John Tamny, whose economic commentary I usually take with multiple grains of salt, writes an op-ed about the price of gold in today’s Wall Street Journal, a publication where the probability of reading nonsense is dangerously high. Amazingly, Tamny writes that the falling price of gold is a good sign for the US economy. “The recent decline in the price of gold, ” Tamny informs us, “is cause for cautious optimism.” What’s this? A sign that creeping sanity is infiltrating the editorial page of the Wall Street Journal? Is the Age of Enlightenment perhaps dawning in America?

Um, not so fast. After all, we are talking about the Wall Street Journal editorial page. Yep, it turns out that Tamny is indeed up to his old tricks again.

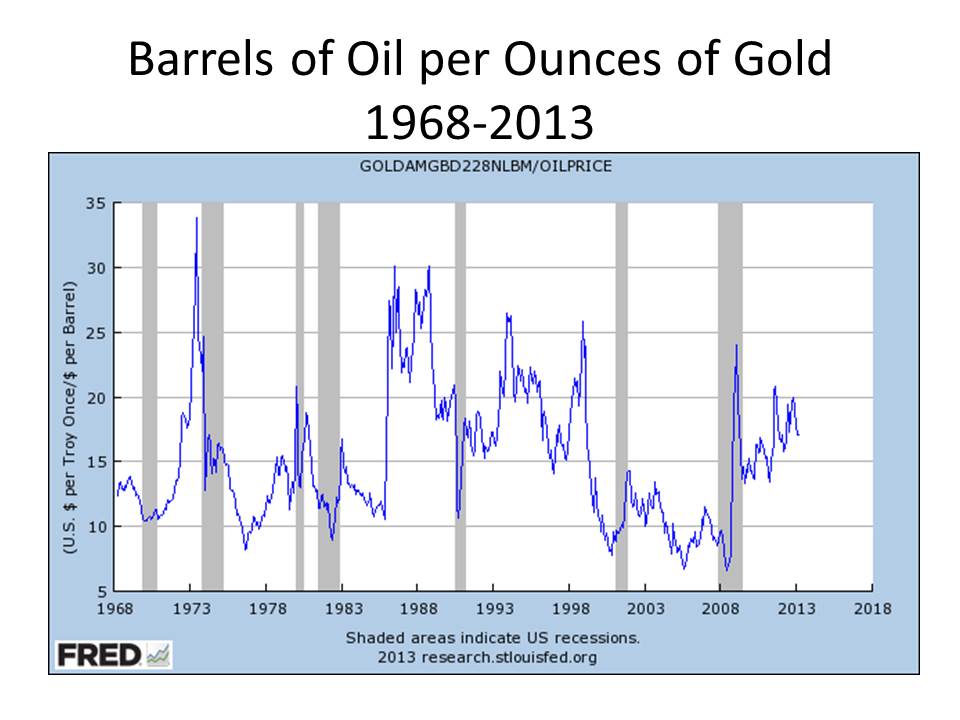

The precious metal has long been referred to as “the golden constant” for its steady value. An example is the skyrocketing price of gold in the 1970s, which didn’t so much signal a spike in gold’s value as it showed the decline of the dollar in which it was priced. If gold’s constancy as a measure of value is doubted, consider oil: In 1971 an ounce of gold at $35 bought 15 barrels, in 1981 an ounce of gold at $480 similarly bought 15 barrels, and today an ounce once again buys a shade above 15.

OMG! The golden constant! Gold was selling for about $35 an ounce in 1970 rose to nearly $900 an ounce in 1980, fell to about $250 an ounce in about 2001, rose back up to almost $1900 in 2011 and is now below $1400, and Mr. Tamny thinks that the value of gold is constant. Give me a break. Evidently, Mr. Tamny attaches deep significance to the fact that the value of gold relative to the value of a barrel of oil was roughly 15 barrels of oil per ounce in 1971, and again in 1981, and now, once again, is at roughly 15 barrels per ounce, though he neglects to inform us whether the significance is economic or mystical.

So I thought that I would test the constancy of this so-called relationship by computing the implied exchange rate between oil and gold since April 1968 when the gold price series maintained by the Federal Reserve Bank of St. Louis begins. The chart below, derived from the St. Louis Fed, plots the monthly average of the number of barrels of oil per ounce of gold from April 1968 (when it was a bit over 12) through March 2013 (when it was about 17). But as the graph makes clear the relative price of gold to oil has been fluctuating wildly over the past 45 years, hitting a low of 6.6 barrels of oil per ounce of gold in June 2008, and a high of 33.8 barrels of oil per ounce of gold in July 1973. And this graph is based on monthly averages; plotting the daily fluctuations would show an even greater amplitude.

Do Mr. Tamny and his buddies at the Wall Street Journal really expect people to buy this nonsense? This is what happens to your brain when you are obsessed with gold. If you think that the US and the world economies have been on a wild ride these past five years, imagine what it would have been like if the US or the world price level had been fluctuating as the relative price of gold in terms of oil has been fluctuating over the same time period. And don’t even think about what would have happened over the past 45 years under Mr. Tamny’s ideal, constant, gold-based monetary standard.

Do Mr. Tamny and his buddies at the Wall Street Journal really expect people to buy this nonsense? This is what happens to your brain when you are obsessed with gold. If you think that the US and the world economies have been on a wild ride these past five years, imagine what it would have been like if the US or the world price level had been fluctuating as the relative price of gold in terms of oil has been fluctuating over the same time period. And don’t even think about what would have happened over the past 45 years under Mr. Tamny’s ideal, constant, gold-based monetary standard.

Let’s get this straight. The value of gold is entirely determined by speculation. The current value of gold has no relationship — none — to the value of the miniscule current services gold now provides. It is totally dependent on the obviously not very well-informed expectations of people like Mr. Tamny.

Gold indeed had a relatively stable value over long periods of time when there was a gold standard, but that was largely due to fortuitous circumstances, not the least of which was the behavior of national central banks that would accumulate gold or give up gold as needed to prevent the value of gold from fluctuating as wildly as it otherwise would have. When, as a result of the First World War, gold was largely demonetized, prices were no longer tied to gold. Then, in the 1920s, when the world tried to restore the gold standard, it was beyond the capacity of the world’s central banks to recreate the gold standard in such a way that their actions smoothed the inevitable fluctuations in the value of gold. Instead, their actions amplified fluctuations in the value of the gold, and the result was the greatest economic catastrophe the world had seen since the Black Death. To suggest another restoration of the gold standard in the face of such an experience is sheer lunacy. But, as members of at least one of our political parties can inform you, just in case you have been asleep for the past decade or so, the lunatic fringe can sometimes transform itself . . . into the lunatic mainstream.