UPDATE: I’m re-upping my introductory blog post, which I posted ten years ago toady. It’s been a great run for me, and I hope for many of you, whose interest and responses have motivated to keep it going. So thanks to all of you who have read and responded to my posts. I’m adding a few retrospective comments and making some slight revisions along the way. In addition to new posts, I will be re-upping some of my old posts that still seem to have relevance to the current state of our world.

What the world needs now, with apologies to the great Burt Bachrach and Hal David, is, well, another blog. But inspired by the great Ralph Hawtrey and the near great Scott Sumner, I decided — just in time for Scott’s return to active blogging — to raise another voice on behalf of a monetary policy actively seeking to promote recovery from what I call the Little Depression, instead of the monetary policy we have now: waiting for recovery to arrive on its own. Just like the Great Depression, our Little Depression was caused mainly by overly tight money in an environment of over-indebtedness and financial fragility, and was then allowed to deepen and become entrenched by monetary authorities unwilling to commit themselves to a monetary expansion aimed at raising prices enough to make business expansion profitable.

That was the lesson of the Great Depression. Unfortunately that lesson, for reasons too complicated to go into now, was never properly understood, because neither Keynesians nor Monetarists had a fully coherent understanding of what happened in the Great Depression. Although Ralph Hawtrey — called by none other than Keynes “his grandparent in the paths of errancy,” and an early, but unacknowledged, progenitor of Chicago School Monetarism — had such an understanding, Hawtrey’s contributions were overshadowed and largely ignored, because of often irrelevant and misguided polemics between Keynesians and Monetarists and Austrians. One of my goals for this blog is to bring to light the many insights of this perhaps most underrated — though competition for that title is pretty stiff — economist of the twentieth century. I have discussed Hawtrey’s contributions in my book on free banking and in a paper published years ago in Encounter and available here. Patrick Deutscher has written a biography of Hawtrey.

What deters businesses from expanding output and employment in a depression is lack of demand; they fear that if they do expand, they won’t be able to sell the added output at prices high enough to cover their costs, winding up with redundant workers and having to engage in costly layoffs. Thus, an expectation of low demand tends to be self-fulfilling. But so is an expectation of rising prices, because the additional output and employment induced by expectations of rising prices will generate the demand that will validate the initial increase in output and employment, creating a virtuous cycle of rising income, expenditure, output, and employment.

The insight that “the inactivity of all is the cause of the inactivity of each” is hardly new. It was not the discovery of Keynes or Keynesian economics; it is the 1922 formulation of Frederick Lavington, another great, but underrated, pre-Keynesian economist in the Cambridge tradition, who, in his modesty and self-effacement, would have been shocked and embarrassed to be credited with the slightest originality for that statement. Indeed, Lavington’s dictum might even be understood as a restatement of Say’s Law, the bugbear of Keynes and object of his most withering scorn. Keynesian economics skillfully repackaged the well-known and long-accepted idea that when an economy is operating with idle capacity and high unemployment, any increase in output tends to be self-reinforcing and cumulative, just as, on the way down, each reduction in output is self-reinforcing and cumulative.

But at least Keynesians get the point that, in a depression or deep recession, individual incentives may not be enough to induce a healthy expansion of output and employment. Aggregate demand can be too low for an expansion to get started on its own. Even though aggregate demand is nothing but the flip side of aggregate supply (as Say’s Law teaches), if resources are idle for whatever reason, perceived effective demand is deficient, diluting incentives to increase production so much that the potential output expansion does not materialize, because expected prices are too low for businesses to want to expand. But if businesses can be induced to expand output, more than likely, they will sell it, because (as Say’s Law teaches) supply usually does create its own demand.

[Comment after 10 years: In a comment, Rowe asked why I wrote that Say’s Law teaches that supply “usually” creates its own demand. At that time, I responded that I was just using “usually” as a weasel word. But I subsequently realized (and showed in a post last year) that the standard proofs of both Walras’s Law and Say’s Law are defective for economies with incomplete forward and state-contingent markets. We actually know less than we once thought we did!]

Keynesians mistakenly denied that, by creating price-level expectations consistent with full employment, monetary policy could induce an expansion of output even in a depression. But at least they understood that the private economy can reach an impasse with price-level expectations too low to sustain full employment. Fiscal policy may play a role in remedying a mismatch between expectations and full employment, but fiscal policy can only be as effective as monetary policy allows it to be. Unfortunately, since the downturn of December 2007, monetary policy, except possibly during QE1 and QE2, has consistently erred on the side of uneasiness.

With some unfortunate exceptions, however, few Keynesians have actually argued against monetary easing. Rather, with some honorable exceptions, it has been conservatives who, by condemning a monetary policy designed to provide incentives conducive to business expansion, have helped to hobble a recovery led by the private sector rather than the government which they profess to want. It is not my habit to attribute ill motives or bad faith to people whom I disagree with. One of the finest compliments ever paid to F. A. Hayek was by Joseph Schumpeter in his review of The Road to Serfdom who chided Hayek for “politeness to a fault in hardly ever attributing to his opponents anything but intellectual error.” But it is a challenge to come up with a plausible explanation for right-wing opposition to monetary easing.

