One of the leading financial journalists of our time, James Grant is obviously a very smart, very well read, commentator on contemporary business and finance. He also has published several highly regarded historical studies, and according to the biographical tag on his review of a new book on the monetary role of gold in the weekend Wall Street Journal, he will soon publish a new historical study of the dearly beloved 1920-21 depression, a study that will certainly be worth reading, if not entirely worth believing. Grant reviewed a new book, War and Gold, by Kwasi Kwarteng, which provides a historical account of the role of gold in monetary affairs and in wartime finance since the 16th century. Despite his admiration for Kwarteng’s work, Grant betrays more than a little annoyance and exasperation with Kwarteng’s failure to appreciate what a many-splendored thing gold really is, deploring the impartial attitude to gold taken by Kwarteng.

Exasperatingly, the author, a University of Cambridge Ph. D. in history and a British parliamentarian, refuses to render historical judgment. He doesn’t exactly decry the world’s descent into “too big to fail” banking, occult-style central banking and tiny, government-issued interest rates. Neither does he precisely support those offenses against wholesome finance. He is neither for the dematerialized, non-gold dollar nor against it. He is a monetary Hamlet.

He does, at least, ask: “Why gold?” I would answer: “Because it’s money, or used to be money, and will likely one day become money again.” The value of gold is inherent, not conferred by governments. Its supply tends to grow by 1% to 2% a year, in line with growth in world population. It is nice to look at and self-evidently valuable.

Evidently, Mr. Grant’s enchantment with gold has led him into incoherence. Is gold money or isn’t it? Obviously not — at least not if you believe that definitions ought to correspond to reality rather than to Platonic ideal forms. Sensing that his grip on reality may be questionable, he tries to have it both ways. If gold isn’t money now, it likely will become money again — “one day.” For sure, gold used to be money, but so did cowerie shells, cattle, and at least a dozen other substances. How does that create any presumption that gold is likely to become money again?

Then we read: “The value of gold is inherent.” OMG! And this from a self-proclaimed Austrian! Has he ever heard of the “subjective theory of value?” Mr. Grant, meet Ludwig von Mises.

Value is not intrinsic, it is not in things. It is within us. (Human Action p. 96)

If value “is not in things,” how can anything be “self-evidently valuable?”

Grant, in his emotional attachment to gold, feels obligated to defend the metal against any charge that it may have been responsible for human suffering.

Shelley wrote lines of poetry to protest the deflation that attended Britain’s return to the gold standard after the Napoleonic wars. Mr. Kwarteng quotes them: “Let the Ghost of Gold / Take from Toil a thousandfold / More than e’er its substance could / In the tyrannies of old.” The author seems to agree with the poet.

Grant responds to this unfair slur against gold:

I myself hold the gold standard blameless. The source of the postwar depression was rather the decision of the British government to return to the level of prices and wages that prevailed before the war, a decision it enforced through monetary means (that is, by reimposing the prewar exchange rate). It was an error that Britain repeated after World War I.

This is a remarkable and fanciful defense, suggesting that the British government actually had a specific target level of prices and wages in mind when it restored the pound to its prewar gold parity. In fact, the idea of a price level was not yet even understood by most economists, let alone by the British government. Restoring the pound to its prewar parity was considered a matter of financial rectitude and honor, not a matter of economic fine-tuning. Nor was the choice of the prewar parity the only reason for the ruinous deflation that followed the postwar resumption of gold payments. The replacement of paper pounds with gold pounds implied a significant increase in the total demand for gold by the world’s leading economic power, which implied an increase in the total world demand for gold, and an increase in its value relative to other commodities, in other words deflation. David Ricardo foresaw the deflationary consequences of the resumption of gold payments, and tried to mitigate those consequences with his Proposals for an Economical and Secure Currency, designed to limit the increase in the monetary demand for gold. The real error after World War I, as Hawtrey and Cassel both pointed out in 1919, was that the resumption of an international gold standard after gold had been effectively demonetized during World War I would lead to an enormous increase in the monetary demand for gold, causing a worldwide deflationary collapse. After the Napoleonic wars, the gold standard was still a peculiarly British institution, the rest of the world then operating on a silver standard.

