John Tamny, whose economic commentary I usually take with multiple grains of salt, writes an op-ed about the price of gold in today’s Wall Street Journal, a publication where the probability of reading nonsense is dangerously high. Amazingly, Tamny writes that the falling price of gold is a good sign for the US economy. “The recent decline in the price of gold, ” Tamny informs us, “is cause for cautious optimism.” What’s this? A sign that creeping sanity is infiltrating the editorial page of the Wall Street Journal? Is the Age of Enlightenment perhaps dawning in America?

Um, not so fast. After all, we are talking about the Wall Street Journal editorial page. Yep, it turns out that Tamny is indeed up to his old tricks again.

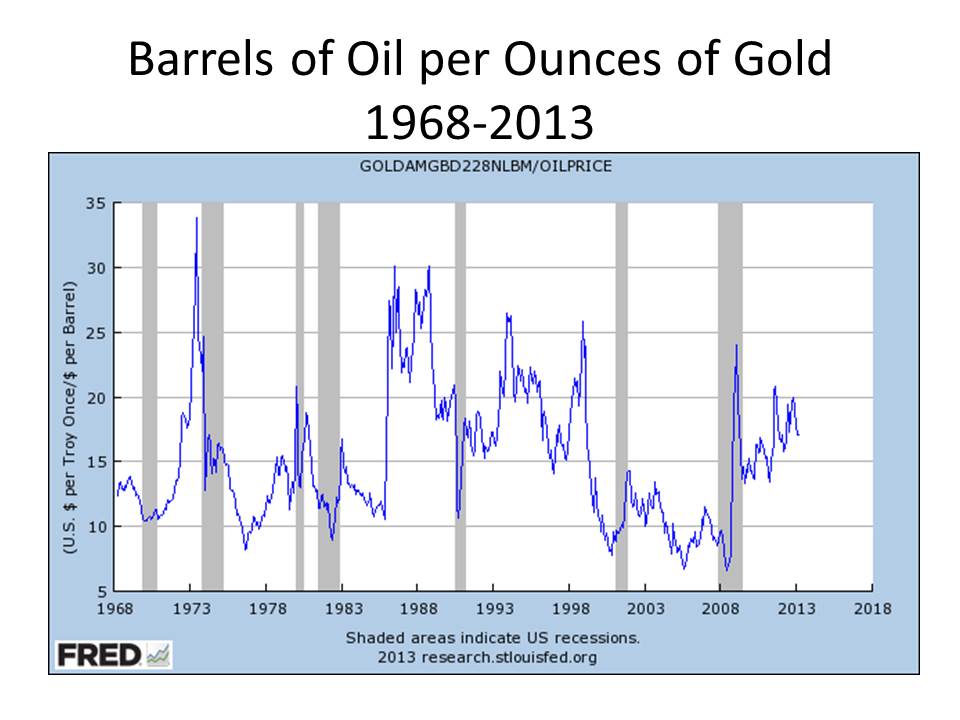

The precious metal has long been referred to as “the golden constant” for its steady value. An example is the skyrocketing price of gold in the 1970s, which didn’t so much signal a spike in gold’s value as it showed the decline of the dollar in which it was priced. If gold’s constancy as a measure of value is doubted, consider oil: In 1971 an ounce of gold at $35 bought 15 barrels, in 1981 an ounce of gold at $480 similarly bought 15 barrels, and today an ounce once again buys a shade above 15.

OMG! The golden constant! Gold was selling for about $35 an ounce in 1970 rose to nearly $900 an ounce in 1980, fell to about $250 an ounce in about 2001, rose back up to almost $1900 in 2011 and is now below $1400, and Mr. Tamny thinks that the value of gold is constant. Give me a break. Evidently, Mr. Tamny attaches deep significance to the fact that the value of gold relative to the value of a barrel of oil was roughly 15 barrels of oil per ounce in 1971, and again in 1981, and now, once again, is at roughly 15 barrels per ounce, though he neglects to inform us whether the significance is economic or mystical.

