In a recent post, I criticized, perhaps without adequate understanding, some of Thomas Piketty’s arguments about capital in his best-selling book. My main criticism is that Piketty’s argument that. under capitalism, there is an inherent tendency toward increasing inequality, ignores the heterogeneity of capital and the tendency for new capital embodying new knowledge, new techniques, and new technologies to render older capital obsolete. Contrary to the simple model of accumulation on which Piketty relies, the accumulation of capital is not a smooth process; it is a very uneven process, generating very high returns to some owners of capital, but also imposing substantial losses on other owners of capital. The only way to avoid the risk of owning suddenly obsolescent capital is to own the market portfolio. But I conjecture that few, if any, great fortunes have been amassed by investing in the market portfolio, and (I further conjecture) great fortunes, once amassed, are usually not liquidated and reinvested in the market portfolio, but continue to be weighted heavily in fairly narrow portfolios of assets from which those great fortunes grew. Great fortunes, aside from being dissipated by deliberate capital consumption, also tend to be eroded by the loss of value through obsolescence, a process that can only be avoided by extreme diversification of holdings or by the exercise of entrepreneurial skill, a skill rarely bequeathed from generation to generation.

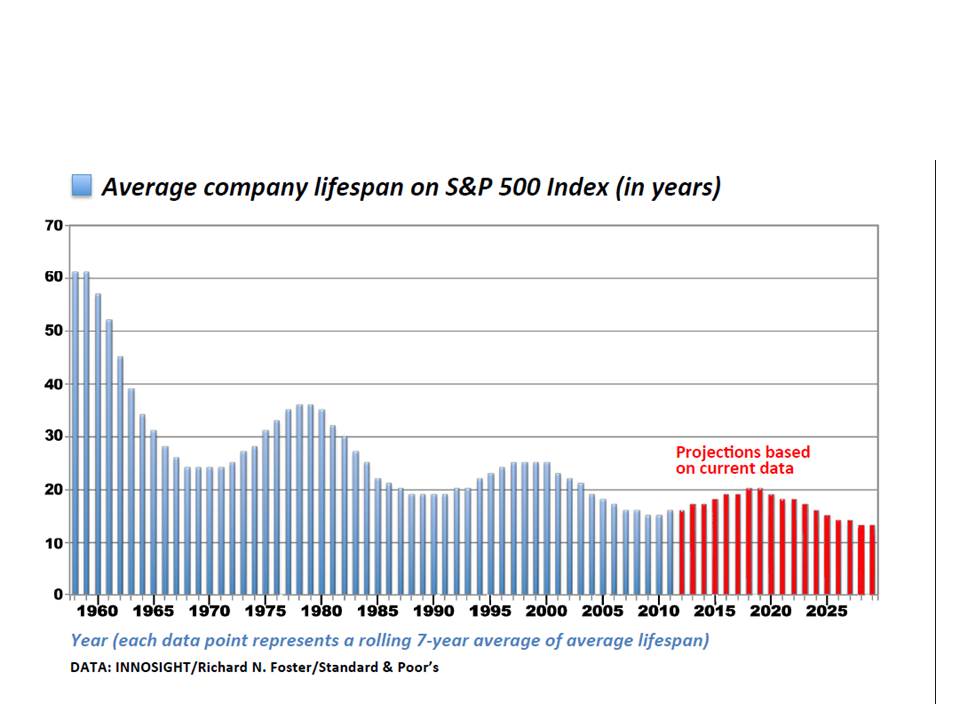

Applying this insight, Larry Summers pointed out in his review of Piketty’s book that the rate of turnover in the Forbes list of the 400 wealthiest individuals between 1982 and 2012 was much higher than the turnover predicted by Piketty’s simple accumulation model. Commenting on my post (in which I referred to Summers’s review), Kevin Donoghue objected that Piketty had criticized the Forbes 400 as a measure of wealth in his book, so that Piketty would not necessarily accept Summers’ criticism based on the Forbes 400. Well, as an alternative, let’s have a look at the S&P 500. I just found this study of the rate of turnover in the 500 firms making up the S&P 500, showing that the rate of turnover in the composition of the S&P 500 has been increased greatly over the past 50 years. See the chart below copied from that study showing that the average length of time for firms on the S&P 500 was over 60 years in 1958, but by 2011 had fallen to less than 20 years. The pace of creative destruction seems to be accelerating

From the same study here’s another chart showing the companies that were deleted from the index between 2001 and 2011 and those that were added.