Grant makes further extravagant and unsupported claims on behalf of the gold standard:

The classical gold standard, in service roughly from 1815 to 1914, was certainly imperfect. What it did deliver was long-term price stability. What the politics of the gold-standard era delivered was modest levels of government borrowing.

The choice of 1815 as the start of the gold standard era is quite arbitrary, 1815 being the year that Britain defeated Napoleonic France, thereby setting the stage for the restoration of the golden pound at its prewar parity. But the very fact that 1815 marked the beginning of the restoration of the prewar gold parity with sterling shows that for Britain the gold standard began much earlier, actually 1717 when Isaac Newton, then master of the mint, established the gold parity at a level that overvalued gold, thereby driving silver out of circulation. So, if the gold standard somehow ensures that government borrowing levels are modest, one would think that borrowing by the British government would have been modest from 1717 to 1797 when the gold standard was suspended. But the chart below showing British government debt as a percentage of GDP from 1692 to 2010 shows that British government debt rose rapidly over most of the 18th century.

Grant suggests that bad behavior by banks is mainly the result of abandonment of the gold standard.

Grant suggests that bad behavior by banks is mainly the result of abandonment of the gold standard.

Progress is the rule, the Whig theory of history teaches, but the old Whigs never met the new bankers. Ordinary people live longer and Olympians run faster than they did a century ago, but no such improvement is evident in our monetary and banking affairs. On the contrary, the dollar commands but 1/1,300th of an ounce of gold today, as compared with the 1/20th of an ounce on the eve of World War I. As for banking, the dismal record of 2007-09 would seem inexplicable to the financial leaders of the Model T era. One of these ancients, Comptroller of the Currency John Skelton Williams, predicted in 1920 that bank failures would soon be unimaginable. In 2008, it was solvency you almost couldn’t imagine.

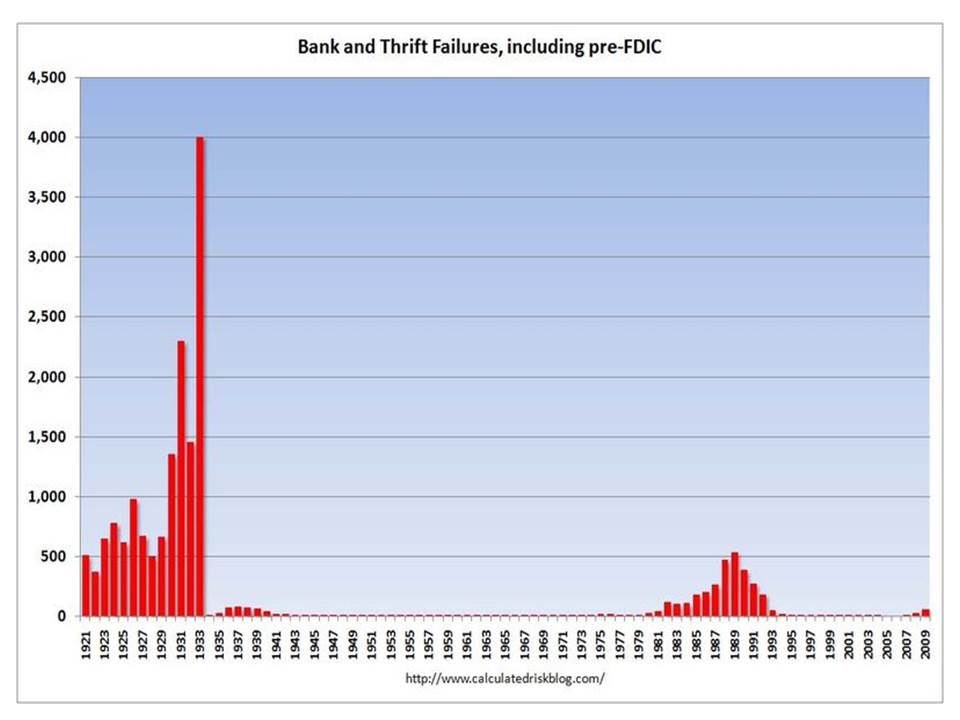

Once again, the claims that Mr. Grant makes on behalf of the gold standard simply do not correspond to reality. The chart below shows the annual number of bank failures in every years since 1920.

