Earlier in the week, Paul Krugman wrote about the Volcker disinflation of the 1980s. Krugman’s annoyance at Stephen Moore (whom Krugman flatters by calling him an economist) and John Cochrane (whom Krugman disflatters by comparing him to Stephen Moore) is understandable, but he has less excuse for letting himself get carried away in an outburst of Keynesian triumphalism.

Right-wing economists like Stephen Moore and John Cochrane — it’s becoming ever harder to tell the difference — have some curious beliefs about history. One of those beliefs is that the experience of disinflation in the 1980s was a huge shock to Keynesians, refuting everything they believed. What makes this belief curious is that it’s the exact opposite of the truth. Keynesians came into the Volcker disinflation — yes, it was mainly the Fed’s doing, not Reagan’s — with a standard, indeed textbook, model of what should happen. And events matched their expectations almost precisely.

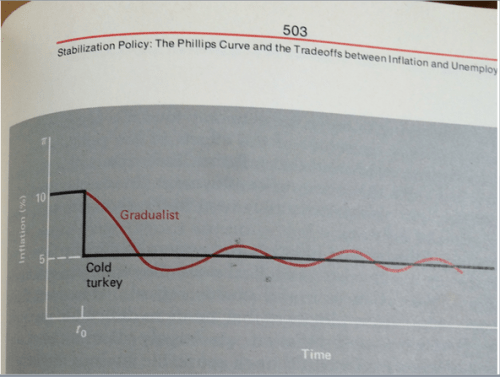

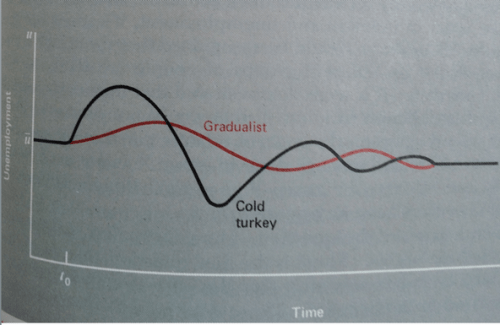

I’ve been cleaning out my library, and just unearthed my copy of Dornbusch and Fischer’s Macroeconomics, first edition, copyright 1978. Quite a lot of that book was concerned with inflation and disinflation, using an adaptive-expectations Phillips curve — that is, an assumed relationship in which the current inflation rate depends on the unemployment rate and on lagged inflation. Using that approach, they laid out at some length various scenarios for a strategy of reducing the rate of money growth, and hence eventually reducing inflation. Here’s one of their charts, with the top half showing inflation and the bottom half showing unemployment:

Not the cleanest dynamics in the world, but the basic point should be clear: cutting inflation would require a temporary surge in unemployment. Eventually, however, unemployment could come back down to more or less its original level; this temporary surge in unemployment would deliver a permanent reduction in the inflation rate, because it would change expectations.

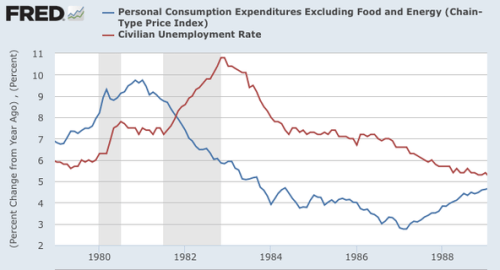

And here’s what the Volcker disinflation actually looked like:

A temporary but huge surge in unemployment, with inflation coming down to a sustained lower level.

So were Keynesian economists feeling amazed and dismayed by the events of the 1980s? On the contrary, they were feeling pretty smug: disinflation had played out exactly the way the models in their textbooks said it should.

Well, this is true, but only up to a point. What Krugman neglects to mention, which is why the Volcker disinflation is not widely viewed as having enhanced the Keynesian forecasting record, is that most Keynesians had opposed the Reagan tax cuts, and one of their main arguments was that the tax cuts would be inflationary. However, in the Reagan-Volcker combination of loose fiscal policy and tight money, it was tight money that dominated. Score one for the Monetarists. The rapid drop in inflation, though accompanied by high unemployment, was viewed as a vindication of the Monetarist view that inflation is always and everywhere a monetary phenomenon, a view which now seems pretty commonplace, but in the 1970s and 1980s was hotly contested, including by Keynesians.

