause the rate of nominal spending and income to keep increasing. Maybe Blanchard and Krugman believe that total nominal spending and total nominal income can keep increasing even if macroeconomic policies aren’t causing nominal spending and nominal income to increase.

I don’t think that’s what they believe, but if they do believe that, then they should explain how continuing increases in nominal spending and income can be generated without corresponding macroeconomic policies that promote those increases in nominal spending and income. As long as macroeconomic policy is focused on keeping the rate of increase in nominal spending at a rate consistent with the target rate of inflation, inflation will be just as transitory as episodes of standing by fans at football games.

UPDATE (9:25am 11/16/2021): Thanks to philipji for catching some problematic passages in my initially posted version. I have also revised the opening paragraph, which was less than clear. Apologies for my sloppy late-night editing before posting.

When I started blogging ten-plus years ago, most of my posts were about monetary policy, because I then felt that the Fed was not doing as much as it could, and should, have been doing to promote a recovery from the Little Depression (aka Great Recession) for which Fed’s policy mistakes bore heavy responsibility. The 2008 financial crisis and the ensuing deep downturn were largely the product of an overly tight monetary policy starting in 2006, and, despite interest-rate cuts in 2007 and 2008, the Fed’s policy consistently erred on the side of tightness because of concerns about rising oil and commodities prices, for almost two months after the start of the crisis. The stance of monetary policy cannot be assessed just by looking at the level of the central bank policy rate; the stance depends on the relationship between the policy rate and the economic conditions at any particular moment. The 2-percent Fed Funds target in the summer of 2008, given economic conditions at the time, meant that monetary policy was tight, not easy.

Although, after the crisis, the Fed never did as much as it could — and should — have to promote recovery, it at least took small measures to avoid a lapse into a ruinous deflation, even as many of the sound-money types, egged on by deranged right-wing scare mongers, warned of runaway inflation.

Slowly but surely, a pathetically slow recovery by the end of Obama’s second term, brought us back to near full employment. By then, my interest in the conduct of monetary policy had given way to a variety of other concerns as we dove into the anni horribiles of the maladministration of Obama’s successor.

Riding a recovery that started seven and a half years before he took office, and buoyed by a right-wing propaganda juggernaut and a pathetically obscene personality cult that broadcast and amplified his brazenly megalomaniacal self-congratulations for the inherited recovery over which he presided, Obama’s successor watched incompetently as the Covid 19 virus spread through the United States, causing the sharpest drop in output and employment in US history.

Ten months after Obama’s successor departed from the White House, the US economy has recovered much, but not all, of the ground lost during the pandemic, employment still below its peak at the start of 2020, and real output still lagging the roughly 2% real growth path along which the economy had been moving for most of the preceding decade.

However, the very rapid increase in output in Q2 2021 and the less rapid, but still substantial, increase in output in Q3 2021, combined with inflation that has risen to the highest rates in 30 years, has provoked ominous warning of resurgent inflation similar to the inflation from the late 1960s till the early 1980s, ending only with the deep 1981-82 recession caused by the resolute anti-inflation policy administered by Fed Chairman Paul Volcker with the backing of the newly elected Ronald Reagan.

It’s worth briefly revisiting that history (which I have discussed previously on this blog here, here, and especially in the following series (1), (2) and (3) from 2020) to understand the nature of the theoretical misunderstanding and the resulting policy errors in the 1970s and 1980s. While I agree that the recent increase in inflation is worrisome, it’s far from clear that inflation is likely, as many now predict, to get worse, although the inflation risk can’t be dismissed.

What I find equally if not more worrisome is that the anti-inflation commentary that we are hearing now from very serious people like Larry Summers in today’s Washington Post is how much it sounds like the inflation talk of 2008, which frightened the Fed, then presided over by a truly eminent economist, Ben Bernanke, into thinking that the chief risk facing the economy was rising headline inflation that would cause inflation expectations to become “unanchored.”

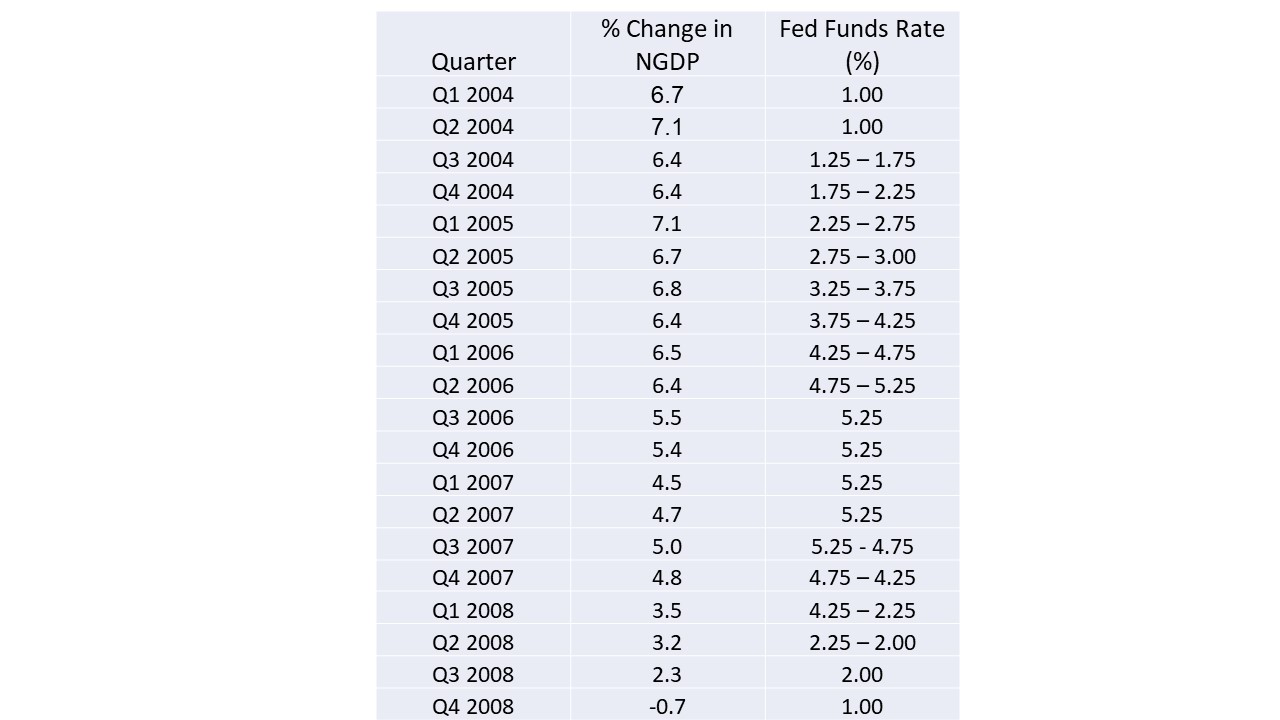

So, rather than provide an economy rapidly sliding into recession, the FOMC, focused on rapid increases in oil and commodity prices, refused to loosen monetary policy in the summer of 2008, even though the pace of growth in nominal gross domestic product (NGDP) had steadily decelerated measured year on year. The accompanying table shows the steady decline in the quarterly year-on-year growth of NGDP in each successive quarter between Q1 2004 and Q4 2008. Between 2004 and 2006, the decline was gradual, but accelerated in 2007 leading to the start of a recession in December 2007.