Somehow, Mr. Grant somehow seems to have overlooked what happened between 1929 and 1932. John Skelton Williams obviously didn’t know what was going to happen in the following decade. Certainly no shame in that. I am guessing that Mr. Grant does know what happened; he just seems too bedazzled by the beauty of the gold standard to care.

Surely the UK went back on the gold standard in 1821 (in the sense of the Bank of England’s notes were once more redeemable for a gold).

LikeLike

That should be “for gold”.

LikeLike

First of all, funny how that when push came to shove, and the economy needed to function at full potential – the gold standard was always shoved aside.

If that doesn’t tell you everything about gold, I don’t know what does.

And second of all – why are we paying attention to James Grant ?

LikeLike

Well, David. I was just reading your previous post dealing with “backing” v. “quantity” theories of money, and now this.

I think a “price stability” argument for the gold standard shows the propounder doesn’t really quite grasp the idea. You might have stable prices under a gold standard, you might not.

What it really boils down to is related to your previous post: a long and not very satisfying discussion about how FRN’s are a liability of the Fed. Empirically speaking it’s not terribly important, currency being a relatively small percentage of “money”; but conceptuatlly it is, because a “note” is a promise to pay something, and the FRN’s “promise” is illusory.

This privilege of being the sole arbiter of when your promise is fulfilled is much closer to the true value of the gold standard.

Here’s one way in which the gold standard might matter a great deal:

I tried to explain and advocate for a gold standard in these posts:

I don’t think I ever mentioned price stability.

Interesting stuff. To me, at least.

LikeLike

David i think i commented, in one of my previous blogs, about smart people making ridiculous judgments. I believe it was related to the Fed meeting minutes where people like Plosser didn’t see any thing to worry about just before everything started falling apart with Lehman and Bear Stearns. James Grant would seem to fall in that category too.

If he is aware that the under the gold standard there was a tendency to move towards deflation, why is he suddenly hit by a love for gold when inflation is hardly a problem? In fact, efforts are being directed towards reflating the economy. How does Grant propose to do that with Gold?

LikeLike

Keynes got this one right I think (in A Tract on Monetary Reform?). Monetary policy can focus either on stabilizing a country’s internal price level, or on stabilizing the exchange rate. The international gold standard, in which countries adopted a fixed gold-to-currency policy, effectively forces monetary authorities to stabilize the exchange rate. What this leads to is not a stable internal price level, but alternating bouts of inflation and deflation (as the internal economy adjusts so as to maintain the stable exchange rate).

LikeLike

One wonders if James Grant even understands “price stability”. While average inflation rates may have been closer to zero under the gold standard, the volatility in prices was substantially larger.

Is that really preferably to a low, but positive, rate of inflation with minimal variance? Predictability of the price level seems vastly more important than the actual price level, itself.

It seems unfathomable that such a “very smart, very well read” commentator would flunk such basic econ 101. One wonders whether writing for the WSJ accelerates the depreciation of human capital.

LikeLike

Shahid, it’s very easy to increase the money supply – that is, for example, the number of dollars – under a gold standard just by changing the dollar to gold ratio by law. Like passing any law, it has to be done out in the open, of course.

One big mistake Britain made by returning to the gold standard after WWI was to also return to the original pound-gold ratio. A lot of thought has to go into where to peg your monetary unit of account. If you read those links I posted previously, you’ll see that the only feasible way to return to a gold standard for the dollar now is to price it at about $30K per ounce. Maybe more, but you get the idea.

The other component of addressing the ‘crisis’ that I proposed was a universal debt jubilee by law. Constitutional amendment, in fact.

Anyway, I’ve put those ideas out there and nobody seems to like them much! Alas.

LikeLike

David, this may be a dumb question, but I don’t recall seeing it before, so I’m just going to ask it. You mentioned here and in your book that one of the main weaknesses of a gold-based monetary system is its vulnerability to rapid swings in the value of gold relative to other goods and services.

