Earlier in the week, Paul Krugman wrote about the Volcker disinflation of the 1980s. Krugman’s annoyance at Stephen Moore (whom Krugman flatters by calling him an economist) and John Cochrane (whom Krugman disflatters by comparing him to Stephen Moore) is understandable, but he has less excuse for letting himself get carried away in an outburst of Keynesian triumphalism.

Right-wing economists like Stephen Moore and John Cochrane — it’s becoming ever harder to tell the difference — have some curious beliefs about history. One of those beliefs is that the experience of disinflation in the 1980s was a huge shock to Keynesians, refuting everything they believed. What makes this belief curious is that it’s the exact opposite of the truth. Keynesians came into the Volcker disinflation — yes, it was mainly the Fed’s doing, not Reagan’s — with a standard, indeed textbook, model of what should happen. And events matched their expectations almost precisely.

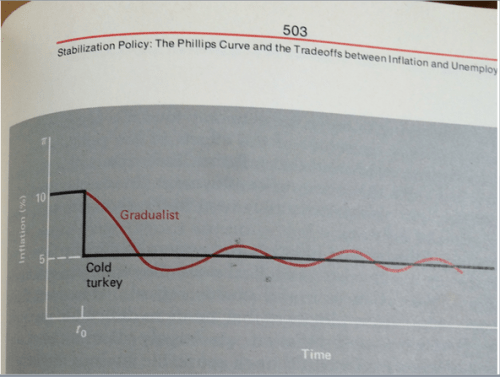

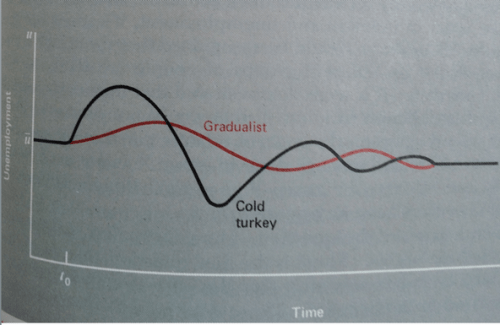

I’ve been cleaning out my library, and just unearthed my copy of Dornbusch and Fischer’s Macroeconomics, first edition, copyright 1978. Quite a lot of that book was concerned with inflation and disinflation, using an adaptive-expectations Phillips curve — that is, an assumed relationship in which the current inflation rate depends on the unemployment rate and on lagged inflation. Using that approach, they laid out at some length various scenarios for a strategy of reducing the rate of money growth, and hence eventually reducing inflation. Here’s one of their charts, with the top half showing inflation and the bottom half showing unemployment:

Not the cleanest dynamics in the world, but the basic point should be clear: cutting inflation would require a temporary surge in unemployment. Eventually, however, unemployment could come back down to more or less its original level; this temporary surge in unemployment would deliver a permanent reduction in the inflation rate, because it would change expectations.

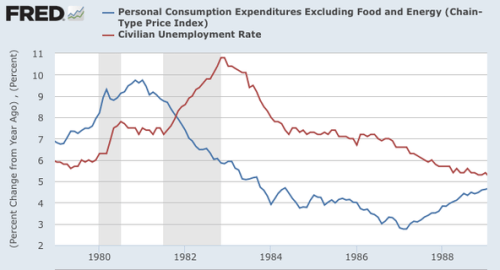

And here’s what the Volcker disinflation actually looked like:

A temporary but huge surge in unemployment, with inflation coming down to a sustained lower level.

So were Keynesian economists feeling amazed and dismayed by the events of the 1980s? On the contrary, they were feeling pretty smug: disinflation had played out exactly the way the models in their textbooks said it should.

Well, this is true, but only up to a point. What Krugman neglects to mention, which is why the Volcker disinflation is not widely viewed as having enhanced the Keynesian forecasting record, is that most Keynesians had opposed the Reagan tax cuts, and one of their main arguments was that the tax cuts would be inflationary. However, in the Reagan-Volcker combination of loose fiscal policy and tight money, it was tight money that dominated. Score one for the Monetarists. The rapid drop in inflation, though accompanied by high unemployment, was viewed as a vindication of the Monetarist view that inflation is always and everywhere a monetary phenomenon, a view which now seems pretty commonplace, but in the 1970s and 1980s was hotly contested, including by Keynesians.

However, the (Friedmanian) Monetarist view was only partially vindicated, because the Volcker disinflation was achieved by way of high interest rates not by tightly controlling the money supply. As I have written before on this blog (here and here) and in chapter 10 of my book on free banking (especially, pp. 214-21), Volcker actually tried very hard to slow down the rate of growth in the money supply, but the attempt to implement a k-percent rule induced perverse dynamics, creating a precautionary demand for money whenever monetary growth overshot the target range, the anticipation of an imminent future tightening causing people, fearful that cash would soon be unavailable, to hoard cash by liquidating assets before the tightening. The scenario played itself out repeatedly in the 1981-82 period, when the most closely watched economic or financial statistic in the world was the Fed’s weekly report of growth in the money supply, with growth rates over the target range being associated with falling stock and commodities prices. Finally, in the summer of 1982, Volcker announced that the Fed would stop trying to achieve its money growth targets, and the great stock market rally of the 1980s took off, and economic recovery quickly followed.

So neither the old-line Keynesian dismissal of monetary policy as irrelevant to the control of inflation, nor the Monetarist obsession with controlling the monetary aggregates fared very well in the aftermath of the Volcker disinflation. The result was the New Keynesian focus on monetary policy as the key tool for macroeconomic stabilization, except that monetary policy no longer meant controlling a targeted monetary aggregate, but controlling a targeted interest rate (as in the Taylor rule).

But Krugman doesn’t mention any of this, focusing instead on the conflicts among non-Keynesians.

Indeed, it was the other side of the macro divide that was left scrambling for answers. The models Chicago was promoting in the 1970s, based on the work of Robert Lucas and company, said that unemployment should have come down quickly, as soon as people realized that the Fed really was bringing down inflation.

Lucas came to Chicago in 1975, and he was the wave of the future at Chicago, but it’s not as if Friedman disappeared; after all, he did win the Nobel Prize in 1976. And although Friedman did not explicitly attack Lucas, it’s clear that, to his credit, Friedman never bought into the rational-expectations revolution. So although Friedman may have been surprised at the depth of the 1981-82 recession – in part attributable to the perverse effects of the money-supply targeting he had convinced the Fed to adopt – the adaptive-expectations model in the Dornbusch-Fischer macro textbook is as much Friedmanian as Keynesian. And by the way, Dornbush and Fischer were both at Chicago in the mid 1970s when the first edition of their macro text was written.

By a few years into the 80s it was obvious that those models were unsustainable in the face of the data. But rather than admit that their dismissal of Keynes was premature, most of those guys went into real business cycle theory — basically, denying that the Fed had anything to do with recessions. And from there they just kept digging ever deeper into the rabbit hole.

But anyway, what you need to know is that the 80s were actually a decade of Keynesian analysis triumphant.

I am just as appalled as Krugman by the real-business-cycle episode, but it was as much a rejection of Friedman, and of all other non-Keynesian monetary theory, as of Keynes. So the inspiring morality tale spun by Krugman in which the hardy band of true-blue Keynesians prevail against those nasty new classical barbarians is a bit overdone and vastly oversimplified.