I’ve written three recent blogposts explaining why the inflation that began accelerating in the second half of 2021 was likely to be transitory (High Inflation Anxiety, Sic Transit Inflatio del Mundi, and Wherein I Try to Calm Professor Blanchard’s Nerves). I didn’t deny that inflation was accelerating and likely required a policy adjustment, but I also didn’t accept that the inflation threat was (or is) as urgent as some, notably Larry Summers, were suggesting.

In my two posts in late 2021, I argued that Summers’s concerns were overblown, because the burst of inflation in the second half of 2021 was caused mainly by increased consumer spending as consumers began drawing down cash and liquid assets accumulated when spending outlets had been unavailable, and was exacerbated by supply bottlenecks that kept output from accommodating increased consumer demand. Beyond that, despite rising expectations at the short-end, I minimized concerns about the unanchoring of inflation expectations owing to the inflationary burst in the second half of 2021, in the absence of any signs of rising inflation expectations in longer-term (5 years or more) bond prices.

Aside from criticizing excessive concern with what I viewed as a transitory burst of inflation not entirely caused by expansive monetary policy, I cautioned against reacting to inflation caused by negative supply shocks. In contrast to Summers’s warnings about the lessons of the 1970s when high inflation became entrenched before finally being broken — at the cost of the worst recession since the Great Depression, by Volcker’s anti-inflation policy — I explained that much of 1970s inflation was caused by supply-side oil shocks, which triggered an unnecessarily severe monetary tightening in 1974-75 and a deep recession that only modestly reduced inflation. Most of the decline in inflation following the oil shock occurred during the 1976 expansion when inflation fell to 5%. But, rather than allow a strong recovery to proceed on its own, the incoming Carter Administration and a compliant Fed, attempting to accelerate the restoration of full employment, increased monetary expansion. (It’s noteworthy that much of the high unemployment at the time reflected the entry of baby-boomers and women into the labor force, one of the few occasions in which an increased natural rate of unemployment can be easily identified.)

The 1977-79 monetary expansion caused inflation to accelerate to the high single digits even before the oil-shocks of 1979-80 led to double-digit inflation, setting the stage for Volcker’s brutal disinflationary campaign in 1981-82. But the mistake of tightening of monetary policy to suppress inflation resulting from negative supply shocks (usually associated with rising oil prices) went unacknowledged, the only lesson being learned, albeit mistakenly, was that high inflation can be reduced only by a monetary tightening sufficient to cause a deep recession.

Because of that mistaken lesson, the Fed, focused solely on the danger of unanchored inflation expectations, resisted pleas in the summer of 2008 to ease monetary policy as the economy was contracting and unemployment rising rapidly until October, a month after the start of the financial crisis. That disastrous misjudgment made me doubt that the arguments of Larry Summers et al. that tight money is required to counter inflation and prevent the unanchoring of inflation expectations, recent inflation being largely attributable, like the inflation blip in 2008, to negative supply shocks, with little evidence that inflation expectations had, or were likely to, become unanchored.

My first two responses to inflation hawks occurred before release of the fourth quarter 2021 GDP report. In the first three quarters, nominal GDP grew by 10.9%, 13.4% and 8.4%. My hope was that the Q4 rate of increase in nominal GDP would show a further decline from the Q3 rate, or at least show no increase. The rising trend of inflation in the final months of 2021, with no evidence of a slowdown in economic activity, made it unlikely that nominal GDP growth in Q4 had not accelerated. In the event, the acceleration of nominal GDP growth to 14.5% in Q4 showed that a tightening of monetary policy had become necessary.

Although a tightening of policy was clearly required to reduce the rate of nominal GDP growth, there was still reason for optimism that the negative supply-side shocks that had amplified inflationary pressure would recede, thereby allowing nominal GDP growth to slow down with no contraction in output and employment. Unfortunately, the economic environment deteriorated drastically in the latter part of 2021 as Russia began the buildup to its invasion of Ukraine, and deteriorated even more once the invasion started.

