I was pleasantly surprised to receive an email a couple of weeks ago from someone I don’t know, a graduate student in economics at George Mason University, James Caton. He sent me a link to a paper (“Good as Gold?: A Quantitative Analysis of Hawtrey and Cassel’s Theory of Gold Demand and the Gold Price Level During the Interwar Period”) that he recently posted on SSRN. Caton was kind enough to credit me and my co-author Ron Batchelder, as well as Doug Irwin (here and here) and Scott Sumner, for reviving interest in the seminal work of Ralph Hawtrey and Gustav Cassel on the interwar gold standard and the key role in causing the Great Depression played by the process of restoring the gold standard after it had been effectively suspended after World War I began.

The thesis independently, but cooperatively, advanced by Hawtrey and Cassel was that under a gold standard, fluctuations in the gold price level were sensitive to variations in the demand for gold reserves by the central banks. The main contribution of Caton’s paper is to provide econometric evidence of the tight correlation between variations in the total gold holdings of the world’s central banks and the gold price level in the period between the end of World War I (1918) to the start of Great Depression (1930-32). Caton uses a variation on a model used by Scott Sumner in his empirical work on the Great Depression to predict changes in the value of gold, and, hence, changes in the gold price level of commodities. If central banks in the aggregate are adding to their gold reserves at a faster rate than the rate at which the total world stock of gold is growing, then gold would be likely to appreciate, and if central banks are adding to their gold reserves at a slower rate than that at which the world stock is growing, then gold would be likely to depreciate.

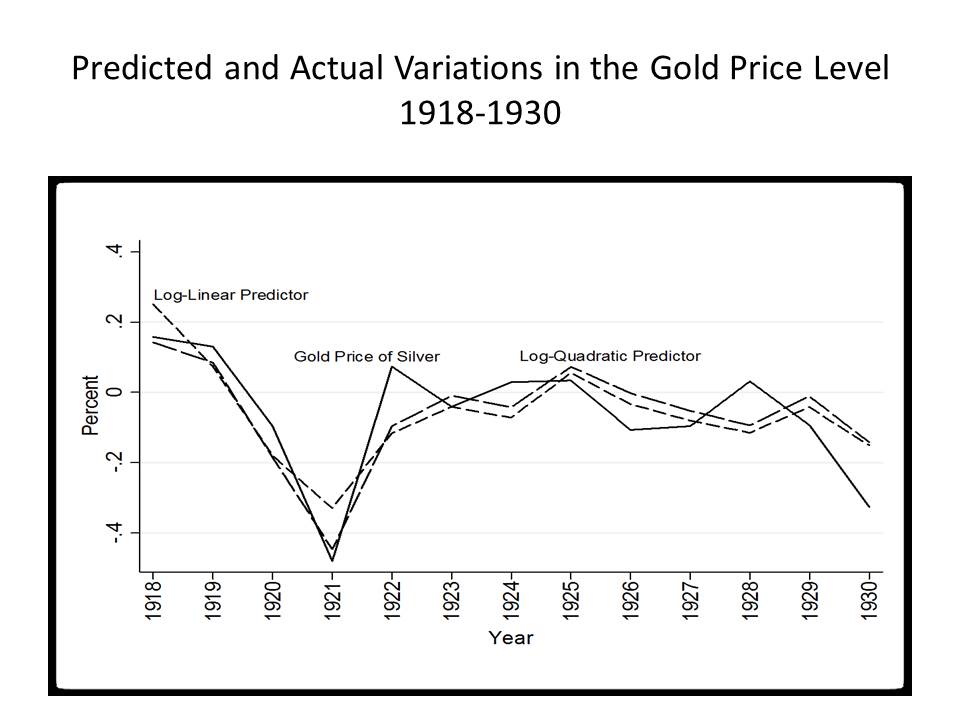

So from the published sources, Caton constructed a time series of international monetary gold holdings and the total world stock of gold from 1918 to 1932 and regressed the international gold price level on the international gold reserve ratio (the ratio of monetary gold reserves to the total world stock of gold). He used two different measures of the world gold price level, the Sauerback-Statist price index and the gold price of silver. Based on his regressions (calculated in both log-linear and log-quadratic forms and separately for the periods 1918-30, 1918-31, 1918-32), he compared the predicted gold price level against both the Sauerback-Statist price index and the gold price of silver. The chart below shows his result for the log-linear regression estimated over the period 1918-30.

Pretty impressive, if you ask me. Have a look yourself.

