UPDATE (9:25am 11/16/2021): Thanks to philipji for catching some problematic passages in my initially posted version. I have also revised the opening paragraph, which was less than clear. Apologies for my sloppy late-night editing before posting.

When I started blogging ten-plus years ago, most of my posts were about monetary policy, because I then felt that the Fed was not doing as much as it could, and should, have been doing to promote a recovery from the Little Depression (aka Great Recession) for which Fed’s policy mistakes bore heavy responsibility. The 2008 financial crisis and the ensuing deep downturn were largely the product of an overly tight monetary policy starting in 2006, and, despite interest-rate cuts in 2007 and 2008, the Fed’s policy consistently erred on the side of tightness because of concerns about rising oil and commodities prices, for almost two months after the start of the crisis. The stance of monetary policy cannot be assessed just by looking at the level of the central bank policy rate; the stance depends on the relationship between the policy rate and the economic conditions at any particular moment. The 2-percent Fed Funds target in the summer of 2008, given economic conditions at the time, meant that monetary policy was tight, not easy.

Although, after the crisis, the Fed never did as much as it could — and should — have to promote recovery, it at least took small measures to avoid a lapse into a ruinous deflation, even as many of the sound-money types, egged on by deranged right-wing scare mongers, warned of runaway inflation.

Slowly but surely, a pathetically slow recovery by the end of Obama’s second term, brought us back to near full employment. By then, my interest in the conduct of monetary policy had given way to a variety of other concerns as we dove into the anni horribiles of the maladministration of Obama’s successor.

Riding a recovery that started seven and a half years before he took office, and buoyed by a right-wing propaganda juggernaut and a pathetically obscene personality cult that broadcast and amplified his brazenly megalomaniacal self-congratulations for the inherited recovery over which he presided, Obama’s successor watched incompetently as the Covid 19 virus spread through the United States, causing the sharpest drop in output and employment in US history.

Ten months after Obama’s successor departed from the White House, the US economy has recovered much, but not all, of the ground lost during the pandemic, employment still below its peak at the start of 2020, and real output still lagging the roughly 2% real growth path along which the economy had been moving for most of the preceding decade.

However, the very rapid increase in output in Q2 2021 and the less rapid, but still substantial, increase in output in Q3 2021, combined with inflation that has risen to the highest rates in 30 years, has provoked ominous warning of resurgent inflation similar to the inflation from the late 1960s till the early 1980s, ending only with the deep 1981-82 recession caused by the resolute anti-inflation policy administered by Fed Chairman Paul Volcker with the backing of the newly elected Ronald Reagan.

It’s worth briefly revisiting that history (which I have discussed previously on this blog here, here, and especially in the following series (1), (2) and (3) from 2020) to understand the nature of the theoretical misunderstanding and the resulting policy errors in the 1970s and 1980s. While I agree that the recent increase in inflation is worrisome, it’s far from clear that inflation is likely, as many now predict, to get worse, although the inflation risk can’t be dismissed.

What I find equally if not more worrisome is that the anti-inflation commentary that we are hearing now from very serious people like Larry Summers in today’s Washington Post is how much it sounds like the inflation talk of 2008, which frightened the Fed, then presided over by a truly eminent economist, Ben Bernanke, into thinking that the chief risk facing the economy was rising headline inflation that would cause inflation expectations to become “unanchored.”

