Sometimes you get into a Twitter argument when you least expect to. It was after 11pm two Saturday nights ago when I saw this tweet by Gabriel Mathy (@gabriel_mathy)

Friedman says if there had been no Fed, there would have been no Depression. That’s certainly wrong, even if your position is that the Fed did little to nothing to mitigate the Depression (which is reasonable IMO)

Chiming in, I thought to reinforce Mathy’s criticism of Friedman, I tweeted the following:

Friedman totally misunderstood the dynamics of the Great Depression, which was driven by increasing demand for gold after 1928, in particular by the Bank of France and by the Fed. He had no way of knowing what the US demand for gold would have been if there had not been a Fed

I got a response from Mathy that I really wasn’t expecting who tweeted with seeming annoyance

There already isn’t enough gold to back the gold standard by the end of World War I, it’s just a matter of time until a negative shock large enough sent the world into a downward spiral (my emphasis). Just took a few years after resumption of the gold standard in most countries in the mid-20s. (my emphasis)

I didn’t know exactly what to make of Mathy’s assertion that there wasn’t enough gold by the end of World War I. The gold standard was effectively abandoned at the outset of WWI and the US price level was nearly double the prewar US price level after the postwar inflation of 1919. Even after the deflation of 1920-21, US prices were still much higher in 1922 than they were in 1914. Gold production fell during World War I, but gold coins had been withdrawn from circulation and replaced with paper or token coins. The idea that there is a fixed relationship between the amount of gold and the amount of money, especially after gold coinage had been eliminated, has no theoretical basis.

So I tweeted back:

The US holdings of gold after WWI were so great that Keynes in his Tract on Monetary Reform [argued] that the great danger of a postwar gold standard was inflation because the US would certainly convert its useless holding of gold for something more useful

To which Mathy responded

The USA is not the only country though. The UK had to implement tight monetary policies to back the gold standard, and eventually had to leave the gold standard. As did the USA in 1931. The Great Depression is a global crisis.

Mathy’s response, I’m afraid, is completely wrong. Of course, the Great Depression is a global crisis. It was a global crisis, because, under the (newly restored) gold standard, the price level in gold-standard countries was determined internationally. And, holding 40% of the world’s monetary reserves of gold at the end of World War I, the US, the largest and most dynamic economy in the world, was clearly able to control, as Keynes understood, the common international price level for gold-standard countries.

The tight monetary policy imposed on the UK resulted from its decision to rejoin the gold standard at the prewar dollar parity. Had the US followed a modestly inflationary monetary policy, allowing an outflow of gold during the 1920s rather than inducing an inflow, deflation would not have been imposed on the UK.

But instead of that response, I replied as follows:

The US didn’t leave till 1933 when FDR devalued. I agree that individual countries, worried about losing gold, protected their reserves by raising interest rates. Had they all reduced rates together, the conflict between individual incentives and common interest could have been avoided.

Mathy then kept the focus on the chronology of the Great Depression, clarifying that he meant that in 1931 the US, like the UK, tightened monetary policy to remain on the gold standard, not that the US, like the UK, also left the gold standard in 1931:

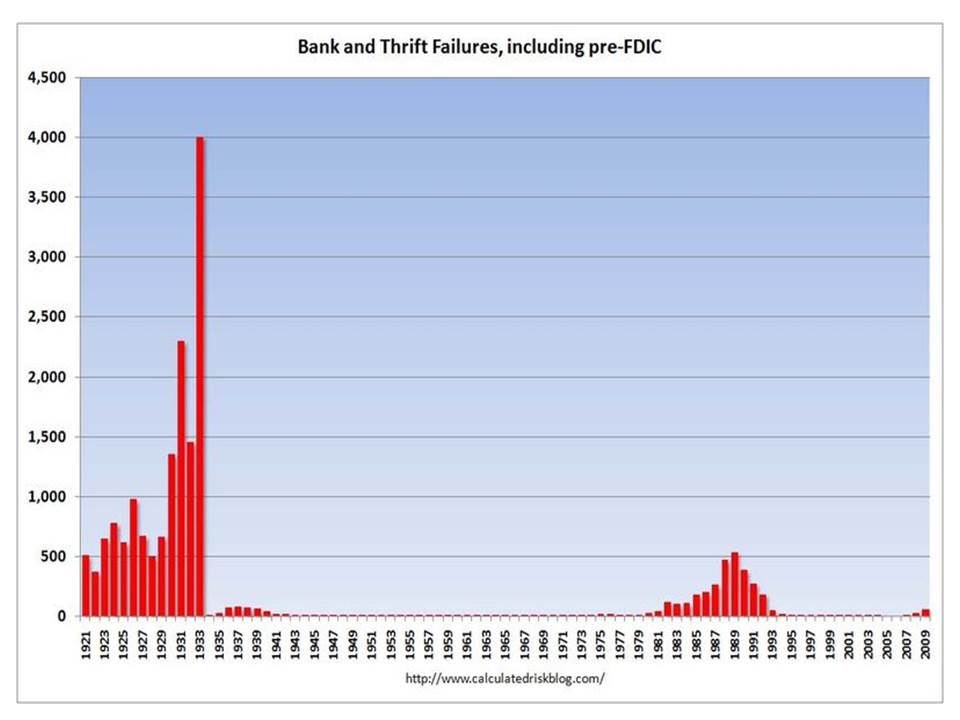

The USA tightens in 1931 to stay on the gold standard. And this sets off a wave of bank failures.

Fair enough, but once the situation deteriorated after the crash and the onset of deflation, the dynamics of the financial crisis made managing the gold standard increasingly difficult, given the increasingly pessimistic expectations conditioned by deepening economic contraction and deflation. While an easier US monetary policy in the late 1920s might have avoided the catastrophe and preserved the gold standard, an easier monetary policy may, at some point, have become inconsistent with staying on the gold standard.

So my response to Mathy was more categorical than was warranted.

Again, the US did not have to tighten in 1931 to stay on the gold standard. I agree that the authorities might have sincerely thought that they needed to tighten to stay on the gold standard, but they were wrong if that’s what they thought.

Mathy was having none of it, unleashing a serious snark attack

You know better I guess, despite collapsing free gold amidst a massive speculative attack

What I ought to have said is that the gold standard was not worth saving if doing so entailed continuing deflation. If I understand him, Mathy believes that deflation after World War I was inevitable and unavoidable, because there wasn’t enough gold to sustain the gold standard after World War I. I was arguing that if there was a shortage of gold, it was because of the policies followed, often in compliance with legal gold-cover requirements, that central banks, especially the Bank of France, which started accumulating gold rapidly in 1928, and the Fed, which raised interest rates to burst a supposed stock-market bubble, were following. But as I point out below, the gold accumulation by the Bank of France far exceeded what was mandated by legal gold-cover requirements.

My point is that the gold shortage that Mathy believes doomed the gold standard was not preordained; it could have been mitigated by policies to reduce, or reverse, gold accumulation. France could have rejoined the gold standard without accumulating enormous quantities of gold in 1928-29, and the Fed did not have to raise interest rates in 1928-29, attracting additional gold to its own already massive holdings just as France was rapidly accumulating gold.

When France formally rejoined the gold standard in July 1928, the gold reserves of the Bank of France were approximately equal to its foreign-exchange holdings and its gold-reserve ratio was 39.5% slightly above the newly established legal required ratio of 35%. In subsequent years, the gold reserves of the Bank of France steadily increased while foreign exchange reserves declined. At the close of 1929, the gold-reserve ratio of the Bank of France stood at 47.3%, while its holdings of foreign exchange hardly changed. French gold holdings increased in 1930 by slightly more than in 1929, with foreign-exchange holdings almost constant; the French gold-reserve ratio at the end of 1930 was 53.2%. The 1931 increase in French gold reserves, owing to a 20% drop in foreign-exchange holdings, was even larger than in 1930, raising the gold-reserve ratio to 60.5% at the end of 1931.

Once deflation and the Great Depression started late in 1929, deteriorating rapidly in 1930, salvaging the gold standard became increasingly unlikely, with speculators becoming increasingly alert to the possibility of currency devaluation or convertibility suspension. Speculation against a pegged exchange rate is not always a good bet, but it’s rarely a bad one, any change in the pegged rate being almost surely in the direction that speculators are betting on.

But, it was still at least possible that, if gold-cover requirements for outstanding banknotes and bank reserves were relaxed or suspended, central banks could have caused a gold outflow sufficient to counter the deflationary expectations then feeding speculative demands for gold. Gold does not have many non-monetary uses, so a significant release of gold from idle central-bank reserves might have caused gold to depreciate relative to other real assets, thereby slowing, or even reversing, deflation.

