I notice that there has been a bit of a dustup lately about free banking, triggered by two posts by Izabella Kaminska, first on FTAlphaville followed by another on her own blog. I don’t want to get too deeply into the specifics of Kaminska’s posts, save to correct a couple of factual misstatements and conceptual misunderstandings (see below). At any rate, George Selgin has a detailed reply to Kaminska’s errors with which I mostly agree, and Scott Sumner has scolded her for not distinguishing between sensible free bankers, e.g., Larry White, George Selgin, Kevin Dowd, and Bill Woolsey, and the anti-Fed, gold-bug nutcases who, following in the footsteps of Ron Paul, have adopted free banking as a slogan with which to pursue their anti-Fed crusade.

Now it just so happens that, as some readers may know, I wrote a book about free banking, which I began writing almost 30 years ago. The point of the book was not to call for a revolutionary change in our monetary system, but to show that financial innovations and market forces were causing our modern monetary system to evolve into something like the theoretical model of a free banking system that had been worked out in a general sort of way by some classical monetary theorists, starting with Adam Smith, who believed that a system of private banks operating under a gold standard would supply as much money as, but no more money than, the public wanted to hold. In other words, the quantity of money produced by a system of competing banks, operating under convertibility, could be left to take care of itself, with no centralized quantitative control over either the quantity of bank liabilities or the amount of reserves held by the banking system.

So I especially liked the following comment by J. V. Dubois to Scott’s post

[M]y thing against free banking is that we actually already have it. We already have private banks issuing their own monies directly used for transactions – they are called bank accounts and debit/credit cards. There are countries like Sweden where there are now shops that do not accept physical cash (only bank monies) – a policy actively promoted government, if you can believe it.

There are now even financial products like Xapo Debit Card that automatically converts all payments received on your account into non-monetary assets (with Xapo it is bitcoins) and back into monies when you use the card for payment. There is a very healthy international bank money market so no matter what money you personally use, you can travel all around the world and pay comfortably without ever seeing or touching official local government currency.

In opposition to the Smithian school of thought, there was the view of Smith’s close friend David Hume, who famously articulated what became known as the Price-Specie-Flow Mechanism, a mechanism that Smith wisely omitted from his discussion of international monetary adjustment in the Wealth of Nations, despite having relied on PSFM with due acknowledgment of Hume, in his Lectures on Jurisprudence. In contrast to Smith’s belief that there is a market mechanism limiting the competitive issue of convertible bank liabilities (notes and deposits) to the amount demanded by the public, Hume argued that banks were inherently predisposed to overissue their liabilities, the liabilities being issuable at almost no cost, so that private banks, seeking to profit from the divergence between the face value of their liabilities and the cost of issuing them, were veritable engines of inflation.

These two opposing views of banks later morphed into what became known almost 70 years later as the Banking and Currency Schools. Taking the Humean position, the Currency School argued that without quantitative control over the quantity of banknotes issued, the banking system would inevitably issue an excess of banknotes, causing overtrading, speculation, inflation, a drain on the gold reserves of the banking system, culminating in financial crises. To prevent recurring financial crises, the Currency School proposed a legal limit on the total quantity of banknotes beyond which limit, additional banknotes could be only be issued (by the Bank of England) in exchange for an equivalent amount of gold at the legal gold parity. Taking the Smithian position, the Banking School argued that there were market mechanisms by which any excess liabilities created by the banking system would automatically be returned to the banking system — the law of reflux. Thus, as long as convertibility obtained (i.e., the bank notes were exchangeable for gold at the legal gold parity), any overissue would be self-correcting, so that a legal limit on the quantity of banknotes was, at best, superfluous, and, at worst, would itself trigger a financial crisis.

As it turned out, the legal limit on the quantity of banknotes proposed by the Currency School was enacted in the Bank Charter Act of 1844, and, just as the Banking School predicted, led to a financial crisis in 1847, when, as soon as the total quantity of banknotes approached the legal limit, a sudden precautionary demand for banknotes led to a financial panic that was subdued only after the government announced that the Bank of England would incur no legal liability for issuing banknotes beyond the legal limit. Similar financial panics ensued in 1857 and 1866, and they were also subdued by suspending the relevant statutory limits on the quantity of banknotes. There were no further financial crises in Great Britain in the nineteenth century (except possibly for a minicrisis in 1890), because bank deposits increasingly displaced banknotes as the preferred medium of exchange, the quantity of bank deposits being subject to no statutory limit, and because the market anticipated that, in a crisis, the statutory limit on the quantity of banknotes would be suspended, so that a sudden precautionary demand for banknotes never materialized in the first place.

Let me pause here to comment on the factual and conceptual misunderstandings in Kaminska’s first post. Discussing the role of the Bank of England in the British monetary system in the first half of the nineteenth century, she writes:

But with great money-issuance power comes great responsibility, and more specifically the great temptation to abuse that power via the means of imprudent money-printing. This fate befell the BoE — as it does most banks — not helped by the fact that the BoE still had to compete with a whole bunch of private banks who were just as keen as it to issue money to an equally imprudent degree.

