I was pleasantly surprised to receive an email a couple of weeks ago from someone I don’t know, a graduate student in economics at George Mason University, James Caton. He sent me a link to a paper (“Good as Gold?: A Quantitative Analysis of Hawtrey and Cassel’s Theory of Gold Demand and the Gold Price Level During the Interwar Period”) that he recently posted on SSRN. Caton was kind enough to credit me and my co-author Ron Batchelder, as well as Doug Irwin (here and here) and Scott Sumner, for reviving interest in the seminal work of Ralph Hawtrey and Gustav Cassel on the interwar gold standard and the key role in causing the Great Depression played by the process of restoring the gold standard after it had been effectively suspended after World War I began.

The thesis independently, but cooperatively, advanced by Hawtrey and Cassel was that under a gold standard, fluctuations in the gold price level were sensitive to variations in the demand for gold reserves by the central banks. The main contribution of Caton’s paper is to provide econometric evidence of the tight correlation between variations in the total gold holdings of the world’s central banks and the gold price level in the period between the end of World War I (1918) to the start of Great Depression (1930-32). Caton uses a variation on a model used by Scott Sumner in his empirical work on the Great Depression to predict changes in the value of gold, and, hence, changes in the gold price level of commodities. If central banks in the aggregate are adding to their gold reserves at a faster rate than the rate at which the total world stock of gold is growing, then gold would be likely to appreciate, and if central banks are adding to their gold reserves at a slower rate than that at which the world stock is growing, then gold would be likely to depreciate.

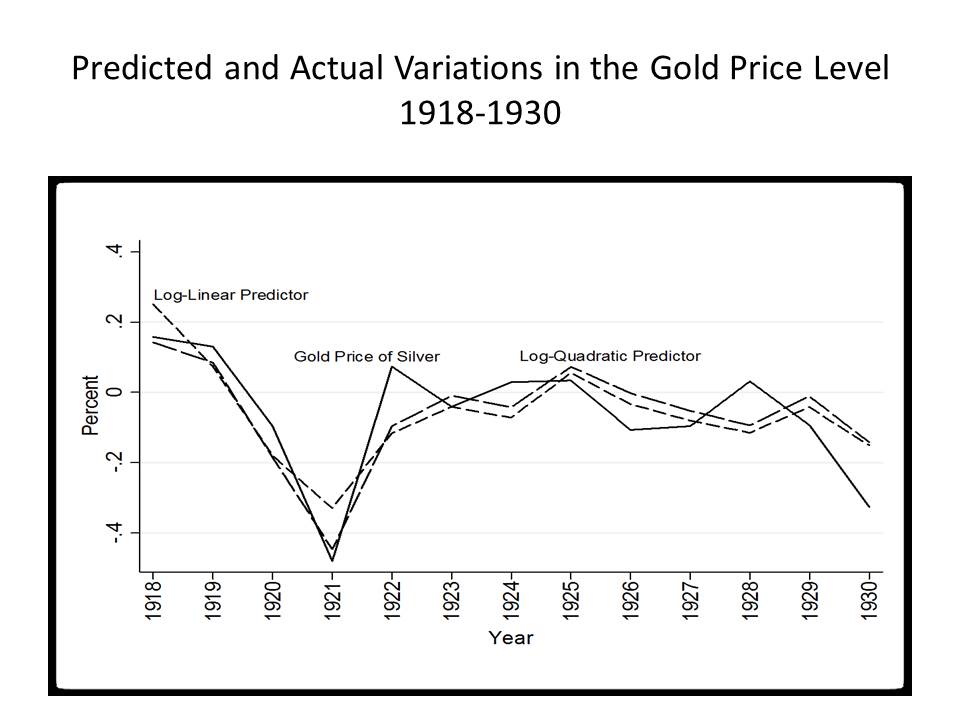

So from the published sources, Caton constructed a time series of international monetary gold holdings and the total world stock of gold from 1918 to 1932 and regressed the international gold price level on the international gold reserve ratio (the ratio of monetary gold reserves to the total world stock of gold). He used two different measures of the world gold price level, the Sauerback-Statist price index and the gold price of silver. Based on his regressions (calculated in both log-linear and log-quadratic forms and separately for the periods 1918-30, 1918-31, 1918-32), he compared the predicted gold price level against both the Sauerback-Statist price index and the gold price of silver. The chart below shows his result for the log-linear regression estimated over the period 1918-30.

Pretty impressive, if you ask me. Have a look yourself.

Let me also mention that Caton’s results also shed important light on the puzzling behavior of the world price level immediately after the end of World War I. Unlike most wars in which the wartime inflation comes to an abrupt end after the end of the war, inflation actually accelerated after the end of the war. The inflation did not actually stop for almost two years after the end of the war, when a huge deflation set in. Caton shows that the behavior of the price level was largely determined by the declining gold holdings of the Federal Reserve after the war ended. Unnerved by the rapid inflation, the Fed finally changed policy, and began accumulating gold rapidly in 1920 by raising the discount rate to an all-time high of 7 percent. Although no other countries were then on the gold standard, other countries, unwilling, for the most part, to allow their currencies to depreciate too much against the dollar, imported US deflation.

Jim is also a blogger. Check out his blog here.

Update: Thanks to commenter Blue Aurora for pointing out that I neglected to provide a link to Jim Caton’s paper. Sorry about that. The link is now embedded.