The price of Brent crude, just over $50/barrel in January 2021, rose to over $80/barrel in November of 2021. Tensions between Russia and Ukraine rose steadily during 2021, so it is not easy to determine the extent to which those increasing tensions were causing oil prices to rise and to what extent they rose because of increasing economic activity and inflationary pressure on oil prices. Brent crude fell to $70 in December before rising to $100/barrel in February on the eve of the invasion, briefly reaching $130/barrel shortly thereafter, before falling back to $100/barrel. Aside from the effect on energy prices, generalized uncertainty and potential effects on wheat prices and the federal budget from a drawn-out conflict in Ukraine have caused inflation expectations to increase.

Under these circumstances, it makes little sense to tighten policy suddenly. The appropriate policy strategy is to lean toward restraint and announce that the aim of policy is to reduce the rate of GDP growth gradually until a sustainable 4-5% rate of nominal GDP growth consistent with an inflation rate of about 2-3% a year is reached. The overnight rate of interest being the primary instrument whereby the Fed can either increase or decrease the rate of nominal GDP growth, it is unnecessary, and probably unwise, for the Fed to announce in advance a path of interest-rate increases. Instead, the Fed should communicate its target range for nominal GDP growth and condition the size and frequency of future rate increases on the deviations of the economy from that targeted growth path of nominal GDP.

Previous monetary policy mistakes that caused either recessions or excessive inflation have for more than half a century resulted from using interest rates or some other policy instrument to control inflation or unemployment rather than to moderate deviations from a stable growth rate in nominal GDP. Attempts to reduce inflation by maintaining or increasing already high interest rates until inflation actually fell needlessly and perversely prolonged and deepened recessions. Monetary conditions ought be eased as soon as nominal GDP growth falls below the target range for nominal GDP growth. Inflation automatically tends to fall in the early stages of recovery from a recession, and nothing is gained, and much harm is done, by maintaining a tight-money policy after nominal GDP growth has fallen below the target range. That’s the great, and still unlearned, lesson of monetary policy.

The bread and butter of economics is demand and supply. The basic idea of a demand function (or a demand curve) is to describe a relationship between the price at which a given product, commodity or service can be bought and the quantity that will bought by some individual. The standard assumption is that the quantity demanded increases as the price falls, so that the demand curve is downward-sloping, but not much more can be said about the shape of a demand curve unless special assumptions are made about the individual’s preferences.

Demand curves aren’t natural phenomena with concrete existence; they are hypothetical or notional constructs pertaining to individual preferences. To pass from individual demands to a market demand for a product, commodity or service requires another conceptual process summing the quantities demanded by each individual at any given price. The conceptual process is never actually performed, so the downward-sloping market demand curve is just presumed, not observed as a fact of nature.

The summation process required to pass from individual demands to a market demand implies that the quantity demanded at any price is the quantity demanded when each individual pays exactly the same price that every other demander pays. At a price of $10/widget, the widget demand curve tells us how many widgets would be purchased if every purchaser in the market can buy as much as desired at $10/widget. If some customers can buy at $10/widget while others have to pay $20/widget or some can’t buy any widgets at any price, then the quantity of widgets actually bought will not equal the quantity on the hypothetical widget demand curve corresponding to $10/widget.

Similar reasoning underlies the supply function or supply curve for any product, commodity or service. The market supply curve is built up from the preferences and costs of individuals and firms and represents the amount of a product, commodity or service that would be willing to offer for sale at different prices. The market supply curve is the result of a conceptual summation process that adds up the amounts that would be hypothetically be offered for sale by every agent at different prices.

The point of this pedantry is to emphasize the that the demand and supply curves we use are drawn on the assumption that a single uniform market price prevails in every market and that all demanders and suppliers can trade without limit at those prices and their trading plans are fully executed. This is the equilibrium paradigm underlying the supply-demand analysis of econ 101.

Economists quite unself-consciously deploy supply-demand concepts to analyze labor markets in a variety of settings. Sometimes, if the labor market under analysis is limited to a particular trade or a particular skill or a particular geographic area, the supply-demand framework is reasonable and appropriate. But when applied to the aggregate labor market of the whole economy, the supply-demand framework is inappropriate, because the ceteris-paribus proviso (all prices other than the price of the product, commodity or service in question are held constant) attached to every supply-demand model is obviously violated.