The decline in the rate of NGDP growth was associated with a gradual increase in the Fed funds target rate from a very low level 1% until Q2 2004, but by Q2 2006, when the rate reached 5%, the slowdown in the growth of total spending quickened. As the rate of spending declined, the Fed eased interest rates in the second half of 2007, but that easing was insufficient to prevent an economy, already suffering financial distress after the the housing bubble burst in 2006, from lapsing into recession.

Although the Fed cut its interest-rate target substantially in March 2008, during the summer of 2008, when the recession was rapidly deteriorating, the FOMC, fearing that inflation expectations would become “unanchored”, given rising headline inflation associated with very large increases in crude-oil prices (which climbed to a record $130 a barrel) and in commodity prices even as the recession was visibly worsening, refused to reduce rates further.

The Fed, to be sure, was confronted with a difficult policy dilemma, but it was a disastrous error to prioritize a speculative concern about the “unanchoring” of long-term inflation expectations over the reality of a fragile and clearly weakening financial system in a contracting economy already clearly in a recession. The Fed made the wrong choice, and the crisis came.

That was then, and now is now. The choices are different, but once again, on one side there is pressure to prioritize the speculative concern about the “unanchoring” of long-term inflation expectations over promoting recovery and increased employment after a a recession and a punishing pandemic. And, once again, the concerns about inflation are driven by a likely transitory increase in the price of crude oil and gasoline prices.

The case for prioritizing fighting inflation was just made by none other than Larry Summers in an op-ed in the Washington Post. Let’s have a look at Summer’s case for fighting inflation now.

Fed Chair Jerome H. Powell’s Jackson Hole speech in late August provided a clear, comprehensive and authoritative statement, enumerated in five pillars, of the widespread team “transitory” view of inflation that prevailed at that time and shaped policy thinking at the central bank and in the administration. Today, all five pillars are wobbly at best.

First, there was a claim that price increases were confined to a few sectors. No longer. In October, prices for commodity goods outside of food and energy rose at more than a 12 percent annual rate. Various Federal Reserve system indexes that exclude sectors with extreme price movements are now at record highs.

Summers has a point. Price increases are spreading throughout the economy. However, that doesn’t mean that increasing oil prices are not causing the prices of many other products to increase as well, inasmuch as oil and other substitute forms of energy are so widely used throughout the economy. If the increase in oil prices, and likely, in food prices, has peaked, or will do so soon, it does not necessarily make sense to fight a war against an enemy that has retreated or is about to do so.

Second, Powell suggested that high inflation in key sectors, such as used cars and durable goods more broadly, was coming under control and would start falling again. In October, used-car prices accelerated to more than a 30 percent annual inflation rate, new cars to a 17 percent rate and household furnishings by an annualized rate of just above 10 percent.

Id.

Again, citing large increases in the price of cars when it’s clear that there are special circumstances causing new car prices to rise rapidly, bringing used-car prices tagging along, is not very persuasive, especially when those special circumstances appear likely to be short-lived. To be sure other durables prices are also rising, but in the absence of a deeper source of inflation, the atmospherics cited by Summers are not that compelling.

Third, the speech pointed out that there was “little evidence of wage increases that might threaten excessive inflation.” This claim is untenable today with vacancy and quit rates at record highs, workers who switch jobs in sectors ranging from fast food to investment banking getting double-digit pay increases, and ominous Employment Cost Index increases.

Id.

Wage increases are usually an indicator of inflation, though, again the withdrawal, permanent or temporary, of many workers from employment in the past two years is a likely cause of increased wages that is independent of an underlying and ongoing inflationary trend.

Fourth, the speech argued that inflation expectations remained anchored. When Powell spoke, market inflation expectations for the term of the next Federal Reserve chair were around 2.5 percent. Now they are about 3.1 percent, up half a percentage point in the past month alone. And consumer sentiment is at a 10-year low due to inflation fears.

Id.

Clearly inflation expectations have increased over the short term for a variety of reasons that we have just been considering. But the curve of inflation expectations still seems to be reverting toward a lower level in the medium term and the long-term.

Fifth, Powell emphasized global deflationary trends. In the same week the United States learned of the fastest annual inflation rate in 30 years, Japan, China and Germany all reported their highest inflation in more than a decade. And the price of oil, the most important global determinant of inflation, is very high and not expected by forward markets to decline rapidly.

Id.

Again, Summers is simply recycling the same argument. We know that there has been a short-term increase in inflation. The question we need to grapple with is whether this short-term inflationary blip is likely to be self-limiting, or will feed on itself, causing inflation expectations to become “unanchored”. Forward prices of oil may not be showing that the price of oil will decline rapidly, but they aren’t showing expectations of further increases. Without further increases in oil prices, it is fair to ask what the source of further, ongoing inflation, that will cause “unanchoring”?

As it has in the past, the threat of “unanchoring”, is doing an awful lot of work. And it is not clear how the work is being done except by way of begging the question that really needs to be answered not begged.

After his windup, Summers offers fairly mild suggestions for his anti-inflation program, and only one of his comments seems mistaken.

Because of inflation, real interest rates are lower, as money is easier than a year ago. The Fed should signal that this is unacceptable and will be reversed.

Id.

The real interest rate about which the Fed should be concerned is the ex ante real interest rate reflecting both the expected yield from real capital and the expected rate of inflation (which may and often does have feedback effects on the expected yield from real capital). Past inflation does not automatically get transformed into an increase in expected inflation, and it is not necessarily the case that past inflation has left the expected yield from real capital unaffected, so Summers’ inference that the recent blip in inflation necessarily implies that monetary policy has been eased could well be mistaken. Yet again, these are judgments (or even guesses) that policymakers have to make about the subjective judgments of market participants. Those are policy judgments that can’t be made simply by reading off a computer screen.

While I’m not overly concerned by Summers’s list of inflation danger signs, there’s no doubt that inflation risk has risen. Yet, at least for now, that risk seems to be manageable. The risk may require the Fed to take pre-emptive measures against inflation down the road, but I don’t think that we have reached that point yet.

The main reason why I think that inflation risk has been overblown is that inflation is a common occurrence in postwar economies, as occurred in the US after both World Wars, and after the Korean War and the Vietnam War. It is widely recognized that war itself is inflationary owing, among other reasons, to the usual practice of governments to finance wartime expenditures by printing money, but inflationary pressures tend to persist even after the wars end.

Why does inflation persist after wars come to an end? The main reason is that, during wartime, resources, labor and capital, are shifted from producing goods for civilian purposes to waging war and producing and transporting supplies to support the war effort. Because total spending, financed by printing money, increases during the war, money income goes up even though the production of goods and services for civilian purposes goes down.

The output of goods and services for civilian purposes having been reduced, the increased money income accruing to the civilian population implies rising prices of the civilian goods and services that are produced. The tendency for prices to rise during wartime is mitigated by the reduced availability of outlets for private spending, people normally postponing much of their non-essential spending while the war is ongoing. Consequently, the public accumulates cash and liquid assets during wartime with the intention of spending the accumulated cash and liquid assets when life returns to normal after the war.

