Last week I was struggling to cut and paste my 11-part series on Hawtrey’s Good and Bad Trade into the paper on that topic that I am scheduled to present next week at the Southern Economic Association meetings in Tampa Florida, completing the task just before coming down with a cold which has kept me from doing anything useful since last Thursday. But I was at least sufficiently aware of my surroundings to notice another flurry of interest in quantitative easing, presumably coinciding with Janet Yellen’s testimony at the hearings conducted by the Senate Banking Committee about her nomination to succeed Ben Bernanke as Chairman of Federal Reserve Board.

In my cursory reading of the latest discussions, I didn’t find a lot that has not already been said, so I will take that as an opportunity to restate some points that I have previously made on this blog. But before I do that, I can’t help observing (not for the first time either) that the two main arguments made by critics of QE do not exactly coexist harmoniously with each other. First, QE is ineffective; second it is dangerous. To be sure, the tension between these two claims about QE does not prove that both can’t be true, and certainly doesn’t prove that both are wrong. But the tension might at least have given a moment’s pause to those crying that Quantitative Easing, having failed for five years to accomplish anything besides enriching Wall Street and taking bread from the mouths of struggling retirees, is going to cause the sky to fall any minute.

Nor, come to think of it, does the faux populism of the attack on a rising stock market and of the crocodile tears for helpless retirees living off the interest on their CDs coexist harmoniously with the support by many of the same characters opposing QE (e.g., Freedomworks, CATO, the Heritage Foundation, and the Wall Street Journal editorial page) for privatizing social security via private investment accounts to be invested in the stock market, the argument being that the rate of return on investing in stocks has historically been greater than the rate of return on payments into the social security system. I am also waiting for an explanation of why abused pensioners unhappy with the returns on their CDs can’t cash in the CDs and buy dividend-paying-stocks? In which charter of the inalienable rights of Americans, I wonder, does one find it written that a perfectly secure real rate of interest of not less than 2% on any debt instrument issued by the US government shall always be guaranteed?

Now there is no denying that what is characterized as a massive program of asset purchases by the Federal Reserve System has failed to stimulate a recovery comparable in strength to almost every recovery since World War II. However, not even the opponents of QE are suggesting that the recovery has been weak as a direct result of QE — that would be a bridge too far even for the hard money caucus — only that whatever benefits may have been generated by QE are too paltry to justify its supposedly bad side-effects (present or future inflation, reduced real wages, asset bubbles, harm to savers, enabling of deficit-spending, among others). But to draw any conclusion about the effects of QE, you need some kind of a baseline of comparison. QE opponents therefore like to use previous US recoveries, without the benefit of QE, as their baseline.

But that is not the only baseline available for purposes of comparison. There is also the Eurozone, which has avoided QE and until recently kept interest rates higher than in the US, though to be sure not as high as US opponents of QE (and defenders of the natural rights of savers) would have liked. Compared to the Eurozone, where nominal GDP has barely risen since 2010, and real GDP and employment have shrunk, QE, which has been associated with nearly 4% annual growth in US nominal GDP and slightly more than 2% annual growth in US real GDP, has clearly outperformed the eurozone.