Thoughtlessly applying a simple supply-demand model to analyze the labor market of an entire economy leads to the conclusion that widespread unemployment, when some workers are unemployed, but would have accepted employment offers at wages that comparably skilled workers are actually receiving, implies that wages are above the market-clearing wage level consistent with full employment.

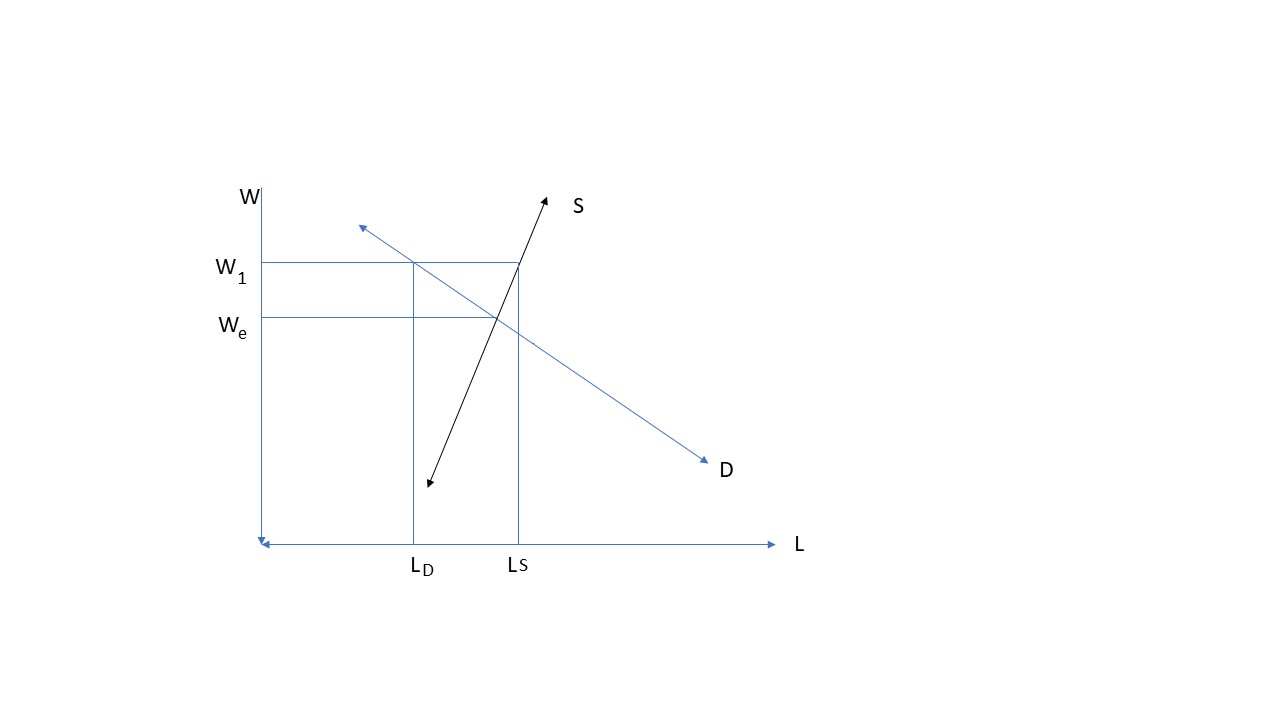

The attached diagram for simplest version of this analysis. The market wage (W1) is higher than the equilibrium wage (We) at which all workers willing to accept that wage could be employed. The difference between the number of workers seeking employment at the market wage (LS) and the number of workers that employers seek to hire (LD) measures the amount of unemployment. According to this analysis, unemployment would be eliminated if the market wage fell from W1 to We.