So I thought that I would test the constancy of this so-called relationship by computing the implied exchange rate between oil and gold since April 1968 when the gold price series maintained by the Federal Reserve Bank of St. Louis begins. The chart below, derived from the St. Louis Fed, plots the monthly average of the number of barrels of oil per ounce of gold from April 1968 (when it was a bit over 12) through March 2013 (when it was about 17). But as the graph makes clear the relative price of gold to oil has been fluctuating wildly over the past 45 years, hitting a low of 6.6 barrels of oil per ounce of gold in June 2008, and a high of 33.8 barrels of oil per ounce of gold in July 1973. And this graph is based on monthly averages; plotting the daily fluctuations would show an even greater amplitude.

Do Mr. Tamny and his buddies at the Wall Street Journal really expect people to buy this nonsense? This is what happens to your brain when you are obsessed with gold. If you think that the US and the world economies have been on a wild ride these past five years, imagine what it would have been like if the US or the world price level had been fluctuating as the relative price of gold in terms of oil has been fluctuating over the same time period. And don’t even think about what would have happened over the past 45 years under Mr. Tamny’s ideal, constant, gold-based monetary standard.

Do Mr. Tamny and his buddies at the Wall Street Journal really expect people to buy this nonsense? This is what happens to your brain when you are obsessed with gold. If you think that the US and the world economies have been on a wild ride these past five years, imagine what it would have been like if the US or the world price level had been fluctuating as the relative price of gold in terms of oil has been fluctuating over the same time period. And don’t even think about what would have happened over the past 45 years under Mr. Tamny’s ideal, constant, gold-based monetary standard.

Let’s get this straight. The value of gold is entirely determined by speculation. The current value of gold has no relationship — none — to the value of the miniscule current services gold now provides. It is totally dependent on the obviously not very well-informed expectations of people like Mr. Tamny.

Gold indeed had a relatively stable value over long periods of time when there was a gold standard, but that was largely due to fortuitous circumstances, not the least of which was the behavior of national central banks that would accumulate gold or give up gold as needed to prevent the value of gold from fluctuating as wildly as it otherwise would have. When, as a result of the First World War, gold was largely demonetized, prices were no longer tied to gold. Then, in the 1920s, when the world tried to restore the gold standard, it was beyond the capacity of the world’s central banks to recreate the gold standard in such a way that their actions smoothed the inevitable fluctuations in the value of gold. Instead, their actions amplified fluctuations in the value of the gold, and the result was the greatest economic catastrophe the world had seen since the Black Death. To suggest another restoration of the gold standard in the face of such an experience is sheer lunacy. But, as members of at least one of our political parties can inform you, just in case you have been asleep for the past decade or so, the lunatic fringe can sometimes transform itself . . . into the lunatic mainstream.

David, it´s a ‘constant’ only in the sense it has provided near zero average returns!

Asset Average Annual Real Returns, 1838-2012

Stocks 6.49%

Treasury bonds 2.77%

Gold 0.46%

LikeLike

David, excellent post! At first I was astonished that Tamny had written something that you thought was worthwhile… and then I kept reading, and the world came back together again for me. Not that I’m an expert on Tamny’s “work”: I saw just one article by him, but it was incredibly preposterous… even for a rank amateur like myself! The comments section was filled with derision from all quarters… all schools of thought… except one guy, who so tirelessly defended Tamny (and so won his praise) that I started to suspect that the commenter was actually Tamny himself.

Now what about David Stockman?! He’s out there making lots of noise about his new book and he’s really pushing the gold standard hard. Perhaps he’s deserving of your attention in another article?

LikeLike

Interesting as always, David.