My question is: what, if any, problems would arise in a free banking system where banks promised to redeem deposits and notes not for a fixed amount of physical gold but instead for a contractually-specified amount of purchasing power? In other words, if the relative value of gold increased, the amount of gold the bank would be obligated to redeem per dollar would decrease, and vice versa.

I suppose it would be like a privatized version of Fisher’s compensated dollar plan. Assuming the incentive problems could by fixed by the remedies you and Earl Thompson proposed, would it be workable?

LikeLike

In regard to your last point, it seems that many other factors besides the role of gold in the monetary system can strongly influence the frequency of bank failures. As Larry White has shown, both England and Scotland had gold-based systems prior to Peel’s Act, but England had proportionately more bank failures due to various restrictions on note issuance and bank size. And while the US saw thousands of bank failures in the early 1930s, Canada did not have any (perhaps primarily due to its nationwide branch banking system, as opposed to the US reliance on unit banking).

These are familiar points, of course, but they still indicate (to me, at least) that the role of gold alone cannot determine the stability or fragility of a given monetary system.

LikeLike

John S:

I can’t see how, if the (say) dollar price of gold is fixed by law that doesn’t more or less guarantee a stable monetary system, barring a sudden dramatic increase in the supply of gold, which could happen in theory, I suppose, but the unlikelihood of that is one of the reasons gold has had a monetary role in the first place.

Of course, a stable monetary system is not the same as a stable economy. I would certainly agree that a gold based monetary system doesn’t guarantee a stable economy. Then again, so what? Put crudely, “haves” like a stable economy; “have-nots” don’t, for obvious and quite legitimate reasons. Neither should have the monetary system’s endorsement.

Parenthetically, Canada did not have a central bank in the early 1930’s, and until it did it apparently was on a gold standard. Maybe that explains why they didn’t have the widespread bank failures in the early ’30’s that the US did:

LikeLike

JMRJ,

There could also be a sudden dramatic increase in the demand for gold, which would increase its relative value and be deflationary if gold redemption is fixed as a physical amount. It’s possible that the US and France, by sucking huge amounts of gold out of circulation, were responsible for half or more of the deflation of the early 1930s.

http://www.voxeu.org/article/did-france-cause-great-depression

LikeLike

Thank you for the link on Canada. Re: gold standards and central banking, you may enjoy this link:

http://www.freebanking.org/2012/02/11/more-on-the-gold-standard-with-regret/

LikeLike

David, O/T: Where’s the best place to find a chart of the price level (P) vs year which compares a theoretical model of P to empirical data? Here’s two examples of what I mean for Canada and for Japan. Those both use the same model, by the way, and the author of the model also created a related pair of curves for the interest rates in those two countries (and others). He’s trying to compare his model results with professional examples but he can’t find any professional examples (he says when he does a Google image search for “price level model” he only finds his own plots (again he’s looking for model results vs empirical data)!). Do you have any idea where he should he be looking?

Thanks!

LikeLike

I hope that when my paper on the classical and interwarl gold standard and price volatility is published, the Austrians – at least the reputable ones – can finally stop proclaiming the sanctity of the classical gold standard… My gut tells me that I’m dreaming.

LikeLike

Great blogging.

James Grant is a puzzle, and he has been wrong for decades on end, ever predicting much higher inflation and interest rates. Sheesh, he was preaching that back in the 1980s, and he has never changed.

Grant’s fallback position is now that governments have repressed interest rates, so he was not really wrong.

There is a Bain & Co report out there on “A World Awash in Money” and it is worth reading. There are gluts of capital is the short story. That better explains low interest rates than Grant. Also, central banks have generally been tight since the 1980s, driving down inflation and interest rates all through Western economies.

How Grant cannot perceive this is beyond me.

So now Western central banks have driven economies to or near ZLB—and now we must devise monetary policy for this reality. I do not think more tight money is the answer.

And why gold for the gold nuts? The Chinese used silver as money and coinage (actually ingots) starting around 700 AD, and Chinese banks are still called “Silver Houses.” Why not a silver standard? Platinum?