Applying supply-demand analysis to aggregate unemployment fails on two levels. First, workers clearly are unable to execute their plans to offer their labor services at the wage at which other workers are employed, so individual workers are off their supply curves. Second, it is impossible to assume, supply-demand analysis requires, that all other prices and incomes remain constant so that the demand and supply curves do not move as wages and employment change. When multiple variables are mutually interdependent and simultaneously determined, the analysis of just two variables (wages and employment) cannot be isolated from the rest of the system. Focusing on the wage as the variable that needs to change to restore full employment is an example of the tunnel vision.

Keynes rejected the idea that economy-wide unemployment could be eliminated by cutting wages. Although Keynes’s argument against wage cuts as a cure for unemployment was flawed, he did have at least an intuitive grasp of the basic weakness in the argument for wage cuts: that high aggregate unemployment is not usefully analyzed as a symptom of excessive wages. To explain why wage cuts aren’t the cure for high unemployment, Keynes introduced a distinction between voluntary and involuntary unemployment.

Forty years later, Robert Lucas began his effort — not the first such effort, but by far the most successful — to discredit the concept of involuntary unemployment. Here’s an early example:

Keynes [hypothesized] that measured unemployment can be decomposed into two distinct components: ‘voluntary’ (or frictional) and ‘involuntary’, with full employment then identified as the level prevailing when involuntary employment equals zero. It seems appropriate, then, to begin by reviewing Keynes’ reasons for introducing this distinction in the first place. . . .

Accepting the necessity of a distinction between explanations for normal and cyclical unemployment does not, however, compel one to identify the first as voluntary and the second as involuntary, as Keynes goes on to do. This terminology suggests that the key to the distinction lies in some difference in the way two different types of unemployment are perceived by workers. Now in the first place, the distinction we are after concerns sources of unemployment, not differentiated types. . . .[O]ne may classify motives for holding money without imagining that anyone can subdivide his own cash holdings into “transactions balances,” “precautionary balances”, and so forth. The recognition that one needs to distinguish among sources of unemployment does not in any way imply that one needs to distinguish among types.

Nor is there any evident reason why one would want to draw this distinction. Certainly the more one thinks about the decision problem facing individual workers and firms the less sense this distinction makes. The worker who loses a good job in prosperous time does not volunteer to be in this situation: he has suffered a capital loss. Similarly, the firm which loses an experienced employee in depressed times suffers an undesirable capital loss. Nevertheless, the unemployed worker at any time can always find some job at once, and a firm can always fill a vacancy instantaneously. That neither typically does so by choice is not difficult to understand given the quality of the jobs and the employees which are easiest to find. Thus there is an involuntary element in all unemployment, in the sense that no one chooses bad luck over good; there is also a voluntary element in all unemployment, in the sense that however miserable one’s current work options, one can always choose to accept them.

Lucas, Studies in Business Cycle Theory, pp. 241-43

Consider this revision of Lucas’s argument:

The expressway driver who is slowed down in a traffic jam does not volunteer to be in this situation; he has suffered a waste of his time. Nevertheless, the driver can get off the expressway at the next exit to find an alternate route. Thus, there is an involuntary element in every traffic jam, in the sense that no one chooses to waste time; there is also a voluntary element in all traffic jams, in the sense that however stuck one is in traffic, one can always take the next exit on the expressway.

What is lost on Lucas is that, for an individual worker, taking a wage cut to avoid being laid off by the employer accomplishes nothing, because the willingness of a single worker to accept a wage cut would not induce the employer to increase output and employment. Unless all workers agreed to take wage cuts, a wage cut to one employee would have not cause the employer to reconsider its plan to reduce in the face of declining demand for its product. Only the collective offer of all workers to accept a wage cut would induce an output response by the employer and a decision not to lay off part of its work force.

But even a collective offer by all workers to accept a wage cut would be unlikely to avoid an output reduction and layoffs. Consider a simple case in which the demand for the employer’s output declines by a third. Suppose the employer’s marginal cost of output is half the selling price (implying a demand elasticity of -2). Assume that demand is linear. With no change in its marginal cost, the firm would reduce output by a third, presumably laying off up to a third of its employees. Could workers avoid the layoffs by accepting lower wages to enable the firm to reduce its price? Or asked in another way, how much would marginal cost have to fall for the firm not to reduce output after the demand reduction?