However, the (Friedmanian) Monetarist view was only partially vindicated, because the Volcker disinflation was achieved by way of high interest rates not by tightly controlling the money supply. As I have written before on this blog (here and here) and in chapter 10 of my book on free banking (especially, pp. 214-21), Volcker actually tried very hard to slow down the rate of growth in the money supply, but the attempt to implement a k-percent rule induced perverse dynamics, creating a precautionary demand for money whenever monetary growth overshot the target range, the anticipation of an imminent future tightening causing people, fearful that cash would soon be unavailable, to hoard cash by liquidating assets before the tightening. The scenario played itself out repeatedly in the 1981-82 period, when the most closely watched economic or financial statistic in the world was the Fed’s weekly report of growth in the money supply, with growth rates over the target range being associated with falling stock and commodities prices. Finally, in the summer of 1982, Volcker announced that the Fed would stop trying to achieve its money growth targets, and the great stock market rally of the 1980s took off, and economic recovery quickly followed.

So neither the old-line Keynesian dismissal of monetary policy as irrelevant to the control of inflation, nor the Monetarist obsession with controlling the monetary aggregates fared very well in the aftermath of the Volcker disinflation. The result was the New Keynesian focus on monetary policy as the key tool for macroeconomic stabilization, except that monetary policy no longer meant controlling a targeted monetary aggregate, but controlling a targeted interest rate (as in the Taylor rule).

But Krugman doesn’t mention any of this, focusing instead on the conflicts among non-Keynesians.

Indeed, it was the other side of the macro divide that was left scrambling for answers. The models Chicago was promoting in the 1970s, based on the work of Robert Lucas and company, said that unemployment should have come down quickly, as soon as people realized that the Fed really was bringing down inflation.

Lucas came to Chicago in 1975, and he was the wave of the future at Chicago, but it’s not as if Friedman disappeared; after all, he did win the Nobel Prize in 1976. And although Friedman did not explicitly attack Lucas, it’s clear that, to his credit, Friedman never bought into the rational-expectations revolution. So although Friedman may have been surprised at the depth of the 1981-82 recession – in part attributable to the perverse effects of the money-supply targeting he had convinced the Fed to adopt – the adaptive-expectations model in the Dornbusch-Fischer macro textbook is as much Friedmanian as Keynesian. And by the way, Dornbush and Fischer were both at Chicago in the mid 1970s when the first edition of their macro text was written.

By a few years into the 80s it was obvious that those models were unsustainable in the face of the data. But rather than admit that their dismissal of Keynes was premature, most of those guys went into real business cycle theory — basically, denying that the Fed had anything to do with recessions. And from there they just kept digging ever deeper into the rabbit hole.

But anyway, what you need to know is that the 80s were actually a decade of Keynesian analysis triumphant.

I am just as appalled as Krugman by the real-business-cycle episode, but it was as much a rejection of Friedman, and of all other non-Keynesian monetary theory, as of Keynes. So the inspiring morality tale spun by Krugman in which the hardy band of true-blue Keynesians prevail against those nasty new classical barbarians is a bit overdone and vastly oversimplified.

Except Volker introduced tight money when Carter was in power. The loose fiscal policy came later wouldn’t you say?

LikeLike

Correct, he did introduce tight money under Carter in 1979, the economy went into a recession, and Carter, in a battle with Teddy Kennedy for the Democratic nomination for President, was able to persuade Volcker to relax the tight money policy, so the economy staged a recovery of sorts in 1980 until Reagan was elected and promised Volcker that he would give tight money his political support.

LikeLike

Dumb question – How many people did Volcker personally hire / fire during his tenure?

Had Volcker at any time during his tenure publicly announced that they were targeting the rate of employment?

Volcker (to delight of monetarists) announced that he was targeting the money supply growth rate, but where / when did he announce that he was targeting the unemployment rate?

Krugman’s declaration:

“Not the cleanest dynamics in the world, but the basic point should be clear: cutting inflation would require a temporary surge in unemployment.”

Never mind that you can’t extrapolate causality from the graphs that are shown. Notice the cause and effect here that Krugman describes. He does not say that if the Fed reduces the inflation rate, that will put a lot of people out of work. He says that people must be put out of work to reduce the inflation rate.

Now take a look at Federal government employment during the early Reagan years:

http://research.stlouisfed.org/fred2/series/CES9091000001

Was the fall in federal employment from 3.2 million in April of 1980 to 2.8 million in April of 1982 fiscal or monetary policy? Who should get credit for the temporary decrease in government employment – Reagan or Volcker?

LikeLike

“Was the fall in federal employment from 3.2 million in April of 1980 to 2.8 million in April of 1982 fiscal or monetary policy? Who should get credit for the temporary decrease in government employment – Reagan or Volcker?”