The lack of outlets for private spending is reinforced when, as happened in World War I, World War II, the Korean War and the late stages of the Vietnam War, price controls prevent the prices of civilian goods still being produced from rising, so that consumers can’t buy goods – either at all or as much as they would like – that they would willingly have paid for. The result is suppressed inflation until wartime price controls are lifted, and deferred price increases are allowed to occur. As prices rise, the excess cash that had been accumulated while the goods people demanded were unavailable is absorbed by purchases made at the postponed increases in price.

In his last book, Incomes and Money, Ralph Hawtrey described with characteristic clarity the process by which postwar inflation absorbed redundant cash balances accumulated during the World War II when price controls were lifted.

America, like Britain, had imposed price controls during the war, and had accumulated a great amount of redundant money. So long as the price controls continued, the American manufacturers were precluded from checking demand by raising their prices. But the price controls were abandoned in the latter half of 1946, and there resulted a rise of prices reaching 30 per cent on manufactured goods in the latter part of 1947. That meant that American industry was able to defend itself against the excess demand. By the end of 1947 the rise of prices had nearly eliminated the redundant money; that it to say, the quantity of money (currency and bank deposits) was little more than in a normal proportion to the national income. There was no longer over-employment in American industry, and there was no reluctance to take export orders.

Hawtrey, Incomes and Money, p. 7

Responding to Paul Krugman’s similar claim that there was high inflation following World War II, Summers posted the following twitter thread.

@paulkrugman continues his efforts to minimize the inflation threat to the American economy and progressive politics by pointing to the fact that inflation surged and then there was a year of deflation after World War 2.

If this is the best argument for not being alarmed that someone as smart, rhetorically effective and committed as Paul can make, my anxiety about inflation is increased.

Pervasive price controls were removed after the war. Economists know that measured prices with controls are artificial, so subsequent inflation proves little.

Millions of soldiers were returning home and a massive demobilization was in effect. Nothing like the current pervasive labor shortage was present.

Summers is surely correct that the situation today is not perfectly analogous to the post-WWII situation, but post-WWII inflation, as Hawtrey explained, was only partially attributable to the lifting of price controls. He ignores the effect of excess cash balances, which ultimately had to be spent or somehow withdrawn from circulation through a deliberate policy of deflation, which neither Summers nor most economists would think advisable or even acceptable. While the inflationary effect of absorbing excess cash balances is therefore almost inevitable, the duration of the inflation is limited and need not cause inflation expectations to become “unanchored.”

With the advent of highly effective Covid vaccines, we are now gradually emerging from the worst horrors of the Covid pandemic, when a substantial fraction of the labor force was either laid off or chose to withdraw from employment. As formerly idle workers return to work, we are in a prolonged quasi-postwar situation.

Just as the demand for civilian products declines during wartime, the demand for a broad range of private goods declined during the pandemic as people stopped going to restaurants, going on vacations, attending public gathering, and limited their driving and travel. Thus, the fraction of earnings that was saved increased as outlets for private spending became unavailable, inappropriate or undesirable.

As the pandemic has receded, restoring outlets for private spending, pent-up suppressed private demands have re-emerged, financed by households drawing down accumulated cash balances or drawing on credit lines augmented by paying down indebtedness. For many goods, like cars, the release of pent-up private demand has outpaced the increase in supply, leading to substantial price increases that are unlikely to be sustained once short-term supply bottlenecks are eliminated. But such imbalances between rapid increases in demand and sluggish increases in supply does not seem like a reliable basis on which to make policy choices.

So what are we to do now? As always, Ralph Hawtrey offers the best advice. The control of inflation, he taught, ultimately depends on controlling the relationship between the rate of growth in total nominal spending (and income) and the rate of growth of total real output. If total nominal spending (and income) is increasing faster than the increase in total real output, the difference will be reflected in the prices at which goods and services are provided.

In the five years from 2015 to 2019, the average growth rate in nominal spending (and income) was about 3.9%. During that period the average rate of growth in real output was 2.2% annually and the average rate of inflation was 1.7%. It has been reasonably suggested that extrapolating the 3.9% annual growth in nominal spending in the previous five years provides a reasonable baseline against which to compare actual spending in 2020 and 2021.

Actual nominal spending in Q3 2021 was slightly below what nominal GDP would have been in Q3 if it had continued growing at the extrapolated 3.9% growth path in nominal GDP. But for nominal GDP in Q4 not exceed that extrapolated growth path in Q4, Q4 could increase by an annual rate of no more than 4.3%. Inasmuch as spending in Q3 2021 was growing at 7.8%, the growth rate of nominal spending would have to slow substantially in Q4 from its Q3 growth rate.

But it is not clear that a 3.9% growth rate in nominal spending is the appropriate baseline to use. From 2015 to 2019, the average growth rate in real output was only 2.2% annually and the average inflation rate was only 1.7%. The Fed has long announced that its inflation target was 2% and in the 2015 to 2019 period, it consistently failed to meet that target. If the target inflation was 2% rather than 1.7%, presumably the Fed believed that annual growth would not have been less with 2% inflation than with 1.7%, so there is no reason to believe that the Fed should not have been aiming for more than 3.9% growth in total spending. If so a baseline for extrapolating the growth path for nominal spending should certainly not be less than 4.2%, Even a 4.5% baseline seems reasonable, and a baseline as high as 5% does not seem unreasonable.

With a 5% baseline, total nominal spending in Q4 could increase by as much as 5.4% without raising total nominal spending above its target path. But I think the more important point is not whether total spending does or does not rise above its growth path. The important goal is for the growth in nominal spending to decline steadily toward a reasonable growth path of about 4.5 to 5% and for this goal to be communicated to the public in a convincing manner. The 13.4% increase in total spending in Q2, when it appeared that the pandemic might soon be over, was likely a one-off outlier reflecting the release of pent-up demand. The 7.8% increase in Q3 was excessive, but substantially less than the Q2 rate of increase. If the Q4 increase does not continue downward trend in the rate of increase in nominal spending, it will be time to re-evaluate policy to ensure that the growth of spending is brought down to a non-inflationary range.

UPDATE: Re-upping this slightly revised post from July 11, 2011

Paul Krugman recently gave a lecture “Mr. Keynes and the Moderns” (a play on the title of the most influential article ever written about The General Theory, “Mr. Keynes and the Classics,” by another Nobel laureate J. R. Hicks) at a conference in Cambridge, England commemorating the publication of Keynes’s General Theory 75 years ago. Scott Sumner and Nick Rowe, among others, have already commented on his lecture. Coincidentally, in my previous posting, I discussed the views of Sumner and Krugman on the zero-interest lower bound, a topic that figures heavily in Krugman’s discussion of Keynes and his relevance for our current difficulties. (I note in passing that Krugman credits Brad Delong for applying the term “Little Depression” to those difficulties, a term that I thought I had invented, but, oh well, I am happy to share the credit with Brad).

In my earlier posting, I mentioned that Keynes’s, slightly older, colleague A. C. Pigou responded to the zero-interest lower bound in his review of The General Theory. In a way, the response enhanced Pigou’s reputation, attaching his name to one of the most famous “effects” in the history of economics, but it made no dent in the Keynesian Revolution. I also referred to “the layers upon layers of interesting personal and historical dynamics lying beneath the surface of Pigou’s review of Keynes.” One large element of those dynamics was that Keynes chose to make, not Hayek or Robbins, not French devotees of the gold standard, not American laissez-faire ideologues, but Pigou, a left-of-center social reformer, who in the early 1930s had co-authored with Keynes a famous letter advocating increased public-works spending to combat unemployment, the main target of his immense rhetorical powers and polemical invective. The first paragraph of Pigou’s review reveals just how deeply Keynes’s onslaught had wounded Pigou.