And so it was that by the 1840s — and a number of Napoleonic Wars later — a terrible inflation had begun to grip the land.

So Kaminska seems to have fallen for the Humean notion that banks are inherently predisposed to overissue and, without some quantitative restraint on their issue of liabilities, are engines of inflation. But, as the law of reflux teaches us, this is not true, especially when banks, as they inevitably must, make their liabilities convertible on demand into some outside asset whose supply is not under their control. After 1821, the gold standard having been officially restored in England, the outside asset was gold. So what was happening to the British price level after 1821 was determined not by the actions of the banking system (at least to a first approximation), but by the value of gold which was determined internationally. That’s the conceptual misunderstanding that I want to correct.

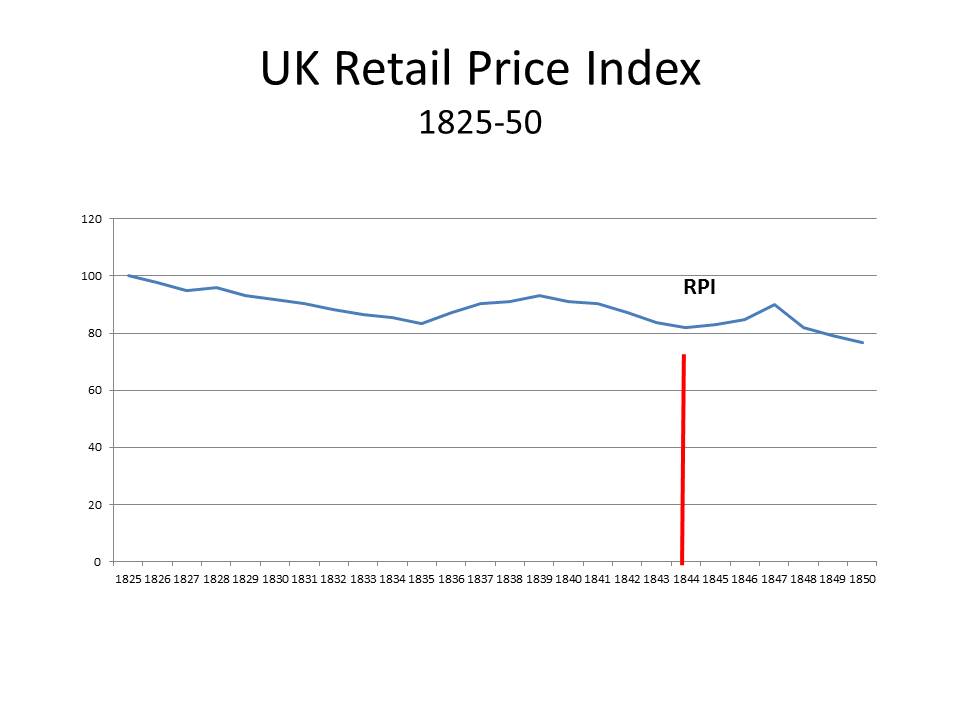

Now for the factual misunderstanding. The chart below shows the British Retail Price Index between 1825 and 1850. The British price level was clearly falling for most of the period. After falling steadily from 1825 to about 1835, the price level rebounded till 1839, but it prices again started to fall reaching a low point in 1844, before starting another brief rebound and rising sharply in 1847 until the panic when prices again started falling rapidly.

From a historical perspective, the outcome of the implicit Smith-Hume disagreement, which developed into the explicit dispute over the Bank Charter Act of 1844 between the Banking and Currency Schools, was highly unsatisfactory. Not only was the dysfunctional Bank Charter Act enacted, but the orthodox view of how the gold standard operates was defined by the Humean price-specie-flow mechanism and the Humean fallacy that banks are engines of inflation, which made it appear that, for the gold standard to function, the quantity of money had to be tied rigidly to the gold reserve, thereby placing the burden of adjustment primarily on countries losing gold, so that inflationary excesses would be avoided. (Fortunately, for the world economy, gold supplies increased fairly rapidly during the nineteenth century, the spread of the gold standard meant that the monetary demand for gold was increasing faster than the supply of gold, causing gold to appreciate for most of the nineteenth century.)

When I set out to write my book on free banking, my intention was to clear up the historical misunderstandings, largely attributable to David Hume, surrounding the operation of the gold standard and the behavior of competitive banks. In contrast to the Humean view that banks are inherently inflationary — a view endorsed by quantity theorists of all stripes and enshrined in the money-multiplier analysis found in every economics textbook — that the price level would go to infinity if banks were not constrained by a legal reserve requirement on their creation of liabilities, there was an alternative view that the creation of liabilities by the banking system is characterized by the same sort of revenue and cost considerations governing other profit-making enterprises, and that the equilibrium of a private banking system is not that value of money is driven down to zero, as Milton Friedman, for example, claimed in his Program for Monetary Stability.