Find out who deserves the credit for similar declines in 1990 , 2000 , and 2010 and you’ll have an answer , of sorts. The list of those responsible may run in the thousands :

https://www.census.gov/history/www/reference/legislation/

LikeLike

To quick questions:

1. You leap from Keynesians thinking taxes matter for inflation to “dismissing monetary policy as irrelevant”. There’s obviously a gargantuan difference between the two. Can you clarify how you get from one to the other?

2. I just want to clarify – you agree that Krugman is not criticizing Friedman over the Lucas comment right? I had taken that to be a criticism of RE, not monetarism. You seem to be acting like Krugman was criticizing Friedman and I don’t quite understand how he is.

LikeLike

It’s Dornbusch, not Dornbush.

Like the previous commenter, I think you’re misreading Krugman somewhat. As I read him, he agrees with Friedman on many things, obviously not including admiration for Pinochet and Ayn Rand. Many of his own teachers were influenced by Friedman (Robert Hall is another obvious example) and he doesn’t fault them for that. His beef is with the likes of Lucas and Prescott.

I think Krugman, like Tobin, sees Friedman’s monetary theory as part of the tradition initiated by Irving Fisher and developed by Keynes.

LikeLike

“…but the attempt to implement a k-percent rule induced perverse dynamics, creating a precautionary demand for money whenever monetary growth overshot the target range, the anticipation of an imminent future tightening causing people, fearful that cash would soon be unavailable, to hoard cash by liquidating assets before the tightening.”

Interesting observation. It reminds me of the post Peel’s Act period, when the Bank of England issue department and banking department were created. I’m sure you know all this, but the Act prevented the Issue Department from providing the Banking Department with bank notes. If people were worried that the Banking Department might run out of notes, they’d withdraw now thereby precipitating the very crisis they were anticipating. It seems to me that attempts to limit the quantity of money are prone to setting-off these sorts of perverse dynamics.

LikeLike

What I don’t understand is why Cochrane ran a tight fiscal policy. Cochrane says Reagan ran a primary budget balance, but the record shows Reagan ran large primary or operating deficits. Cochrane says thus the Reagan-Volcker policies were coordinated. Alan Meltzer says Reagan’s fiscal and monetary policies were incoherent. Forgotten today is how distressed Reaganauts were with Volcker, and Treasury Secy Don Regan floated a plan to move the Fed into the Treasury…not a bad plan, actually.

LikeLike

Ben,

Read:

Click to access fightingInflationCongressWhiteHouse.pdf

———————————————————————————————

Reagan’s Treasury Secretary Donald Regan told his senior staff during one of their first meetings, “I don’t know why we need an independent Federal Reserve Board.”

Later into Reagan’s first term:

“There is, on the one hand, an argument to keep the Fed independent to avoid the problem of an administration running away on an inflationary policy,” Treasury Under- secretary Beryl W. Sprinkel told a reporter.

“But on the other hand, the president is elected by all the people and he has a right to put his policies into being and to be held accountable for them. And since we have been down here we have not gotten the kind of monetary policy that we asked for.”

News that the study was being conducted angered Wall Street.

“Interference with the central bank would be taken very poorly in the investment community,” an unnamed money manager told The New York Times.

“Paul Volcker … has become the whipping boy for high interest rates and the administration is delighted to have somebody they can point the finger at.

But, in truth, the administration would be lost without him – and so would the credibility of the fight against inflation.”

With investors turning angry, Treasury Secretary Regan seemingly backed off, saying during a press conference, “I think the Fed’s independence is a good thing.”

—————————————————————————————-

And so Ben, which side do you fall on? I seem to recall you in several posts giving Volcker credit for the reduction in inflation – which squares with the Wall Street view of the 1980’s – independent monetary policy enacted by the central back led to a reduction in inflation. Regan’s background was head of Merrill Lynch before becoming Treasury Secretary, and so when threatened by Wall Street, he did an about face on the need for independence of monetary policy.

Your statement:

Finally – Treasury Secy Don Regan floated a plan to move the Fed into the Treasury…not a bad plan, actually.

No, that was Ted Kennedy during his Senate election campaign in 1982.

LikeLike

Frank Restly: I like the Don Regan plan. The President should make monetary policy, and voters can toss him out if they think he has done a bad job.

BTW, we trust the President with nukes, bio-weapons, certain health policies and more. But not monetary policy?

LikeLike

“BTW, we trust the President with nukes, bio-weapons, certain health policies and more. But not monetary policy?”

