Trying hard, but not entirely successfully, to contain his astonishment, Paul Krugman has a very good post (“France 1930, Germany 2013) inspired by Doug Irwin’s “very good” paper (see also this shorter version) “Did France Cause the Great Depression?” Here’s Krugman take away from Irwin’s paper.

[Irwin] points out that France, with its undervalued currency, soaked up a huge proportion of the world’s gold reserves in 1930-31, and suggests that France was responsible for about half the global deflation that took place over that period.

The thing is, France itself didn’t do that badly in the early stages of the Great Depression — again thanks to that undervalued currency. In fact, it was less affected than most other advanced countries (pdf) in 1929-31:

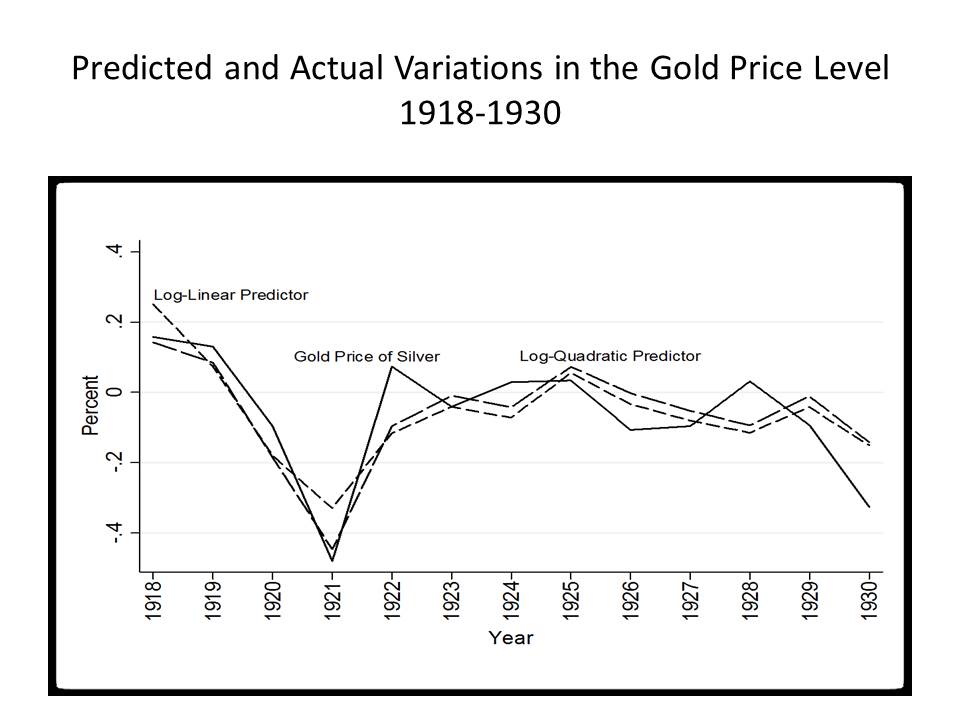

Krugman is on the right track here — certainly a hopeful sign — but he misses the distinction between an undervalued French franc, which, despite temporary adverse effects on other countries, would normally be self-correcting under the gold standard, and the explosive increase in demand for gold by the insane Bank of France after the franc was pegged at an undervalued parity against the dollar. Undervaluation of the franc began in December 1926 when Premier Raymond Poincare stabilized its value at about 25 francs to the dollar, the franc having fallen to 50 francs to the dollar in July when Poincare, a former prime minister, had been returned to office to deal with a worsening currency crisis. Undervaluation of the franc would have done no permanent damage to the world economy if the Bank of France had not used the resulting inflow of foreign exchange to accumulate gold, cashing in sterling- and dollar-denominated financial assets for gold. This was a step beyond classic exchange-rate protection (currency manipulation) whereby a country uses a combination of an undervalued exchange rate and a tight monetary policy to keep accumulating foreign-exchange reserves as a way of favoring its export and import-competing industries. Exchange-rate protection may have been one motivation for the French policy, but that objective did not require gold accumulation; it could have been achieved by accumulating foreign exchange reserves without demanding redemption of those reserves in terms of gold, as the Bank of France began doing aggressively in 1927. A more likely motivation for gold accumulation policy of the Bank of France seems to have been French resentment against a monetary system that, from the French perspective, granted a privileged status to the dollar and to sterling, allowing central banks to treat dollar- and sterling-denominated financial assets as official exchange reserves, thereby enabling issuers of dollar and sterling-denominated assets the ability to obtain funds on more favorable terms than issuers of instruments denominated in other currencies.