BTW, anyone who wants to can convert their dollars into gold. It is a free market now.

Strange thing about gold: The value of gold is not stable. The value of gold vacillates widely, as seen from a peak in 1980, to a nadir about 10 years ago, and then another peak in 2010, and it has been falling since.

Since 2010, you would be better off with cash under a mattress than gold!

LikeLike

John S. – I don’t see the incentive to hoard gold when dollars are redeemable in gold at a fixed rate, other than political reasons. In any case, as long as dollar issuing authority has enough gold on hand to cover dollars outstanding – which is, after all, what the gold standard is – what difference does it make if others hoard gold?

Benjamin Cole: Under a gold standard the dollar value of gold cannot “vacillate widely” because it is fixed by law. It seems you’re not getting that. The idea is the same as any other kind of weight or measure, like quarts or miles or degrees celsius.

But I like to grapple with arguments against the gold standard. Sometimes I’m not so sure I understand everything I have to myself.

LikeLike

JMRJ,

You’d think people would stop rationalizing the virtues of fixed exchange rates. What with them failing so disastrously.

LikeLike

Daniel, what do you mean, failing disastrously?

Take the long view. We’re 43 years post “floating” exchange rates. In that time we’ve had the great 1970’s inflation, the Savings and Loan debacle of the 1980’s, the stock market crash of 1987, the Mexican peso crisis, the Asian currency crisis, the Long Term capital Management crisis, the dot com bubble bust, the real estate bubble, the 2008 banking crisis. Is this success?

Yet stability is not the economic summum bonum either way. I’m not talking about stability; I’m talking about economic justice.

Justice and truth. How can you have them when the promise to pay is for some a matter of rigorous toil and for others a matter of fiat – my promise is fulfilled when I say it is?

I think the real problems posed by deciding upon a “monetary” system, as opposed to an economic system, transcend economics. The should be addressed by the law. And the law’s primary contribution in this area is to fix a value for the unit of account. If the value isn’t fixed, it’s subject to countless other interests and considerations, and the way that pans out is that the powerful interests an considerations trump all the others.

It’s as if you give someone the power to conjure a quart of milk, rather than doing the work required to produce an actual quart of milk. It’s a formula for undeserved privilege and mischief.

LikeLike

Lorenzo, Right. But before the pound was made convertible again, its value in terms of gold had to be restored to roughly the old, pre-suspension, parity.

Daniel, Yes, eventually, but the gold standard hung around for a pretty long time before it was finally pushed aside for good.

JMRJ, Thanks for the links to your posts. I just had a quick look, but will try to read more carefully later. My initial take is that we are not at all on the same page, but you probably figured that out already.

Shahid, I don’t think he does propose to do that. I think he believes that gold will empower the confidence fairy and once businesses are confident about the future, they will start investing and hiring like crazy.

doncoffin64, Good point, I actually meant to discuss that point, but was too tired to work that into the discussion.

Dan, Evidently writing for the Wall Street Journal creates all kinds of risks, but lots of people still like to do it. I take your point about the desirability of low and steady inflation, but there may be circumstances in which variability in the rate of inflation is actually optimal. What is more important is low or stable wage inflation.

JMRJ, Changing the legal value of money in terms of gold, doesn’t change the money supply, it changes the amount of money demanded by the public, the money supply adjusts to meet the demand.

John, Why would a free banking system adopt a variable price of gold and who would decide how the value of gold would vary? In the last chapter of my book I proposed such a system would, relying on the work of Earl Thompson, but it would only about through legislation, not through competition. See my book. I agree that gold is not the only factor affecting the stability of a banking system, but historically gold has often been a destabilizing factor.

JMRJ, It is true that Canada did not have widespread bank failures in the Great Depression. But it did have a Great Depression. Contrary to Friedman’s misleading account in the Monetary History, bank failures were not the cause of the Great Depression, it was the appreciation of gold, which was caused mainly by a huge increase in the international monetary demand for gold. Bank failures merely exacerbated a crisis that would have been a catastrophe even if not a single bank had failed.