We do? See:

http://en.wikipedia.org/wiki/Article_One_of_the_United_States_Constitution#Section_8:_Powers_of_Congress

Congress’s legislative powers are enumerated in Section Eight – “To declare War, grant Letters of Marque and Reprisal, and make Rules concerning Captures on Land and Water”

Perhaps you have heard of the phrase “Separation of Powers”?

You would prefer the President be lawmaker, judge, jury, and executioner in all legal matters? I believe that is called imperialism.

LikeLike

Dr. Glasner, I’m curious what your take is of this book review on the gold standard, WWI, WWII and the relative power of the U.S. and Germany……

http://www.theatlantic.com/international/archive/2014/12/the-real-story-of-how-america-became-an-economic-superpower/384034/?single_page=true

LikeLike

Lars Christensen and Lorenzo from Oz on Adam Tooze:

http://marketmonetarist.com/category/adam-tooze

LikeLike

Frank, I have no recollection of Volcker ever saying that he was targeting the rate of unemployment. The rise in unemployment was, I think, viewed as collateral damage of the reduction in inflation. I think the question whether you say people will be put out of work if the Fed reduces inflation or that people must be put out of work for the inflation rate to be reduced is largely, if not entirely, a question of semantics.

Marko, Interesting point.

Daniel, I was making the point in the context of the controversy about fiscal policy and monetary policy in the late 1970s and early 1980s. Keynesians were warning that tax cuts were inflationary. Taxes were cut, and inflation came down. It seemed, that at least at some superficial level, that monetary policy dominated fiscal policy. Dismissing monetary policy as irrelevant was probably not a good characterization of what most American Keynesians thought, but I think there were a fair number of prominent English Keynesian – Nicholas Kaldor and Joan Robinson are two names that come to mind – who might well have espoused that view.

Kevin, Yes I know, and I did actually spell it correctly part of the time.

Do you know of any instances in which Friedman expressed admiration for Ayn Rand? His record on Pinochet is far from spotless, but I don’t recall his have expressed admiration for the General. Again, my problem was not that Krugman was criticizing Friedman, but that his defense of Keynesians against Lucas ignores that there were problems with the Keynesian forecasting record during the Volcker disinflation.

My complaint is not that Krugman was confusing Friedman and Lucas, but rather he was ignoring Friedman, when in fact, Friedman was still a highly influential figure, whose position was partly vindicated (monetary policy matters for inflation) and partly discredited (a good monetary policy is one that stabilizes the growth rate of the monetary aggregates at about 3% a year).

JP, Yes that is exactly the point, and you cite the classic historical example.

Benjamin and Frank, I think the criticism of Volcker intensified in the period after the recovery when they were upset that Volcker seemed to be leaning against the wind and dampening the boom. At least until the runup to the 1982 Congressional elections, I think that the Reagan administration was relatively supportive of Volcker and the Fed.

TravisV, Thanks for bringing this to my attention. Very interesting, perhaps I will write a post about it.

LikeLike

David,

“I think the question whether you say people will be put out of work if the Fed reduces inflation or that people must be put out of work for the inflation rate to be reduced is largely, if not entirely, a question of semantics.”

Establishing causality in economics (or any science) is a question of semantics? Does the Phillips curve show a causal relationship between inflation and employment or a casual relationship? If causal, which direction does causality run?

There are plenty of examples of highly correlated systems where no known causal relationship is known or believed to exist. Some humorous ones here:

http://www.fastcodesign.com/3030529/infographic-of-the-day/hilarious-graphs-prove-that-correlation-isnt-causation

LikeLike

Great post. The 1980s were not kind either to traditional Keynesianism or traditional monetarism, or the New Classicals!

I also think that talking about “Chicago” as if it was as uniform a school of thought as, say, Cambridge in the 1970s is very misleading.

LikeLike

Incidentally, the only occasion I can recall when Friedman mentioned Ayn Rand was on a talk from the 1990s on Youtube in which he talked about libertarianism and tolerance, and used Ayn Rand and Von Mises as examples of people who were very tolerant in the abstract but could be very intolerant of disagreement in person.

LikeLike

Well done, excellent blog on why the monetarists were wrong about Volcker’s Disinflation. I will try and post an abbreviated version of this at TheMoneyIllusion, where the kids are brainwashed into believing otherwise.

LikeLike

http://www.wsj.com/articles/the-fed-cash-machine-1421018574

Dying to see a David Glasner take on above post.