The world economy was able to withstand the French gold-accumulation policy in 1927-28, because the Federal Reserve was tolerating an outflow of gold, thereby accommodating to some degree the French demand for gold. But after the Fed raised its discount rate to 5% in 1928 and 6% in February 1929, gold began flowing into the US as well, causing gold to start appreciating (in other words, prices to start falling) in world markets by the summer of 1929. But rather than reverse course, the Bank of France and the Fed, despite reductions in their official lending rates, continued pursuing policies that caused huge amounts of gold to flow into the French and US vaults in 1930 and 1931. Hawtrey and Cassel, of course, had warned against such a scenario as early as 1919, and proposed measures to prevent or reverse the looming catastrophe before it took place and after it started, but with little success. For a more complete account of this sad story, and the failure of the economics profession, with a very few notable exceptions, to figure out what happened, see my paper with Ron Batchelder “Pre-Keynesian Monetary Theories of the Great Depression: Whatever Happened to Hawtrey and Cassel?”

As Krugman observes, the French economy did not do so badly in 1929-31, because it was viewed as the most stable, thrifty, and dynamic economy in Europe. But France looked good only because Britain and Germany were in even worse shape. Because France was better off the Britain and Germany, and because its currency was understood to be undervalued, the French franc was considered to be stable, and, thus, unlikely to be devalued. So, unlike sterling, the reichsmark, and the dollar, the franc was not subjected to speculative attacks, becoming instead a haven for capital seeking safety.

Interestingly, Krugman even shows some sympathetic understanding for the plight of the French:

Notice, by the way, that the French weren’t evil or malicious here — they were just adhering to their hard-money ideology in an environment where that had terrible adverse effects on other countries.

Just wondering, would Krugman ever invoke adherence to a hard-money ideology as a mitigating factor in passing judgment on a Republican?

Krugman concludes by comparing Germany today with France in 1930.

Obviously the details are different, but I would argue that Germany is playing a somewhat similar role today — not as drastic, but with less excuse. For Germany is an economic hegemon in a way France never was; it has responsibilities, which it isn’t meeting.

Indeed, there are similarities, but there is a crucial difference in the mechanism by which damage is being inflicted: the world price level in 1930, under the gold standard, was determined by the value of gold. An increase in the demand for gold by central banks necessarily raised the value of gold, causing deflation for all countries either on the gold standard or maintaining a fixed exchange rate against a gold-standard currency. By accumulating gold, nearly quadrupling its gold reserves between 1926 and 1932, the Bank of France was a mighty deflationary force, inflicting immense damage on the international economy. Today, the Eurozone price level does not depend on the independent policy actions of any national central bank, including that of Germany. The Eurozone price level is rather determined by the policy choices of a nominally independent European Central Bank. But the ECB is clearly unable to any adopt policy not approved by the German government and its leader Mrs. Merkel, and Mrs. Merkel has rejected any policy that would raise prices in the Eurozone to a level consistent with full employment. Though the mechanism by which Mrs. Merkel and her government are now inflicting damage on the Eurozone is different from the mechanism by which the insane Bank of France inflicted damage during the Great Depression, the damage is just as pointless and just as inexcusable. But as the damage caused by Mrs. Merkel, in relative terms at any rate, seems somewhat smaller in magnitude than that caused by the insane Bank of France, I would not judge her more harshly than I would the Bank of France — insanity being, in matters of monetary policy, no defense.

HT: ChargerCarl