When in 1919, he wrote The Economic Consequences of the Peace, Mr. Keynes did a good day’s work for the world, in helping it back towards sanity. But he did a bad day’s work for himself as an economist. For he discovered then, and his sub-conscious mind has not been able to forget since, that the best way to win attention for one’s own ideas is to present them in a matrix of sarcastic comment upon other people. This method has long been a routine one among political pamphleteers. It is less appropriate, and fortunately less common, in scientific discussion. Einstein actually did for Physics what Mr. Keynes believes himself to have done for Economics. He developed a far-reaching generalization, under which Newton’s results can be subsumed as a special case. But he did not, in announcing his discovery, insinuate, through carefully barbed sentences, that Newton and those who had hitherto followed his lead were a gang of incompetent bunglers. The example is illustrious: but Mr. Keynes has not followed it. The general tone de haut en bas and the patronage extended to his old master Marshall are particularly to be regretted. It is not by this manner of writing that his desire to convince his fellow economists is best promoted.

Krugman acknowledges Keynes’s shady scholarship (“I know that there’s dispute about whether Keynes was fair in characterizing the classical economists in this way”), only to absolve him of blame. He then uses Keynes’s example to attack “modern economists” who deny that a failure of aggregate demand can cause of mass unemployment, offering up John Cochrane and Niall Ferguson as examples, even though Ferguson is a historian not an economist.

Krugman also addresses Robert Barro’s assertion that Keynes’s explanation for high unemployment was that wages and prices were stuck at levels too high to allow full employment, a problem easily solvable, in Barro’s view, by monetary expansion. Although plainly annoyed by Barro’s attempt to trivialize Keynes’s contribution, Krugman never addresses the point squarely, preferring instead to justify Keynes’s frustration with those (conveniently nameless) “classical economists.”

Keynes’s critique of the classical economists was that they had failed to grasp how everything changes when you allow for the fact that output may be demand-constrained.

Not so, as I pointed out in my first post. Frederick Lavington, an even more orthodox disciple than Pigou of Marshall, had no trouble understanding that “the inactivity of all is the cause of the inactivity of each.” It was Keynes who failed to see that the failure of demand was equally a failure of supply.

They mistook accounting identities for causal relationships, believing in particular that because spending must equal income, supply creates its own demand and desired savings are automatically invested.

Supply does create its own demand when economic agents succeed in executing their plans to supply; it is when, owing to their incorrect and inconsistent expectations about future prices, economic agents fail to execute their plans to supply, that both supply and demand start to contract. Lavington understood that; Pigou understood that. Keynes understood it, too, but believing that his new way of understanding how contractions are caused was superior to that of his predecessors, he felt justified in misrepresenting their views, and attributing to them a caricature of Say’s Law that they would never have taken seriously.

And to praise Keynes for understanding the difference between accounting identities and causal relationships that befuddled his predecessors is almost perverse, as Keynes’s notorious confusion about whether the equality of savings and investment is an equilibrium condition or an accounting identity was pointed out by Dennis Robertson, Ralph Hawtrey and Gottfried Haberler within a year after The General Theory was published. To quote Robertson:

(Mr. Keynes’s critics) have merely maintained that he has so framed his definition that Amount Saved and Amount Invested are identical; that it therefore makes no sense even to inquire what the force is which “ensures equality” between them; and that since the identity holds whether money income is constant or changing, and, if it is changing, whether real income is changing proportionately, or not at all, this way of putting things does not seem to be a very suitable instrument for the analysis of economic change.

It just so happens that in 1925, Keynes, in one of his greatest pieces of sustained, and almost crushing sarcasm, The Economic Consequences of Mr. Churchill, offered an explanation of high unemployment exactly the same as that attributed to Keynes by Barro. Churchill’s decision to restore the convertibility of sterling to gold at the prewar parity meant that a further deflation of at least 10 percent in wages and prices would be necessary to restore equilibrium. Keynes felt that the human cost of that deflation would be intolerable, and held Churchill responsible for it.

Of course Keynes in 1925 was not yet the Keynes of The General Theory. But what historical facts of the 10 years following Britain’s restoration of the gold standard in 1925 at the prewar parity cannot be explained with the theoretical resources available in 1925? The deflation that began in England in 1925 had been predicted by Keynes. The even worse deflation that began in 1929 had been predicted by Ralph Hawtrey and Gustav Cassel soon after World War I ended, if a way could not be found to limit the demand for gold by countries, rejoining the gold standard in aftermath of the war. The United States, holding 40 percent of the world’s monetary gold reserves, might have accommodated that demand by allowing some of its reserves to be exported. But obsession with breaking a supposed stock-market bubble in 1928-29 led the Fed to tighten its policy even as the international demand for gold was increasing rapidly, as Germany, France and many other countries went back on the gold standard, producing the international credit crisis and deflation of 1929-31. Recovery came not from Keynesian policies, but from abandoning the gold standard, thereby eliminating the deflationary pressure implicit in a rapidly rising demand for gold with a more or less fixed total supply.

Keynesian stories about liquidity traps and Monetarist stories about bank failures are epiphenomena obscuring rather than illuminating the true picture of what was happening. The story of the Little Depression is similar in many ways, except the source of monetary tightness was not the gold standard, but a monetary regime that focused attention on rising price inflation in 2008 when the appropriate indicator, wage inflation, had already started to decline.

I indicated in my first posting on Tuesday that I was going to comment on some recent comparisons between the current anemic recovery and earlier more robust recoveries since World War II. The comparison that I want to perform involves some simple econometrics, and it is taking longer than anticipated to iron out the little kinks that I keep finding. So I will have to put off that discussion a while longer. As a diversion, I will follow up on a point that Scott Sumner made in discussing Paul Krugman’s reasoning for having favored fiscal policy over monetary policy to lead us out of the recession.

Scott’s focus is on the factual question whether it is really true, as Krugman and Michael Woodford have claimed, that a monetary authority, like, say, the Bank of Japan, may simply be unable to create the inflation expectations necessary to achieve equilibrium, given the zero-interest-rate lower bound, when the equilibrium real interest rate is less than zero. Scott counters that a more plausible explanation for the inability of the Bank of Japan to escape from a liquidity trap is that its aversion to inflation is so well-known that it becomes rational for the public to expect that the Bank of Japan would not permit the inflation necessary for equilibrium.

It seems that a lot of people have trouble understanding the idea that there can be conditions in which inflation — or, to be more precise, expected inflation — is necessary for a recovery from a depression. We have become so used to thinking of inflation as a costly and disruptive aspect of economic life, that the notion that inflation may be an integral element of an economic equilibrium goes very deeply against the grain of our intuition.

The theoretical background of this point actually goes back to A. C. Pigou (another famous Cambridge economist, Alfred Marshall’s successor) who, in his 1936 review of Keynes’s General Theory, referred to what he called Mr. Keynes’s vision of the day of judgment, namely, a situation in which, because of depressed entrepreneurial profit expectations or a high propensity to save, macro-equilibrium (the equality of savings and investment) would correspond to a level of income and output below the level consistent with full employment.