Re Volcker and the Reaganauts,

Here the Reaganauts call for looser money in 1981:

And here Don Regan suggest the Fed be put into the Treasury Department:

http://news.google.com/newspapers?nid=1499&dat=19841213&id=HsIdAAAAIBAJ&sjid=HSoEAAAAIBAJ&pg=6649,3052061

Speaking before the National Association of Realtors in December 1984, President Reagan echoed the Regan assault on the Fed. “Let me assure you we are not pleased with the recent increases in interest rates,” said President Reagan. “And frankly there is no satisfactory reason for them.”

The Reaganauts, like the Nixonians, were not obsessed with minute rates of inflation. Anything below 5% was good enough (and indeed that’s all Volcker did).

Nixon also pressured Burns to ease up, and sought FOMC board members who would print money.

A fascinating turn of events awaits us after the 2016 elections, if they provide of GOP sweep.

Already I see clues that the “deficits don’t matter” mantra is being dusted off, under new names such as “the primary deficit” (forget about debt payments)

The real fun could be what the GOP does re Fed policy. The tight-money crowd would suffocate America. But surely there are some GOP’ers who put practical considerations before ideology. I expect some fig leaf to be generated that will allow the GOP to embrace a looser monetary policy.

I cannot imagine the GOP getting into 2018, and not saying “crank up the presses dudes, there is an election coming on.”

LikeLike

Ben,

I read through the newspaper article and this snippet caught my attention:

Don Regan:

“We are the only large industrial nation that has an independent central bank, Regan said, adding that the Fed’s independence has hampered the decision making ability of every president”

Total B. S.

Congress sets the level of spending.

Congress sets the level of taxation.

Treasury Department makes up the difference when spending exceeds taxes.

Monetary policy only comes into play when government borrows to fund the deficit.

If Reagan / Regan had a problem with either the level of taxation or the level of spending, that was an issue to resolve with Congress (not the Fed).

For a guy who worked at one of the premier investment banks in the U. S., Regan did not understand capitalism very well.

LikeLike

Sorry to all for these late responses, but I was distracted by life and by my post on the 1920-21 depression

Frank, you said:

“Establishing causality in economics (or any science) is a question of semantics? Does the Phillips curve show a causal relationship between inflation and employment or a casual relationship? If causal, which direction does causality run?”

I think that unidirectional causality in complex models (i.e., models in which many variables are simultaneously determined) is a special case. In general, you can’t say which way the causality runs, because it runs in both directions.

W., Even Cambridge in the 1970s was not homogeneous. Frank Hahn, a neoclassical, was not beloved of Joan Robinson and her followers. Chicago certainly had its factions as well. Harry Johnson was writing stinging attacks on Friedman in the 1970s while he was at Chicago (one semester a year).

About Friedman, he was not exactly tolerant of deviations from Monetarist orthodoxy, as Fischer Black found out during his brief sojourn at Chicago.

Ray, Thanks. What exactly is the point that you think is inconsistent with Money Illusion dogma?

Benjamin, Thanks for the link. I thought about writing something about that when I saw it, but decided that it wasn’t worth the effort, and that was before I got distracted. Sorry to disappoint.

I think Krugman, who was on the CEA staff in Reagan’s first term, recently wrote about the attitude of the Reagan administration toward Volcker. He observes correctly that there were different factions in the administration, strict Monetarists, supply-siders, and another group which I can’t remember as I write this. Regan was obviously not part of the Monetarist camp, but you can’t necessarily assume that Regan was speaking on behalf of Reagan, because there were others in the administration who were also trying to influence him in the opposite direction.

Frank, As long as there is an outstanding national debt, the Fed can conduct monetary policy via open market operations even if the government is not currently borrowing. The Fed can also conduct monetary policy via foreign exchange operations.

LikeLike

David,

I was addressing Regan’s statement that Fed independence hampers fiscal policy – it does not in the sense that fiscal policy is cumulative action by both the Executive and Legislative branches of government. Perhaps Regan was looking for a scapegoat rather than admitting difficulty in working with the Democratic legislature or with other factions within the administration.

“As long as there is an outstanding national debt, the Fed can conduct monetary policy via open market operations even if the government is not currently borrowing. The Fed can also conduct monetary policy via foreign exchange operations.”

You are addressing whether Fed policy can be hampered by fiscal policy (absence / existence of government debt). I was addressing whether fiscal policy has been “hampered by the Fed for every President” as Regan so proclaimed. My point was that current fiscal policy is only hampered by monetary policy if the federal government decides to borrow to fund current deficits.

And really, the central bank does not even need foreign exchange operations to conduct monetary policy – they can lend at an interest rate that they set.

LikeLike