I want to begin this post by saying that I’m flattered by, and grateful to, Frances Coppola for the first line of her blog post yesterday. But – and I note that imitation is the sincerest form of flattery – I fear I have to take issue with her over competitive devaluation.

Frances quotes at length from a quotation from Hawtrey’s Trade Depression and the Way Out that I used in a post I wrote almost four years ago. Hawtrey explained why competitive devaluation in the 1930s was – and in my view still is – not a problem (except under extreme assumptions, which I will discuss at the end of this post). Indeed, I called competitive devaluation a free lunch, providing her with a title for her post. Here’s the passage that Frances quotes:

This competitive depreciation is an entirely imaginary danger. The benefit that a country derives from the depreciation of its currency is in the rise of its price level relative to its wage level, and does not depend on its competitive advantage. If other countries depreciate their currencies, its competitive advantage is destroyed, but the advantage of the price level remains both to it and to them. They in turn may carry the depreciation further, and gain a competitive advantage. But this race in depreciation reaches a natural limit when the fall in wages and in the prices of manufactured goods in terms of gold has gone so far in all the countries concerned as to regain the normal relation with the prices of primary products. When that occurs, the depression is over, and industry is everywhere remunerative and fully employed. Any countries that lag behind in the race will suffer from unemployment in their manufacturing industry. But the remedy lies in their own hands; all they have to do is to depreciate their currencies to the extent necessary to make the price level remunerative to their industry. Their tardiness does not benefit their competitors, once these latter are employed up to capacity. Indeed, if the countries that hang back are an important part of the world’s economic system, the result must be to leave the disparity of price levels partly uncorrected, with undesirable consequences to everybody. . . .

The picture of an endless competition in currency depreciation is completely misleading. The race of depreciation is towards a definite goal; it is a competitive return to equilibrium. The situation is like that of a fishing fleet threatened with a storm; no harm is done if their return to a harbor of refuge is “competitive.” Let them race; the sooner they get there the better. (pp. 154-57)

Here’s Frances’s take on Hawtrey and me:

The highlight “in terms of gold” is mine, because it is the key to why Glasner is wrong. Hawtrey was right in his time, but his thinking does not apply now. We do not value today’s currencies in terms of gold. We value them in terms of each other. And in such a system, competitive devaluation is by definition beggar-my-neighbour.

Let me explain. Hawtrey defines currency values in relation to gold, and advertises the benefit of devaluing in relation to gold. The fact that gold is the standard means there is no direct relationship between my currency and yours. I may devalue my currency relative to gold, but you do not have to: my currency will be worth less compared to yours, but if the medium of account is gold, this does not matter since yours will still be worth the same amount in terms of gold. Assuming that the world price of gold remains stable, devaluation therefore principally affects the DOMESTIC price level. As Hawtrey says, there may additionally be some external competitive advantage, but this is not the principal effect and it does not really matter if other countries also devalue. It is adjusting the relationship of domestic wages and prices in terms of gold that matters, since this eventually forces down the price of finished goods and therefore supports domestic demand.

Conversely, in a floating fiat currency system such as we have now, if I devalue my currency relative to yours, your currency rises relative to mine. There may be a domestic inflationary effect due to import price rises, but we do not value domestic wages or the prices of finished goods in terms of other currencies, so there can be no relative adjustment of wages to prices such as Hawtrey envisages. Devaluing the currency DOES NOT support domestic demand in a floating fiat currency system. It only rebalances the external position by making imports relatively more expensive and exports relatively cheaper.

This difference is crucial. In a gold standard system, devaluing the currency is a monetary adjustment to support domestic demand. In a floating fiat currency system, itis an external adjustment to improve competitiveness relative to other countries.

Actually, Frances did not quote the entire passage from Hawtrey that I reproduced in my post, and Frances would have done well to quote from, and to think carefully about, what Hawtrey said in the paragraphs preceding the ones she quoted. Here they are:

When Great Britain left the gold standard, deflationary measure were everywhere resorted to. Not only did the Bank of England raise its rate, but the tremendous withdrawals of gold from the United States involved an increase of rediscounts and a rise of rates there, and the gold that reached Europe was immobilized or hoarded. . . .

The consequence was that the fall in the price level continued. The British price level rose in the first few weeks after the suspension of the gold standard, but then accompanied the gold price level in its downward trend. This fall of prices calls for no other explanation than the deflationary measures which had been imposed. Indeed what does demand explanation is the moderation of the fall, which was on the whole not so steep after September 1931 as before.