The “classical” or “orthodox” remedy to such a situation was to reduce the rate of interest, or, as the British say “Bank Rate” (as in “Magna Carta” with no definite article) at which the Bank of England lends to its customers (mainly banks). But if entrepreneurs are so pessimistic, or households so determined to save rather than consume, an equilibrium corresponding to a level of income and output consistent with full employment could, in Keynes’s ghastly vision, only come about with a negative interest rate. Now a zero interest rate in economics is a little bit like the speed of light in physics; all kinds of crazy things start to happen if you posit a negative interest rate and it seems inconsistent with the assumptions of rational behavior to assume that people would lend for a negative interest when they could simply hold the money already in their pockets. That’s why Pigou’s metaphor was so powerful. There are layers upon layers of interesting personal and historical dynamics lying beneath the surface of Pigou’s review of Keynes, but I won’t pursue that tangent here, tempting though it would be to go in that direction.

The conclusion that Keynes drew from his model is the one that we all were taught in our first course in macro and that Paul Krugman holds close to his heart, the government can come to the rescue by increasing its spending on whatever, thereby increasing aggregate demand, raising income and output up to the level consistent with full employment. But Pigou, whose own policy recommendations were not much different from those of Keynes, felt that Keynes had left out an important element of the model in his discussion. As a matter of logic, which to Pigou was as, or more important than, policy, an economy confronting Keynes’s day of judgment would not forever be stuck in “underemployment equilibrium” just because the rate of interest could not fall to the (negative) level required for full employment.

Rather, Pigou insisted, at least in theory, though not necessarily in practice, deflation, resulting from unemployed workers bidding down wages to gain employment, would raise the real value of the money supply (fixed in nominal terms in Keynes’s model) thereby generating a windfall to holders of money, inducing them to increase consumption, raising aggregate demand and eventually restoring full employment. Discussion of the theoretical validity and policy relevance of what came to be known as the Pigou effect (or, occasionally, as the Pigou-Haberler Effect, or even the Pigou-Haberler-Scitovsky effect) became a really big deal in macroeconomics in the 1940s and 1950s and was still being taught in the 1960s and 1970s.

What seems remarkable to me now about that whole episode is that the analysis simply left out the possibility that the zero-interest-rate lower bound becomes irrelevant if the expected rate of inflation exceeds the putative negative equilibrium real interest rate that would hypothetically generate a macro-equilibrium at a level of income and output consistent with full employment.

If only Pigou had corrected the logic of Keynes’s model by positing an expected rate of inflation greater than the negative real interest rate rather than positing a process of deflation to increase the real value of the money stock, how different would the course of history and the development of macroeconomics and monetary theory have been.

One economist who did think about the expected rate of inflation as an equilibrating variable in a macroeconomic model was one of my teachers, the late, great Earl Thompson, who introduced the idea of an equilibrium rate of inflation in his remarkable unpublished paper, “A Reformulation of Macreconomic Theory.” If inflation is an equilibrating variable, then it cannot make sense for monetary authorities to commit themselves to a single unvarying target for the rate of inflation. Under certain circumstances, macroeconomic equilibrium may be incompatible with a rate of inflation below some minimum level. Has it occurred to the inflation hawks on the FOMC and their supporters that the minimum rate of inflation consistent with equilibrium is above the 2 percent rate that Fed has now set as its policy goal?

One final point, which I am still trying to work out more coherently, is that it really may not be appropriate to think of the real rate of interest and the expected rate of inflation as being determined independently of each other. They clearly interact. As I point out in my paper “The Fisher Effect Under Deflationary Expectations,” increasing the expected rate of inflation when the real rate of interest is very low or negative tends to increase not just the nominal rate, but the real rate as well, by generating the positive feedback effects on income and employment that result when a depressed economy starts to expand.

With unemployment at the lowest levels since the start of the millennium (initial unemployment claims in February were the lowest since 1973!), lots of people are starting to wonder if we might be headed for a pick-up in the rate of inflation, which has been averaging well under 2% a year since the financial crisis of September 2008 ushered in the Little Depression of 2008-09 and beyond. The Fed has already signaled its intention to continue raising interest rates even though inflation remains well anchored at rates below the Fed’s 2% target. And among Fed watchers and Fed cognoscenti, the only question being asked is not whether the Fed will raise its Fed Funds rate target, but how frequent those (presumably) quarter-point increments will be.

The prevailing view seems to be that the thought process of the Federal Open Market Committee (FOMC) in raising interest rates — even before there is any real evidence of an increase in an inflation rate that is still below the Fed’s 2% target — is that a preemptive strike is required to prevent inflation from accelerating and rising above what has become an inflation ceiling — not an inflation target — of 2%.

Why does the Fed believe that inflation is going to rise? That’s what the econoblogosphere has, of late, been trying to figure out. And the consensus seems to be that the FOMC is basing its assessment that the risk that inflation will break the 2% ceiling that it has implicitly adopted has become unacceptably high. That risk assessment is based on some sort of analysis in which it is inferred from the Phillips Curve that, with unemployment nearing historically low levels, rising inflation has become dangerously likely. And so the next question is: why is the FOMC fretting about the Phillips Curve?

In a blog post earlier this week, David Andolfatto of the St. Louis Federal Reserve Bank, tried to spell out in some detail the kind of reasoning that lay behind the FOMC decision to actively tighten the stance of monetary policy to avoid any increase in inflation. At the same time, Andolfatto expressed his own view, that the rate of inflation is not determined by the rate of unemployment, but by the stance of monetary policy.

Andolfatto’s avowal of monetarist faith in the purely monetary forces that govern the rate of inflation elicited a rejoinder from Paul Krugman expressing considerable annoyance at Andolfatto’s monetarism.

Here are three questions about inflation, unemployment, and Fed policy. Some people may imagine that they’re the same question, but they definitely aren’t:

Does the Fed know how low the unemployment rate can go?

Should the Fed be tightening now, even though inflation is still low?

Is there any relationship between unemployment and inflation?

It seems obvious to me that the answer to (1) is no. We’re currently well above historical estimates of full employment, and inflation remains subdued. Could unemployment fall to 3.5% without accelerating inflation? Honestly, we don’t know.

Agreed.

I would also argue that the Fed is making a mistake by tightening now, for several reasons. One is that we really don’t know how low U can go, and won’t find out if we don’t give it a chance. Another is that the costs of getting it wrong are asymmetric: waiting too long to tighten might be awkward, but tightening too soon increases the risks of falling back into a liquidity trap. Finally, there are very good reasons to believe that the Fed’s 2 percent inflation target is too low; certainly the belief that it was high enough to make the zero lower bound irrelevant has been massively falsified by experience.

Agreed, but the better approach would be to target the price level, or even better nominal GDP, so that short-term undershooting of the inflation target would provide increased leeway to allow inflation to overshoot the inflation target without undermining the credibility of the commitment to price stability.

But should we drop the whole notion that unemployment has anything to do with inflation? Via FTAlphaville, I see that David Andolfatto is at it again, asserting that there’s something weird about asserting an unemployment-inflation link, and that inflation is driven by an imbalance between money supply and money demand.