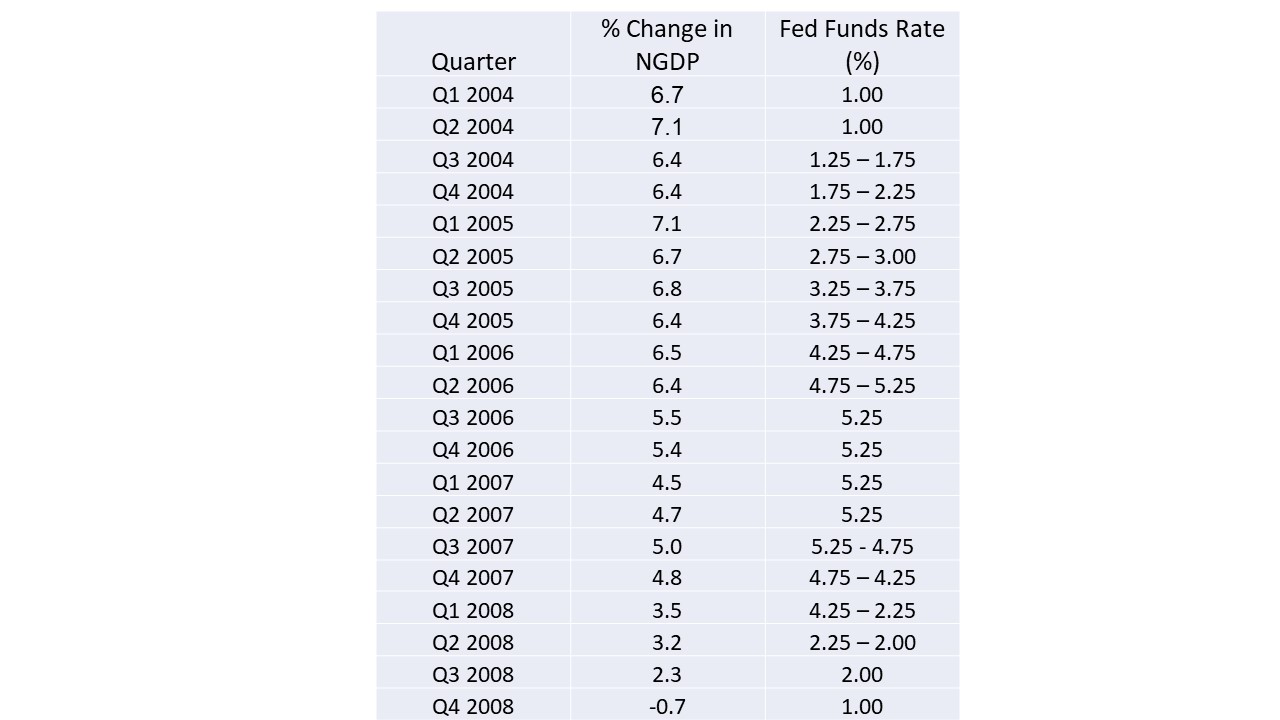

So, rather than provide an economy rapidly sliding into recession, the FOMC, focused on rapid increases in oil and commodity prices, refused to loosen monetary policy in the summer of 2008, even though the pace of growth in nominal gross domestic product (NGDP) had steadily decelerated measured year on year. The accompanying table shows the steady decline in the quarterly year-on-year growth of NGDP in each successive quarter between Q1 2004 and Q4 2008. Between 2004 and 2006, the decline was gradual, but accelerated in 2007 leading to the start of a recession in December 2007.

The decline in the rate of NGDP growth was associated with a gradual increase in the Fed funds target rate from a very low level 1% until Q2 2004, but by Q2 2006, when the rate reached 5%, the slowdown in the growth of total spending quickened. As the rate of spending declined, the Fed eased interest rates in the second half of 2007, but that easing was insufficient to prevent an economy, already suffering financial distress after the the housing bubble burst in 2006, from lapsing into recession.

Although the Fed cut its interest-rate target substantially in March 2008, during the summer of 2008, when the recession was rapidly deteriorating, the FOMC, fearing that inflation expectations would become “unanchored”, given rising headline inflation associated with very large increases in crude-oil prices (which climbed to a record $130 a barrel) and in commodity prices even as the recession was visibly worsening, refused to reduce rates further.

The Fed, to be sure, was confronted with a difficult policy dilemma, but it was a disastrous error to prioritize a speculative concern about the “unanchoring” of long-term inflation expectations over the reality of a fragile and clearly weakening financial system in a contracting economy already clearly in a recession. The Fed made the wrong choice, and the crisis came.

That was then, and now is now. The choices are different, but once again, on one side there is pressure to prioritize the speculative concern about the “unanchoring” of long-term inflation expectations over promoting recovery and increased employment after a a recession and a punishing pandemic. And, once again, the concerns about inflation are driven by a likely transitory increase in the price of crude oil and gasoline prices.

The case for prioritizing fighting inflation was just made by none other than Larry Summers in an op-ed in the Washington Post. Let’s have a look at Summer’s case for fighting inflation now.

Fed Chair Jerome H. Powell’s Jackson Hole speech in late August provided a clear, comprehensive and authoritative statement, enumerated in five pillars, of the widespread team “transitory” view of inflation that prevailed at that time and shaped policy thinking at the central bank and in the administration. Today, all five pillars are wobbly at best.

