Brad Delong has a nice little piece bashing Milton Friedman, an activity that, within reasonable limits, I consider altogether commendable and like to engage in myself from time to time (see here, here, here, here, here , here, here, here, here and here). Citing Barry Eichengreen’s recent book Hall of Mirrors, Delong tries to lay the blame for our long-lasting Little Depression (aka Great Recession) on Milton Friedman and his disciples whose purely monetary explanation for the Great Depression caused the rest of us to neglect or ignore the work of Keynes and Minsky and their followers in explaining the Great Depression.

According to Eichengreen, the Great Depression and the Great Recession are related. The inadequate response to our current troubles can be traced to the triumph of the monetarist disciples of Milton Friedman over their Keynesian and Minskyite peers in describing the history of the Great Depression.

In A Monetary History of the United States, published in 1963, Friedman and Anna Jacobson Schwartz famously argued that the Great Depression was due solely and completely to the failure of the US Federal Reserve to expand the country’s monetary base and thereby keep the economy on a path of stable growth. Had there been no decline in the money stock, their argument goes, there would have been no Great Depression.

This interpretation makes a certain kind of sense, but it relies on a critical assumption. Friedman and Schwartz’s prescription would have worked only if interest rates and what economists call the “velocity of money” – the rate at which money changes hands – were largely independent of one another.

What is more likely, however, is that the drop in interest rates resulting from the interventions needed to expand the country’s supply of money would have put a brake on the velocity of money, undermining the proposed cure. In that case, ending the Great Depression would have also required the fiscal expansion called for by John Maynard Keynes and the supportive credit-market policies prescribed by Hyman Minsky.

I’m sorry, but I find this criticism of Friedman and his followers just a bit annoying. Why? Well, there are a number of reasons, but I will focus on one: it perpetuates the myth that a purely monetary explanation of the Great Depression originated with Friedman.

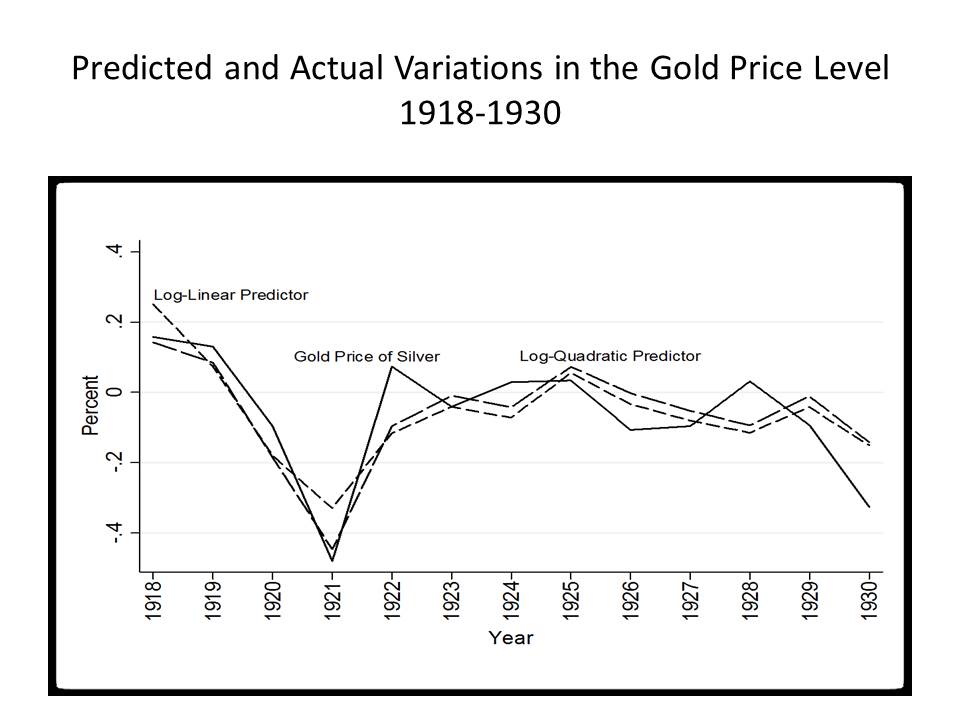

Why is it a myth? Because it wasn’t Friedman who first propounded a purely monetary theory of the Great Depression. Nor did the few precursors, like Clark Warburton, that Friedman ever acknowledged. Ralph Hawtrey and Gustav Cassel did — 10 years before the start of the Great Depression in 1919, when they independently warned that going back on the gold standard at the post-World War I price level (in terms of gold) — about twice the pre-War price level — would cause a disastrous deflation unless the world’s monetary authorities took concerted action to reduce the international monetary demand for gold as countries went back on the gold standard to a level consistent with the elevated post-War price level. The Genoa Monetary Conference of 1922, inspired by the work of Hawtrey and Cassel, resulted in an agreement (unfortunately voluntary and non-binding) that, as countries returned to the gold standard, they would neither reintroduce gold coinage nor keep their monetary reserves in the form of physical gold, but instead would hold reserves in dollar or (once the gold convertibility of sterling was restored) pound-denominated assets. (Ron Batchelder and I have a paper discussing the work of Hawtrey and Casssel on the Great Depression; Doug Irwin has a paper discussing Cassel.)