Yet when the commercial and financial world saw that gold prices were falling rather than sterling prices rising, they evolved the purely empirical conclusion that a depreciation of the pound had no effect in raising the price level, but that it caused the price level in terms of gold and of those currencies in relation to which the pound depreciated to fall.

For any such conclusion there was no foundation. Whenever the gold price level tended to fall, the tendency would make itself felt in a fall in the pound concurrently with the fall in commodities. But it would be quite unwarrantable to infer that the fall in the pound was the cause of the fall in commodities.

On the other hand, there is no doubt that the depreciation of any currency, by reducing the cost of manufacture in the country concerned in terms of gold, tends to lower the gold prices of manufactured goods. . . .

But that is quite a different thing from lowering the price level. For the fall in manufacturing costs results in a greater demand for manufactured goods, and therefore the derivative demand for primary products is increased. While the prices of finished goods fall, the prices of primary products rise. Whether the price level as a whole would rise or fall it is not possible to say a priori, but the tendency is toward correcting the disparity between the price levels of finished products and primary products. That is a step towards equilibrium. And there is on the whole an increase of productive activity. The competition of the country which depreciates its currency will result in some reduction of output from the manufacturing industry of other countries. But this reduction will be less than the increase in the country’s output, for if there were no net increase in the world’s output there would be no fall of prices.

So Hawtrey was refuting precisely the argument raised by Frances. Because the value of gold was not stable after Britain left the gold standard and depreciated its currency, the deflationary effect in other countries was mistakenly attributed to the British depreciation. But Hawtrey points out that this reasoning was backwards. The fall in prices in the rest of the world was caused by deflationary measures that were increasing the demand for gold and causing prices in terms of gold to continue to fall, as they had been since 1929. It was the fall in prices in terms of gold that was causing the pound to depreciate, not the other way around

Frances identifies an important difference between an international system of fiat currencies in which currency values are determined in relationship to each other in foreign exchange markets and a gold standard in which currency values are determined relative to gold. However, she seems to be suggesting that currency values in a fiat money system affect only the prices of imports and exports. But that can’t be so, because if the prices of imports and exports are affected, then the prices of the goods that compete with imports and exports must also be affected. And if the prices of tradable goods are affected, then the prices of non-tradables will also — though probably with a lag — eventually be affected as well. Of course, insofar as relative prices before the change in currency values were not in equilibrium, one can’t predict that all prices will adjust proportionately after the change.

To make the point in more abstract terms, the principle of purchasing power parity (PPP) operates under both a gold standard and a fiat money standard, and one can’t just assume that the gold standard has some special property that allows PPP to hold, while PPP is somehow disabled under a fiat currency system. Absent an explanation of why PPP doesn’t hold in a floating fiat currency system, the assertion that devaluing a currency (i.e., driving down the exchange value of one currency relative to other currencies) “is an external adjustment to improve competitiveness relative to other countries” is baseless.

I would also add a semantic point about this part of Frances’s argument:

We do not value today’s currencies in terms of gold. We value them in terms of each other. And in such a system, competitive devaluation is by definition beggar-my-neighbour.

Unfortunately, Frances falls into the common trap of believing that a definition actually tell us something about the real word, when in fact a definition tell us no more than what meaning is supposed to be attached to a word. The real world is invariant with respect to our definitions; our definitions convey no information about reality. So for Frances to say – apparently with the feeling that she is thereby proving her point – that competitive devaluation is by definition beggar-my-neighbour is completely uninformative about happens in the world; she is merely informing us about how she chooses to define the words she is using.

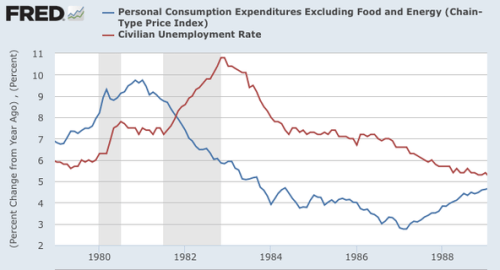

Frances goes on to refer to this graph taken from Gavyn Davies in the Financial Times, concerning a speech made by Stanley Fischer about research done by Fed staff economists showing that the 20% appreciation in the dollar over the past 18 months has reduced the rate of US inflation by as much as 1% and is projected to cause US GDP in three years to be about 3% lower than it would have been without dollar appreciation.