The modern discovery (or rediscovery) that banks are not inherently disposed to debase their liabilities was made by James Tobin in his classic paper “Commercial Banks and Creators of Money.” Tobin’s analysis was extended by others (notably Ben Klein, Earl Thompson, and Fischer Black) to show that the standard arguments for imposing quantitative limits on the creation of bank liabilities were unfounded, because, even with no legal constraints, there are economic forces limiting their creation of liabilities. A few years after these contributions, F. A. Hayek also figured out that there are competitive forces constraining the creation of liabilities by the banking system. He further developed the idea in a short book Denationalization of Money which did much to raise the profile of the idea of free banking, at least in some circles.

If there is an economic constraint on the creation of bank liabilities, and if, accordingly, the creation of bank liabilities was responsive to the demands of individuals to hold those liabilities, the Friedman/Monetarist idea that the goal of monetary policy should be to manage the total quantity of bank liabilities so that it would grow continuously at a fixed rate was really dumb. It was tried unsuccessfully by Paul Volcker in the early 1980s, in his struggle to bring inflation under control. It failed for precisely the reason that the Bank Charter Act had to be suspended periodically in the nineteenth century: the quantitative limit on the growth of the money supply itself triggered a precautionary demand to hold money that led to a financial crisis. In order to avoid a financial crisis, the Volcker Fed constantly allowed the monetary aggregates to exceed their growth targets, but until Volcker announced in the summer of 1982 that the Fed would stop paying attention to the aggregates, the economy was teetering on the verge of a financial crisis, undergoing the deepest recession since the Great Depression. After the threat of a Friedman/Monetarist financial crisis was lifted, the US economy almost immediately began one of the fastest expansions of the post-war period.

Nevertheless, for years afterwards, Friedman and his fellow Monetarists kept warning that rapid growth of the monetary aggregates meant that the double-digit inflation of the late 1970s and early 1980s would soon return. So one of my aims in my book was to use free-banking theory – the idea that there are economic forces constraining the issue of bank liabilities and that banks are not inherently engines of inflation – to refute the Monetarist notion that the key to economic stability is to make the money stock grow at a constant 3% annual rate of growth.

Another goal was to explain that competitive banks necessarily have to select some outside asset into which to make their liabilities convertible. Otherwise those liabilities would have no value, or at least so I argued, and still believe. The existence of what we now call network effects forces banks to converge on whatever assets are already serving as money in whatever geographic location they are trying to draw customers from. Thus, free banking is entirely consistent with an already existing fiat currency, so that there is no necessary link between free banking and a gold (or other commodity) standard. Moreover, if free banking were adopted without abolishing existing fiat currencies and legal tender laws, there is almost no chance that, as Hayek argued, new privately established monetary units would arise to displace the existing fiat currencies.

My final goal was to suggest a new way of conducting monetary policy that would enhance the stability of a free banking system, proposing a monetary regime that would ensure the optimum behavior of prices over time. When I wrote the book, I had been convinced by Earl Thompson that the optimum behavior of the price level over time would be achieved if an index of nominal wages was stabilized. He proposed accomplishing this objective by way of indirect convertibility of the dollar into an index of nominal wages by way of a modified form of Irving Fisher’s compensated dollar plan. I won’t discuss how or why that goal could be achieved, but I am no longer convinced of the optimality of stabilizing an index of nominal wages. So I am now more inclined toward nominal GDP level targeting as a monetary policy regime than the system I proposed in my book.

But let me come back to the point that I think J. V. Dubois was getting at in his comment. Historically, idea of free banking meant that private banks should be allowed to issue bank notes of their own (with the issuing bank clearly identified) without unreasonable regulations, restrictions or burdens not generally applied to other institutions. During the period when private banknotes were widely circulating, banknotes were a more prevalent form of money than bank deposits. So in the 21st century, the right of banks to issue hand to hand circulating banknotes is hardly a crucial issue for monetary policy. What really matters is the overall legal and regulatory framework under which banks operate.

The term “free banking” does very little to shed light on most of these issues. For example, what kind of functions should banks perform? Should commercial banks also engage in investment banking? Should commercial bank liabilities be ensured by the government, and if so under what terms, and up to what limits? There are just a couple of issues; there are many others. And they aren’t necessarily easily resolved by invoking the free-banking slogan. When I was writing, I meant by “free banking” a system in which the market determined the total quantity of bank liabilities. I am still willing to use “free banking” in that sense, but there are all kinds of issues concerning the asset side of bank balance sheets that also need to be addressed, and I don’t find it helpful to use the term free banking to address those issues.

So a country like Canada now, where we have no reserve requirements, is almost a “free banking” country (we no longer have private bank notes, but we do have Canadian Tire money)?

Also, Canada pre-1914 was considered to be a “Free Banking” country. Do you agree with that (and does your book cover that history)?

LikeLike

Excellent article.

The Banking School believes that the law of reflux will lead to the quantity of bank liabilities being optimized as long as banks tie their issue of liabilities to an outside entity, like gold, or central bank base money.

I think you are endorsing this view as correct.

I have 2 questions.