After the short, but fierce, deflation of 1920-21 (see here and here), when the US (about the only country in the world then on the gold standard) led the world in reducing the price level by about a third, but still about two-thirds higher than the pre-War price level, the Genoa system worked moderately well until 1928 when the Bank of France, totally defying the Genoa Agreement, launched its insane policy of converting its monetary reserves into physical gold. As long as the US was prepared to accommodate the insane French gold-lust by permitting a sufficient efflux of gold from its own immense holdings, the Genoa system continued to function. But in late 1928 and 1929, the Fed, responding to domestic fears about a possible stock-market bubble, kept raising interest rates to levels not seen since the deflationary disaster of 1920-21. And sure enough, a 6.5% discount rate (just shy of the calamitous 7% rate set in 1920) reversed the flow of gold out of the US, and soon the US was accumulating gold almost as rapidly as the insane Bank of France was.

This was exactly the scenario against which Hawtrey and Cassel had been warning since 1919. They saw it happening, and watched in horror while their warnings were disregarded as virtually the whole world plunged blindly into a deflationary abyss. Keynes had some inkling of what was going on – he was an old friend and admirer of Hawtrey and had considerable regard for Cassel – but, for reasons I don’t really understand, Keynes was intent on explaining the downturn in terms of his own evolving theoretical vision of how the economy works, even though just about everything that was happening had already been foreseen by Hawtrey and Cassel.

More than a quarter of a century after the fact, and after the Keynesian Revolution in macroeconomics was well established, along came Friedman, woefully ignorant of pre-Keynesian monetary theory, but determined to show that the Keynesian explanation for the Great Depression was wrong and unnecessary. So Friedman came up with his own explanation of the Great Depression that did not even begin until December 1930 when the Fed allowed the Bank of United States to fail, triggering, in Friedman’s telling, a wave of bank failures that caused the US money supply to decline by a third by 1933. Rather than see the Great Depression as a global phenomenon caused by a massive increase in the world’s monetary demand for gold, Friedman portrayed it as a largely domestic phenomenon, though somehow linked to contemporaneous downturns elsewhere, for which the primary explanation was the Fed’s passivity in the face of contagious bank failures. Friedman, mistaking the epiphenomenon for the phenomenon itself, ignorantly disregarded the monetary theory of the Great Depression that had already been worked out by Hawtrey and Cassel and substituted in its place a simplistic, dumbed-down version of the quantity theory. So Friedman reinvented the wheel, but did a really miserable job of it.

A. C. Pigou, Alfred Marshall’s student and successor at Cambridge, was a brilliant and prolific economic theorist in his own right. In his modesty and reverence for his teacher, Pigou was given to say “It’s all in Marshall.” When it comes to explaining the Great Depression, one might say as well “it’s all in Hawtrey.”

So I agree that Delong is totally justified in criticizing Friedman and his followers for giving such a silly explanation of the Great Depression, as if it were, for all intents and purposes, made in the US, and as if the Great Depression didn’t really start until 1931. But the problem with Friedman is not, as Delong suggests, that he distracted us from the superior insights of Keynes and Minsky into the causes of the Great Depression. The problem is that Friedman botched the monetary theory, even though the monetary theory had already been worked out for him if only he had bothered to read it. But Friedman’s interest in the history of monetary theory did not extend very far, if at all, beyond an overrated book by his teacher Lloyd Mints A History of Banking Theory.

As for whether fiscal expansion called for by Keynes was necessary to end the Great Depression, we do know that the key factor explaining recovery from the Great Depression was leaving the gold standard. And the most important example of the importance of leaving the gold standard is the remarkable explosion of output in the US beginning in April 1933 (surely before expansionary fiscal policy could take effect) following the suspension of the gold standard by FDR and an effective 40% devaluation of the dollar in terms of gold. Between April and July 1933, industrial production in the US increased by 70%, stock prices nearly doubled, employment rose by 25%, while wholesale prices rose by 14%. All that is directly attributable to FDR’s decision to take the US off gold, and devalue the dollar (see here). Unfortunately, in July 1933, FDR snatched defeat from the jaws of victory (or depression from the jaws of recovery) by starting the National Recovery Administration, whose stated goal was (OMG!) to raise prices by cartelizing industries and restricting output, while imposing a 30% increase in nominal wages. That was enough to bring the recovery to a virtual standstill, prolonging the Great Depression for years.

I don’t say that the fiscal expansion under FDR had no stimulative effect in the Great Depression or that the fiscal expansion under Obama in the Little Depression had no stimulative effect, but you can’t prove that monetary policy is useless just by reminding us that Friedman liked to assume (as if it were a fact) that the demand for money is highly insensitive to changes in the rate of interest. The difference between the rapid recovery from the Great Depression when countries left the gold standard and the weak recovery from the Little Depression is that leaving the gold standard had an immediate effect on price-level expectations, while monetary expansion during the Little Depression was undertaken with explicit assurances by the monetary authorities that the 2% inflation target – in the upper direction, at any rate — was, and would forever more remain, sacred and inviolable.