But one can fully accept that inflation is driven by an excess supply of money without denying that there is a link between inflation and unemployment. In the normal course of events an excess supply of money may lead to increased spending as people attempt to exchange their excess cash balances for real goods and services. The increased spending can induce additional output and additional employment along with rising prices. The reverse happens when there is an excess demand for cash balances and people attempt to build up their cash holdings by cutting back their spending, reducing output. So the inflation unemployment relationship results from the effects induced by a particular causal circumstance. Nor does that mean that an imbalance in the supply of money is the only cause of inflation or price level changes.

Inflation can also result from nothing more than the anticipation of inflation. Expected inflation can also affect output and employment, so inflation and unemployment are related not only by both being affected by excess supply of (demand for) money, but by both being affect by expected inflation.

Even if you think that inflation is fundamentally a monetary phenomenon (which you shouldn’t, as I’ll explain in a minute), wage- and price-setters don’t care about money demand; they care about their own ability or lack thereof to charge more, which has to – has to – involve the amount of slack in the economy. As Karl Smith pointed out a decade ago, the doctrine of immaculate inflation, in which money translates directly into inflation – a doctrine that was invoked to predict inflationary consequences from Fed easing despite a depressed economy – makes no sense.

There’s no reason for anyone to care about overall money demand in this scenario. Price setters respond to the perceived change in the rate of spending induced by an excess supply of money. (I note parenthetically, that I am referring now to an excess supply of base money, not to an excess supply of bank-created money, which, unlike base money, is not a hot potato that cannot be withdrawn from circulation in response to market incentives.) Now some price setters may actually use macroeconomic information to forecast price movements, but recognizing that channel would take us into the realm of an expectations-theory of inflation, not the strict monetary theory of inflation that Krugman is criticizing.

And the claim that there’s weak or no evidence of a link between unemployment and inflation is sustainable only if you insist on restricting yourself to recent U.S. data. Take a longer and broader view, and the evidence is obvious.

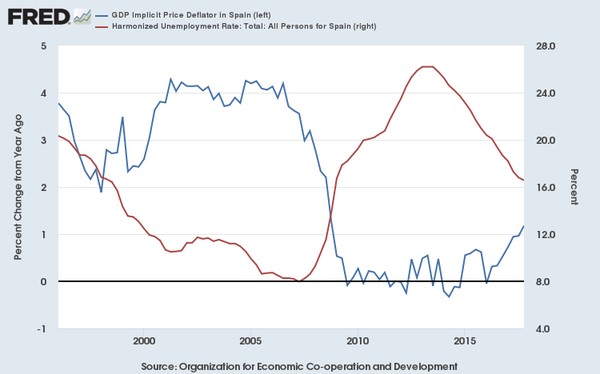

Consider, for example, the case of Spain. Inflation in Spain is definitely not driven by monetary factors, since Spain hasn’t even had its own money since it joined the euro. Nonetheless, there have been big moves in both Spanish inflation and Spanish unemployment:

That period of low unemployment, by Spanish standards, was the result of huge inflows of capital, fueling a real estate bubble. Then came the sudden stop after the Greek crisis, which sent unemployment soaring.

Meanwhile, the pre-crisis era was marked by relatively high inflation, well above the euro-area average; the post-crisis era by near-zero inflation, below the rest of the euro area, allowing Spain to achieve (at immense cost) an “internal devaluation” that has driven an export-led recovery.

So, do you really want to claim that the swings in inflation had nothing to do with the swings in unemployment? Really, really?

No one claims – at least no one who believes in a monetary theory of inflation — should claim that swings in inflation and unemployment are unrelated, but to acknowledge the relationship between inflation and unemployment does not entail acceptance of the proposition that unemployment is a causal determinant of inflation.

But if you concede that unemployment had a lot to do with Spanish inflation and disinflation, you’ve already conceded the basic logic of the Phillips curve. You may say, with considerable justification, that U.S. data are too noisy to have any confidence in particular estimates of that curve. But denying that it makes sense to talk about unemployment driving inflation is foolish.

No it’s not foolish, because the relationship between inflation and unemployment is not a causal relationship; it’s a coincidental relationship. The level of employment depends on many things and some of the things that employment depends on also affect inflation. That doesn’t mean that employment causally affects inflation.

When I read Krugman’s post and the Andalfatto post that provoked Krugman, it occurred to me that the way to summarize all of this is to say that unemployment and inflation are determined by a variety of deep structural (causal) relationships. The Phillips Curve, although it was once fashionable to refer to it as the missing equation in the Keynesian model, is not a structural relationship; it is a reduced form. The negative relationship between unemployment and inflation that is found by empirical studies does not tell us that high unemployment reduces inflation, any more than a positive empirical relationship between the price of a commodity and the quantity sold would tell you that the demand curve for that product is positively sloped.

It may be interesting to know that there is a negative empirical relationship between inflation and unemployment, but we can’t rely on that relationship in making macroeconomic policy. I am not a big admirer of the Lucas Critique for reasons that I have discussed in other posts (e.g., here and here). But, the Lucas Critique, a rather trivial result that was widely understood even before Lucas took ownership of the idea, does at least warn us not to confuse a reduced form with a causal relationship.

Scott Sumner wrote a post commenting on my previous post about Paul Krugman’s column in the New York Times last Friday. I found Krugman’s column really interesting in his ability to pack so much real economic content into an 800-word column written to help non-economists understand recent fluctuations in the stock market. Part of what I was doing in my post was to offer my own criticism of the efficient market hypothesis (EMH) of which Krugman is probably not an enthusiastic adherent either. Nevertheless, both Krugman and I recognize that EMH serves as a useful way to discipline how we think about fluctuating stock prices.

Here is a passage of Krugman’s that I commented on:

But why are long-term interest rates so low? As I argued in my last column, the answer is basically weakness in investment spending, despite low short-term interest rates, which suggests that those rates will have to stay low for a long time.

My comment was:

Again, this seems inexactly worded. Weakness in investment spending is a symptom not a cause, so we are back to where we started from. At the margin, there are no attractive investment opportunities.

Scott had this to say about my comment:

David is certainly right that Krugman’s statement is “inexactly worded”, but I’m also a bit confused by his criticism. Certainly “weakness in investment spending” is not a “symptom” of low interest rates, which is how his comment reads in context. Rather I think David meant that the shift in the investment schedule is a symptom of a low level of AD, which is a very reasonable argument, and one he develops later in the post. But that’s just a quibble about wording. More substantively, I’m persuaded by Krugman’s argument that weak investment is about more than just AD; the modern information economy (with, I would add, a slowgrowing working age population) just doesn’t generate as much investment spending as before, even at full employment.

Just to be clear, what I was trying to say was that investment spending is determined by “fundamentals,” i.e., expectations about future conditions (including what demand for firms’ output will be, what competing firms are planning to do, what cost conditions will be, and a whole range of other considerations. It is the combination of all those real and psychological factors that determines the projected returns from undertaking an investment, and those expected returns must be compared with the cost of capital to reach a final decision about which projects will be undertaken, thereby giving rise to actual investment spending. So I certainly did not mean to say that weakness in investment spending is a symptom of low interest rates. I meant that it is a symptom of the entire economic environment that, depending on the level of interest rates, makes specific investment projects seem attractive or unattractive. Actually, I don’t think that there is any real disagreement between Scott and me on this particular point; I just mention the point to avoid possible misunderstandings.