You also talk about the need for “A new way of conducting monetary policy that would enhance the stability of a free banking system”. You now think that NGDP targeting may be central to this new policy.

So my first question is : If the banking system has market mechanisms that ensure that banks optimize the money supply, why is an additional monetary policy needed to enhance its stability ?

My second question is: Related to J.V. Dubois’s comment, do you believe that if the fed were to target NGDP and abandon any remnants of reserve requirements then the US banking system could be described as “free banking” ? If not, what additional changes would be needed ?

LikeLike

David:

Both you and the free bankers place too much emphasis on gold convertibility. The gold channel is not the only channel through which money can reflux to the issuing bank. Money can also reflux through the loan channel, the bond channel, the tax channel, and the used office furniture channel.

American colonial currencies (1690-1750) were virtually never convertible into gold or silver, but they were valued because the governments that issued them accepted them for taxes and loan repayments. Sometimes pegs were maintained and sometimes not, but it’s not the peg that matters. It’s the assets backing the money that matter.

LikeLike

Thank you David for sharing your thoughts on free banking.

Though your stance agrees with mine and Larry’s on some points, it differs on some other important ones, including (as you are aware) the merits of Banking School doctrines and of Fullarton’s “law of reflux” and their relevance to modern free banking theory. The difference seems worth pointing out here for the sake of your readers who may be unaware of it. In Free Banking in Britain Larry White distinguished “Banking School” from “Free Banking” School doctrines. Among other non-trivial differnces was the plain fact that the Banking School writers, and Tooke in particular, didn’t oppose the Bank of England’s monopoly. It was Tooke after all who once equated free trade in banking with free trade in swindling. So, while Banking School theorists may indeed have though the quantity of bank money to be capable of regulating itself, they didn’t see any crucial role for competition in banknote provision in this self regulation.

Instead their theory of bank money supply self-regulation hinged on the “law of reflux” to which you refer. According to that law, an excess supply of bank money is automatically eliminated by means of the repayment of bank loans. This idea suffers, first, from its confusion of demand for money balances with demand for credit, and, second, from its assumption that by having their loans repaid banks are somehow “constrained” not to lend again–as if, in finding themselves flush with reserves, they cannot manage, with the aid of generous enough terms, to find borrowers to take those reserves off their hands. As a theory of how competitive banks are prevented from over-issuing this is just plain wrong; as one of how even a monopoly issuer cannot over-issue, it is tragically misleading.

In our own work Larry and I have consistently rejected the law of reflux as Fullarton understood it. In my case I distinguish that law from what I call the law of “adverse clearings.” The difference is crucial but also simple: according to the latter law, competitive banks are prevented from expanding the money stock excessively, not by amplified loan repayments (again, that’s no constraint at all) but by the return of unwanted balances of their IOUs to rival banks and the consequent, regular settlement interbank dues. That only competing banks, and not a monopoly issuer like the Band of England, is constrained by adverse clearings is, or should be, very obvious. (I believe, by the way, that Smith may have had adverse clearings rather than Fullarton’s “reflux” in mind in speaking of the tendency of unwanted banknotes to “overflow” the channels of circulation.)

Turning to a second difference: The significance of the monopolization seems to us important mainly because it was the device that first allowed particular banks to escape the discipline of adverse clearings, and which, by so doing, made them uniquely capable of either generating excessive credit or triggering general credit crunches. (Bagehot covers this ground well.) The history of monetary instability is, to a very substantial extent, a history of the unintended consequences of currency monopolization. This point, which turns the conventional wisdom regarding the desirability of central banking on its head, cannot be emphasized enough in response to the contrary claim that currency monopolization is no longer of any importance.

This brings me to the last point, concerning what free banking is about. I also, believe it or not, don’t see free banking primarily as a call for reform. I see it as a research topic, analogous to the theory of free trade. Most people, including those who reject free trade, appreciate the importance of the theory even if they sometimes fail to grasp or accept its implications. The theory matters, because it supplies a crucial basis for examining the implications of tariffs and other sorts of departures from free trade. Someone obviously not versed in the basic trade theory cannot expect to be taken very seriously by other trade economists.

In my opinion our theories of money and banking suffer from lacking any similar foundation in free banking theory. When one hears pronouncements about the desirability or consequences of this or that set of interventions in banking, one is entitled to ask, “Compared to what alternative?” and, more specifically, “According to what theory of unregulated banking?” The free bankers may be accused of having only developed a very rudimentary theory–one that fails to shed light on a host of issues, as you observe in your last paragraphs. But we have at least tried to draw attention to the need for such a theory rather than the ad hoc alternatives that presently guide most understanding of bank regulation. By such I mean the set of a priori assumptions about unregulated banking that one encounters, not only in the pronouncements of non-economists like Ms. Kaminska, but no less in those of supposed experts. Listen to Ben Bernanke’s GW lectures, and you get the idea. Like it or not, all, including conventional, thinking about bank regulation rests on some (albeit implicit) theory of free banking. Incomplete as my and Larry’s theory may be, we still have reason to believe that it is at least better than the alternatives most economists tacitly rely upon!