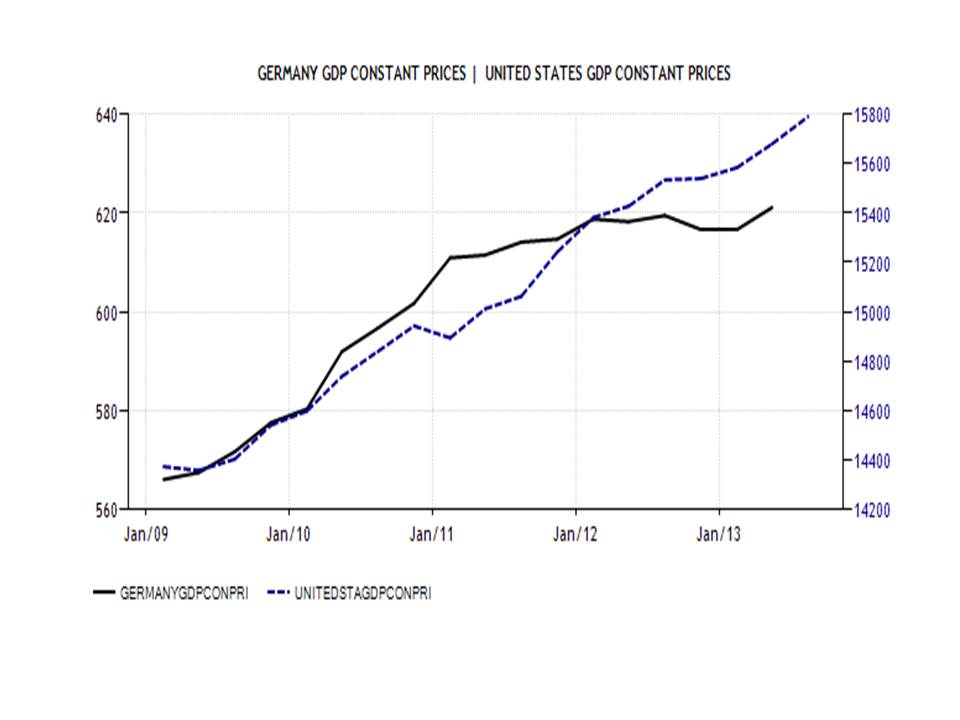

Now maybe you don’t like the Eurozone, as it includes all those dysfunctional debt-ridden southern European countries, as a baseline for comparison. OK, then let’s just do a straight, head-to-head matchup between the inflation-addicted US and solid, budget-balancing, inflation-hating Germany. Well that comparison shows (see the chart below) that since 2011 US real GDP has increased by about 5% while German real GDP has increased by less than 2%.

So it does seem possible that, after all, QE and low interest rates may well have made things measurably better than they would have otherwise been. But don’t expect to opponents of QE to acknowledge that possibility.

Of course that still leaves the question on the table, why has this recovery been so weak? Well, Paul Krugman, channeling Larry Summers, offered a demographic hypothesis in his column Monday: that with declining population growth, there have been diminishing investment opportunities, which, together with an aging population, trying to save enough to support themselves in their old age, causes the supply of savings to outstrip the available investment opportunities, driving the real interest rate down to zero. As real interest rates fall, the ability of the economy to tolerate deflation — or even very low inflation — declines. That is a straightforward, and inescapable, implication of the Fisher equation (see my paper “The Fisher Effect Under Deflationary Expectations”).

So, if Summers and Krugman are right – and the trend of real interest rates for the past three decades is not inconsistent with their position – then we need to rethink revise upwards our estimates of what rate of inflation is too low. I will note parenthetically, that Samuel Brittan, who has been for decades just about the most sensible economic journalist in the world, needs to figure out that too little inflation may indeed be a bad thing.

But this brings me back to the puzzling question that causes so many people to assume that monetary policy is useless. Why have trillions of dollars of asset purchases not generated the inflation that other monetary expansions have generated? And if all those assets now on the Fed balance sheet haven’t generated inflation, what reason is there to think that the Fed could increase the rate of inflation if that is what is necessary to avoid chronic (secular) stagnation?

The answer, it seems to me is the following. If everyone believes that the Fed is committed to its inflation target — and not even the supposedly dovish Janet Yellen, bless her heart, has given the slightest indication that she favors raising the Fed’s inflation target, a target that, recent experience shows, the Fed is far more willing to undershoot than to overshoot – then Fed purchases of assets with currency are not going to stimulate additional private spending. Private spending, at or near the zero lower bound, are determined largely by expectations of future income and prices. The quantity of money in private hands, being almost costless to hold, is no longer a hot potato. So if there is no desire to reduce excess cash holdings, the only mechanism by which monetary policy can affect private spending is through expectations. But the Fed, having succeeded in anchoring inflation expectations at 2%, has succeeded in unilaterally disarming itself. So economic expansion is constrained by the combination of a zero real interest rate and expected inflation held at or below 2% by a political consensus that the Fed, even if it were inclined to, is effectively powerless to challenge.

Scott Sumner calls this monetary offset. I don’t think that we disagree much on the economic analysis, but it seems to me that he overestimates the amount of discretion that the Fed can actually exercise over monetary policy. Except at the margins, the Fed is completely boxed in by a political consensus it dares not question. FDR came into office in 1933, and was able to effect a revolution in monetary policy within his first month in office, thereby saving the country and Western Civilization. Perhaps Obama had an opportunity to do something similar early in his first term, but not any more. We are stuck at 2%, but it is no solution.

