The following (with some minor revisions) is a Twitter thread I posted yesterday. Unfortunately, because it was my first attempt at threading the thread wound up being split into three sub-threads and rather than try to reconnect them all, I will just post the complete thread here as a blogpost.

1. Here’s an outline of an unwritten paper developing some ideas from my paper “Hayek Hicks Radner and Four Equilibrium Concepts” (see here for an earlier ungated version) and some from previous blog posts, in particular Phillips Curve Musings.

2. Standard supply-demand analysis is a form of partial-equilibrium (PE) analysis, which means that it is contingent on a ceteris paribus (CP) assumption, an assumption largely incompatible with realistic dynamic macroeconomic analysis.

3. Macroeconomic analysis is necessarily situated a in general-equilibrium (GE) context that precludes any CP assumption, because there are no variables that are held constant in GE analysis.

4. In the General Theory, Keynes criticized the argument based on supply-demand analysis that cutting nominal wages would cure unemployment. Instead, despite his Marshallian training (upbringing) in PE analysis, Keynes argued that PE (AKA supply-demand) analysis is unsuited for understanding the problem of aggregate (involuntary) unemployment.

5. The comparative-statics method described by Samuelson in the Foundations of Econ Analysis formalized PE analysis under the maintained assumption that a unique GE obtains and deriving a “meaningful theorem” from the 1st- and 2nd-order conditions for a local optimum.

6. PE analysis, as formalized by Samuelson, is conditioned on the assumption that GE obtains. It is focused on the effect of changing a single parameter in a single market small enough for the effects on other markets of the parameter change to be made negligible.

7. Thus, PE analysis, the essence of micro-economics is predicated on the macrofoundation that all, but one, markets are in equilibrium.

8. Samuelson’s meaningful theorems were a misnomer reflecting mid-20th-century operationalism. They can now be understood as empirically refutable propositions implied by theorems augmented with a CP assumption that interactions b/w markets are small enough to be neglected.

9. If a PE model is appropriately specified, and if the market under consideration is small or only minimally related to other markets, then differences between predictions and observations will be statistically insignificant.

10. So PE analysis uses comparative-statics to compare two alternative general equilibria that differ only in respect of a small parameter change.

11. The difference allows an inference about the causal effect of a small change in that parameter, but says nothing about how an economy would actually adjust to a parameter change.

12. PE analysis is conditioned on the CP assumption that the analyzed market and the parameter change are small enough to allow any interaction between the parameter change and markets other than the market under consideration to be disregarded.

13. However, the process whereby one equilibrium transitions to another is left undetermined; the difference between the two equilibria with and without the parameter change is computed but no account of an adjustment process leading from one equilibrium to the other is provided.

14. Hence, the term “comparative statics.”

15. The only suggestion of an adjustment process is an assumption that the price-adjustment in any market is an increasing function of excess demand in the market.

16. In his seminal account of GE, Walras posited the device of an auctioneer who announces prices–one for each market–computes desired purchases and sales at those prices, and sets, under an adjustment algorithm, new prices at which desired purchases and sales are recomputed.

17. The process continues until a set of equilibrium prices is found at which excess demands in all markets are zero. In Walras’s heuristic account of what he called the tatonnement process, trading is allowed only after the equilibrium price vector is found by the auctioneer.

18. Walras and his successors assumed, but did not prove, that, if an equilibrium price vector exists, the tatonnement process would eventually, through trial and error, converge on that price vector.

19. However, contributions by Sonnenschein, Mantel and Debreu (hereinafter referred to as the SMD Theorem) show that no price-adjustment rule necessarily converges on a unique equilibrium price vector even if one exists.

20. The possibility that there are multiple equilibria with distinct equilibrium price vectors may or may not be worth explicit attention, but for purposes of this discussion, I confine myself to the case in which a unique equilibrium exists.

21. The SMD Theorem underscores the lack of any explanatory account of a mechanism whereby changes in market prices, responding to excess demands or supplies, guide a decentralized system of competitive markets toward an equilibrium state, even if a unique equilibrium exists.

22. The Walrasian tatonnement process has been replaced by the Arrow-Debreu-McKenzie (ADM) model in an economy of infinite duration consisting of an infinite number of generations of agents with given resources and technology.

23. The equilibrium of the model involves all agents populating the economy over all time periods meeting before trading starts, and, based on initial endowments and common knowledge, making plans given an announced equilibrium price vector for all time in all markets.