LikeLike

“if free banking were adopted without abolishing existing fiat currencies and legal tender laws, there is almost no chance that, as Hayek argued, new privately established monetary units would arise to displace the existing fiat currencies”

In “The Denationalization of Money” Hayek argued that you should be able to pay taxes with privately-issued currencies. However, this would in effect turn those ‘private currencies into’ de facto state currencies, or forms of government ‘fiat money’. For some reason Hayek chose to ignore this massive contradiction in his argument. Essentially, what he was actually arguing was that private corporations should be be granted special state powers, i.e. the power to issue money backed by the state’s legal powers of taxation.

LikeLike

What would be the brief reason for why you now consider nominal income targeting to be superior to nominal wage targeting? Off the top of my head, I think that an NGDP target would perhaps require fewer nominal wage cuts, which are economically difficult. Or perhaps wages are too narrow a subset of factor prices in general, so factor prices should be stabilized while final output prices are allowed to fall? I believe that Selgin has made the latter argument.

LikeLike

phiippe101: Private bank deposits are today publicly receivable in payment of taxes (indeed, the IRS instructs taxpayers against remitting Federal Reserve notes), yet no one claims that this makes such deposits “de facto” state monies or “forms of government ‘fiat money’.”

In fact Hayek doesn’t contradict himself at all. He merely suggests that, as long as governments must also be paid, they should not discriminate against private currencies by refusing them in favor of their own fiat monies in payment. It is hard to imagine how else one could conceive of having the government provide for a “level playing field” among alternative competing currencies.

LikeLike

“Private bank deposits are today publicly receivable in payment of taxes”

Not really. Taxes are (ultimately) paid to the Treasury’s account at the central bank, i.e. they are paid with base money (state money), not with commercial bank deposits.

Furthermore, a bank deposit is a promise to pay state money. If tax was somehow paid with a commercial bank deposit, that would simply represent a loan from the Treasury to the issuing bank. As such the tax would not actually be paid – the bank would still owe it to the Treasury.

In Hayek’s scheme, in contrast, the privately-issued currencies are not promises to pay state money. They are more like bitcoin. If the government were to accept bitcoins in payment of taxes, that would obviously give a massive special state privilege to bitcoin.

“[Hayek] merely suggests that, as long as governments must also be paid, they should not discriminate against private currencies by refusing them in favor of their own fiat monies in payment”

So I should be able to pay my taxes by printing a number on a piece of paper and handing it to the Treasury?

Maybe I should also be able to pay my private debts by printing a number on a piece of paper and handing it to my creditor?

Of course that is nonsensical. What Hayek is actually advocating is that the government should give some private corporations special privileges.

LikeLike

“competitive banks are prevented from expanding the money stock excessively, not by amplified loan repayments (again, that’s no constraint at all) but by the return of unwanted balances of their IOUs to rival banks and the consequent, regular settlement interbank dues. ”

1. A bank whose assets move in step with its money-issue, and whose assets are enough to buy back all the money it has issued, can never be accused of “expanding the money stock excessively”. Remember that the bank only issued new dollars to people who wanted those dollars badly enough to offer at least a dollar’s worth of bonds and such in exchange. By analogy, a mint that issues 1 oz coins only to people who bring in 1 oz of silver will never issue excessive amounts of coins.

2. A note-issuing bank will find that there is a certain amount of dollars that the public wishes to hold. If the bank exceeds that amount, then unwanted notes will reflux to the bank and the bank’s assets will fall in step with its note-issue. If the bank issues too few notes, then the public will bring bonds in to the bank and ask for new notes. As the banker complies and issues more notes, it will also get new assets. Whether the notes are flowing in or out, the bank’s ratio of assets to notes will stay the same, and there will be no change in the value of the bank’s dollars. The so-called “constraint” of amplified loan repayments is irrelevant. The constraint that matters is that the bank wants to stay solvent, and such a bank will not try to offer “generous enough terms” in order to issue more notes than people want.

3. Interbank settlement is also irrelevant. Assume $1=1 oz. If a bank foolishly issues $1 for .99 oz., then whether that note is redeemed for 1 oz by rival banks or by the bank’s own customers, the loss of 0.01 oz is the same. But a bank that issued $1 for 1.00 oz has nothing to fear from refluxing notes, whether they came from customers or from rival banks.

LikeLike

“If the government were to accept bitcoins in payment of taxes, that would obviously give a massive special state privilege to bitcoin.” That would be so only if bitcoin were treated differently from other similarly worthy rival media of exchange. In principle (for I am not one to see much practicality in such an arrangement) that state might agree to accept any widely accepted exchange medium in payment of taxes. So long as the offer is extended broadly, with the intend of providing for equal treatment, “privilege” is the wrong word for it.

LikeLike

“Maybe I should also be able to pay my private debts by printing a number on a piece of paper and handing it to my creditor?

Of course that is nonsensical. ”

No it’s not. I do it all the time. I hand my $50 IOU to my mechanic, who pays it to his worker, who pays it to the grocer, who pays it to me in rent after a month. Or I could pay it to an IRS agent, who will cash it at my banker, who will pay it to the grocer, etc.