First, there was a claim that price increases were confined to a few sectors. No longer. In October, prices for commodity goods outside of food and energy rose at more than a 12 percent annual rate. Various Federal Reserve system indexes that exclude sectors with extreme price movements are now at record highs.

https://www.washingtonpost.com/opinions/2021/11/15/inflation-its-past-time-team-transitory-stand-down/

Summers has a point. Price increases are spreading throughout the economy. However, that doesn’t mean that increasing oil prices are not causing the prices of many other products to increase as well, inasmuch as oil and other substitute forms of energy are so widely used throughout the economy. If the increase in oil prices, and likely, in food prices, has peaked, or will do so soon, it does not necessarily make sense to fight a war against an enemy that has retreated or is about to do so.

Second, Powell suggested that high inflation in key sectors, such as used cars and durable goods more broadly, was coming under control and would start falling again. In October, used-car prices accelerated to more than a 30 percent annual inflation rate, new cars to a 17 percent rate and household furnishings by an annualized rate of just above 10 percent.

Id.

Again, citing large increases in the price of cars when it’s clear that there are special circumstances causing new car prices to rise rapidly, bringing used-car prices tagging along, is not very persuasive, especially when those special circumstances appear likely to be short-lived. To be sure other durables prices are also rising, but in the absence of a deeper source of inflation, the atmospherics cited by Summers are not that compelling.

Third, the speech pointed out that there was “little evidence of wage increases that might threaten excessive inflation.” This claim is untenable today with vacancy and quit rates at record highs, workers who switch jobs in sectors ranging from fast food to investment banking getting double-digit pay increases, and ominous Employment Cost Index increases.

Id.

Wage increases are usually an indicator of inflation, though, again the withdrawal, permanent or temporary, of many workers from employment in the past two years is a likely cause of increased wages that is independent of an underlying and ongoing inflationary trend.

Fourth, the speech argued that inflation expectations remained anchored. When Powell spoke, market inflation expectations for the term of the next Federal Reserve chair were around 2.5 percent. Now they are about 3.1 percent, up half a percentage point in the past month alone. And consumer sentiment is at a 10-year low due to inflation fears.

Id.

Clearly inflation expectations have increased over the short term for a variety of reasons that we have just been considering. But the curve of inflation expectations still seems to be reverting toward a lower level in the medium term and the long-term.

Fifth, Powell emphasized global deflationary trends. In the same week the United States learned of the fastest annual inflation rate in 30 years, Japan, China and Germany all reported their highest inflation in more than a decade. And the price of oil, the most important global determinant of inflation, is very high and not expected by forward markets to decline rapidly.

Id.

Again, Summers is simply recycling the same argument. We know that there has been a short-term increase in inflation. The question we need to grapple with is whether this short-term inflationary blip is likely to be self-limiting, or will feed on itself, causing inflation expectations to become “unanchored”. Forward prices of oil may not be showing that the price of oil will decline rapidly, but they aren’t showing expectations of further increases. Without further increases in oil prices, it is fair to ask what the source of further, ongoing inflation, that will cause “unanchoring”?

As it has in the past, the threat of “unanchoring”, is doing an awful lot of work. And it is not clear how the work is being done except by way of begging the question that really needs to be answered not begged.

After his windup, Summers offers fairly mild suggestions for his anti-inflation program, and only one of his comments seems mistaken.

Because of inflation, real interest rates are lower, as money is easier than a year ago. The Fed should signal that this is unacceptable and will be reversed.

Id.

The real interest rate about which the Fed should be concerned is the ex ante real interest rate reflecting both the expected yield from real capital and the expected rate of inflation (which may and often does have feedback effects on the expected yield from real capital). Past inflation does not automatically get transformed into an increase in expected inflation, and it is not necessarily the case that past inflation has left the expected yield from real capital unaffected, so Summers’ inference that the recent blip in inflation necessarily implies that monetary policy has been eased could well be mistaken. Yet again, these are judgments (or even guesses) that policymakers have to make about the subjective judgments of market participants. Those are policy judgments that can’t be made simply by reading off a computer screen.

While I’m not overly concerned by Summers’s list of inflation danger signs, there’s no doubt that inflation risk has risen. Yet, at least for now, that risk seems to be manageable. The risk may require the Fed to take pre-emptive measures against inflation down the road, but I don’t think that we have reached that point yet.

The main reason why I think that inflation risk has been overblown is that inflation is a common occurrence in postwar economies, as occurred in the US after both World Wars, and after the Korean War and the Vietnam War. It is widely recognized that war itself is inflationary owing, among other reasons, to the usual practice of governments to finance wartime expenditures by printing money, but inflationary pressures tend to persist even after the wars end.