Of course, deflation would not have stopped unless the deflationary expectations fueling speculative demands for gold were reversed. Different expectational responses would have led to different outcomes. More often than not, inflationary and deflationary expectations are self-fulfilling. Because expectations tend to be mutually interdependent – my inflationary expectations reinforce your inflationary expectations and vice versa — the notion of rational expectation in this context borders on the nonsensical, making outcomes inherently unpredictable. Reversing inflationary or deflationary expectations requires policy credibility and a willingness by policy makers to take policy actions – even or especially painful ones — that demonstrate their resolve.

In 1930 Ralph Hawtrey testified to the Macmillan Committee on Finance and Industry, he recommended that the Bank of England reduce interest rates to counter the unemployment and deflation. That testimony elicited the following exchange between Hugh Pattison Macmillan, the chairman of the Committee and Hawtrey:

MACMILLAN: Suppose . . . without restricting credit . . . that gold had gone out to a very considerable extent, would that not have had very serious consequences on the international position of London?

HAWTREY: I do not think the credit of London depends on any particular figure of gold holding. . . . The harm began to be done in March and April of 1925 [when] the fall in American prices started. There was no reason why the Bank of England should have taken any action at that time so far as the question of loss of gold is concerned. . . . I believed at the time and I still think that the right treatment would have been to restore the gold standard de facto before it was restored de jure. That is what all the other countries have done. . . . I would have suggested that we should have adopted the practice of always selling gold to a sufficient extent to prevent the exchange depreciating. There would have been no legal obligation to continue convertibility into gold . . . If that course had been adopted, the Bank of England would never have been anxious about the gold holding, they would have been able to see it ebb away to quite a considerable extent with perfect equanimity, . . and might have continued with a 4 percent Bank Rate.

MACMILLAN: . . . the course you suggest would not have been consistent with what one may call orthodox Central Banking, would it?

HAWTREY: I do not know what orthodox Central Banking is.

MACMILLAN: . . . when gold ebbs away you must restrict credit as a general principle?

HAWTREY: . . . that kind of orthodoxy is like conventions at bridge; you have to break them when the circumstances call for it. I think that a gold reserve exists to be used. . . . Perhaps once in a century the time comes when you can use your gold reserve for the governing purpose, provided you have the courage to use practically all of it.

Hawtrey’s argument lay behind this response of mine to Mathy:

What else is a gold reserve is for? That’s like saying you can’t fight a fire because you’ll drain the water tank. But I agree that by 1931 there was no point in defending the gold standard and the US should have made clear the goal was reflation to the 1926 price level as FDR did in 1933.

Mathy responded:

If the Fed cuts discount rates to 0%, capital outflow will eventually exhaust gold reserves. So do you recommend a massive OMO in 1929? What specifically is the plan?

In 1927, the Fed reduced its discount rate to 3.5%; in February 1928, it was raised the rate to 4%. The rate was raised again in August 1928 and to 6% in September 1929. The only reason the Fed raised interest rates in 1928 was a misguided concern with rising stock prices. A zero interest rate was hardly necessary in 1929, nor were massive open-market operations. Had the Fed kept its interest rate at 4%, and the Bank of France not accumulated gold rapidly in 1928-29, the history of the world might well have followed a course much different from the one actually followed.

In another exchange, Mathy pointed to the 1920s adoption of the gold-exchange standard rather than a (supposedly) orthodox version of the gold standard as evidence that there wasn’t enough gold to support the gold standard after World War I. (See my post on the difference between the gold standard and the gold-exchange standard.)

Mathy: You seem to be implying there was plentiful free gold [i.e., gold held by central banks in excess of the amount required by legal gold-cover requirements] in the world after WW1 so that gold was not a constraint. How much free gold to you reckon there was?

Glasner: All of it was free. Legal reserve requirements soaked up much but nearly all the free gold

Mathy: All of it was not free, and countries suffered speculative attacks before their real or perceived minimum backings of gold were reached

Glasner: All of it would have been free but for the legal reserve requirements. Of course countries were subject to speculative attacks, when the only way for a country to avoid deflation was to leave the gold standard.

Mathy: You keep asserting an abundance of free gold, so let’s see some numbers. The lack of free gold led to the gold exchange standard where countries would back currencies with other currencies (themselves only partially backed by gold) because there wasn’t enough gold.

Glasner: The gold exchange standard was a rational response to the WWI inflation and post WWI deflation and it could have worked well if it had not been undermined by the Bank of France and gold accumulation by the US after 1928.