LikeLike

“That would be so only if bitcoin were treated differently from other similarly worthy rival media of exchange”

So the government decides which media are acceptable, and in so doing it also increases the acceptability and value of that media in the market.

So yes, it gives a special state privilege to the media that it accepts in payment.

LikeLike

Mike Sproul,

that’s not what I meant. If I write IOU $50 on a piece of paper I am promising to pay $50. That is not the same thing as paying a $50 debt by writing ’50 Phils’ on a piece of paper, handing it to the person and announcing that the debt is paid.

LikeLike

Philippe, how would you have the state adopt a neutral stance in a world of multiple currencies? Surely not by having it accept only its own product, and not by having it refuse to be paid altogether. If Hayek’s view strikes you as unreasonable, what alternative would you have had him take?

Regardless of your reply, I think your last reply perfectly unsatisfactory. Of course governments buy all sorts f private goods every day as they must if they are not to produce everything under the son. They therefore add to the demand for so many private goods their own demand for them. Yet no one imagine that competition is thereby thwarted in all the affected industries.

LikeLike

The key point in tax payments is that cheques used to pay tax are accepted at par by the Treasury. Although bank money is not state money, it has a legal privilege. This legal privilege is missing from shadow banking entities, like commercial paper.

Based on the text “Understanding Modern Money” by Randall Wray, cheques in the United States (or checks, as they would write it) did not necessarily clear at par in earlier periods (I am working from memory, so I forget what changed that status – the Fed?). This made bank money quite distinct from state money.

In order for cheques to clear at par, the government has to trust the banks. The only way that will work is if they are regulated; it would make little sense to do something like trust rating agencies. It would seem suicidal to allow unregulated entities access to a government-backed settlement system.

LikeLike

Mike Sproul,

“Or I could pay it to an IRS agent”

Except you can’t actually do that. The IRS is not in the business of giving out loans to everyone who scribbles “IOU” on a piece of paper.

LikeLike

Brian,

“The key point in tax payments is that cheques used to pay tax are accepted at par by the Treasury”

Tax payments are ultimately paid into the Treasury’s account at the central bank. That can only be done by transferring reserve balances from commercial bank reserve accounts to the Treasury’s account (or by the central bank directly crediting the Treasury’s account without simultaneously debiting a commercial bank account). So at the end of the day taxes are paid with the state’s currency, not with checks or bank deposits.

LikeLike

“The IRS is not in the business of giving out loans to everyone who scribbles “IOU” on a piece of paper.”

Of course they are. People make promises to pay the IRS all the time.

LikeLike

Mike, you can’t write “IOU $50” and post it to the IRS to “pay” your taxes. They do accept IOUs from banks and some other financial institutions, such as checks, but then payment has to be made by these institutions to the treasury.

LikeLike

Good post David, and good comment George.

I have one disagreement with George, but it might be mostly semantic. When George distinguishes between “monopoly” and “competitive” banks, what is at the root of this distinction? I would say it is the distinction between what I call “alpha” and “beta” banks: beta banks promise to redeem their notes for alpha notes at par, but alpha banks make no such promise the other way. It’s asymmetric redeemability.

In defence of Hume, if the introduction of competitive banks creates a close substitute to gold that reduces the (global) demand to hold gold, then this would be inflationary. (But if Hume was talking about introducing banks in a *small* open economy, my defence would not work. And when David says that banks had no effect on the price level “(at least to a first approximation)” is that referring to the small country assumption as being approximately true?)

LikeLike

Nick Rowe asks, “When George distinguishes between “monopoly” and “competitive” banks, what is at the root of this distinction?”

In the historical context to which much of David’s remarks refer, the distinction was simple enough, because it boils down to having or not having multiple banks issuing notes redeemable in some non-bank commodity money. Today competitive note issue would mean letting commercial banks issue notes redeemable in central bank notes. The central bank would remain a monopoly supplier of (fiat) base money, but not a monopoly supplier of hand-to-hand paper currency.

LikeLike

The Monetary Proposal put forward by Friedman was simply the best way to ensure economic stability over a long period of time. He didn’t say it was a perfect gadget, and so, of course, unknown situations could occur that would necessitate other measures. Also, there are other such targeted proposals, other than the money supply, I guess, that could possibly work. But the intent is the same in both cases, as far as I can determine. How they will work in practice is an empirical question.

This was as opposed to a Group of Managers deciding what to do ( or a Gold Standard, say) at any given time. There might have been an expansion after 1982, but the question would be whether or not wise policies were followed after that, and to what extent those policies led to 2008. In other words, did the Group of Managers make mistakes, and how large were they?

James Tobin turning up really surprised me, because, unless I’m wrong, both he and Friedman supported Narrow Banking, largely, I thought, for the same reasons, dealing with the best plan for long term economic stability. In fact, the Monetary Proposal was simply one part of a plan for economic stability that included Narrow Banking. I’m not sure I see how your historical presentation ( which I certainly learned from ) obviates the need for such a proposal even today, other than saying Friedman’s targeted plan didn’t work out in practice. But even by your account, that had to be seen in action to determine its efficacy. Theory alone wasn’t enough.