Dear Dr. Glasner,

This was a great post but I am not sure that just to make a simple comparison with the Real GDP trend of Germany and USA in order to simply make an argument for QE, the argument seems rather simplistic and unconvincing there might be other real economic forces specially in the supply side that might make the case for a faster growth in the US other than just QE. However I do believe that QE had a small positive effect the first 2 times until it marginal utility equalized its cost. I read the paper of Sumner you linked, about “monetary offset” and I think his argument is very convincing, and this leads me to ask you a question: –so if I take the argument of Sumner in saying that Fiscal stimulus is institutionally limited and its impact constrained by the current system in which the Fed commits itself to keep inflation under a limit and at the same time Fed interventions and I take your argument in this post that monetary policy is itself self limited by the anchored expectation regime the Fed successfully created, how can we solve this problem? either the Fed allow more inflation and brakes the anchor or government makes substantial and radical supply side reforms seems to me the two possibilities, any thoughts on this?, many thanks and keep enlighten us with your posts

LikeLike

Excellent blogging—and the Fed too often signals it is fine with far less than 2 percent inflation. Some FOMC members rhapsodize about deflation.

We will hit ZLB early in next recession…the United States of Japan…

LikeLike

The calls that QE is dangerous are easily explained by this:

The whole aim of practical politics is to keep the populace alarmed (and hence clamorous to be led to safety) by menacing it with an endless series of hobgoblins, all of them imaginary.

H. L. Mencken

LikeLike

David,

I disagree with everything you say but your conclusion. QE is dangerous and ineffective for a few reasons. First, it shortens the duration of government (consolidated) liabilities. If it continues for a few years, which it well might given its ineffectiveness, QE could leave the consolidated balance sheet mostly funded at the short-term IOR. Implications? The U.S. taxpayer is much more exposed to a future increase in rates; institutionally, it also raises the possibility that the Fed will attempt to avoid visible losses by delaying rate increases. Both have implications for deficits and inflation.

Second, QE is dangerous because it aligns speculator strategies along the carry/frontrunning trade. The effect of this alignment is a homogeneity in speculator balance sheets. This homogeneity results in a fragile system vulnerable to shock and panic once QE begins to unwind. BTW, this sort of analysis uses complexity theory as its guide.

Third, QE is dangerous because it is seen by market participants as propping up the prices of legacy assets. This reduces capital mobility and economy-wide returns, and depresses investment.

All that said, I very much agree with your conclusion. For QE to be effective in the way it is designed, the Fed must risk un-anchoring inflation expectations. There is no free lunch. Instead, there is a trade-off between higher nominal growth and the risk of accelerating inflation.

LikeLike

“Now maybe you don’t like the Eurozone, as it includes all those dysfunctional debt-ridden southern European countries, as a baseline for comparison. OK, then let’s just do a straight, head-to-head matchup between the inflation-addicted US and solid, budget-balancing, inflation-hating Germany.”

However, I can see some people claiming that Germany’s worse economics performance since 2011Q1 is attributable precisely to her fiscal fastidiousness. There is however ample reason to believe that is not the case. The following is the percent change in the real general government consumption expenditure between 2009Q4 and 2013Q2 (except as noted):

1.Malta 13.6

2.Luxembourg 10.0

3.France 4.5 2013Q3

4.Estonia 4.2

5.Germany 3.5

6.Belgium 2.9

7.Finland 2.0

8.Austria 0.5 2013Q3

Euro Area (-0.6)

9.Netherland (-2.4) 2013Q3

10.Slovenia (-4.1)

11.Italy (-4.6)

12.Spain (-5.1)

United States (-5.3) 2013Q3

13.Slovakia (-6.0)

14.Ireland (-10.6)

15.Portugal (-11.2)

16.Cyprus (-17.0)