Working out the algebra, one finds that for the firm to keep producing as much after a one-third reduction in demand, the firm’s marginal cost would have to fall by two-thirds, a decline that could only be achieved by a radical reduction in labor costs. This is surely an oversimplified view of the alternatives available to workers and employers, but the point is that workers facing a layoff after the demand for the product they produce have almost no ability to remain employed even by collectively accepting a wage cut.

That conclusion applies a fortiori when decisions whether to accept a wage cut are left to individual workers, because the willingness of workers individually to accept a wage cut is irrelevant to their chances of retaining their jobs. Being laid off because of decline in the demand for the product a worker is producing is a much different situation from being laid off, because a worker’s employer is shifting to a new technology for which the workers lack the requisite skills, and can remain employed only by accepting re-assignment to a lower-paying job.

Let’s follow Lucas a bit further:

Keynes, in chapter 2, deals with the situation facing an individual unemployed worker by evasion and wordplay only. Sentences like “more labor would, as a rule, be forthcoming at the existing money wage if it were demanded” are used again and again as though, from the point of view of a jobless worker, it is unambiguous what is meant by “the existing money wage.” Unless we define an individual’s wage rate as the price someone else is willing to pay him for his labor (in which case Keynes’s assertion is defined to be false to be false), what is it?

Lucas, Id.

I must admit that, reading this passage again perhaps 30 or more years after my first reading, I’m astonished that I could have once read it without astonishment. Lucas gives the game away by accusing Keynes of engaging in evasion and wordplay before embarking himself on sustained evasion and wordplay. The meaning of the “existing money wage” is hardly ambiguous, it is the money wage the unemployed worker was receiving before losing his job and the wage that his fellow workers, who remain employed, continue to receive.

Is Lucas suggesting that the reason that the worker lost his job while his fellow workers who did not lose theirs is that the value of his marginal product fell but the value of his co-workers’ marginal product did not? Perhaps, but that would only add to my astonishment. At the current wage, employers had to reduce the number of workers until their marginal product was high enough for the employer to continue employing them. That was not necessarily, and certainly not primarily, because some workers were more capable than those that were laid off.

The fact is, I think, that Keynes wanted to get labor markets out of the way in chapter 2 so that he could get on to the demand theory which really interested him.

More wordplay. Is it fact or opinion? Well, he says that thinks it’s a fact. In other words, it’s really an opinion.

This is surely understandable, but what is the excuse for letting his carelessly drawn distinction between voluntary and involuntary unemployment dominate aggregative thinking on labor markets for the forty years following?

Mr. Keynes, really, what is your excuse for being such an awful human being?

[I]nvoluntary unemployment is not a fact or a phenomenon which it is the task of theorists to explain. It is, on the contrary, a theoretical construct which Keynes introduced in the hope it would be helpful in discovering a correct explanation for a genuine phenomenon: large-scale fluctuations in measured, total unemployment. Is it the task of modern theoretical economics to ‘explain’ the theoretical constructs of our predecessor, whether or not they have proved fruitful? I hope not, for a surer route to sterility could scarcely be imagined.

Lucas, Id.

Let’s rewrite this paragraph with a few strategic word substitutions:

Heliocentrism is not a fact or phenomenon which it is the task of theorists to explain. It is, on the contrary, a theoretical construct which Copernicus introduced in the hope it would be helpful in discovering a correct explanation for a genuine phenomenon the observed movement of the planets in the heavens. Is it the task of modern theoretical physics to “explain” the theoretical constructs of our predecessors, whether or not they have proved fruitful? I hope not, for a surer route to sterility could scarcely be imagined.

Copernicus died in 1542 shortly before his work on heliocentrism was published. Galileo’s works on heliocentrism were not published until 1610 almost 70 years after Copernicus published his work. So, under Lucas’s forty-year time limit, Galileo had no business trying to explain Copernican heliocentrism which had still not yet proven fruitful. Moreover, even after Galileo had published his works, geocentric models were providing predictions of planetary motion as good as, if not better than, the heliocentric models, so decisive empirical evidence in favor of heliocentrism was still lacking. Not until Newton published his great work 70 years after Galileo, and 140 years after Copernicus, was heliocentrism finally accepted as fact.

