One of my few, and not very compelling, claims to fame is a (still unpublished) paper (“The Fisher Effect Under Deflationary Expectations“) that I wrote in late 2010 in which I used the Fisher Equation relating the real and nominal rates of interest via the expected rate of inflation to explain what happens in a financial panic. I pointed out that the usual understanding that the nominal rate of interest and the expected rate of inflation move in the same direction, and possibly even by the same amount, cannot be valid when the expected rate of inflation is negative and the real rate is less than expected deflation. In those perilous conditions, the normal equilibrating process, by which the nominal rate adjusts to reflect changes in inflation expectations, becomes inoperative, because the nominal rate gets stuck at zero. In that unstable environment, the only avenue for adjustment is in the market for assets. In particular, when the expected yield from holding money (the expected rate of deflation) approaches or exceeds the expected yield on real capital, asset prices crash as asset owners all try to sell at the same time, the crash continuing until the expected yield on holding assets is no longer less than the expected yield from holding money. Of course, even that adjustment mechanism will restore an equilibrium only if the economy does not collapse entirely before a new equilibrium of asset prices and expected yields can be attained, a contingency not necessarily as unlikely as one might hope.

I therefore hypothesized that while there is not much reason, in a well-behaved economy, for asset prices to be very sensitive to changes in expected inflation, when expected inflation approaches, or exceeds, the expected return on capital assets (the real rate of interest), changes in expected inflation are likely to have large effects on asset values. This possibility that the relationship between expected inflation and asset prices could differ depending on the prevalent macroeconomic environment suggested an empirical study of the relationship between expected inflation (as approximated by the TIPS spread on 10-year Treasuries) and the S&P 500 stock index. My results were fairly remarkable, showing that, since early 2008 (just after the start of the downturn in late 2007), there was a consistently strong positive correlation between expected inflation and the S&P 500. However, from 2003 to 2008, no statistically significant correlation between expected inflation and asset prices showed up in the data.

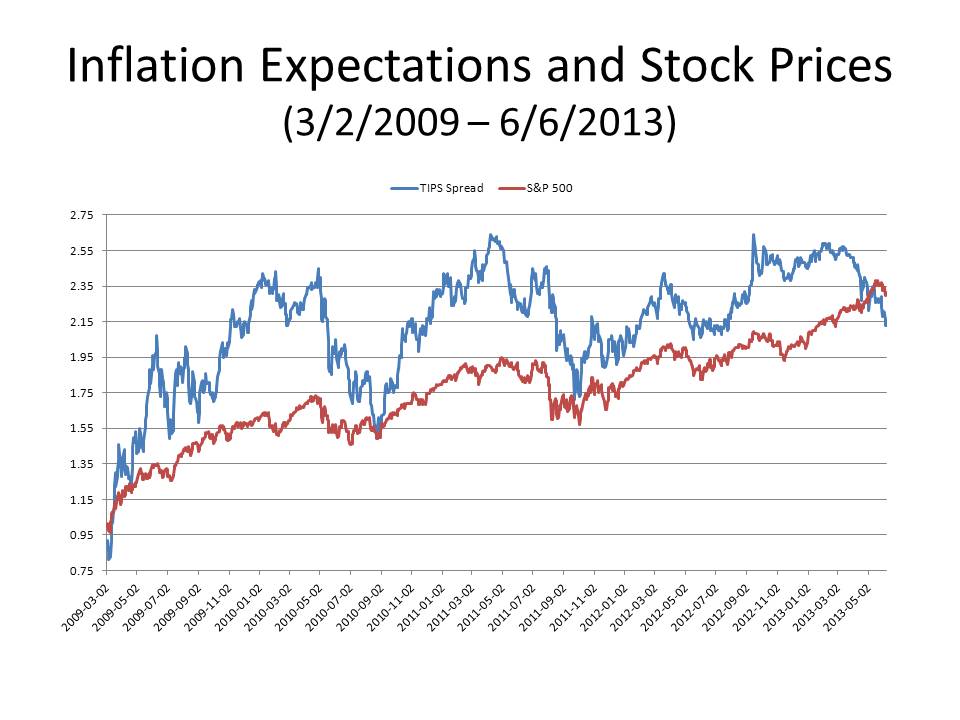

Ever since then, I have used this study (and subsequent informal follow-ups that have consistently generated similar results) as the basis for my oft-repeated claim that the stock market loves inflation. But now, guess what? The correlation between inflation expectations and the S&P 500 has recently vanished. The first of the two attached charts plots both expected inflation, as measured by the 10-year TIPS spread, and the S&P 500 (normalized to 1 on March 2, 2009). It is obvious that two series are highly correlated. However, you can see that over the last few months it looks as if the correlation has been reversed, with inflation expectations falling even as the S&P 500 has been regularly reaching new all-time highs.