But I would also add a cautionary note that, because the population of individuals and publicly held business firms is growing, comparing the composition of a fixed number (400) of wealthiest individuals or (500) most successful corporations over time may overstate the increase over time in the rate of turnover, any group of fixed numerical size becoming a smaller percentage of the population over time. Even with that caveat, however, what this tells me is that there is a lot of variability in the value of capital assets. Wealth grows, but it grows unevenly. Capital is accumulated, but it is also lost.

Does the process of capital accumulation necessarily lead to increasing inequality of wealth and income? Perhaps, but I don’t think that the answer is necessarily determined by the relationship between the real rate of interest and the rate of growth in GDP.

Many people have suggested that an important cause of rising inequality has been the increasing importance of winner-take-all markets in which a few top performers seem to be compensated at very much higher rates than other, only slightly less gifted, performers. This sort of inequality is reflected in widening gaps between the highest and lowest paid participants in a given occupation. In some cases at least, the differences between the highest and lowest paid don’t seem to correspond to the differences in skill, though admittedly skill is often difficult to measure.

This concentration of rewards is especially characteristic of competitive sports, winners gaining much larger rewards than losers. However, because the winner’s return comes, at least in part, at the expense of the loser, the private gain to winning exceeds the social gain. That’s why all organized professional sports engage in some form of revenue sharing and impose limits on spending on players. Without such measures, competitive sports would not be viable, because the private return to improve quality exceeds the collective return from improved quality. There are, of course, times when a superstar like Babe Ruth or Michael Jordan can actually increase the return to losers, but that seems to be the exception.

To what extent other sorts of winner-take-all markets share this intrinsic inefficiency is not immediately clear to me, but it does not seem implausible to think that there is an incentive to overinvest in skills that increase the expected return to participants in winner-take-all markets. If so, the source of inequality may also be a source of inefficiency.

You are obviously correct.

But I think your frame of “other types of capital” is rhetorically weak.

Instead, say because of technology today, “entrepreneurs need less labor AND capital”

Meaning, don’t let “ubermen” be another type of capital. Screw that.

Say instead, there are three players in the game

FIRST AND MORE IMPORTANT: entrepreneurs

then capital

then labor

per Piketty it’s kind of interesting that capital can beat labor – but since they are both losing to entrepreneurs WHO CARES?

But what he outright misses is how fucking desperate capital is to GET to invest in ubermen.

Don’t be nice about it man, you cannot EVER oversell the importance of Jobs, Andreessen, Page – they are not products of capital, they are products of capitalism, and capitalism isn’t about the primacy of capital. Capitalism will always fail unless it rides shotgun to genius.

LikeLike

Regarding the book, a separate point from your theme above:

I haven’t read the book, but infer some frustrations with it based on reading a number of reviews. The main one is that there seems to be lacking a basic, tight macro conceptual accounting framework.

For example, the idea that r > g leads to an expansion of capital ratios assumes (unless otherwise sufficiently qualified) that r is invested. This is a point that Larry Summers made in his review and he was the only one I noticed that made it. And it’s a very basic accounting point. The degree to which it is assumed is central to the type of argument that Picketty makes. And it seems to have been overlooked. This is macro accounting 101 – as a foundation for economic measurement.

The other big one is that I’ve seen nobody hone in on is the fact that financial assets are a reflection of underlying real assets – to some degree. Yet I’ve seen no reference to this basic aspect of potential double accounting (or potential confusion at least) of capital and/or wealth – because the reviews suggest he has comprehensively included both types of assets. Again, the assumed macro accounting framework is critical to the conceptualization of the important ideas in the book. If he’s addressed this adequately, it certainly isn’t a point that has been reinforced in the reviews, and I infer otherwise.

(I’m only inferring this from the reviews I’ve seen.)