Frances focuses on these two comments by Gavyn. First:

Importantly, the impact of the higher exchange rate does not reverse itself, at least in the time horizon of this simulation – it is a permanent hit to the level of GDP, assuming that monetary policy is not eased in the meantime.

And then:

According to the model, the annual growth rate should have dropped by about 0.5-1.0 per cent by now, and this effect should increase somewhat further by the end of this year.

Then, Frances continues:

But of course this assumes that the US does not ease monetary policy further. Suppose that it does?

The hit to net exports shown on the above graph is caused by imports becoming relatively cheaper and exports relatively more expensive as other countries devalue. If the US eased monetary policy in order to devalue the dollar support nominal GDP, the relative prices of imports and exports would rebalance – to the detriment of those countries attempting to export to the US.

What Frances overlooks is that by easing monetary policy to support nominal GDP, the US, aside from moderating or reversing the increase in its real exchange rate, would have raised total US aggregate demand, causing US income and employment to increase as well. Increased US income and employment would have increased US demand for imports (and for the products of American exporters), thereby reducing US net exports and increasing aggregate demand in the rest of the world. That was Hawtrey’s argument why competitive devaluation causes an increase in total world demand. Francis continues with a description of the predicament of the countries affected by US currency devaluation:

They have three choices: they respond with further devaluation of their own currencies to support exports, they impose import tariffs to support their own balance of trade, or they accept the deflationary shock themselves. The first is the feared “competitive devaluation” – exporting deflation to other countries through manipulation of the currency; the second, if widely practised, results in a general contraction of global trade, to everyone’s detriment; and you would think that no government would willingly accept the third.

But, as Hawtrey showed, competitive devaluation is not a problem. Depreciating your currency cushions the fall in nominal income and aggregate demand. If aggregate demand is kept stable, then the increased output, income, and employment associated with a falling exchange rate will spill over into a demand for the exports of other countries and an increase in the home demand for exportable home products. So it’s a win-win situation.

However, the Fed has permitted passive monetary tightening over the last eighteen months, and in December 2015 embarked on active monetary tightening in the form of interest rate rises. Davies questions the rationale for this, given the extraordinary rise in the dollar REER and the growing evidence that the US economy is weakening. I share his concern.

And I share his concern, too. So what are we even arguing about? Equally troubling is how passive tightening has reduced US demand for imports and for US exportable products, so passive tightening has negative indirect effects on aggregate demand in the rest of the world.

Although currency depreciation generally tends to increase the home demand for imports and for exportables, there are in fact conditions when the general rule that competitive devaluation is expansionary for all countries may be violated. In a number of previous posts (e.g., this, this, this, this and this) about currency manipulation, I have explained that when currency depreciation is undertaken along with a contractionary monetary policy, the terms-of-trade effect predominates without any countervailing effect on aggregate demand. If a country depreciates its exchange rate by intervening in foreign-exchange markets, buying foreign currencies with its own currency, thereby raising the value of foreign currencies relative to its own currency, it is also increasing the quantity of the domestic currency in the hands of the public. Increasing the quantity of domestic currency tends to raise domestic prices, thereby reversing, though probably with a lag, the effect on the currency’s real exchange rate. To prevent the real-exchange rate from returning to its previous level, the monetary authority must sterilize the issue of domestic currency with which it purchased foreign currencies. This can be done by open-market sales of assets by the cental bank, or by imposing increased reserve requirements on banks, thereby forcing banks to hold the new currency that had been created to depreciate the home currency.

This sort of currency manipulation, or exchange-rate protection, as Max Corden referred to it in his classic paper (reprinted here), is very different from conventional currency depreciation brought about by monetary expansion. The combination of currency depreciation and tight money creates an ongoing shortage of cash, so that the desired additional cash balances can be obtained only by way of reduced expenditures and a consequent export surplus. Since World War II, Japan, Germany, Taiwan, South Korea, and China are among the countries that have used currency undervaluation and tight money as a mechanism for exchange-rate protectionism in promoting industrialization. But exchange rate protection is possible not only under a fiat currency system. Currency manipulation was also possible under the gold standard, as happened when the France restored the gold standard in 1928, and pegged the franc to the dollar at a lower exchange rate than the franc had reached prior to the restoration of convertibility. That depreciation was accompanied by increased reserve requirements on French banknotes, providing the Bank of France with a continuing inflow of foreign exchange reserves with which it was able to pursue its insane policy of accumulating gold, thereby precipitating, with a major assist from the high-interest rate policy of the Fed, the deflation that turned into the Great Depression.