I take a slightly different view to you in that *most* commodities actually exhibit some kind of long-term mean relationship with oil. (This appears to particularly be the case since the early 2000s. Indeed, the increasing linkage to oil prices is thought to be one of the key drivers in the previous commodity boom.) All this is not too surprising when one considers that oil/energy is a fundamental supply input to all commodities and so obviously stands to effect final prices.

Anyway, the point is that one could make this “golden constant” argument about a bunch of different goods and commodities, including copper, soy and fertilizer. I have some relevant graphs here: http://stickmanscorral.blogspot.no/2012/09/are-charts-of-oil-priced-in-gold-really.html

Funny that I’ve never seen someone in the WSJ editorial page call for a soy bean standard, though.

LikeLike

Tamney, an ignorant hard money zealot, was a telemarkerter for Cato before Steve Forbes decided it would be a good idea to let him write for his website. And now his painful, ignorant drivel is on the pages of the WSJ. It’s like the WSJ is running backward on a treadmill, destination: The Stone Age. Clownshow in clownshoes.

LikeLike

A lot of nonsense gets published. Why are you especially upset with The Wall Street Journal?

“The value of gold is entirely determined by speculation”: In other words, by the same factors that determine the value of the dollar, in the existing system. You seem to be sneering at this speculation when you refer to “the obviously not very well-informed expectations of people like Mr. Tamny”; but it seems to me that this speculation, *taken as a whole*, is well-informed and rational. (If you think otherwise, I wonder why.)

“To suggest another restoration of the gold standard in the face of such an experience is sheer lunacy.” The term ‘gold standard’ comprises a pretty wide variety of monetary systems. The one in place in the late 20s and early 30s worked poorly, but there are many alternatives that must be considered versions of “the gold standard.”

LikeLike

Brilliant. In the econ class I’m teaching in an MBA program (for stdents with little-or-no background in econ), we’re going to spend some time, at their request, on the recent gold price changes. I’m giving them the link to this as reading before we have our discussion.

LikeLike

Historically, silver has been a much more important monetary metal than gold. Gold being the dominant monetary metal was a relatively brief interlude during the Industrial age.

Given that silver and gold occur in the Earth’s crust at about a 15:1 ratio, a certain level of prosperity had to be reached before a gold standard was practical. The Industrial Revolution massively increased productivity, hence the 1873-1914 apotheosis of gold. But that same productivity that enabled widespread use of the gold standard surely also doomed it, since the accelerating rise in production of goods and services was bound to outstrip gold supply, creating ever greater risk of a disastrous monetary contraction.

The process was somewhat the reverse of the “Price Revolution” of the C16th and C17th, when the late C15th surge in Central European silver production, followed by the flood of American silver, meant the supply of silver constantly outran European production, creating continuous monetary expansion, aggravated by use of paper instruments and various debasements, and so a persistently rising price level.

LikeLike

This is an especially laughable Tamny article. Near as I can tell he doesn’t consider a bank deposit to be money… only physical bills and coins.

http://www.forbes.com/sites/johntamny/2012/07/29/ron-paul-fractional-reserve-banking-and-the-money-multiplier-myth/2/

LikeLike

I have a speculative hypothesis that the more one uses the Wall Street Journal as one’s source for news and commentary, the probability of being seriously and systematically misinformed asymptotically approaches 1.

LikeLike

Marcus, Thanks for sharing.

Tom, Well, it took me a couple of minutes to read Tamny’s piece; I think it would take a lot longer to read Stockman’s book. I don’t think it’s worth it. But I’ll keep my eye open for anything he writes that’s more easily digestible. In the meantime, James Surowiecki has a piece about him in this week’s New Yorker.

Grant, Oil is clearly related to the value of a lot of goods, but the value of gold has almost no relationship to its cost of production, because the outstanding stock is so large relative to current output.

Tommy, Looks like you’ve done a lot of research. The WSJ was once a great newspaper.

Philo, Because I published two or three pieces in the Journal in the 1980s, and I don’t like to see a once great newspaper being trashed.