LikeLike

Food for thought:

– the main capital I can think of which stays in the hands of somes owners (and even that changes at some horizon) is real estate. Ok, that has a low turn over. But according to this article, the yield of this part is highly surestimated by T. Piketty (basically: it is based on nominal values of housing, and not on rental level, which is the true return of this kind of capital).

– Everybody talks about entrepreneur, capital and labor shares, as if the cost-share theorem was true. But it is not, as soon as production is made under constrains. A key to understand the past two centuries of growth are to be found in energy, I think. Economists clearly undervalue it, historians seem to unveil its role in the past. Next century will confirm or infirm. With energy, all production/captation issues are to be taken completely differently.

LikeLike

Morgan, Capital is usually valuable because it is an embodiment of an idea. How valuable depends on the idea and how well it is executed.

JKH, At some point, we’ll have to read the book ourselves, won’t we?

Adrien, Thanks for the link to the article, I will try to have a look at it.

LikeLike

Piketty does not ignore the heterogeneity of capital. In fact he is at pains to point out that it is precisely because it is heterogenous that the best he can do, when it comes to quantifying the stock of capital, is to express it as a ratio of two money values: the market value of capital and national income.

Nor does he ignore the way new technologies render older capital obsolete. Indeed that fact that it does so is his rationale for arguing, contra Larry Summers, that capital is more readily substituted for labour than econometric studies suggest. (The key point here is that Piketty is thinking in terms of decades; long-run elasticity reflects “the metamorphoses of capital” so we don’t run up against one-man-one-shovel complementarities.)

Nor does he suppose that the 1% live a quiet life. On the contrary, he acknowledges that individuals can make and lose fortunes quickly. That can happen without much change in the distribution of wealth between the top percentile and the rest. If Lord Tomnoddy loses the family fortune playing cards at Boodles, the chances are that the guys who clean him out aren’t paupers themselves. The same goes for the stock exchange.

In short, this is exactly right: “JKH, At some point, we’ll have to read the book ourselves, won’t we?”

LikeLike

Kevin, Thanks for the lesson. Please excuse my laziness, but can you give me a quick explanation of how the relationship between the growth rate of GDP and the real rate of interest fits into Piketty’s thinking, or have I misunderstood what Summers was saying about that in his review?

LikeLike

David, on my reading Piketty has nothing remarkable to say about the determinants of g. It’s the sum of growth in GDP per capita (which depends on productivity) and population growth (which depends on how many kids people want to raise). As for the rate of return on wealth, r, he mentions the usual textbook stuff, about time-preference etc., while acknowledging that it is somewhat vacuous. His book is not about what drives r, g and s; it’s about how they impact inequality. As the philosophers would say, r, s and g are his explanans and distribution is his explanandum.

My sugestion for those who want to know what the book has to say, but don’t want to read it, is this: read Solow’s review carefully and completely ignore everybody else. It’s by far the most faithful synopsis I’ve seen. Here’s the link:

http://www.newrepublic.com/article/117429/capital-twenty-first-century-thomas-piketty-reviewed

LikeLike

It’s a fair point overall on reading the book.

Although connecting the dots on numerous in depth reviews of a popular book one hasn’t read is an interesting exercise. In this case, the dots connect fairly well across enough reviews.

I thought Summers wrote an interesting review that was self-sustaining in expanding on some important ideas – including at least one of the points I referenced.

I’m just reluctant to get the book for the purpose of confirming he (LS) doesn’t know what he’s talking about.

I think that’s a bit of a risky exercise.

P.S.

I read Solow’s review previously and thought it was brilliant.

LikeLike

David, I think that the turnover in the S&P 500 doesn’t really support your point. Looking at the list of companies that exited, an awful lot of them did so because of mergers. I can speak from experience about Pharmacia, which was an extremely successful company. Pfizer bought the company because they wanted to lock in the profits from the shared Celebrex franchise. Pfizer has stayed in the S&P 500, but has massively destroyed capital by shutting down R&D facilities in the UK, in Michigan, and in Connecticut. Though if the tax-avoiding reverse merger with Astra Zeneca goes through, I guess Pfizer will also leave the S&P.