Tom, Sorry, I have no clue.

Benjamin, Well Grant is a good and entertaining writer. Fun to read, just don’t take anything he says too seriously.

JMRJ, Under a gold standard, the value of gold can fluctuate. The dollar price of gold doesn’t change, but the prices of goods can go up or down. When gold gains value, prices fall; when it loses value, prices rise

Daniel, Fixed and fluctuating exchange rates both have their advantages and their disadvantages.

LikeLike

JMRJ

I’m talking about economic justice.

Ah, yes – there we have it. Economics as a morality play. I guess it’s “moral” for people to lose their jobs whenever the demand for money goes up.

Excuse me if I fail to be impressed by your thinly disguised self-interest.

Fixed and fluctuating exchange rates both have their advantages and their disadvantages.

No matter how bad inflation is, deflation is even worse.

Hyper-inflation didn’t bring about Hitler, deflation did.

End of story.

LikeLike

David, thanks for responding. If you ever do get a chance to devote some thought to the constitutional amendment idea I’d be very grateful to know those thoughts. I put that idea out there a couple of years ago and never really got any detailed feedback or criticism. Lots of hostility, though! 🙂 Open-mindedness on some of these things is very difficult to find.

Daniel, economics inescapably involves moral questions to the extent it has an impact on how wealth is distributed. Don’t be obtuse.

LikeLike

JMRJ

So you think it’s in fact moral for people to lose their jobs when the demand for money goes up. Or for unexpected inflation to occur when demand for money goes down.

You’re right, there should be a law – one against sadists like yourself.

LikeLike

Daniel, It’s hard to generalize from historically unique circumstances.

JMRJ, Open-mindedness seems to be an underrated virtue.

Daniel, Just a suggestion, but you might want to consider dialing it down a notch.

LikeLike

David,

It’s hard to generalize from historically unique circumstances.

If the 1930s were so unique, how come that today’s repeat of the same economic phenomenon (deflation) brought the extremists to fore AGAIN ?

That’s what deflation does – brings out the crazies.

And I’m having a really hard time being understanding with people who nakedly promote their self-interest, even when it would cost society so much.

The hipocrisy is astounding.

LikeLike

Well, Daniel, I assume you’re referring to me, but there’s nothing crazy about a gold standard, however ill-advised you might believe it to be.

And I don’t know why you appear to think I am promoting my self-interest. I don’t own any gold.

When I first started studying these kinds of things I was firmly in the gold bug camp and adamantly opposed to central banks. I’m still a gold standard fan, but listening to others, further study and thought has softened my thinking about a central bank:

I don’t think there are any pat answers here. Some other thoughts I had about central banks, gold standards, and the nature of money:

I hope David doesn’t mind the multiple links, I’m just a little pressed for time this AM and can’t rehash these ideas fully over here. I appreciate constructive comments and criticisms, as I’m trying to get a handle on all this myself. I’ve found this blog quite uniquely instructive. So thanks.

LikeLike

Like I previously said – if your ideas of “justice” lead to millions of people losing their jobs when the demand for gold goes up, you’re a monster.

LikeLike

Damiel, if you have some argument to make that a rise in the demand for gold plus a gold standard equals “millions of people losing their jobs”, any more than the demand for tractors or figs would, why don’t you make it?

Engaging in hysteria and hyperbole doesn’t really advance anyone’s understanding of anything, including (maybe especially) your own.

LikeLike

JMRJ,

I should know better than to reason with people who have firm opinions on macroeconomics despite being completely ignorant of the subject, but here goes

M * V = P * Y = NGDP

Under the gold standard, M is fixed.

We also know for a fact that wages are sticky downwards. And don’t even try to argue with this.

Now ask yourself – if M is fixed, and wages don’t readily go down, what happens when V (money velocity) goes down ?

Edumacate yourself, bro. Economics is not a morality play.

LikeLike

Daniel, first,, putting ideas into equations is not a magical formula for truth. In the main as far as economics goes it is uninformative pretense.

Second, under a gold standard M is not fixed. You’re simply wrong.

Since that disposes of your assertion it is not necessary to deal with the supposedly unarguable point that wages are sticky.