24. Uncertainty is accommodated by the mechanism of contingent trading in alternative states of the world. Given assumptions about technology and preferences, the ADM equilibrium determines the set prices for all contingent states of the world in all time periods.

25. Given equilibrium prices, all agents enter into optimal transactions in advance, conditioned on those prices. Time unfolds according to the equilibrium set of plans and associated transactions agreed upon at the outset and executed without fail over the course of time.

26. At the ADM equilibrium price vector all agents can execute their chosen optimal transactions at those prices in all markets (certain or contingent) in all time periods. In other words, at that price vector, excess demands in all markets with positive prices are zero.

27. The ADM model makes no pretense of identifying a process that discovers the equilibrium price vector. All that can be said about that price vector is that if it exists and trading occurs at equilibrium prices, then excess demands will be zero if prices are positive.

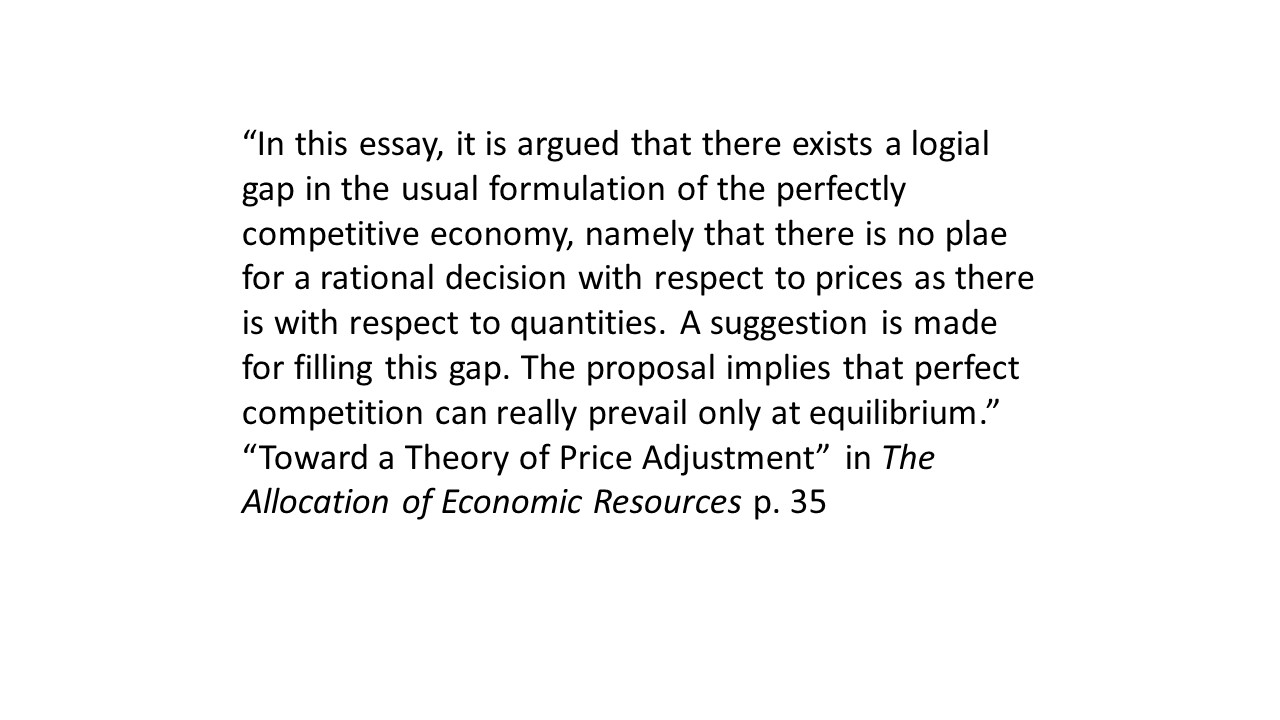

28. Arrow himself drew attention to the gap in the ADM model, writing in 1959:

29. In addition to the explanatory gap identified by Arrow, another shortcoming of the ADM model was discussed by Radner: the dependence of the ADM model on a complete set of forward and state-contingent markets at time zero when equilibrium prices are determined.

30. Not only is the complete-market assumption a backdoor reintroduction of perfect foresight, it excludes many features of the greatest interest in modern market economies: the existence of money, stock markets, and money-crating commercial banks.