But the differences between Scott and me about the EMH seem to be substantive. Scott quotes this passage from my previous post:

The efficient market hypothesis (EMH) is at best misleading in positing that market prices are determined by solid fundamentals. What does it mean for fundamentals to be solid? It means that the fundamentals remain what they are independent of what people think they are. But if fundamentals themselves depend on opinions, the idea that values are determined by fundamentals is a snare and a delusion.

Scott responded as follows:

I don’t think it’s correct to say the EMH is based on “solid fundamentals”. Rather, AFAIK, the EMH says that asset prices are based on rational expectations of future fundamentals, what David calls “opinions”. Thus when David tries to replace the EMH view of fundamentals with something more reasonable, he ends up with the actual EMH, as envisioned by people like Eugene Fama. Or am I missing something?

In fairness, David also rejects rational expectations, so he would not accept even my version of the EMH, but I think he’s too quick to dismiss the EMH as being obviously wrong. Lots of people who are much smarter than me believe in the EMH, and if there was an obvious flaw I think it would have been discovered by now.

I accept Scott’s correction that EMH is based on the rational expectation of future fundamentals, but I don’t think that the distinction is as meaningful as Scott does. The problem is that in a typical rational-expectations model, the fundamentals are given and don’t change, so that fundamentals are actually static. The seemingly non-static property of a rational-expectations model is achieved by introducing stochastic parameters with known means and variances, so that the ultimate realizations of stochastic variables within the model are not known in advance. However, the rational expectations of all stochastic variables are unbiased, and they are – in some sense — the best expectations possible given the underlying stochastic nature of the variables. But given that stochastic structure, current asset prices reflect the actual – and unchanging — fundamentals, the stochastic elements in the model being fully reflected in asset prices today. Prices may change ex post, but, conditional on the realizations of the stochastic variables (whose probability distributions are assumed to have been known in advance), those changes are fully anticipated. Thus, in a rational-expectations equilibrium, causation still runs from fundamentals to expectations.

The problem with rational expectations is not a flaw in logic. In fact, the importance of rational expectations is that it is a very important logical test for the coherence of a model. If a model cannot be solved for a rational-expectations equilibrium, it suffers from a basic lack of coherence. Something is basically wrong with a model in which the expectation of the equilibrium values predicted by the model does not lead to their realization. But a logical property of the model is not the same as a positive theory of how expectations are formed and how they evolve. In the real world, knowledge is constantly growing, and new knowledge implies that the fundamentals underlying the economy must be changing as knowledge grows. The future fundamentals that will determine the future prices of a future economy cannot be rationally expected in the present, because we have no way of specifying probability distributions corresponding to dynamic evolving systems.

If future fundamentals are logically unknowable — even in a probabilistic sense — in the present, because we can’t predict what our future knowledge will be, because if we could, future knowledge would already be known, making it present knowledge, then expectations of the future can’t possibly be rational because we never have the knowledge that would be necessary to form rational expectations. And so I can’t accept Scott’s assertion that asset prices are based on rational expectations of future fundamentals. It seems to me that the causation goes in the other direction as well: future fundamentals will be based, at least in part, on current expectations.

Paul Krugman has a nice column today warning us that the recent record highs in the stock market indices don’t mean that happy days are here again. While I agree with much of what he says, I don’t agree with all of it, so let me try to sort out what I think is right and what I think may not be right.

Like most economists, I don’t usually have much to say about stocks. Stocks are even more susceptible than other markets to popular delusions and the madness of crowds, and stock prices generally have a lot less to do with the state of the economy or its future prospects than many people believe.

I think that’s generally right. The efficient market hypothesis (EMH) is at best misleading in positing that market prices are determined by solid fundamentals. What does it mean for fundamentals to be solid? It means that the fundamentals remain what they are independent of what people think they are. But if fundamentals themselves depend on opinions, the idea that values are determined by fundamentals is a snare and a delusion. So the fundamental idea on which the EMH is premised that there are fundamentals is itself fundamentally wrong. Fundamentals are no more than conjectures and psychologically flimsy perceptions, and individual perceptions are themselves very much influenced by how other people perceive the world and their perceptions. That’s why fads are contagious and bubbles can arise. But because fundamentals are nothing but opinions, expectations can be self-fulfilling. So it is possible for some ex ante bubbles to wind up being justified ex post, but only because expectations can be self-fulfilling.

Still, we shouldn’t completely ignore stock prices. The fact that the major averages have lately been hitting new highs — the Dow has risen 177 percent from its low point in March 2009 — is newsworthy and noteworthy. What are those Wall Street indexes telling us?

Stock prices are in fact governed by expectations, but expectations may or may not be rational, where a rational expectation is an expectation that could actually be realized in some possible state of the world.

The answer, I’d suggest, isn’t entirely positive. In fact, in some ways the stock market’s gains reflect economic weaknesses, not strengths. And understanding how that works may help us make sense of the troubling state our economy is in. . . .

The truth . . . is that there are three big points of slippage between stock prices and the success of the economy in general. First, stock prices reflect profits, not overall incomes. Second, they also reflect the availability of other investment opportunities — or the lack thereof. Finally, the relationship between stock prices and real investment that expands the economy’s capacity has gotten very tenuous.

To put this into the slightly different language of basic financial theory, stock prices reflect the expected future cash flows from owning shares of publicly traded corporations. So stock prices reflect the net value of the tangible and intangible capital assets of these corporations. The public valuations of those assets reflected in stock prices reflect expectations about the future income streams associated with those assets, but those expected future income streams must be discounted so that they can be expressed as a present value. The rate at which future income streams are discounted into the present represents what Krugman calls “the availability of other investment opportunities.” If lots of good investment opportunities are available, then future income streams will be discounted at a higher rate than if there aren’t so many good investment opportunities. In theory the discount rate at which future income streams are discounted would reflect the rate of return corresponding to the marginal investment opportunities that are on the verge of being adopted or abandoned, because they just break even. What Krugman means by the tenuous relationship between stock prices and real investment that expands the economy’ capacity will have to be considered below.

Krugman maintains that, over the past two decades, even though the economy as a whole has not done all that well, stock prices have increased a lot, because the share of capital in total GDP has increased at the expense of labor. He also points out that the low — even negative — real interest rates on government bonds are indicative of the poor opportunities now available (at the margin) to investors.

And these days those options [“for converting money today into income tomorrow”] are pretty poor, with interest rates on long-term government bonds not only very low by historical standards but zero or negative once you adjust for inflation. So investors are willing to pay a lot for future income, hence high stock prices for any given level of profits.

Two points should be noted here. First, scare talk about low interest rates causing bubbles because investors search for yield is nonsense. Even in a fundamentalist EMH universe, a deterioration of marginal investment opportunities causing a drop in the real interest rate will, for given expectations of future income streams, imply that the present value of the assets generating those streams would rise. Rising asset prices in such circumstances are totally rational, which is exactly what bubbles are not. Second, the low interest rates on long-term government bonds are not the cause of poor investment opportunities but the result of poor investment opportunities. Krugman certainly understands that, but many of his readers might not.

But why are long-term interest rates so low? As I argued in my last column, the answer is basically weakness in investment spending, despite low short-term interest rates, which suggests that those rates will have to stay low for a long time.

