A little over three months ago on a brutally hot day in Washington DC, I gave a talk about a not yet completed paper at the Mercatus Center Conference on Monetary Rules for a Post-Crisis World. The title of my paper was (and still is) “Rules versus Discretion Historically Contemplated.” I hope to post a draft of the paper soon on SSRN.

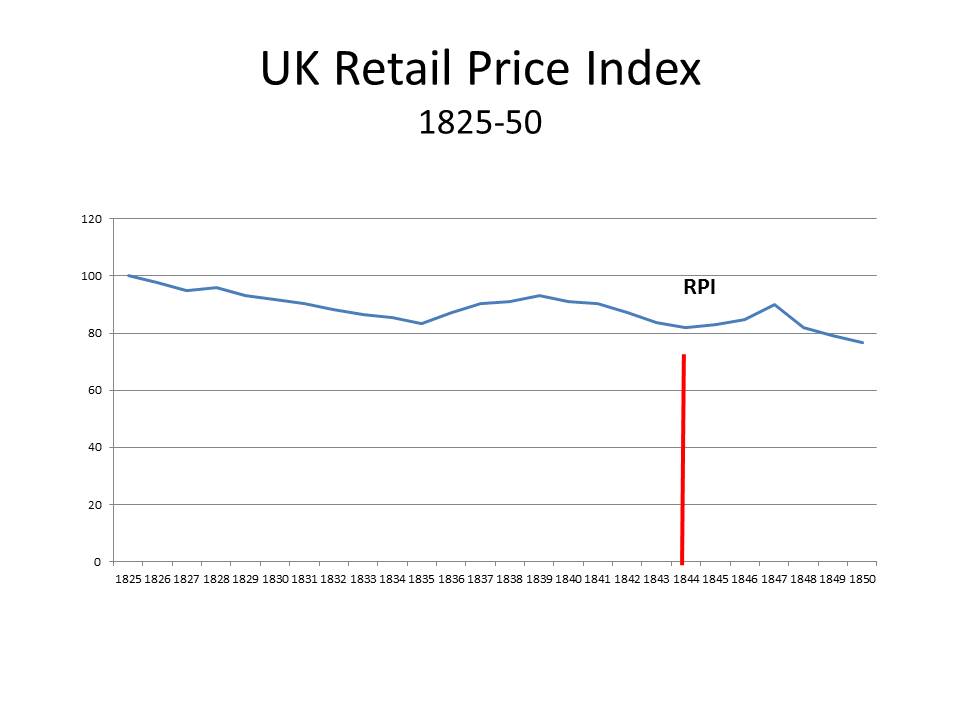

One of the attendees at the conference was Larry White who started his graduate training at UCLA just after I had left. When I wrote a post about my talk, Larry responded with a post of his own in which he took issue with some of what I had to say about the gold standard, which I described as the first formal attempt at a legislated monetary rule. Actually, in my talk and my paper, my intention was not as much to criticize the gold standard as it was to criticize the idea, which originated after the gold standard had already been adopted in England, of imposing a fixed numerical rule in addition to the gold standard to control the quantity of banknotes or the total stock of money. The fixed mechanical rule was imposed by an act of Parliament, the Bank Charter Act of 1844. The rule, intended to avoid financial crises such as those experienced in 1825 and 1836, actually led to further crises in 1847, 1857 and 1866 and the latter crises were quelled only after the British government suspended those provisions of the Act preventing the Bank of England from increasing the quantity of banknotes in circulation. So my first point was that the fixed quantitative rule made the gold standard less stable than it would otherwise have been.

