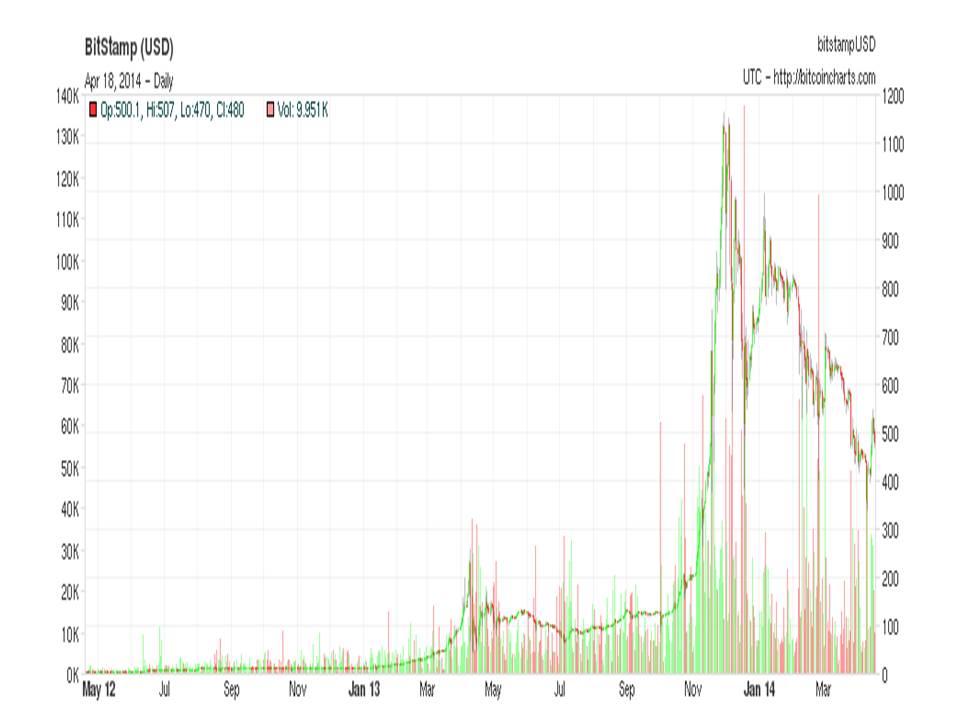

Look out, bitcoin’s back. After the first bitcoin bubble burst almost exactly three years ago on December 15, 2017, when bitcoin hit its previous all-time high of over $19,600, bitcoin lost more than 80% its value, falling to less than $3200 on December 14, 2018. It gradually recovered, more than doubling its value (to over $7000) by December 13, 2019 and reached a new all-time high today at $20,872.

Bitcoin’s remarkable recovery is again sparking senseless talk by its more extreme promoters that it will soon transform the world monetary system leading the collapse of fiat currencies and a flight to bitcoin to escape the hyperinflationary collapse of worthless unbacked fiat currencies. This is nonsense, as I have explained at length in a number of previous posts (e.g., here, here, and here) at even greater length in a forthcoming paper, a draft of which is available here.

In this post, I offer a summary of my argument about why bitcoin, despite its success as a speculative asset, is intrinsically unsuited to be a widely used medium of exchange, let alone a dominant currency. Indeed, success as a speculative asset is precisely what disqualifies it as anything more than a niche medium of exchange.

By a “medium of exchange,” I mean a good or instrument readily accepted in exchange by agents even if they don’t value the non-monetary services provided by that good or instrument in the expectation that other agents will be accepted in exchange at a reasonably predictable value close to its current value. After a good begins to function as a medium of exchange, its value may rise above the value it would have had if it were demanded only for the real services it provides, but arbitrage ensures that the value of a medium of exchange will be equalized in all uses, monetary or and real, so the expected value of a medium of exchange will not vary as a result of the intended use for which it is acquired.

By a “pure medium of exchange” I mean a good or instrument providing no non-monetary services and therefore demanded solely on account of its expected future resale value. The analysis of the value of a pure medium of exchange seems to hinge on three different factors affecting its expected future resale value: (1) backward induction, (2) tax liability, and (3) network effects.

Backward induction refers to the influence of a predictable future state on the present. If agents all foresee a future event that influence of that future event, however distant, must rebound backward towards the present. Thus, the certainty that a pure medium of exchange must lose its value once no one is willing to accept in exchange, its predictable loss of value must deprive it of value immediately, because no one will want to be the last person to accept it.

Backward induction is used routinely in formal exchange and game-theoretic models, but its relevance is often disputed when the certainty and the timing of the last period is unclear. In that environment, people seem more willing to assume that there will always be someone else around who will accept the medium of exchange at a positive value. Even so, backward induction at least suggests that the value of any pure medium of exchange is sensitive to expectational shocks, making a pure medium of exchange a potentially unstable pillar of an economic system.

Tax liability refers to the acceptability of a medium of exchange to discharge tax liabilities to the government. Acceptability to discharge a stream of future tax liabilities imposed by the government can maintain a positive value for a pure medium of exchange even if the backward induction argument is otherwise compelling. However, acceptability to discharge tax payments is routinely extended to government issued, or government sanctioned, fiat currencies but never to privately issued cryptocurrencies.

Network effects result from the property of some goods that their usefulness is contingent on and enhanced by the extent to which the good is used by other people. Think of the difference between a refrigerator and a telephone. Clearly, the desirability of and the demand for a medium of exchange increases with the number of other people using that medium of exchange. Additionally, as more people use any given medium of exchange, the cost to any individual user of switching to another medium of exchange than that used by the network of users of which that user is a part increases.

Network effects are important for many reasons, but for purposes of this discussion, network effects are particularly important because they provide another explanation than the tax-liability argument for why backward induction need not drive the value of a pure medium of exchange to zero. If a new medium of exchange provides some exchange service superior to, or not provided at all by, the service provided by the existing, more widely used, medium of exchange, and it attracts even a small network of users that take advantage of that service, a demand for the continued use of the alternative medium of exchange may be created. If the switching cost associated with adopting another medium of exchange and foregoing the unique service provided by the new medium of exchange is sufficiently high, current users of the new medium of exchange may persist in use of the new medium of exchange despite its predictable future loss of value.

Thus, even though it provides no current real services, and even though its current value is drawn entirely from its expected future value, bitcoin may have succeeded in providing a niche medium of exchange service for transactions in which one or both parties have a strong desire or need for anonymity. The underlying blockchain technology is thought to provide such assurance to those transacting with bitcoins. At least for now, this niche service seems to serve a small network of users better than any available alternative, and the current costs of switching to an alternative medium of exchange providing similar assurance of anonymity may be prohibitive. That network effect, combined with high switching cost, may be sufficient to prevent backward induction from driving the value of bitcoins down to zero, as might otherwise seem likely.

While this argument suggests that bitcoin will not soon disappear, the hopes of its promoters and supporters for continued appreciation to result in the collapse of fiat currencies and their replacement by bitcoin and possibly other cryptocurrencies seem destined for disappointment. Expectations of rapid appreciation do not attract new uses into the network of users of a medium of exchange. On the contrary, as implicitly recognized by the familiar proposition (now known as Gresham’s Law) that bad money drives out the good, the expectation of rapid appreciation deters, rather than attracts, traders from using the appreciating (good) money in exchange, encouraging instead the use of the alternative (bad) money whose value is expected to be comparatively stable. Centuries, if not millenia, of monetary experience have demonstrated the wisdom of this proposition over and over again.

The very success of bitcoin as a speculative asset turns out to be the kiss of death for its chances of ever displacing the dollar as the dominant currency in the world.