17.Greece (-20.0) 2011Q1

http://appsso.eurostat.ec.europa.eu/nui/show.do?query=BOOKMARK_DS-055780_QID_-3AE25C01_UID_-3F171EB0&layout=TIME,C,X,0;GEO,L,Y,0;S_ADJ,L,Z,0;UNIT,L,Z,1;INDIC_NA,L,Z,2;INDICATORS,C,Z,3;&zSelection=DS-055780S_ADJ,SWDA;DS-055780INDIC_NA,P3_S13;DS-055780INDICATORS,OBS_FLAG;DS-055780UNIT,MIO_NAC_CLV2005;&rankName1=INDIC-NA_1_2_-1_2&rankName2=S-ADJ_1_2_-1_2&rankName3=INDICATORS_1_2_-1_2&rankName4=UNIT_1_2_-1_2&rankName5=TIME_1_0_0_0&rankName6=GEO_1_2_0_1&sortC=ASC_-1_FIRST&rStp=&cStp=&rDCh=&cDCh=&rDM=true&cDM=true&footnes=false&empty=false&wai=false&time_mode=NONE&time_most_recent=false&lang=EN&cfo=%23%23%23%2C%23%23%23.%23%23%23

This information also stands in stark contrast to the claims by Austrian Economic Theorists, Monetary Realists. Modern Monetary Theorists and others that there has been absolutely no fiscal consolidation taking place in the United States.

LikeLike

Great essay.

Of course there was always humor in the juxtaposition of claims that QE would be disastrous and claims that it would be impotent, especially when these emanated from a single individual (Stephen Williamson, for one). But the two claims hardly appear symmetrical these days. Diviners of QE’s dangers must trade in increasingly arcane conjectures and prognostications. But skeptics need only point to the lack of any significant improvement in inflation, growth, or employment. So the reasonable discussion would seem to be, not whether curtailment of QE is urgent — probably not, since even a skeptic must allow that it might be helping a little bit — but whether other, even less conventional policies might be more effective. It’s true that this discussion might be difficult absent a dramatic political change. But the same would have seemed true of monthly $65 billion asset purchases back in 2009…

(Parenthetically, I think the least helpful development of the past year or so has been the media’s now-kneejerk tendency to call QE “the Fed’s stimulus”. This can do no good either to the cause of loose money or to the cause of fiscal expansion.)

LikeLike

g2, You are certainly right that a simple comparison between the real GDP growth in Germany and the US over the past 2 years can’t really prove anything about whether QE has been helpful. But it is a data point, and, therefore, worth taking into account in assessing the totality of the evidence on the efficacy of QE. About your question about what policy strategy would help promote a stronger recovery, my recommendation has been that the monetary authorities should announce that they are trying to raise the price level of the price level path by about 10 percent over the current path. Scott Sumner would phrase it in terms of an 10 percent increase in the NGDP path, and I have no quarrel with that way of describing it – the idea is basically the same. I think that supply-side reforms should be evaluated on their merits as supply-side reforms not as countercyclical policies.

Benjamin, Thanks. Two percent inflation (or slightly less!) is a convenient phrase for them to hide behind, isn’t it? On the other hand, I will say that Bernanke just made a speech which I heard part of on Cspan radio, arguing cogently that Fed policy statements about tapering asset purchases have been consistently misconstrued since June. In the current environment, I thought that the speech was a rather admirable admission that the Fed had not communicated its strategy clearly enough.

Floccina, Indeed! I wonder what Mencken would make of the cast of characters now on stage.

Diego, If we consolidate the Fed and Treasury balance sheets (not strictly correct, but not a bad approximation), the profits from interest saved on long-term bonds can be used to cover the interest rate risk at the short-end. Why is that not a prudent strategy? I agree that the Fed should not base its future policy decisions on concerns about its balance sheet. That doesn’t seem to me to be a reason for the Fed not to follow a policy today that is otherwise appropriate. I only vaguely grasp your second point, and would appreciate seeing it spelled out in greater detail. Specifically which legacy assets are you referring to? Mortgage-backed securities? Anything else? I am glad to see that we have at least finally found something to agree about.

Mark, Thanks for doing all these calculations. Your diligence is quite remarkable.

Will, Thanks. The difference is that $65 billion in asset purchases is not something that the public can relate to. That’s why opponents try to describe it as a bailout for the banks or as subsidy to Wall Street. Changing the inflation target is something that everybody would immediately understand (if only superficially), and, unfortunately, be shocked by.