31. Radner showed that for full equilibrium to obtain, not only must excess demands in current markets be zero, but whenever current markets and current prices for future delivery are missing, agents must correctly expect those future prices.

32. But there is no plausible account of an equilibrating mechanism whereby price expectations become consistent with GE. Although PE analysis suggests that price adjustments do clear markets, no analogous analysis explains how future price expectations are equilibrated.

33. But if both price expectations and actual prices must be equilibrated for GE to obtain, the notion that “market-clearing” price adjustments are sufficient to achieve macroeconomic “equilibrium” is untenable.

34. Nevertheless, the idea that individual price expectations are rational (correct), so that, except for random shocks, continuous equilibrium is maintained, became the bedrock for New Classical macroeconomics and its New Keynesian and real-business cycle offshoots.

35. Macroeconomic theory has become a theory of dynamic intertemporal optimization subject to stochastic disturbances and market frictions that prevent or delay optimal adjustment to the disturbances, potentially allowing scope for countercyclical monetary or fiscal policies.

36. Given incomplete markets, the assumption of nearly continuous intertemporal equilibrium implies that agents correctly foresee future prices except when random shocks occur, whereupon agents revise expectations in line with the new information communicated by the shocks.

37. Modern macroeconomics replaced the Walrasian auctioneer with agents able to forecast the time path of all prices indefinitely into the future, except for intermittent unforeseen shocks that require agents to optimally their revise previous forecasts.

38. When new information or random events, requiring revision of previous expectations, occur, the new information becomes common knowledge and is processed and interpreted in the same way by all agents. Agents with rational expectations always share the same expectations.

39. So in modern macro, Arrow’s explanatory gap is filled by assuming that all agents, given their common knowledge, correctly anticipate current and future equilibrium prices subject to unpredictable forecast errors that change their expectations of future prices to change.

40. Equilibrium prices aren’t determined by an economic process or idealized market interactions of Walrasian tatonnement. Equilibrium prices are anticipated by agents, except after random changes in common knowledge. Semi-omniscient agents replace the Walrasian auctioneer.

41. Modern macro assumes that agents’ common knowledge enables them to form expectations that, until superseded by new knowledge, will be validated. The assumption is wrong, and the mistake is deeper than just the unrealism of perfect competition singled out by Arrow.

42. Assuming perfect competition, like assuming zero friction in physics, may be a reasonable simplification for some problems in economics, because the simplification renders an otherwise intractable problem tractable.

43. But to assume that agents’ common knowledge enables them to forecast future prices correctly transforms a model of decentralized decision-making into a model of central planning with each agent possessing the knowledge only possessed by an omniscient central planner.

44. The rational-expectations assumption fills Arrow’s explanatory gap, but in a deeply unsatisfactory way. A better approach to filling the gap would be to acknowledge that agents have private knowledge (and theories) that they rely on in forming their expectations.

45. Agents’ expectations are – at least potentially, if not inevitably – inconsistent. Because expectations differ, it’s the expectations of market specialists, who are better-informed than non-specialists, that determine the prices at which most transactions occur.

46. Because price expectations differ even among specialists, prices, even in competitive markets, need not be uniform, so that observed price differences reflect expectational differences among specialists.

47. When market specialists have similar expectations about future prices, current prices will converge on the common expectation, with arbitrage tending to force transactions prices to converge toward notwithstanding the existence of expectational differences.

48. However, the knowledge advantage of market specialists over non-specialists is largely limited to their knowledge of the workings of, at most, a small number of related markets.

49. The perspective of specialists whose expectations govern the actual transactions prices in most markets is almost always a PE perspective from which potentially relevant developments in other markets and in macroeconomic conditions are largely excluded.

50. The interrelationships between markets that, according to the SMD theorem, preclude any price-adjustment algorithm, from converging on the equilibrium price vector may also preclude market specialists from converging, even roughly, on the equilibrium price vector.

51. A strict equilibrium approach to business cycles, either real-business cycle or New Keynesian, requires outlandish assumptions about agents’ common knowledge and their capacity to anticipate the future prices upon which optimal production and consumption plans are based.

52. It is hard to imagine how, without those outlandish assumptions, the theoretical superstructure of real-business cycle theory, New Keynesian theory, or any other version of New Classical economics founded on the rational-expectations postulate can be salvaged.

53. The dominance of an untenable macroeconomic paradigm has tragically led modern macroeconomics into a theoretical dead end.