Donald Pretari

LikeLike

Brian, I never heard of Canadian Tire money. I don’t know that much about Canadian monetary history except that there was no central bank, no or few restrictions on branch banking and not many bank failures during the Great Depression. So I don’t feel competent to judge whether Canada is or is not a free banking country. At any rate, my view is that free banking is not an absolute, and I don’t think that some relatively low level of legal reserve requirements would necessarily be inconsistent with free banking. Reserve requirements are a tax; free banking doesn’t require that banks not be subject to taxation.

Rob, My view is that the optimal behavior of the price level is unlikely to be achieved without some deliberate central guidance. The basic reason is that the benefits from monetary stability are public and not confined to holders of cash. Those rather large externalities imply that banks have an insufficient incentive to generate the optimal time path for the price level. I think your second question is largely a matter of semantics, so please excuse me if I don’t see any point in trying to answer it.

Mike, I think that we have previously discussed this point. I don’t see how the backing theory pins down any particular value of money. Your backing theory simply says that the total value of outstanding liabilities on the banks’ balance sheets must equal the value of their assets, but without some nominal anchor that could be true at a very broad range of price levels.

George, Thanks for your very thoughtful comment. I am aware that Larry White and you have a rather different understanding from mine of how competition in banking works. While I agree with you that competition is important, we disagree on the consequences of a lack of competition. I also think that competition between deposit-taking banks and note-issuing banks is also important and provides a very powerful constraint on the note-issuing banks. While I prefer Fullarton to Tooke as a monetary theorist, and have read Fullarton more carefully than Tooke, I think that you may be being unfair to Tooke by citing that particular quotation. I think Tooke started out his career as an exponent of Currency School ideas, and that quotation may have been taken from his early Currency School period. I totally agree with your comparison of free trade theory with free banking theory and I think you have provided a good explanation of how free banking theory can be useful even if one isn’t committed to free banking as an ideological principle. Let me just ask you this question. How does Tobin’s paper “Commercial Banks as Creators of Money” fit into your conceptual framework for monetary theory.

Philippe, I think that Hayek simply wanted to put all currencies on an equal footing, and not give government currencies a competitive advantage over privately issued currencies. He believed that, otherwise unredeemable private currencies could nevertheless maintain a positive value, but provided no explanation for why those currencies would retain value if they were not redeemable into an outside asset, so I think that there was a logical flaw in his argument.

Kevin, I don’t necessarily think that NGDP targeting is superior to targeting a wage index, I think it would be more correct to say that I am agnostic on the question. One reason for my loss of enthusiasm for targeting a wage index is that I am troubled by the zero-lower bound problem that would arise with low real interest rates and non-increasing average wages. Thompson’s argument for stabilizing a wage index was based on a search-theoretic model, and I am dubious about how well search theory captures the relevant features of the labor market.

Nick, I agree that by creating a substitute for gold used as money, banks tend to reduce the demand for gold and thereby reducing its value, which would be inflationary. So yes, my qualification about the effect on prices being nil could be understood as a reference to the a small country assumption, but there are other possible complicating effects that could also be subsumed under the first approximation rubric.

LikeLike

David:

“Your backing theory simply says that the total value of outstanding liabilities on the banks’ balance sheets must equal the value of their assets, but without some nominal anchor that could be true at a very broad range of price levels.”

Simple. If bank has issued $100 and holds assets worth 100 oz, then $1=1 oz. Maybe the bank will offer instant metallic convertibility at that rate, or maybe it will promise convertibility at that rate 100 years from now, or maybe it will peg its dollars at that rate, and then use open market operations to keep it there, without ever offering true metallic convertibility.

LikeLike

Very elegant. But somehow we still got the sub-prime crisis where banks over-lent (though in an environment of low inflation, thanks to the Fed and prior policy). That hardly indicates that banks are automatically responsible due to market forces. There is an ever-present temptation, as Hume probably saw, so run a short-term scam to make the bank officers rich, at the expense of a lot of borrowers and shareholders down the line. This doesn’t (hopefully) swing the whole monetary boat, but it does mean that the banks need close supervision.

LikeLike

David,

“He believed that, otherwise unredeemable private currencies could nevertheless maintain a positive value, but provided no explanation for why those currencies would retain value if they were not redeemable into an outside asset, so I think that there was a logical flaw in his argument.”

Well if they were accepted by the government in payment of taxes, they would be backed by taxation just as state ‘fiat’ money is today. Which would mean that they weren’t actually private currencies, but state currencies issued by private corporations with the legal privilege to print state money.

LikeLike

Philippe, You raise an interesting point, but aren’t you proving too much? What other than state fiat money, would you allow the government to accept in payment of taxes?

LikeLike

David, it seems to me that ideally the government should just accept its own fiat currency in payment of taxes, if it can. I don’t see the point of setting up an artificial market for pretend ‘private’ currencies, assuming such a thing is even workable. What are the benefits supposed to be?