Third, law trumps economics, unless we are governed by economists, which I hope even you will agree is at least mildly problematic. I could throw around a lot of legal terms and call you ignorant, too. It doesn’t enlighten anyone, including me and you.

I’m interested in any further contributions you have to make.

LikeLike

under a gold standard M is not fixed

Predictably, you took a dump on the chess board and strutted around claiming victory. Serves me right for attempting to play chess with a pigeon.

Have fun with your sadistic fantasies of “economic justice”.

LikeLike

Daniel and David, in the meantime I’ll suggest something novel for you both to consider.

It seems to me there would be considerable advantage to pegging the price of gold artificially high, indeed dramatically artificially high. With a very high dollar to gold price, the government can generate a lot of revenue through seigniorage, without taxing anyone but gold producers.

For example I have suggested that the dollar gold price should be $30K per ounce or higher. Gold producers could make a handsome profit selling it to the government for half that, with the rest being revenue to the government as seigniorage.

Do you find that at all interesting?

LikeLike

Daniel, you’re not acquitting yourself well. I didn’t claim victory, you might be right on the overall idea that the gold standard is objectionable.

I’m interested in the opinions of people who disagree with me on these things. I’m prepared to learn from you. This is not a contest.

Gold production can go up or down so M isn’t fixed. Maybe you can respond without throwing a tantrum.

LikeLike

JMRJ,

It isn’t just variation in gold production that can change M. Under a free banking gold standard, the banks themselves can change their gold reserve ratios in response to changes in V (if V declines, lending can expand since expected gross & net interbank clearings will be lower and precautionary required reserves will also be lower. Vice versa as V increases; see Selgin’s “Theory of Free Banking”). In fact, even under a centrally managed gold standard, reserve requirements can be altered, allowing for changes in M.

LikeLike

Daniel, please refer to this previous post by David Glasner.

“under a gold standard, if people want to hold more dollars, more dollars can be created. Yes more dollars can be created out of thin air under a gold standard! The whole point is that any dollars created have to be convertible on demand into gold. Well if people want to hold more dollars, they can be created, and held, just as desired. Given that people want to hold the dollars, not spend them (remember that that was the assumption we just started with), creating additional dollars to be held will not cause an increase in the rate of dollars returned for redemption. So an increase in the demand for money need not cause a recession under the gold standard.”

Thus, your statement that “Under the gold standard, M is fixed” is false.

LikeLike

David, you asked: “Why would a free banking system adopt a variable price of gold and who would decide how the value of gold would vary?”

It seems to me that under a gold-based free banking system, banks must choose to keep something fixed while allowing something else to vary. If the nominal price of gold is fixed, then as the relative value of gold increases, prices must fall (i.e., the value of the banks’ notes and deposits in terms of other goods & services must increase).

Although fixed nominal gold prices were customary, even in free banking systems, I don’t see why a bank couldn’t instead choose to keep the relative value of its notes and deposits constant by changing the nominal price of gold? I think this would be beneficial both for the bank and its customers by shielding them from the effects of rapid swings in the relative value of gold.

Imagine a variation in the Goldfinger scenario where a criminal mastermind radioactively poisons half of the world’s gold minds. The relative value of gold would increase, and banks that kept their redemption rate constant would be inundated with redemption requests by arbitrageurs looking to sell gold in the open market. While Goldfinger is fanciful, the actions of the Bank of France in the 1930s and trends in recent years have shown that rapid increases in the value of gold are not implausible.

Customers and merchants would also benefit from flexible nominal gold prices. For one thing, pricing in a stable purchasing power unit of account would be attractive since it would lessen the need for price changes in response to changes in monetary gold flows and stocks. If the value of gold were to drastically decline (say due to improved mining techniques, such as cheaper seawater gold extraction), this scheme would protect holders of bank money from being wiped out by the devaluation of the underlying asset of redemption (gold). Borrowers would also be shielded from increased debt burdens due to an increase in the relative value of gold (and lenders would be shielded from the reverse case).