Again, this seems inexactly worded. Weakness in investment spending is a symptom not a cause, so we are back to where we started from. At the margin, there are no attractive investment opportunities. The mystery deepens:

This may seem, however, to present a paradox. If the private sector doesn’t see itself as having a lot of good investment opportunities, how can profits be so high? The answer, I’d suggest, is that these days profits often seem to bear little relationship to investment in new capacity. Instead, profits come from some kind of market power — brand position, the advantages of an established network, or good old-fashioned monopoly. And companies making profits from such power can simultaneously have high stock prices and little reason to spend.

Why do profits bear only a weak relationship to investment in new capacity? Krugman suggests that the cause is that rising profits are due to the exercise of market power, firms increasing profits not by increasing output, but by restricting output to raise prices (not necessarily in absolute terms but relative to costs). This is a kind of microeconomic explanation of a macroeconomic phenomenon, which does not necessarily make it wrong, but it is a somewhat anomalous argument for a Keynesian. Be that as it may, to be credible such an argument must explain how the share of corporate profits in total income has been able to grow steadily for nearly twenty years. What would account for a steady economy-wide increase in the market power of corporations lasting for two decades?

Consider the fact that the three most valuable companies in America are Apple, Google and Microsoft. None of the three spends large sums on bricks and mortar. In fact, all three are sitting on huge reserves of cash. When interest rates go down, they don’t have much incentive to spend more on expanding their businesses; they just keep raking in earnings, and the public becomes willing to pay more for a piece of those earnings.

Krugman’s example suggests that the continuing increase in market power, if that is what has been happening, has been structural. By structural I mean that much of the growth in the economy over the past two decades has been in sectors characterized by strong network effects or aggressive enforcement of intellectual property rights. Network effects and strong intellectual property rights tend to create, enhance, and entrench market power, supporting very large gaps between prices and variable costs, which is the standard metric for identifying exercises of market power. The nature of what these companies offer consumers is such that their marginal cost of production is very low, so that reducing price and expanding output would not require a substantial increase in their demand for inputs (at least compared to other industries with higher marginal costs), but would cause a big loss of profit.

But I would suggest looking at the problem from a different perspective, using the distinction between two kinds of capital investment proposed by Ralph Hawtrey. One kind of investment is capital deepening, which involves an increase in the capital intensity of production, the idea being to reduce the cost of production by installing new or better equipment to economize on other inputs (usually labor); the other kind of investment is capital widening, which involves an increase in the scale of output but not in capital intensity, for example building a new plant or expanding an existing one. Capital deepening tends to reduce the demand for labor while capital widening tends to increase it.

More of the investment now being undertaken may be of the capital-deepening sort than has been true historically. Aside from the structural shifts mentioned above, the reduction in capital-widening investment may be the result of declining optimism by businesses in their projections about future demand for their products, making capital-widening investments seem less profitable. For the economy as a whole, a decline in optimism about future demand may turn out to be self-fulfilling. Thus, an increasing share of total investment has become capital-deepening and a declining share capital-widening. But for the economy as a whole, this self-fulfilling pessimism implies that total investment declines. The question is whether monetary (or fiscal) policy could now do anything to increase expectations of future demand sufficiently to induce an self-fulfilling increase in optimism and in capital-widening investment.

Mervyn King, former Governor of the Bank of England, and professor of economics at LSE, recently published a book, The End of Alchemy, containing his reflections on the current state of economic theory and policy from the special vantage point of someone who has been a practitioner of both callings at the highest levels. Paul Krugman has a review of King’s book in the current edition of the New York Review of Books. Krugman points out that King’s tenure at the Bank of England coincided with that of Ben Bernanke, also an academic economist of some renown before embarking on a second career as a central banker, and who has also published a book about his experience as a central banker. A quick check of the Wikipedia article about King reveals a fact left unmentioned by Krugman: that while a Kennedy Scholar at MIT in the late 1970s, King actually shared an office with the young Ben Bernanke who was then working on his Ph. D. at MIT.

In his review, Krugman observes that, unlike Bernanke’s recent memoir, King’s book is less an account of his tenure as a central banker during the 2008 financial crisis and its aftermath than it is a “meditation on monetary theory and the methodology of economics.” Here’s how Krugman describes King’s book.

Now King, like Bernanke, has written a book inspired by his experiences. But it’s not at all the book one might have expected. It’s not a play-by-play of the crisis, or a tell-all, or a personal memoir. In fact, King not-so-subtly mocks the authors of such books, which “share the same invisible subtitle: ‘how I saved the world.’”

King’s book is, instead, devoted to “economic ideas.” It is rich in wide-ranging historical detail, with many stories I didn’t know—the desperate shortage of banknotes at the outbreak of World War I, the remarkable emergence of the “Swiss dinar” (old Iraqi notes printed from Swiss plates) in Kurdistan. But it is mainly an extended meditation on monetary theory and the methodology of economics.

And a fascinating meditation it is. As I’ll explain shortly, King takes sides in a long-running dispute between mainstream economic analysis and a more or less radical fringe that rejects the mainstream’s methods—and comes down on the side of the radical fringe. The policy implications of his methodological radicalism aren’t as clear or, I’d argue, as persuasive as one might like, but he definitely challenges policy as well as research orthodoxy.

You don’t have to agree with everything King says—and I don’t—to be impressed by his willingness to let his freak flag fly. His assertion that we haven’t done nearly enough to head off the next financial crisis will, I think, receive wide assent; I don’t know anyone who thinks, for example, that the US financial reforms enacted in 2010 were sufficient. But his assertion that the whole intellectual frame we’ve been using is more or less irreparably flawed is a brave position that should produce a lot of soul-searching among both economists and policy officials.

I don’t want to discuss Krugman’s review in detail, but I was struck by a passage toward the end of the review in which Krugman takes issue with King’s rather pessimistic assessment of the possibility that central bankers or economic policy makers can do much to improve an economy that is underperforming.

In any case, King’s policy proposals don’t stop with banking reform. He also weighs in on macroeconomic policy, on how to fight the economic weakness that has persisted long after the acute phase of the financial crisis ended. He dismisses talk of demographic and other “headwinds”—such as an aging population—that may be holding the economy back. What has happened, he declares, is a change in the narrative that consumers are telling themselves to a story far more pessimistic about what the future might hold, leading them to spend less year after year. And then a funny thing happens: his radical views on economics lead him to what would ordinarily be considered conservative, even boringly orthodox policy recommendations.

The conventional Keynesian view . . . is that what we need in the face of persistent weakness is policies to boost demand. Keep interest rates low, and maybe raise inflation targets to further encourage people to spend rather than hoard. Have government take advantage of incredibly low interest rates by borrowing and spending on much-needed infrastructure. Offer relief to individuals and nations crippled by debt. And so on.

King is, however, having none of it. Under his leadership, the Bank of England was aggressively engaged in monetary easing by keeping interest rates low—the bank was as aggressive in this respect or even more so than the Bernanke Fed. Now, however, King seems to condemn his old policies:

Monetary stimulus via low interest rates works largely by giving incentives to bring forward spending from the future to the present. But this is a short-term effect. After a time, tomorrow becomes today. Then we have to repeat the exercise and bring forward spending from the new tomorrow to the new today. As time passes, we will be digging larger and larger holes in future demand. The result is a self-reinforcing path of weak growth in the economy.