In summary, it does not appear possible, even in principle, to classify individual unemployed people as either voluntarily or involuntarily unemployed depending on the characteristics of the decision problem they face. One cannot, even conceptually, arrive at a usable definition of full employment

Lucas, Id.

Belying his claim to be introducing scientific rigor into macroeocnomics, Lucas restorts to an extended scholastic inquiry into whether an unemployed worker can really ever be unemployed involuntarily. Based on his scholastic inquiry into the nature of volunatriness, Lucas declares that Keynes was mistaken because would not accept the discipline of optimization and equilibrium. But Lucas’s insistence on the discipline of optimization and equilibrium is misplaced unless he can provide an actual mechanism whereby the notional optimization of a single agent can be reconciled with notional optimization of other individuals.

It was his inability to provide any explanation of the mechanism whereby the notional optimization of individual agents can be reconciled with the notional optimizations of other individual agents that led Lucas to resort to rational expectations to circumvent the need for such a mechanism. He successfully persuaded the economics profession that evading the need to explain such a reconciliation mechanism, the profession would not be shirking their explanatory duty, but would merely be fulfilling their methodological obligation to uphold the neoclassical axioms of rationality and optimization neatly subsumed under the heading of microfoundations.

Rational expectations and microfoundations provided the pretext that could justify or at least excuse the absence of any explanation of how an equilibrium is reached and maintained by assuming that the rational expectations assumption is an adequate substitute for the Walrasian auctioneer, so that each and every agent, using the common knowledge (and only the common knowledge) available to all agents, would reliably anticipate the equilibrium price vector prevailing throughout their infinite lives, thereby guaranteeing continuous equilibrium and consistency of all optimal plans. That feat having been securely accomplished, it was but a small and convenient step to collapse the multitude of individual agents into a single representative agent, so that the virtue of submitting to the discipline of optimization could find its just and fitting reward.

UPDATE (4/3/2022): Reupping this post with the response to my query sent by Brad DeLong.

I’m writing this post in hopes of eliciting some guidance from readers about the three propagation mechanisms to which Robert Lucas and Thomas Sargent refer in their famous 1978 article, “After Keynesian Macroeconomics.” The three propagation mechanisms were mentioned to parry criticisms of the rational-expectations principle underlying the New Classical macroeconomics that Lucas and Sargent were then developing as an alternative to Keynesian macroeconomics. I am wondering how subsequent research has dealt with these propagation mechanisms and how they are now treated in current macro-theory. Here is the relevant passage from Lucas and Sargent:

A second line of criticism stems from the correct observation that if agents’ expectations are rational and if their information sets include lagged values of the variable being forecast, then agents’ forecast errors must be a serially uncorrelated random process. That is, on average there must be no detectable relationships between a period’s forecast error and any previous period’s. This feature has led several critics to conclude that equilibrium models cannot account for more than an insignificant part of the highly serially correlated movements we observe in real output, employment, unemployment, and other series. Tobin (1977, p. 461) has put the argument succinctly:

One currently popular explanation of variations in employment is temporary confusion of relative and absolute prices. Employers and workers are fooled into too many jobs by unexpected inflation, but only until they learn it affects other prices, not just the prices of what they sell. The reverse happens temporarily when inflation falls short of expectation. This model can scarcely explain more than transient disequilibrium in labor markets.

So how can the faithful explain the slow cycles of unemployment we actually observe? Only by arguing that the natural rate itself fluctuates, that variations in unemployment rates are substantially changes in voluntary, frictional, or structural unemployment rather than in involuntary joblessness due to generally deficient demand.