Mathy: Both you and [Douglas] Irwin assume that the gold inflows into France are the result of French policy. But moving your gold to France, a country committed to the gold standard, is exactly what a speculative attack on another currency at risk of leaving the gold standard looks like.

Mathy: What specific policies did the Bank if France implement in 1928 that caused gold inflows? We can just reason from accounting identities, assuming that international flows to France are about pull factors from France rather than push factors from abroad.

Mathy: So lay out your counterfactual- how much gold should the US and France have let go abroad, and how does this prevent the Depression?

Glasner: The increase in gold monetary holdings corresponds to a higher real value of gold. Under the gold standard that translates into [de]flation. Alternatively, to prevent gold outflows central banks raised rates which slowed economic activity and led to deflation.

Mathy: So give me some numbers. What does the Fed do specifically in 1928 and what does France do specifically in 1928 that avoid the debacle of 1929. You can take your time, pick this up Monday.

Mathy: The UK was suffering from high unemployment before 1928 because there wasn’t enough gold in the system. The Bank of England had been able to draw gold “from the moon” with a higher bank rate. After WW1, this was no longer possible.

Glasner: Unemployment in the UK steadily fell after 1922 and continued falling till ’29. With a fixed exchange rate against the $, and productivity in the US rising faster than in the UK, the UK needed more US inflation than it got to reach full employment. That has nothing to do with what happened after 1929.

Mathy: UK unemployment rises 1925-1926 actually, that’s incorrect and it’s near double digits throughout the 1920s. That’s not good at all and the problems start long before 1928.

There’s a lot to unpack here, and I will try to at least touch on the main points. Mathy questions whether there was enough free gold available in the 1920s, while also acknowledging that the gold-exchange standard was instituted in the 1920s precisely to avoid the demands on monetary gold reserves that would result from restoring gold coinage and imposing legal gold-cover requirements on central-bank liabilities. So, if free-gold reserves were insufficient before the Great Depression, it was because of the countries that restored the gold standard and also imposed legal gold-cover requirements, notably the French Monetary Law enacted in June 1928 that imposed a minimum 35% gold-cover requirement when convertibility of the franc was restored.

It’s true that there were speculative movements of gold into France when there were fears that countries might devalue their currencies or suspend gold convertibility, but those speculative movements did not begin until late 1930 or 1931.

Two aspects of the French restoration of gold convertibility should be mentioned. First, France pegged the dollar/franc exchange rate at $0.0392, with the intention of inducing a current-account surplus and a gold inflow. Normally that inflow would have been transitory as French prices and wages rose to the world level. But the French Monetary Law allowed the creation of new central-bank liabilities only in exchange for gold or foreign exchange convertible into gold. So French demand for additional cash balances could be satisfied only insofar as total spending in France was restricted sufficiently to ensure an inflow of gold or convertible foreign exchange. Hawtrey explained this brilliantly in Chapter two of The Art of Central Banking.

Mathy suggests that the gold-standard was adopted by countries without enough gold to operate a true gold standard, which he thinks proves that there wasn’t enough free gold available. What resort to the gold-exchange standard shows is that countries without enough gold were able to join the gold standard without first incurring the substantial cost of accumulating (either by direct gold purchases or by inducing large amounts of gold inflows by raising domestic interest rates); it does not prove that the gold-exchange standard system was inherently unstable.

Why did some countries restoring the gold standard not have enough gold? First, much of the world’s stock of gold reserves had been shipped to the US during World War I when countries were importing food, supplies and war material from the US paid with gold, or, promising to repay after the war, on credit. Second, wartime and immediate postwar inflation required increased quantities of cash to conduct transactions and satisfy liquidity demands. Third, legislated gold-cover requirements in the US, and later in France and other countries rejoining the gold standard, obligated monetary authorities to accumulate gold.

Those gold-cover requirements, forcing countries to accumulate additional gold to satisfy any increased demand by the public for cash, were an ongoing, and unnecessary, cause of rising demand for gold reserves as countries rejoined the gold standard in the 1920s, imparting an inherent deflationary bias to the gold standard. The 1922 Genoa Accords attempted to cushion this deflationary bias by allowing countries to rejoin the gold standard without making their own currencies directly convertible into gold, but by committing themselves to a fixed exchange rate against those currencies – at first the dollar and subsequently pound sterling – that were directly convertible into gold. But the accords were purely advisory and provided no effective mechanism to prevent the feared increase in the monetary demand for gold. And the French never intended to rejoin the gold standard except by making the franc convertible directly into gold.