I am not against speculation. My point is that any commodity whose value depends largely on speculative demand is going to be subject to large swings in its value. Such volatility makes a commodity especially unsuitable to serve as a medium of exchange.

The gold standard of the 1920s and 1930s was unsuccessful largely because it attempted to recreate a system that had broken down. Humpty Dumpty may have been a fine specimen in his prime, but once he took a fall, all the king’s horses and all the king’s men couldn’t put him back together again. Same is true of the gold standard.

Donald. Thanks. Glad to be of service.

Lorenzo, I am not sure that the gold standard was necessarily doomed by the increased productivity of the nineteenth century. It was world war I that destroyed it.

Tom, Thanks for the link.

Julian, Sounds ad hoc, but very plausible.

LikeLike

David,

Perhaps the gold standard is broken, and even a Larry White-type Free Banking system based on gold-backed commodity money is unrealistic, too.

My question is: if so, then why do central banks still even have gold on their balance sheets and continue to add to their stocks? According to Businessweek, “Central banks own about 19 percent of all gold ever mined, and last year boosted their holdings by the most since 1964.”

http://www.businessweek.com/news/2013-04-16/gold-tumble-divides-central-banks-as-sri-lanka-sees-opportunity#p2

What is the purpose of all these superfluous gold holdings? I don’t mean this as a “gotcha,” I’m genuinely curious what the role of gold in the int’l monetary/financial system is today.

LikeLike

David: clearly, the gold standard wasn’t doomed by the increased productivity of the C19th, since it lasted into the C20th. Indeed, increased gold production produced a mildly inflationary period up to WWI. Though I would argue the expansion of the gold standard had a deleterious effect on the British economy since, unlike Germany with the benefits of unification and technological catch-up and unlike the US with expanding population and land use, it did not have commensurate supply improvements to counteract the general deflationary effect of the expansion of the “gold zone”–it was already on the technological frontier and did not have much more efficiency to squeeze out of its institutions.

As for WWI dooming it, presumably if the same patience had been followed after WWI as after the Napoleonic War, perhaps it would have lasted longer. My point was to wonder whether the continuing increase in productivity in the C20th would have permitted it to be sustained; I rather think not.

LikeLike

David, I understand not wanting to waste your time on Stockman’s book, but he is making the rounds! How about just one of his media appearances or his “readers digest” version of the book (NY Times article). Here’s some of his appearances recently:

Bill Maher Show

Chris Matthews “Hardball”

Debate with Krugman on some pannel discussion (I forgot the network)

“On Point” radio show w/ Tom Ashbrook (NPR show… he gets a full hour on this one)

Here’s his NY Time article:

Re: Tamny’s article I link to above. The fascinating thing is that Tamny’s so wrong he’s actually right on a couple of points! For instance he concludes the money multiplier is a myth, but try to follow his reasoning! Again the only think I can think is that because only so many people can have paper bills and coins in their pockets, the fact that bank deposits can be greater than the amount of physical cash is meaningless… that cash didn’t multiply! Ha!

LikeLike

Perfect graph comparing Gold with other stuff is always great. You can see that the Value of Gold has an intrinsic value. Which cannot be made out of nothing like fiat money.

LikeLike

John, There may be a lot of reasons why central banks are still holding on to their gold, and I have never really studied it, so I can’t speak authoritatively. But the obvious reason is that that holding such huge amounts of gold makes them hostages to gold in the same way that China is a hostage to US Treasury obligations. If they try to unload their holdings they risk creating a self-fulfilling expectation that the price of gold is going to drop which would wipe out a huge portion of their assets. So central banks are now complicit in propping up the value of this essentially useless commodity.