Let me also mention that Caton’s results also shed important light on the puzzling behavior of the world price level immediately after the end of World War I. Unlike most wars in which the wartime inflation comes to an abrupt end after the end of the war, inflation actually accelerated after the end of the war. The inflation did not actually stop for almost two years after the end of the war, when a huge deflation set in. Caton shows that the behavior of the price level was largely determined by the declining gold holdings of the Federal Reserve after the war ended. Unnerved by the rapid inflation, the Fed finally changed policy, and began accumulating gold rapidly in 1920 by raising the discount rate to an all-time high of 7 percent. Although no other countries were then on the gold standard, other countries, unwilling, for the most part, to allow their currencies to depreciate too much against the dollar, imported US deflation.

Jim is also a blogger. Check out his blog here.

Update: Thanks to commenter Blue Aurora for pointing out that I neglected to provide a link to Jim Caton’s paper. Sorry about that. The link is now embedded.

It seems that your efforts to get R.G. Hawtrey (and to a lesser extent, Gustav Cassel) recognised are paying off, David Glasner. Congratulations!

Who knows? As I suggested in the past that you take up such a role, perhaps there might be a “CWRGH” (Collected Writings/Works of Ralph George Hawtrey) in the same way there is a “CWJMK” (Collected Writings/Works of John Maynard Keynes) at some point in the future!

James Caton’s working paper looks like a good first draft, and I think he deserves the attention on his work that you have highlighted. (Sorry sir, but you failed to directly link us to his working paper on the SSRN!)

I do have one thing to say for both you and James Caton, however…

Why not cite Liaquat Ahamed’s 2009 book (which won the 2010 Pulitzer Prize in History), Lords of Finance: The Bankers Who Broke the World?

Although Liaquat Ahamed acknowledges that his book derives much from the arguments made by Milton Friedman and Anna Schwartz’s 1963 classic, A Monetary History of the United States, 1867–1960, and Barry Eichengreen’s 1992 book, Golden Fetters: The Gold Standard and the Great Depression, 1919–1939, I think it still ought to be cited in any papers dealing with these monetary matters because it repackaged and further spread these important issues to a wider audience.

LikeLike

Blue Aurora, Thanks for your comment and for pointing out that I failed to provide a link to Caton’s paper. I just provided the link to the paper. Certainly it would be wonderful if we had an edition of Hawtrey’s collected works. In addition to aboutl20 books that he wrote, there are probably at least 100 scholarly articles and perhaps another 100 book reviews that he wrote in his long career, plus other unpublished writings from his days at the Treasury. It’s nice of you to suggest me for the job, but the last I heard, nobody is looking to publish Hawtrey’s collected works. Even if there were, I don’t think I would be interested.

LikeLike

You’re welcome sir. Naturally, I’m not surprised that are very few if any people who would be interested in creating a “CWRGH”. You said to me earlier on this blog that such a venture might have to go to a younger scholar instead.

Out of curiosity, have you read Lords of Finance: The Bankers Who Broke the World by Liaquat Ahamed?

Regardless of whether you have or not…as I said, it derives much from previous scholarship done by (Friedman and Schwartz 1963) and (Eichengreen 1992), but I think it would be appropriate to cite due to the timeliness of its publication (and the same serendipity happened to This Time is Different: Eight Centuries of Financial Folly by Carmen Reinhart and Kenneth Rogoff). I have no doubt that future historians, future economists, and future policy-makers are among the readership of that book, which certainly benefited from the surge of interest in economic matters as the global financial crisis devastated the world economy.

Naturally, you are not obliged to cite Liaquat Ahamed’s 2009 book, and I won’t blame you if you choose not to.

LikeLike

Blue Aurora, Oh yes, I did read and enjoy Lords of Finance. I thought it was a very well done book and I learned a lot from it. But I don’t think that I agreed with everything he wrote, though I can’t really remember any specific points of disagreement at the moment Most of the citations in the paper are to publications of an earlier vintage. At this point, I would be reluctant to add any citations unless it was something specific that we were relying on.

LikeLike

I see. All I was really suggesting was a one-sentence reference to Lords of Finance which goes something along the lines of: “Public interest in monetary theory and policy was stimulated by the serendipitous publication of Lords of Finance: The Bankers Who Broke The World by Liaquat Ahamed (2009).”

That stated, I’m not going to blame you for not putting in that reference in your paper! (Nor will I blame James Caton for not doing so.)

LikeLike