Mathy asks how much gold I think that the French and the US should have let go to avoid the Great Depression. This is an impossible question to answer, because French gold accumulation in 1928-29, combined with increased US interest rates in 1928-29, which caused a nearly equivalent gold inflow into the US, triggered deflation in the second half of 1929 that amplified deflationary expectations, causing a stock market crash, a financial crisis and ultimately the Great Depression. Once deflation got underway, the measures needed to calm the crisis and reverse the downturn became much more extreme than those that would have prevented the downturn in the first place.

Had the Fed kept its discount rate at 3.5 to 4 percent, had France not undervalued the franc in setting its gold peg, and had France created a mechanism for domestic credit expansion instead of making an increase in the quantity of francs impossible except through a current account surplus, and had the Bank of France been willing to accumulate foreign exchange instead of requiring its foreign-exchange holdings to be redeemed for gold, the crisis would not have occurred.

Here are some quick and dirty estimates of the effect of French policy on the availability of free gold. In July 1928 when France rejoined the gold standard and enacted the Monetary Law drafted by the Bank of France, the notes and demand deposits against which the Bank was required to gold reserves totaled almost ff76 billion (=$2.98 billion). French gold holdings in July 1928 were then just under ff30 billion (=$1.17 billion), implying a reserve ratio of 39.5%. (See the discussion above.)

By the end of 1931, the total of French banknotes and deposits against which the Bank of France was required to hold gold reserves was almost ff114 billion (=$4.46 billion). French gold holdings at the end of 1931 totaled ff68.9 billion (=$2.7 billion), implying a gold-reserve ratio of 60.5%. If the French had merely maintained the 40% gold-reserve ratio of 1928, their gold holdings in 1931 would have been approximately ff45 billion (=$1.7 billion).

Thus, from July 1929 to December 1931, France absorbed $1 billion of gold reserves that would have otherwise been available to other central banks or made available for use in non-monetary applications. The idea that free gold was a constraint on central bank policy is primarily associated with the period immediately before and after the British suspension of the gold standard in September 1931, which occasioned speculative movements of gold from the US to France to avoid a US suspension of the gold standard or a devaluation. From January 1931 through August 1931, the gold holdings of the Bank of France increased by just over ff3 billion (=$78 million). From August to December of 1931 French gold holdings increased by ff10.3 billion (=$404 million).

So, insofar as a lack of free gold was a constraint on US monetary expansion via open market purchases in 1931, which is the only time period when there is a colorable argument that free gold was a constraint on the Fed, it seems highly unlikely that that constraint would have been binding had the Bank of France not accumulated an additional $1 billion of gold reserves (over and above the increased reserves necessary to maintain the 40% gold-reserve ratio of July 1928) after rejoining the gold standard. Of course, the claim that free gold was a binding constraint on Fed policy in the second half of 1931 is far from universally accepted, and I consider the claim to be pretextual.

Finally, I concede that my assertion that unemployment fell steadily in Britain after the end of the 1920-22 depression was not entirely correct. Unemployment did indeed fall substantially after 1922, but remained around 10 percent in 1924 — there are conflicting estimates based on different assumptions about how to determine whom to count as unemployed — when the pound began appreciating before the restoration of the prewar parity. Unemployment continued rising rise until 1926, but remained below the 1922 level. Unemployment then fell substantially in 1926-27, but rose again in 1928 (as gold accumulation by France and the US led to a rise in Bank rate), without reaching the 1926 level. Unemployment fell slightly in 1929 and was less than the 1924 level before the crash. See Eichengreen “Unemployment in Interwar Britain.”

I agree that unemployment had been a serious problem in Britain before 1928. But that wasn’t because sufficient gold was lacking in the system. Unemployment was a British problem caused by an overvalued exchange rate; it was not a systemic gold-standard problem.

Before World War I, when the gold standard was largely a sterling standard (just as the postwar gold standard became a dollar standard), the Bank of England had been able to “draw gold from the moon” by raising Bank rate. But the gold that had once been in the moon moved to the US during World War I. What Britain required was a US discount rate low enough to raise the world price level, thereby reducing deflationary pressure on Britain caused by overvaluation of sterling. Instead of keeping the discount rate at 3.5 – 4%, and allowing an outflow of gold, the Fed increased its discount rate, inducing a gold inflow and triggering a worldwide deflationary catastrophe. Between 1929 to 1931, British unemployment nearly doubled because of that catastrophe, not because Britain didn’t have enough gold. The US had plenty of gold and suffered equally from the catastrophe.