Why does inflation persist after wars come to an end? The main reason is that, during wartime, resources, labor and capital, are shifted from producing goods for civilian purposes to waging war and producing and transporting supplies to support the war effort. Because total spending, financed by printing money, increases during the war, money income goes up even though the production of goods and services for civilian purposes goes down.

The output of goods and services for civilian purposes having been reduced, the increased money income accruing to the civilian population implies rising prices of the civilian goods and services that are produced. The tendency for prices to rise during wartime is mitigated by the reduced availability of outlets for private spending, people normally postponing much of their non-essential spending while the war is ongoing. Consequently, the public accumulates cash and liquid assets during wartime with the intention of spending the accumulated cash and liquid assets when life returns to normal after the war.

The lack of outlets for private spending is reinforced when, as happened in World War I, World War II, the Korean War and the late stages of the Vietnam War, price controls prevent the prices of civilian goods still being produced from rising, so that consumers can’t buy goods – either at all or as much as they would like – that they would willingly have paid for. The result is suppressed inflation until wartime price controls are lifted, and deferred price increases are allowed to occur. As prices rise, the excess cash that had been accumulated while the goods people demanded were unavailable is absorbed by purchases made at the postponed increases in price.

In his last book, Incomes and Money, Ralph Hawtrey described with characteristic clarity the process by which postwar inflation absorbed redundant cash balances accumulated during the World War II when price controls were lifted.

America, like Britain, had imposed price controls during the war, and had accumulated a great amount of redundant money. So long as the price controls continued, the American manufacturers were precluded from checking demand by raising their prices. But the price controls were abandoned in the latter half of 1946, and there resulted a rise of prices reaching 30 per cent on manufactured goods in the latter part of 1947. That meant that American industry was able to defend itself against the excess demand. By the end of 1947 the rise of prices had nearly eliminated the redundant money; that it to say, the quantity of money (currency and bank deposits) was little more than in a normal proportion to the national income. There was no longer over-employment in American industry, and there was no reluctance to take export orders.

Hawtrey, Incomes and Money, p. 7

Responding to Paul Krugman’s similar claim that there was high inflation following World War II, Summers posted the following twitter thread.

@paulkrugman continues his efforts to minimize the inflation threat to the American economy and progressive politics by pointing to the fact that inflation surged and then there was a year of deflation after World War 2.

If this is the best argument for not being alarmed that someone as smart, rhetorically effective and committed as Paul can make, my anxiety about inflation is increased.

Pervasive price controls were removed after the war. Economists know that measured prices with controls are artificial, so subsequent inflation proves little.

Millions of soldiers were returning home and a massive demobilization was in effect. Nothing like the current pervasive labor shortage was present.

https://twitter.com/LHSummers/status/1459992638170583041

Summers is surely correct that the situation today is not perfectly analogous to the post-WWII situation, but post-WWII inflation, as Hawtrey explained, was only partially attributable to the lifting of price controls. He ignores the effect of excess cash balances, which ultimately had to be spent or somehow withdrawn from circulation through a deliberate policy of deflation, which neither Summers nor most economists would think advisable or even acceptable. While the inflationary effect of absorbing excess cash balances is therefore almost inevitable, the duration of the inflation is limited and need not cause inflation expectations to become “unanchored.”

With the advent of highly effective Covid vaccines, we are now gradually emerging from the worst horrors of the Covid pandemic, when a substantial fraction of the labor force was either laid off or chose to withdraw from employment. As formerly idle workers return to work, we are in a prolonged quasi-postwar situation.

Just as the demand for civilian products declines during wartime, the demand for a broad range of private goods declined during the pandemic as people stopped going to restaurants, going on vacations, attending public gathering, and limited their driving and travel. Thus, the fraction of earnings that was saved increased as outlets for private spending became unavailable, inappropriate or undesirable.

As the pandemic has receded, restoring outlets for private spending, pent-up suppressed private demands have re-emerged, financed by households drawing down accumulated cash balances or drawing on credit lines augmented by paying down indebtedness. For many goods, like cars, the release of pent-up private demand has outpaced the increase in supply, leading to substantial price increases that are unlikely to be sustained once short-term supply bottlenecks are eliminated. But such imbalances between rapid increases in demand and sluggish increases in supply does not seem like a reliable basis on which to make policy choices.