The critics typically conclude that the theory only attributes a very minor role to aggregate demand fluctuations and necessarily depends on disturbances to aggregate supply to account for most of the fluctuations in real output over the business cycle. “In other words,” as Modigliani (1977) has said, “what happened to the United States in the 1930’s was a severe attack of contagious laziness.” This criticism is fallacious because it fails to distinguish properly between sources of impulses and propagation mechanisms, a distinction stressed by Ragnar Frisch in a classic 1933 paper that provided many of the technical foundations for Keynesian macroeconometric models. Even though the new classical theory implies that the forecast errors which are the aggregate demand impulses are serially uncorrelated, it is certainly logically possible that propagation mechanisms are at work that convert these impulses into serially correlated movements in real variables like output and employment. Indeed, detailed theoretical work has already shown that two concrete propagation mechanisms do precisely that.

One mechanism stems from the presence of costs to firms of adjusting their stocks of capital and labor rapidly. The presence of these costs is known to make it optimal for firms to spread out over time their response to the relative price signals they receive. That is, such a mechanism causes a firm to convert the serially uncorrelated forecast errors in predicting relative prices into serially correlated movements in factor demands and output.

A second propagation mechanism is already present in the most classical of economic growth models. Households’ optimal accumulation plans for claims on physical capital and other assets convert serially uncorrelated impulses into serially correlated demands for the accumulation of real assets. This happens because agents typically want to divide any unexpected changes in income partly between consuming and accumulating assets. Thus, the demand for assets next period depends on initial stocks and on unexpected changes in the prices or income facing agents. This dependence makes serially uncorrelated surprises lead to serially correlated movements in demands for physical assets. Lucas (1975) showed how this propagation mechanism readily accepts errors in forecasting aggregate demand as an impulse source.

A third likely propagation mechanism has been identified by recent work in search theory. (See, for example, McCall 1965, Mortensen 1970, and Lucas and Prescott 1974.) Search theory tries to explain why workers who for some reason are without jobs find it rational not necessarily to take the first job offer that comes along but instead to remain unemployed for awhile until a better offer materializes. Similarly, the theory explains why a firm may find it optimal to wait until a more suitable job applicant appears so that vacancies persist for some time. Mainly for technical reasons, consistent theoretical models that permit this propagation mechanism to accept errors in forecasting aggregate demand as an impulse have not yet been worked out, but the mechanism seems likely eventually to play an important role in a successful model of the time series behavior of the unemployment rate. In models where agents have imperfect information, either of the first two mechanisms and probably the third can make serially correlated movements in real variables stem from the introduction of a serially uncorrelated sequence of forecasting errors. Thus theoretical and econometric models have been constructed in which in principle the serially uncorrelated process of forecasting errors can account for any proportion between zero and one of the steady state variance of real output or employment. The argument that such models must necessarily attribute most of the variance in real output and employment to variations in aggregate supply is simply wrong logically.

My problem with the Lucas-Sargent argument is that even if the deviations from a long-run equilibrium path are serially correlated, shouldn’t those deviations be diminishing over time after the initial disturbance. Can these propagation mechanisms account for amplification of the initial disturbance before the adjustment toward the equilibrium path begins? I would gratefully welcome any responses.

David Glasner has a question about the “rational expectations” business-cycle theories developed in the 1970s:

David Glasner: Three Propagation Mechanisms in Lucas & Sargent: ‘I’m… hop[ing for]… some guidance… about… propagation mechanisms… [in] Robert Lucas and Thomas Sargent[‘s]… “After Keynesian Macroeconomics.”…

The critics typically conclude that the theory only attributes a very minor role to aggregate demand fluctuations and necessarily depends on disturbances to aggregate supply…. [But] even though the new classical theory implies that the forecast errors which are the aggregate demand impulses are serially uncorrelated, it is certainly logically possible that propagation mechanisms are at work that convert these impulses into serially correlated movements in real variables like output and employment… the presence of costs to firms of adjusting their stocks of capital and labor rapidly…. accumulation plans for claims on physical capital and other assets convert serially uncorrelated impulses into serially correlated demands for the accumulation of real assets… workers who for some reason are without jobs find it rational not necessarily to take the first job offer that comes along but instead to remain unemployed for awhile until a better offer materializes…. In principle the serially uncorrelated process of forecasting errors can account for any proportion between zero and one of the [serially correlated] steady state variance of real output or employment. The argument that such models must necessarily attribute most of the variance in real output and employment to variations in aggregate supply is simply wrong logically…