LikeLike

Diego Espinosa,

“First, it shortens the duration of government (consolidated) liabilities. If it continues for a few years, which it well might given its ineffectiveness, QE could leave the consolidated balance sheet mostly funded at the short-term IOR. Implications? The U.S. taxpayer is much more exposed to a future increase in rates; institutionally, it also raises the possibility that the Fed will attempt to avoid visible losses by delaying rate increases. Both have implications for deficits and inflation.”

This claim seems rife with contradictions. The only coherent reason for why US interest rates may rise if if the economy recovers in which case government revenue will rise and paying the net interest costs will not be much of an issue. As for the effect on the Fed’s balance sheet, losses are only an issue if one were concerned about the Fed’s ability to shrink the monetary base, in which case presumably inflation is the problem and in which case we must assume that the economy has recovered. in short if QE is ineffective there will be no interest rate increase. If QE is effective then these issues are probably trivial thanks to the recovery of the economy.

“Second, QE is dangerous because it aligns speculator strategies along the carry/frontrunning trade. The effect of this alignment is a homogeneity in speculator balance sheets. This homogeneity results in a fragile system vulnerable to shock and panic once QE begins to unwind. BTW, this sort of analysis uses complexity theory as its guide.”

If investor balance sheets are homogeneous this should lead to greater financial market volatility (Unlike a sand pile, markets are in constant motion and consequently homogeneity is reasonably easy to detect.) I’ve been tracking financial market volatility by a number of measures throughout the course of the QE programs. I have divided up the periods into Precrisis (before 9/10/2008) , PreQE1, QE1, PreQE2, QE2, PreMEP (Maturity Extension Program), MEP and QE3. What I find is that US stock market volatility was lower during QE2 and QE3 than during the precrisis period, and that bond market volatility has been lower during MEP and QE3 than during the precrisis period.

In contrast, in the Euro Area, where there has been no QE, I find that stock market volatility only dropped to below precrisis levels during QE3 and that it has been consistently above US levels since the end of QE1. With respect to bond market volatility, I find that it has been above precrisis levels throughout, and that it has been consistently above US levels since the end of QE2.

In short I find the exact opposite of what you are claiming. US financial market volatility has dropped with each succeeding QE program to very low levels. In contrast, in the Euro Area, where there has been no QE, financial market volatility has been consistently higher than US volatility, depending on the type of asset, since 2010-11.

“Third, QE is dangerous because it is seen by market participants as propping up the prices of legacy assets. This reduces capital mobility and economy-wide returns, and depresses investment.”

This claim is especially strange since it particularly applies to the Euro Area, where they have done no QE, and not to the US.

The issue of Euro Area financial sector legacy assets has been prominent in the news since early last year as the exact mechanics of a proposed banking union has been discussed. The existence of these assets exacerbates the sovereign debt crisis through bank-sovereign links.

Traditionally one of the approaches to looking at the issue of capital mobility is through real long-term interest rates. In fact the differences in real long-term interest rates that have grown in the Euro Area since the recession have been credited precisely to the poor condition of the financial sector in peripheral countries. This has also been highlighted as evidence of a broken monetary transmission mechanism within the Euro Area.

Another approach to looking at the issue of capital mobility is the correlation between savings and investment rates. If capital is mobile there should be no correlation between the two ratios. And in fact the correlation between gross savings and fixed capital formation in the Euro Area was statistically insignificant just prior to the recession, but it is now highly significant with the correlation coefficient at a level more consistent with states that are not members of the same currency area. It’s very likely that this sharp decline in capital mobility within the Euro Area has inordinately depressed aggregate investment.

And in fact that is what we seem to find. The following is the percent change in the real fixed capital formation between 2010Q1 and 2013Q2 (except as noted):

1.Estonia 60.9

2.Luxembourg 23.3

United States 16.1 2013Q3

3.Austria 10.2 2013Q3

4.Germany 9.4

5.Finland 8.3

6.Slovakia 2.8

7.France 0.9 2013Q3

8.Belgium 0.9

9.Netherlands (-2.9) 2013Q3

Euro Area (-4.6)

10.Italy (-14.5)

11.Slovenia (-18.2)

12.Greece (-19.2) 2011Q1

13.Spain (-19.7)

14.Ireland (-21.2)

15.Malta (-22.4)

16.Portugal (-30.8)