My second point was that, in the depths of the Great Depression, a fixed rule freezing the nominal quantity of money was proposed as an alternative rule to the gold standard. It was this rule that one of its originators, Henry Simons, had in mind when he introduced his famous distinction between rules and discretion. Simons had many other reasons for opposing the gold standard, but he introduced the famous rules-discretion dichotomy as a way of convincing those supporters of the gold standard who considered it a necessary bulwark against comprehensive government control over the economy to recognize that his fixed quantity rule would be a far more effective barrier than the gold standard against arbitrary government meddling and intervention in the private sector, because the gold standard, far from constraining the conduct of central banks, granted them broad discretionary authority. The gold standard was an ineffective rule, because it specified only the target pursued by the monetary authority, but not the means of achieving the target. In Simons view, giving the monetary authority to exercise discretion over the instruments used to achieve its target granted the monetary authority far too much discretion for independent unconstrained decision making.

My third point was that Henry Simons himself recognized that the strict quantity rule that he would have liked to introduce could only be made operational effectively if the entire financial system were radically restructured, an outcome that he reluctantly concluded was unattainable. However, his student Milton Friedman convinced himself that a variant of the Simons rule could actually be implemented quite easily, and he therefore argued over the course of almost his entire career that opponents of discretion ought to favor the quantity rule that he favored instead of continuing to support a restoration of the gold standard. However, Friedman was badly mistaken in assuming that his modified quantity rule eliminated discretion in the manner that Simons had wanted, because his quantity rule was defined in terms of a magnitude, the total money stock in the hands of the public, which was a target, not, as he insisted, an instrument, the quantity of money held by the public being dependent on choices made by the public, not just on choices made by the monetary authority.

So my criticism of quantity rules can be read as at least a partial defense of the gold standard against the attacks of those who criticized the gold standard for being insufficiently rigorous in controlling the conduct of central banks.

Let me now respond to some of Larry’s specific comments and criticisms of my post.

[Glasner] suggests that perhaps the earliest monetary rule, in the general sense of a binding pre-commitment for a money issuer, can be seen in the redemption obligations attached to banknotes. The obligation was contractual: A typical banknote pledged that the bank “will pay the bearer on demand” in specie. . . . He rightly remarks that “convertibility was not originally undertaken as a policy rule; it was undertaken simply as a business expedient” without which the public would not have accepted demand deposits or banknotes.

I wouldn’t characterize the contract in quite the way Glasner does, however, as a “monetary rule to govern the operation of a monetary system.” In a system with many banks of issue, the redemption contract on any one bank’s notes was a commitment from that bank to the holders of those notes only, without anyone intending it as a device to govern the operation of the entire system. The commitment that governs a single bank ipso facto governs an entire monetary system only when that single bank is a central bank, the only bank allowed to issue currency and the repository of the gold reserves of ordinary commercial banks.

It’s hard to write a short description of a system that covers all possible permutations in the system. While I think Larry is correct in noting the difference between the commitment made by any single bank to convert – on demand — its obligations into gold and the legal commitment imposed on an entire system to maintain convertibility into gold, the historical process was rather complicated, because both silver and gold coins circulating in Britain. So the historical fact that British banks were making their obligations convertible into gold was the result of prior decisions that had been made about the legal exchange rate between gold and silver coins, decisions which overvalued gold and undervalued silver, causing full bodied silver coins to disappear from circulation. Given a monetary framework shaped by the legal gold/silver parity established by the British mint, it was inevitable that British banks operating within that framework would make their banknotes convertible into gold not silver.

Under a gold standard with competitive plural note-issuers (a free banking system) holding their own reserves, by contrast, the operation of the monetary system is governed by impersonal market forces rather than by any single agent. This is an important distinction between the properties of a gold standard with free banking and the properties of a gold standard managed by a central bank. The distinction is especially important when it comes to judging whether historical monetary crises and depressions can be accurately described as instances where “the gold standard failed” or instead where “central bank management of the monetary system failed.”

I agree that introducing a central bank into the picture creates the possibility that the actions of the central bank will have a destabilizing effect. But that does not necessarily mean that the actions of the central bank could not also have a stabilizing effect compared to how a pure free-banking system would operate under a gold standard.