LikeLike

Here’s a short piece by Piketty and Saez from the May issue of Science:

http://www.sciencemag.org/content/344/6186/838.full?sid=7215d795-280a-40ea-9123-8fab4cc388bc

“Great fortunes, aside from being dissipated by deliberate capital consumption, also tend to be eroded by the loss of value through obsolescence, a process that can only be avoided by extreme diversification of holdings or by the exercise of entrepreneurial skill, a skill rarely bequeathed from generation to generation.”

But this doesn’t address the relative size of capital and income shares.

Solow writes: “…Whether the capital share falls or rises depends on whether the rate of return has to fall proportionally more or less than the capital-income ratio rises.

There has been a lot of research around this question within economics, but no definitely conclusive answer has emerged. This suggests that the ultimate effect on the capital share, whichever way it goes, will be small. Piketty opts for an increase in the capital share, and I am inclined to agree with him. Productivity growth has been running ahead of real wage growth in the American economy for the last few decades, with no sign of a reversal, so the capital share has risen and the labor share fallen. Perhaps the capital share will go from about 30 percent to about 35 percent, with whatever challenge to democratic culture and politics that entails.”

Piketty in an interview:

“My bottom line is that the average rate of return for all assets combined is not going to zero. It has been going down a little bit over the past 20 to 30 years because of the rise in the capital-to-income ratio, but it has declined less than the increase in the capital–income ratio, so that the capital share has actually increased.”

http://www.ippr.org/juncture/juncture-interview-thomas-piketty-on-capital-in-the-twenty-first-century

I think most observers agree that this doesn’t *have* to happen. It’s not predetermined. But neither do I think that Summers is necessarily right that “r” will come down enough invevatibly as g slows. Summers writes “most economists would attribute both it and rising inequality to the working out of various forces associated with globalization and technological change.” Maybe those forces will “work themselves out” and then politics and policy will bring down r and raise growth rates.

LikeLike

Inequality started to accelerate when the machines started replacing humans in middle jobs. According to a recent study by the FED, the destruction of middle jobs by automation is accelerating. The new robot oligarchs are here: http://www.digitalcosmology.com/Blog/2014/06/04/the-robot-oligarchs/

Talking about g, r and such is a red herring. The issue is how much we should tax automation before it is too late: http://www.digitalcosmology.com/Blog/2014/06/04/the-robot-oligarchs/

LikeLike

TravisV here from TheMoneyIllusion comments section.

Marc Andreessen had similar thoughts here:

http://hisstoryisbunk.blogspot.com/2014/06/stick-fork-in-piketty.html

LikeLike

Kevin, I wasn’t asking for an explanation of the determinants of r and g, I was asking for an explanation of how relationship between r and g affects the distribution of income and wealth. If r is an average rate of return, but is highly variable across different forms of wealth, shouldn’t that imply a different time path for the distribution of wealth compared to the same r with very little variance? Thanks for the Solow reference. I gave it a quick read. Very interesting, but will have to read it again more carefully.

JKH, I don’t think that Kevin actually said that Summers doesn’t know what he’s talking about, but he can speak for himself. No questions that Solow is a brilliant guy.

David, I also was thinking about the possibility that mergers were responsible for some of the turnover. You are right that there should be an adjustment for companies that left the index as a result of mergers (and also for companies that made it to the index by merging rather than internal growth). But I don’t think we know how much the results would be changed by adjusting for mergers.

Peter K, My point is that the income from capital is not necessarily equal to rate of return on newly invested capital, which seems to be what Piketty is using to infer the income from capital. It is possible that owners of existing capital are not, on average, earning a rate of return that exceeds the growth rate. I don’t say that is the case, just that it seems a theoretical possibility. I think Solow’s statement is correct and could be compatible either with Piketty’s position or with the possibility – that’s all I’m suggesting – that the ongoing destruction of old capital by newly created capital reduces the overall return on capital below that implied by Piketty’s law of an increasing capital share.

Digital Cosmology, Well according to Piketty we are simply reverting back to a trend that was temporarily interrupted in the early and middle 20th century.

Travis, Thanks for the link. You’re right he seems to be making a point similar to mine.

LikeLike