LikeLike

Finally, (sorry for the quadruple post, undoubtedly a record!) you asked who would decide the nominal price of gold. Well, couldn’t it be posted daily in bank branches just as foreign exchange buying and selling rates are today? Banks would adjust their posted rates in accordance with their need for reserves, and holders of gold (such as miners) would shop around for the best “exchange rate” into notes and deposits.

Such a system might also be valuable as an early warning system for detecting banks with dangerously low reserves, much as the secondary market for bank notes during the US (not so) free banking era served as a barometer of bank health.

LikeLike

John S:

The only way I understand a gold standard is that the dollar, or other monetary unit of account, is defined by law as some quantity of gold or other. Once this is done there is no “market” in gold in that unit of account, since the dollar price of gold cannot vary. I don’t know how this free banking thing makes any sense, with banks saying a dollar means one thing one day and another thing the next. Besides, banks are as bound by the law as anyone else. If the law says a dollar equals this or that quantity of gold, banks could only vary that by flouting the law.

The whole idea of the gold standard is a consistent, or at least open and honest weight and measure.

Correct me if I’m wrong.

LikeLike

In historical free banking systems (e.g. Scotland, Australia, Canada), the nominal price of was defined by law. So your statement,

“I don’t know how this free banking thing makes any sense, with banks saying a dollar means one thing one day and another thing the next.”

is somewhat misguided because it implies that free banking necessarily means that the gold definition of the dollar/money unit can/must vary, when in fact it did not in practice.

(I think you could have a system with a variable nominal gold price, and that it would be better, but I might be wrong, and at any rate that’s a different discussion.)

Your other statement,

“Gold production can go up or down so M isn’t fixed.”

indicates to me that you believe that the money supply can only change in accordance with gold flows or stocks. This is incorrect. Even if the gold definition of the money unit is invariable, banks in free banking systems could issue as many notes and deposits as they wished (and under gold-based systems where central banks had a monopoly of note issue, banks could create new deposits). The limiting factor was the public’s willingness to hold bank-issued (“inside”) money instead of gold (“outside money”).

Like you, I don’t wish to argue for argument’s sake, only to to discover the truth through discussion.

LikeLike

John S. Well. I see from Wikipedia that Richard Timberlake has been a supporter of the “free-banking” idea. Timberlake and I go way back.

Overall, I think fractional reserve lending should be discouraged. I don’t see how it could be “outlawed”, but I’ve described a scenario where the central bank lends – at no interest – as a public service, and thereby discouragin lending at interest by anyone else:

(see #5)

I did not mean to imply that an increase in the gold supply is the only way M can vary in a gold standard monetary system. Obviously the dollar peg can be changed by law, for example, either expanding or contracting the money supply as the case may be.

You idea that reserve ratios can be changed would also change M, but since that is part and parcel of fractional reserve lending I think that should be discouraged, too.

Interesting thoughts, thank you.

LikeLike

Daniel, I agree and have written that the European Central Bank is repeating the mistakes of the 1930s. Unfortunately the only way out at this point is for the ECB to adopt an easier monetary policy which it seems to have been doing. Since it seems nearly impossible to leave the euro once a country has adopted it, the only available option is for the ECB to change its policy. But, even in the worst case, I don’t expect another Hitler to come to power.

JMRJ, Go ahead and link away

Why do you think it would be a good idea for the government to subsidize gold mines to produce a lot of gold that would just be stored in bank vaults?

John, I didn’t say that under a free banking system a bank couldn’t establish a variable conversion rate between its currency and gold, just that it seems highly unlikely that a competitive system of banks would choose such a standard rather than the simpler and more obvious alternative of a fixed gold/currency exchange rate. The benefits of a variable exchange rate are a public good, and no individual bank would be in a position to internalize them, so I don’t seen what incentive any individual bank would have to adopt what would be a more complicated and costly system.

LikeLike

David, setting aside the question of whether a free banking system would ultimately evolve past a fixed gold/currency conversion rate, do you still believe either of the systems you proposed in your book (price index or labor standard, with gold as the asset of redemption) would be feasible or desirable today, or would you modify that portion of your book if you were to rewrite it?

LikeLike