LikeLike

You tip your hand with these last remarks, Philippe. Its evident from them that you simply dislike the idea of private currencies, and would rather that official fiat money were all that were permitted. That’s a position. But it isn’t an argument.

LikeLike

No, I don’t particularly mind private currencies, such as bitcoin. I’m not a fan of pseudo-private currencies backed by state taxation.

I only said that ideally the government should just accept its own currency in payment of taxes. That doesn’t mean people couldn’t use other things for private exchanges.

But if you wanted to get rid of all existing limitations on private currency issuance you’d have to present a decent argument for why it would be beneficial. If the only real purpose was anti-government sentiment then that’s not much of a reason.

Hayek argued that the main benefit of his scheme was that it would generally result in zero inflation/deflation. But according to most economists that isn’t even a desirable target.

LikeLike

Philipe, to say that a state “backs” a currency by its taxation just because it receives the currency in payments is nonsense. It amounts to a sort of doublespeak designed in effect to justify having the government suppress potential alternatives to its own currency by refusing to accept them. I return to my original case of bank deposits. You claimed it didn’t count, but in fact it does, for by your logic in accepting them the government doesn’t merely accept its own money: it accepts and therefore favors a private substitute. Were you consistent you should argue that the IRS should only accept government fiat money itself, and stop subsidizing those private money substitutes known as checking accounts.

The remark about Hayek’s scheme favoring zero inflation is beside the point of this discussion, but for what its worth most economists did in fact favor zero when he wrote his book. The notion that “2%” was the lowest safe level hadn’t yet caught on. That it is now conventional wisdom doesn’t make it right, either,

LikeLike

Phillippe101:

Here’s an old comment of mine that is relevant to taxes backing money:

A landlord collects rent of 50 oz of silver per year in perpetuity. At an interest rate of 5%, this makes his land worth 1000 oz. So we could say his assets consist of land worth 1000 oz, or alternatively, his assets consist of 1000 oz worth of “rents receivable”. if he has no debts, his net worth is 1000 oz.

The landlord could pay for his groceries by handing the grocer a slip of paper that says “OK for 1 oz rent on my property”. The grocer might accept the slip if he rents from the landlord or does business with someone who does. The landlord could issue up to 1000 of those slips and spend them, and they might circulate as money, adequately backed by the 1000 oz of rents receivable. The landlord might have gotten his land by theft, and he might threaten to imprison tenants who don’t pay, but that’s beside the point. His slips are backed by “rents receivable”, regardless of whether he’s a nice guy.

Change “landlord” to “Argentine government”, and change “rents receivable” to “taxes receivable”, and the Argentine episode is explained.

At this point the landlord could freeze the quantity of slips and declare that new slips will only be issued to those who deposit 1 oz of silver. No problem. As each new slip is issued, he gets another oz, so 1 slip is still worth 1 oz. Plus he now has some silver, so he could start to offer “silver convertibility” in addition to the “rent convertibility” that he already offers. If those silver-issued slips are all redeemed for silver, so that he’s back to having 1000 oz of rents backing 1000 slips, then 1 slip is still worth 1 oz, but quantity theorists might make the mistake of thinking “inconvertible”=”unbacked”, and declare that the slips are now unbacked “fiat” money.

LikeLike

Bank deposits are not private currencies. Bank deposits are promises to pay the state’s currency. They are bank debts, owed to the depositor, the creditor.

If you pay your taxes from your bank account (rather than, say, with cash), you are simply instructing your bank to pay the money to the government on your behalf. Your bank then owes that money (money which it can’t create itself), until the payment is made.

LikeLike

Irrelevant, Philippe. The state is still “supporting” substitutes for its own currency. That they are substitutes that depend on redeemability into state fiat money doesn’t in any obvious way contradict that fact.

LikeLike

The Town of James Island collects taxes. We always receive dollar denominated checks. We never cash them for currency and have no account at the Federal Reserve. We deposit all of the tax monies we receive in to our bank. Now, I am sure that when we accept checks drawn on other banks and deposit them, they are cleared through the Federal Reserve and net clearing balances are settled automatically by changes in our bank’s deposit at the Fed.

Does the Town of James Island sufficient to make sure that Federal Reserve notes have value?

My understanding is that Panama solely uses U.S. dollars for currency. Suppose it goes to free banking, and notes and deposits are redeemable for U.S. currency. Clearing is handled by a private clearinghouse. The clearinghouse holds U.S. government bonds as an asset.

The Panamanian national government accepts checks in payment of taxes.

1. It only accepts checks from Panamanian banks, but only if the check clears through the private clearinghouse.

2. It accepts checks drawn on U.S. banks too.

3. It accepts checks drawn on European banks, but only denominated in dollars.

4. It accepts checks drawn on European banks drawn in Euros at the current exchange rate.

Is Panama’s tax payment policy sufficient to maintain the purchasing power of the U.S. dollar? The Euro?

LikeLike