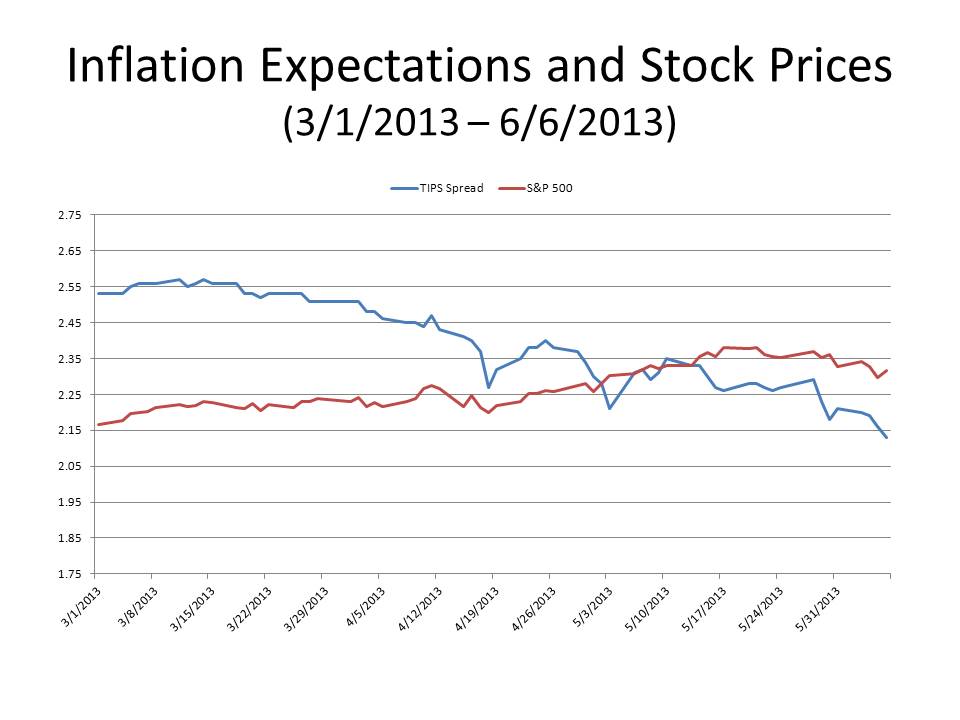

Here is a second chart that provides a closer look at the behavior of the S&P 500 and the TIPS spread since the beginning of March.

So what’s going on? I wish I knew. But here is one possibility. Maybe the economy is finally emerging from its malaise, and, after four years of an almost imperceptible recovery, perhaps the overall economic outlook has improved enough so that, even if we haven’t yet returned to normalcy, we are at least within shouting distance of it. If so, maybe asset prices are no longer as sensitive to inflation expectations as they were from 2008 to 2012. But then the natural question becomes: what caused the economy to reach a kind of tipping point into normalcy in March? I just don’t know.

And if we really are back to normal, then why is the real rate implied by the TIPS negative? True, the TIPS yield is not really the real rate in the Fisher equation, but a negative yield on a 10-year TIPS does not strike me as characteristic of a normal state of affairs. Nevertheless, the real yield on the 10-year TIPS has risen by about 50 basis points since March and by 75 basis points since December, so something noteworthy seems to have happened. And a fairly sharp rise in real rates suggests that recent increases in stock prices have been associated with expectations of increasing real cash flows and a strengthening economy. Increasing optimism about real economic growth, given that there has been no real change in monetary policy since last September when QE3 was announced, may themselves have contributed to declining inflation expectations.

What does this mean for policy? The empirical correlation between inflation expectations and asset prices is subject to an identification problem. Just because recent developments may have caused the observed correlation between inflation expectations and stock prices to disappear, one can’t conclude that, in the “true” structural model, the effect of a monetary policy that raised inflation expectations would not be to raise asset prices. The current semi-normal is not necessarily a true normal.

So my cautionary message is: Don’t use the recent disappearance of the correlation between inflation expectations and asset prices to conclude that it’s safe to abandon QE.