[Comment after 10 years: By 2011 when this post was written, right-wing bad faith had already become too obvious to ignore, but who could then have imagined where the willingness to resort to bad faith arguments without the slightest trace of compunction would lead them and lead us.]

In condemning monetary easing, right-wing opponents claim to be following the good old conservative tradition of supporting sound money and resisting the inflationary proclivities of Democrats and liberals. But how can claims of principled opposition to inflation be taken seriously when inflation, by every measure, is at its lowest ebb since the 1950s and early 1960s? With prices today barely higher than they were three years ago before the crash, scare talk about currency debasement and future hyperinflation reminds me of Ralph Hawtrey’s famous remark that warnings that leaving the gold standard during the Great Depression would cause runaway inflation were like crying “fire, fire” in Noah’s flood.

The groundlessness of right-wing opposition to monetary easing becomes even plainer when one recalls the attacks on Paul Volcker during the first Reagan administration. In that episode President Reagan and Volcker, previously appointed by Jimmy Carter to replace the feckless G. William Miller as Fed Chairman, agreed to make bringing double-digit inflation under control their top priority, whatever the short-term economic and political costs. Reagan, indeed, courageously endured a sharp decline in popularity before the first signs of a recovery became visible late in the summer of 1982, too late to save Reagan and the Republicans from a drubbing in the mid-term elections, despite the drop in inflation to 3-4 percent. By early 1983, with recovery was in full swing, the Fed, having abandoned its earlier attempt to impose strict Monetarist controls on monetary expansion, allowed the monetary aggregates to grow at unusually rapid rates.

However, in 1984 (a Presidential election year) after several consecutive quarters of GDP growth at annual rates above 7 percent, the Fed, fearing a resurgence of inflation, began limiting the rate of growth in the monetary aggregates. Reagan’s secretary of the Treasury, Donald Regan, as well as a variety of outside Administration supporters like Arthur Laffer, Larry Kudlow, and the editorial page of the Wall Street Journal, began to complain bitterly that the Fed, in its preoccupation with fighting inflation, was deliberately sabotaging the recovery. The argument against the Fed’s tightening of monetary policy in 1984 was not without merit. But regardless of the wisdom of the Fed tightening in 1984 (when inflation was significantly higher than it is now), holding up the 1983-84 Reagan recovery as the model for us to follow now, while excoriating Obama and Bernanke for driving inflation all the way up to 1 percent, supposedly leading to currency debauchment and hyperinflation, is just a bit rich. What, I wonder, would Hawtrey have said about that?

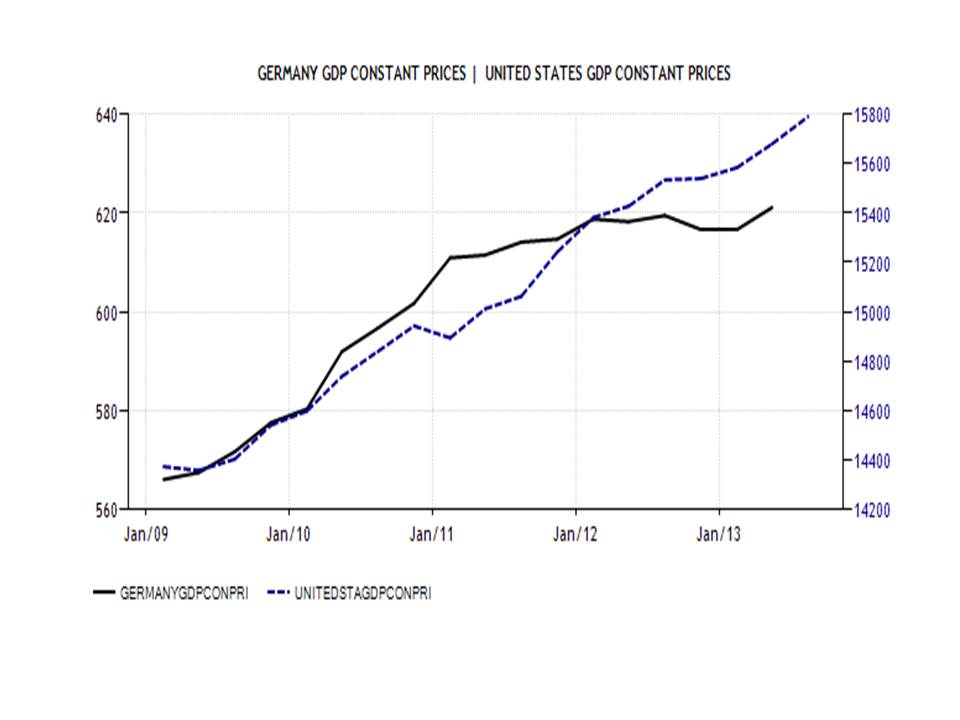

In my next posting I will look a little more closely at some recent comparisons between the current non-recovery and recoveries from previous recessions, especially that of 1983-84.