17.Cyprus (-42.5)

http://appsso.eurostat.ec.europa.eu/nui/show.do?query=BOOKMARK_DS-055780_QID_6FA8C7B_UID_-3F171EB0&layout=TIME,C,X,0;GEO,L,Y,0;S_ADJ,L,Z,0;UNIT,L,Z,1;INDIC_NA,L,Z,2;INDICATORS,C,Z,3;&zSelection=DS-055780S_ADJ,SWDA;DS-055780INDIC_NA,P51;DS-055780INDICATORS,OBS_FLAG;DS-055780UNIT,MIO_NAC_CLV2005;&rankName1=INDIC-NA_1_2_-1_2&rankName2=S-ADJ_1_2_-1_2&rankName3=INDICATORS_1_2_-1_2&rankName4=UNIT_1_2_-1_2&rankName5=TIME_1_0_0_0&rankName6=GEO_1_2_0_1&sortC=ASC_-1_FIRST&rStp=&cStp=&rDCh=&cDCh=&rDM=true&cDM=true&footnes=false&empty=false&wai=false&time_mode=NONE&time_most_recent=false&lang=EN&cfo=%23%23%23%2C%23%23%23.%23%23%23

LikeLike

David, I must take issue with you excursion into and excoriation of the “faux” populists who support privatization of social security and lament the low nominal/real rates of QE impact on elderly savers. Regardless of the motivation, those two positions are not inconsistent. The main reason for privatizing part or all of a social security account is to move the money into the ownership and control of the individual, not the government under the assumption that the individual will be a better steward over his own (forced) savings. The investment decisions can be made by individuals according to their own needs and risk preferences, rather than the government-determined rate of return. Consistent with this view is that extraordinary government intervention (unconventional monetary policy) is resulting in a government-determined rate of return in many investment options. Nobody is guaranteed a 2% real return as you say, but those who are currently frustrated see the current issue as government-driven, not market driven. No one is guaranteed a certain profit level when they sell their house, but if the government put a price control on what you could sell your house (let’s say to stimulate home sales), you’d be a little ticked. Better to try to justify QE on the other arguments (Hayek’s prevention of a secondary deflation; or a belief that fixed income retirees would be worse off absent QE; ). This detour you took was a little gratuitous.

LikeLike

Dr. Glasner, any comments on these latest post of Dr. Selgin about the issues that I asked you about? a quote here: “I submit these old-fashioned monetarist heresies for the consideration of all those who think that an increased target rate of inflation will help us out of our present economic quagmire.”

here: http://www.freebanking.org/2013/11/20/deja-vu-all-over-again/

and here: http://www.freebanking.org/2013/11/21/four-old-fashioned-monetarist-heresies/

LikeLike

David,

The nature of duration risk is to earn a spread b/t short and long term yields while potentially absorbing a loss caused by an increase in short term yields. One cannot say that the spread “reduces” duration risk. It is part and parcel of it. A mis-match of asset and liability durations on the government’s consolidated balance sheet creates risk, and that risk is borne by the taxpayer.

On legacy assets, yes I referred to those such as MBS, commercial real estate portfolios, housing, etc. Fed policy is explicitly directed at propping up the prices of those assets to what it feels are “equilibrium” levels. If the Fed is wrong about “equilibrium”, this harms capital mobility.

LikeLike

Mark, I agree that interest rates will rise when the economy recovers, so that a scenario that posits an increase in interest rates without assuming that there is a recovery causing rapidly falling deficits (already far below the high levels after the downturn) is suspect. The only other plausible cause of rising interest rates would be a premature move to monetary tightening which is inconsistent with premises of the exercise.

gofx, I am unaware of any legal control over the yields on Treasury issues. Those yields are determined in very liquid auction markets, not by government fiat. The faux populists try to avoid that critical distinction for reasons which are understandable, but nonetheless, unsupportable.

g2, Thanks for drawing my attention to his comments. Actually I do have some comments and, if I can find the time, will try to write a post about them.

Diego, I think the point is that there are a lot of risks that are affecting the tax payer. The biggest risk is that the economy will underperform and not generate sufficient tax revenue to support government spending. Trying to improve the economy by QE is aimed at reducing that risk. Even if the duration risk is increased, total taxpayer risk may be reduced.