So what are we to do now? As always, Ralph Hawtrey offers the best advice. The control of inflation, he taught, ultimately depends on controlling the relationship between the rate of growth in total nominal spending (and income) and the rate of growth of total real output. If total nominal spending (and income) is increasing faster than the increase in total real output, the difference will be reflected in the prices at which goods and services are provided.

In the five years from 2015 to 2019, the average growth rate in nominal spending (and income) was about 3.9%. During that period the average rate of growth in real output was 2.2% annually and the average rate of inflation was 1.7%. It has been reasonably suggested that extrapolating the 3.9% annual growth in nominal spending in the previous five years provides a reasonable baseline against which to compare actual spending in 2020 and 2021.

Actual nominal spending in Q3 2021 was slightly below what nominal GDP would have been in Q3 if it had continued growing at the extrapolated 3.9% growth path in nominal GDP. But for nominal GDP in Q4 not exceed that extrapolated growth path in Q4, Q4 could increase by an annual rate of no more than 4.3%. Inasmuch as spending in Q3 2021 was growing at 7.8%, the growth rate of nominal spending would have to slow substantially in Q4 from its Q3 growth rate.

But it is not clear that a 3.9% growth rate in nominal spending is the appropriate baseline to use. From 2015 to 2019, the average growth rate in real output was only 2.2% annually and the average inflation rate was only 1.7%. The Fed has long announced that its inflation target was 2% and in the 2015 to 2019 period, it consistently failed to meet that target. If the target inflation was 2% rather than 1.7%, presumably the Fed believed that annual growth would not have been less with 2% inflation than with 1.7%, so there is no reason to believe that the Fed should not have been aiming for more than 3.9% growth in total spending. If so a baseline for extrapolating the growth path for nominal spending should certainly not be less than 4.2%, Even a 4.5% baseline seems reasonable, and a baseline as high as 5% does not seem unreasonable.

With a 5% baseline, total nominal spending in Q4 could increase by as much as 5.4% without raising total nominal spending above its target path. But I think the more important point is not whether total spending does or does not rise above its growth path. The important goal is for the growth in nominal spending to decline steadily toward a reasonable growth path of about 4.5 to 5% and for this goal to be communicated to the public in a convincing manner. The 13.4% increase in total spending in Q2, when it appeared that the pandemic might soon be over, was likely a one-off outlier reflecting the release of pent-up demand. The 7.8% increase in Q3 was excessive, but substantially less than the Q2 rate of increase. If the Q4 increase does not continue downward trend in the rate of increase in nominal spending, it will be time to re-evaluate policy to ensure that the growth of spending is brought down to a non-inflationary range.

David,

You do realize the nuttiness of all of this don’t you?

We “need” a war to generate inflation.

We “need” inflation to avoid deflation.

We “need” government bonds to be able to pay for a war.

It’s a circular argument.

Once you realize that you don’t “need” government bonds (government can sell equity) and that the equity sold by government can be used to offset the real (inflation adjusted) cost of private debt service, then the other “needs” (inflation and war) disappear.

Deflation in and of itself is not something that should be frowned upon or discouraged. Yes, it creates problems in credit markets and for central bankers, but those problems can be easily remedied without resorting to war and inflation.

LikeLike

Are these sentences in need of editing? If so delete this comment after editing.

While I agree that the recent increase in inflation is worrisome, I don’t think that it’s far from clear that inflation is likely, as many are now suggesting, to get worse, although the inflation risk can’t be dismissed.

However, that doesn’t mean that a major source of the price increases is the increase in oil prices, inasmuch as oil and other substitute forms of energy are so widely used throughout the economy.

LikeLike

Oh my, this is great blogging, and even greater economics. Hats off.

I do not know why Summers has assumed the role of Inflation Monger No. 1.

From the Bureau of Economic Analysis website–

PCE Core:

Change From Month One Year Ago

September 2021 3.6 percent

August 2021 3.6 percent

July 2021 3.6 percent

June 2021 3.6 percent

OK, we are running at 3.6% PCE core, and I think the worst is over. Low wage workers have been gaining. The Fed has managed to sidestep a C19 depression.

Not so bad.

Add on: For the bottom third of the workforce, about 50 million to 60 million people, these are the best labor markets in 60 years. Is this so easily overlooked?

If moderate inflation is the cost of tight labor markets, then bring unto me tight labor markets for 100 years.

LikeLike