Lorenzo, Your increasing productivity thesis is implicitly assuming that productivity increases in gold mining lag behind those elsewhere in the economy, which may be a reasonable assumption, but is not strictly necessary. Actually in the 1920s, Gustav Cassel, aside from warning about the short-term deflationary risk of the restored gold standard, was also warning that there would be a secular deflationary tendency once the gold standard was generally restored, because he did not believe that gold production would increase at the 3% annual rate that he calculated was necessary to avoid long-term deflation. Interestingly, Hawtrey who was in complete agreement with Cassel on the short-term deflationary risk of a restored gold standard, was not convinced by Cassel’s long-run secular argument, and felt that there was as much chance of secular inflation as secular deflation if the short-term deflationary risks were avoided. Of course, short-term deflation destroyed the gold standard, so we don’t know who was right about the long-term prospects, Cassel or Hawtrey.

Tom, Ok, I will watch out for Stockman, but don’t be upset if I continue to ignore him.

Tas, Most economists don’t believe in intrinsic value. And in my opinion, gold’s value is almost completely speculative.

LikeLike

Fair enough. It seems like an interesting question, though.

Your answer (which I appreciate you have not researched before) still doesn’t explain why central banks are adding to their gold holdings. And if it’s a prisoner’s dilemma situation as you describe, then why don’t some of the central banks with smaller gold holdings jump ship first? The first ones to fully defect from gold won’t suffer any losses on their balance sheets.

LikeLike

My grandfather once said, “All gold is fool’s gold.”

You know, in the half-century since he said that, I have yet to see his sentiments disproved. The feeble-minded are inclined to auriferous fever, but it need not be contagious.

And what is it about gold and oil? How about gold vs. natural gas? Why oil? Why not palm oil?

And the famed canard that an “ounce of gold will buy a well-made suit clothes.” That is wide enough to drive an ocean liner through. A suit made in what country? Three-piece, or two? With accessories or not? And what is “well-made”?

Suits that were $700 a few years back now cost $1500? But were $1900 two years ago?

Besides that, I have come to conclusion that commodities-backed currency will inevitably lead to monetary asphyxiation.

You must have constant deflation to make the gold standard work (at all).

Japan had chronic deflation, and it was not pretty.

LikeLike

David: Thank you for your response, very helpful. Particularly for a post I have just done on the three ages of trade over the 2200 years — the age of silk and spices (c220BC-c1500), the age of silver (c1500-c1830) and the industrial age (c1830-).

http://skepticlawyer.com.au/2013/04/29/selenium-silk-spices-and-silver-drivers-of-human-history/

LikeLike

John, Central banks make all sorts of questionable investment decisions, and there are not that many assets that central banks can acquire without inviting unwanted scrutiny, so I don’t think that there is any mystery why they continue to hold or even add to their holdings of gold, but I agree that, once there is a widespread expectation of falling gold prices, it is the central with relatively small holdings of gold that would be most likely to start selling

Benjamin, Your grandfather knew whereof he spoke.

Lorenzo, You are welcome. And thank you for the link. Looks interesting.

LikeLike

What is overlooked is that the ‘average’ over a period of time is constant at around 15.5 barrels of crude per ounce of gold.

The deviations from the mean from time to time were no doubt agreed with the oil cartel around the late 70’s in order that the ‘effects’ of taking the dollar off the gold standard could be used to thwart speculators (outside the ring) and also help adjust economic imbalances when required.

However, by, over time this being corrected by maintaining the average, ensures that the oil cartel is not short changed by the US dollar depreciation (which appears constant). We learned from Lawrence, (aided by Hollywood) if no one else, of the Arabs only trust in gold, not paper.

Why Crude Oil and gold being the measure? If one views oil as the metaphorical ‘ETF’ of commodities, because oil is used by all nations, and is vital to all economies, and is extensive in its use in the extraction, production, manufacturing, and transporting of goods; and gold as the ‘ETF’ of all ‘money’ due to its historical, and unique properties, that have withstood the test of time, then it becomes a reasonable acceptable, ‘bellwether’ for the economy.

LikeLike