As the author of Free Banking and Monetary Reform, Glasner of course knows the distinction well. So I am not here telling him anything he doesn’t know. I am only alerting readers to keep the distinction in mind when they hear or read “the gold standard” being blamed for financial instability. I wish that Glasner had made it more explicit that he is talking about a system run by the Bank of England, not the more automatic type of gold standard with free banking.

But in my book, I did acknowledge that there inherent instabilities associated with a gold standard. That’s why I proposed a system that would aim at stabilizing the average wage level. Almost thirty years on, I have to admit to having my doubts whether that would be the right target to aim for. And those doubts make me more skeptical than I once was about adopting any rigid monetary rule. When it comes to monetary rules, I fear that the best is the enemy of the good.

Glasner highlights the British Parliament’s legislative decision “to restore the convertibility of banknotes issued by the Bank of England into a fixed weight of gold” after a decades-long suspension that began during the Napoleonic wars. He comments:

However, the widely held expectations that the restoration of convertibility of banknotes issued by the Bank of England into gold would produce a stable monetary regime and a stable economy were quickly disappointed, financial crises and depressions occurring in 1825 and again in 1836.

Left unexplained is why the expectations were disappointed, why the monetary regime remained unstable. A reader who hasn’t read Glasner’s other blog entries on the gold standard might think that he is blaming the gold standard as such.

Actually I didn’t mean to blame anyone for the crises of 1825 and 1836. All I meant to do was a) blame the Currency School for agitating for a strict quantitative rule governing the total quantity of banknotes in circulation to be imposed on top of the gold standard, b) point out that the rule that was enacted when Parliament passed the Bank Charter Act of 1844 failed to prevent subsequent crises in 1847, 1857 and 1866, and c) that the crises ended only after the provisions of the Bank Charter Act limiting the issue of banknotes by the Bank of England had been suspended.

My own view is that, because the monopoly Bank of England’s monopoly was not broken up, even with convertibility acting as a long-run constraint, the Bank had the power to create cyclical monetary instability and occasionally did so by (unintentionally) over-issuing and then having to contract suddenly as gold flowed out of its vault — as happened in 1825 and again in 1836. Because the London note-issue was not decentralized, the Bank of England did not experience prompt loss of reserves to rival banks (adverse clearings) as soon as it over-issued. Regulation via the price-specie-flow mechanism (external drain) allowed over-issue to persist longer and grow larger. Correction came only with a delay, and came more harshly than continuous intra-London correction through adverse clearings would have. Bank of England mistakes boggled the entire financial system. It was central bank errors and not the gold standard that disrupted monetary stability after 1821.

Here, I think, we do arrive at a basic theoretical disagreement, because I don’t accept that the price-specie-flow mechanism played any significant role in the international adjustment process. National price levels under the gold standard were positively correlated to a high degree, not negatively correlated, as implied by the price-specie-flow mechanism. Moreover, the Bank Charter Act imposed a fixed quantitative limit on the note issue of all British banks and the Bank of England in particular, so the overissue of banknotes by the Bank of England could not have been the cause of the post-1844 financial crises. If there was excessive credit expansion, it was happening through deposit creation by a great number of competing deposit-creating banks, not the overissue of banknotes by the Bank of England.

This hypothesis about the source of England’s cyclical instability is far from original with me. It was offered during the 1821-1850 period by a number of writers. Some, like Robert Torrens, were members of the Currency School and offered the Currency Principle as a remedy. Others, like James William Gilbart, are better classified as members of the Free Banking School because they argued that competition and adverse clearings would effectively constrain the Bank of England once rival note issuers were allowed in London. Although they offered different remedies, these writers shared the judgment that the Bank of England had over-issued, stimulating an unsustainable boom, then was eventually forced by gold reserve losses to reverse course, instituting a credit crunch. Because Glasner elides the distinction between free banking and central banking in his talk and blog post, he naturally omits the third side in the Currency School-Banking School-Free Banking School debate.