LikeLike

David,

You don’t reduce risk by anticipating returns. The two are separate. Otherwise, Countrywide could have simply told regulators:

“Don’t worry about our huge sub-prime bet. We expect to make so much money on it that it actually reduces our overall balance sheet risk.”

Maybe they did tell the regulators that!

LikeLike

“Private spending, at or near the zero lower bound, are determined largely by expectations of future income and prices.”

sholdn’t that be “is” determined largely ?

in any event, if a society like the US or UK polarizes into superwealthy and poor, this argument is less true; the super wealthy, by definition, spend what they want; the poor always spend all they have, by definition.

it is only the middle class that worries about a job next year vs a new car or refinishing the kitchen

PS: I don’t know what your other readers think, but i think you should write less; the first 2.5 paragraphs should have been cut and the whole piece should have been cut and organized to emphasize the title point

LikeLike

Diego, I am not anticipating returns, I am just saying that the risks seem to be offsetting, because the probability of rising real interest rates in a weak economy is very low unless the monetary authority deliberately tries to raise interest rates and that contingency is obviously under the control of the monetary authority. What am I missing?

Ezra, Yes, it should. Thanks for catching that one.

Income is polarizing to a distressing degree, but I think that we are still far away from the situation you describe.

As for editing, I try to edit everything I write, but obviously there is always room for improvement.

LikeLike

David,

In a word, stagflation.

LikeLike

Also, its a matter of time frames. Let’s say QE has worked as it has the past four years. That is, the economy is stuck at 1.8% RGDP growth or so, and the Fed is buying a net one trillion a year of 7-yr equivalent bonds. In four years, the Fed would have around $7tr of 7yr equivalents. That is, they would own most of the government issued or guaranteed duration available to the market. By the way, if a recession intervened in those years, they Fed would likely pick up its purchases and own even more.

So, four years from now, growth finally rises from 2% to 4%. The Fed Funds rate is at zero, and inflation rises to 4%. The Fed raises the FFR to 1%, but with such strongly-negative real rates, inflation accelerates. The FFR goes to 2%, but the Fed is behind the curve and unwilling to force real rates to be positive for a “considerable period”. Inflation accelerates to 5%. A few years later, it hits 10%, and the FFR finally rises to 5%, which leaves the real rate at -5%. The Fed is still unwilling to get ahead of the curve.

Now, I ask you, what is the Fed’s duration loss at $7tr in 7-yr equivalents and the FFR at 5%?

LikeLike

Diego, I just don’t accept that inflation is a realistic possibility unless and until unemployment falls. Under your scenario that growth continues at the current 2% rate for another three or four years, unemployment may slowly drop, perhaps to 6 percent. That would be a terrible outcome, but that is what the future holds, it is very hard to imagine that inflation would rise above 2%. And I would guess that by then, short-term interest rates would have edged up slightly. Under that scenario, I see no reason why the Fed, upon suddenly observing an increase in growth, would be slow to raise interest rates as growth and perhaps upward pricing pressure began to increase. If the Fed is chomping at the bit to raise interest rates under current conditions, why would it hesitate to raise interest rates four years down the road under the conditions that you are assuming? You can always conjure up a disaster if you assume that the Fed acts stupidly. True the Fed has acted stupidly in the past, but I don’t accept that the Fed should not try to reduce unemployment today because it may do something stupid five years from now.

LikeLike

David,

I think you rule out too much. We have had episodes of 4% cpi inflation with 2% growth. Further, today we are in a situation where growth is 2% and the Fed would not dream of raising rates.

Transitively, one could easily imagine a situation in which cpi were 4% and the Fed could not dream of raising rates.

LikeLike

Diego, Yes we have certainly had episodes of 4% inflation and 2% growth. But have we had episodes of 4% inflation and 2% growth starting from 1% inflation and 2% growth and 7+% unemployment without an interval of more rapid growth and reduced unemployment. Not that I can recall.

Why do you say that the Fed what not now dream of raising rates? Ever hear of Charles Plosser, Richard Fisher, Jeffrey Lacker, and Elizabeth George? I think the Fed feels tremendous pressure to raise rates. So far Bernanke and Yellen have resisted it, but I think that they will be happy to be able to raise rates as soon as there is a plausible case to be made for doing so.

LikeLike