In a recent post, I criticized, perhaps without adequate understanding, some of Thomas Piketty’s arguments about capital in his best-selling book. My main criticism is that Piketty’s argument that. under capitalism, there is an inherent tendency toward increasing inequality, ignores the heterogeneity of capital and the tendency for new capital embodying new knowledge, new techniques, and new technologies to render older capital obsolete. Contrary to the simple model of accumulation on which Piketty relies, the accumulation of capital is not a smooth process; it is a very uneven process, generating very high returns to some owners of capital, but also imposing substantial losses on other owners of capital. The only way to avoid the risk of owning suddenly obsolescent capital is to own the market portfolio. But I conjecture that few, if any, great fortunes have been amassed by investing in the market portfolio, and (I further conjecture) great fortunes, once amassed, are usually not liquidated and reinvested in the market portfolio, but continue to be weighted heavily in fairly narrow portfolios of assets from which those great fortunes grew. Great fortunes, aside from being dissipated by deliberate capital consumption, also tend to be eroded by the loss of value through obsolescence, a process that can only be avoided by extreme diversification of holdings or by the exercise of entrepreneurial skill, a skill rarely bequeathed from generation to generation.

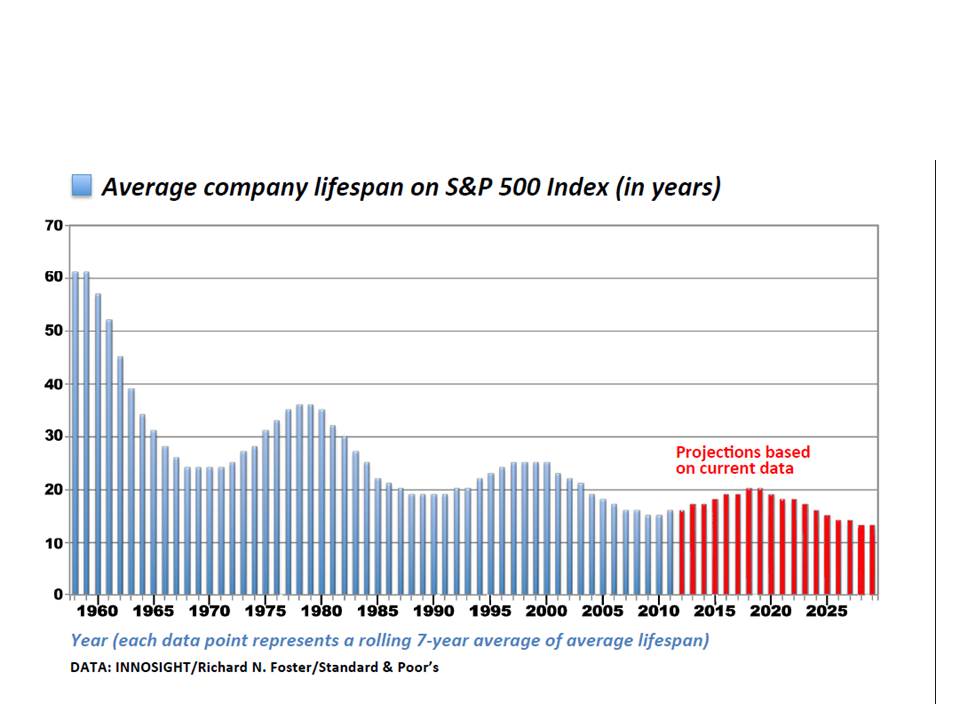

Applying this insight, Larry Summers pointed out in his review of Piketty’s book that the rate of turnover in the Forbes list of the 400 wealthiest individuals between 1982 and 2012 was much higher than the turnover predicted by Piketty’s simple accumulation model. Commenting on my post (in which I referred to Summers’s review), Kevin Donoghue objected that Piketty had criticized the Forbes 400 as a measure of wealth in his book, so that Piketty would not necessarily accept Summers’ criticism based on the Forbes 400. Well, as an alternative, let’s have a look at the S&P 500. I just found this study of the rate of turnover in the 500 firms making up the S&P 500, showing that the rate of turnover in the composition of the S&P 500 has been increased greatly over the past 50 years. See the chart below copied from that study showing that the average length of time for firms on the S&P 500 was over 60 years in 1958, but by 2011 had fallen to less than 20 years. The pace of creative destruction seems to be accelerating

From the same study here’s another chart showing the companies that were deleted from the index between 2001 and 2011 and those that were added.

But I would also add a cautionary note that, because the population of individuals and publicly held business firms is growing, comparing the composition of a fixed number (400) of wealthiest individuals or (500) most successful corporations over time may overstate the increase over time in the rate of turnover, any group of fixed numerical size becoming a smaller percentage of the population over time. Even with that caveat, however, what this tells me is that there is a lot of variability in the value of capital assets. Wealth grows, but it grows unevenly. Capital is accumulated, but it is also lost.

Does the process of capital accumulation necessarily lead to increasing inequality of wealth and income? Perhaps, but I don’t think that the answer is necessarily determined by the relationship between the real rate of interest and the rate of growth in GDP.

Many people have suggested that an important cause of rising inequality has been the increasing importance of winner-take-all markets in which a few top performers seem to be compensated at very much higher rates than other, only slightly less gifted, performers. This sort of inequality is reflected in widening gaps between the highest and lowest paid participants in a given occupation. In some cases at least, the differences between the highest and lowest paid don’t seem to correspond to the differences in skill, though admittedly skill is often difficult to measure.

This concentration of rewards is especially characteristic of competitive sports, winners gaining much larger rewards than losers. However, because the winner’s return comes, at least in part, at the expense of the loser, the private gain to winning exceeds the social gain. That’s why all organized professional sports engage in some form of revenue sharing and impose limits on spending on players. Without such measures, competitive sports would not be viable, because the private return to improve quality exceeds the collective return from improved quality. There are, of course, times when a superstar like Babe Ruth or Michael Jordan can actually increase the return to losers, but that seems to be the exception.

To what extent other sorts of winner-take-all markets share this intrinsic inefficiency is not immediately clear to me, but it does not seem implausible to think that there is an incentive to overinvest in skills that increase the expected return to participants in winner-take-all markets. If so, the source of inequality may also be a source of inefficiency.