And my view is that Free Bankers like Larry White overestimate the importance of note issue in a banking system in which deposits were rapidly overtaking banknotes as the primary means by which banks extended credit. As Henry Simons, himself, recognized this shift from banknotes to bank deposits was itself stimulated, at least in part, by the Bank Charter Act, which made the extension of credit via banknotes prohibitively costly relative to expansion by deposit creation.

Later in his blog post, Glasner fairly summarizes how a gold standard works when a central bank does not subvert or over-ride its automatic operation:

Given the convertibility commitment, the actual quantity of the monetary instrument that is issued is whatever quantity the public wishes to hold.

But he then immediately remarks:

That, at any rate, was the theory of the gold standard. There were — and are – at least two basic problems with that theory. First, making the value of money equal to the value of gold does not imply that the value of money will be stable unless the value of gold is stable, and there is no necessary reason why the value of gold should be stable. Second, the behavior of a banking system may be such that the banking system will itself destabilize the value of gold, e.g., in periods of distress when the public loses confidence in the solvency of banks and banks simultaneously increase their demands for gold. The resulting increase in the monetary demand for gold drives up the value of gold, triggering a vicious cycle in which the attempt by each to increase his own liquidity impairs the solvency of all.

These two purported “basic problems” prompt me to make two sets of comments:

1 While it is true that the purchasing power of gold was not perfectly stable under the classical gold standard, perfection is not the relevant benchmark. The purchasing power of money was more stable under the classical gold standard than it has been under fiat money standards since the Second World War. Average inflation rates were closer to zero, and the price level was more predictable at medium to long horizons. Whatever Glasner may have meant by “necessary reason,” there certainly is a theoretical reason for this performance: the economics of gold mining make the purchasing power of gold (ppg) mean-reverting in the face of monetary demand and supply shocks. An unusually high ppg encourages additional gold mining, until the ppg declines to the normal long-run value determined by the flow supply and demand for gold. An unusually low ppg discourages mining, until the normal long-run ppg is restored. It is true that permanent changes in the gold mining cost conditions can have a permanent impact on the long-run level of the ppg, but empirically such shocks were smaller than the money supply variations that central banks have produced.

2 The behavior of the banking system is indeed critically important for short-run stability. Instability wasn’t a problem in all countries, so we need to ask why some banking systems were unstable or panic-prone, while others were stable. The US banking system was panic prone in the late 19th century while the Canadian system was not. The English system was panic-prone while the Scottish system was not. The behavioral differences were not random or mere facts of nature, but grew directly from differences in the legal restrictions constraining the banks. The Canadian and Scottish systems, unlike the US and English systems, allowed their banks to adequately diversify, and to respond to peak currency demands, thus allowed banks to be more solvent and more liquid, and thus avoided loss of confidence in the banks. The problem in the US and England was not the gold standard, or a flaw in “the theory of the gold standard,” but ill-conceived legal restrictions that weakened the banking systems.

Larry makes two good points, but I doubt that they are very important in practice. The problem with the value of gold is that there is a very long time lag before the adjustment in the rate of output of new gold will cause the value of gold to revert back to its normal level. The annual output of gold is only about 3 percent of the total stock of gold. If the monetary demand for gold is large relative to the total stock and that demand is unstable, the swing in the overall demand for gold can easily dominate the small resulting change in the annual rate of output. So I do not have much confidence that the mean-reversion characteristic of the purchasing power of gold to be of much help in the short or even the medium term. I also agree with Larry that the Canadian and Scottish banking systems exhibited a lot more stability than the neighboring US and English banking systems. That is an important point, but I don’t think it is decisive. It’s true that there were no bank failures in Canada in the Great Depression. But the absence of bank failures, while certainly a great benefit, did not prevent Canada from suffering a downturn of about the same depth and duration as the US did between 1929 and 1933. The main cause of the Great Depression was the deflation caused by the appreciation of the value of gold. The deflation caused bank failures when banks were small and unstable and did not cause bank failures when banks were large and diversified. But the deflation was still wreaking havoc on the rest of the economy even though banks weren’t failing.