My problem with the Lucas-Sargent argument is that even if the deviations from a long-run equilibrium path are serially correlated, shouldn’t those deviations be diminishing over time after the initial disturbance? Can these propagation mechanisms account for amplification of the initial disturbance before the adjustment toward the equilibrium path begins? I would gratefully welcome any responses…

In some ways this is of only history-of-thought interest. For Lucas and Prescott, at least, had within five years of the writing of “After Keynesian Macroeconomics” decided that the critics were right: that their models of how mistaken decisions driven by serially-uncorrelated forecast errors could not account for the bulk of the serially correlated business-cycle variance of real output and employment, and they needed to shift to studying real business cycle theory instead of price-misperceptions theory. The first problem was that time-series methods generated shocks that came at the wrong times to explain recessions. The second problem was that the propagation mechanisms did not amplify but rather damped the shock: at best they produced some kind of partial-adjustment process that extended the impact of a shock on real variables to N periods and diminished its impact in any single period to 1/N. There was no… what is the word?…. multiplier in the system.

It was stunning to watch in real time in the early 1980s. As Paul Volcker hit the economy on the head with the monetary-stringency brick, repeatedly, quarter after quarter; as his serially correlated and hence easily anticipated policy moves had large and highly serially correlated effects on output; Robert Lucas and company simply… pretended it was not happening: that monetary policy was not having major effects on output and employment in the first half of the 1980s, and that it was not the case thjat the monetary policies that were having such profound real impacts had no plausible interpretation as “surprises” leading to “misperceptions”. Meanwhile, over in the other corner, Robert Barro was claiming that he saw no break in the standard pattern of federal deficits from the Reagan administration’s combination of tax cuts plus defense buildup.

Those of us who were graduate students at the time watched this, and drew conclusions about the likelihood that Lucas, Prescott, and company had good enough judgment and close enough contact with reality that their proposed “real business cycle” research program would be a productive one—conclusions that, I think, time has proved fully correct.

Behind all this, of course, was this issue: the “microfoundations” of the Lucas “island economy” model were totally stupid: people are supposed to “misperceive” relative prices because they know the nominal prices at which they sell but do not know the nominal prices at which they buy, hence people confuse a monetary shock-generated rise in the nominal price level with an increase in the real price of what they produce, and hence work harder and longer and produce more? (I forget who it was who said at the time that the model seemed to require a family in which the husband worked and the wife went to the grocery store and the husband never listened to anything the wife said.) These so-called “microfoundations” could only be rationally understood as some kind of metaphor. But what kind of metaphor? And why should it have any special status, and claim on our attention?

Paul Krugman’s judgment on the consequences of this intellectual turn is even harsher than mine:

What made the Dark Ages dark was the fact that so much knowledge had been lost, that so much known to the Greeks and Romans had been forgotten by the barbarian kingdoms that followed. And that’s what seems to have happened to macroeconomics in much of the economics profession. The knowledge that S=I doesn’t imply the Treasury view—the general understanding that macroeconomics is more than supply and demand plus the quantity equation — somehow got lost in much of the profession. I’m tempted to go on and say something about being overrun by barbarians in the grip of an obscurantist faith…

I would merely say that it has left us, over what is now two generations, with a turn to DSGE models—Dynamic Stochastic General Equilibrium—that must satisfy a set of formal rhetorical requirements that really do not help us fit the data, and that it gave many, many people an excuse not to read and hence a license to remain ignorant of James Tobin.

I am an economist in the Washington DC area. My research and writing has been mostly on monetary economics and policy and the history of economics. In my book Free Banking and Monetary Reform, I argued for a non-Monetarist non-Keynesian approach to monetary policy, based on a theory of a competitive supply of money. Over the years, I have become increasingly impressed by the similarities between my approach and that of R. G. Hawtrey and hope to bring Hawtrey’s unduly neglected contributions to the attention of a wider audience.