About a month ago, I started a series of posts about monetary policy in the 1920s, (about the Bank of France, Benjamin Strong, the difference between a gold-exchange standard and a gold standard, and Ludwig von Mises’s unwitting affirmation of the Hawtrey-Cassel explanation of the Great Depression). The series was not planned, each post being written as new ideas occurred to me or as I found interesting tidbits (about Strong and Mises) in reading stuff I was reading about the Bank of France or the gold-exchange standard.

Another idea that occurred to me was to look at the 1991 English translation of the memoirs of Emile Moreau, Governor of the Bank of France from 1926 to 1930; I managed to find a used copy for sale on Amazon, which I got in the mail over the weekend. I have only read snatches here and there, by looking up names in the index, and we’ll see when I get around to reading the book from cover to cover. One of the more interesting things about the book is the foreward to the English translation by Milton Friedman (and one by Charles Kindleberger as well) to go along with the preface to the 1954 French edition by Jacques Rueff (about which I may have something to say in a future post — we’ll see about that, too).

Friedman’s foreward to Moreau’s memoir is sometimes cited as evidence that he backtracked from his denial in the Monetary History that the Great Depression had been caused by international forces, Friedman insisting that there was actually nothing special about the initial 1929 downturn and that the situation only got out of hand in December 1930 when the Fed foolishly (or maliciously) allowed the Bank of United States to fail, triggering a wave of bank runs and bank failures that caused a sharp decline in the US money stock. According to Friedman it was only at that point that what had been a typical business-cycle downturn degenerated into what Friedman like to call the Great Contraction.

Friedman based his claim that domestic US forces, not an international disturbance, had caused the Great Depression on the empirical observation that US gold reserves increased in 1929; that’s called reasoning from a quantity change. From that fact, Friedman inferred that international forces could not have caused the 1929 downturn, because an international disturbance would have meant that the demand for gold would have increased in the international centers associated with the disturbance, in which case gold would have been flowing out of, not into, the US. In a 1985 article in AER, Gertrude Fremling pointed out an obvious problem with Friedman’s argument which was that gold was being produced every year, and some of the newly produced gold was going into the reserves of central banks. An absolute increase in US gold reserves did not necessarily signify a monetary disturbance in the US. In fact, Fremling showed that US gold reserves actually increased proportionately less than total gold reserves. Unfortunately, Fremling failed to point out that there was a flood of gold pouring into France in 1929, making it easier for Friedman to ignore the problem with his misidentification of the US as the source of the Great Depression.

With that introduction out of the way, let me now quote Friedman’s 1991 acknowledgment that the Bank of France played some role in causing the Great Depression.

Rereading the memoirs of this splendid translation . . . has impressed me with important subtleties that I missed when I read the memoirs in a language not my own and in which I am far from completely fluent. Had I fully appreciated those subtleties when Anna Schwartz and I were writing our A Monetary History of the United States, we would likely have assessed responsibility for the international character of the Great Depression somewhat differently. We attributed responsibility for the initiation of a worldwide contraction to the United States and I would not alter that judgment now. However, we also remarked, “The international effects were severe and the transmission rapid, not only because the gold-exchange standard had rendered the international financial system more vulnerable to disturbances, but also because the United States did not follow gold-standard rules.” Were I writing that sentence today, I would say “because the United States and France did not follow gold-standard rules.”

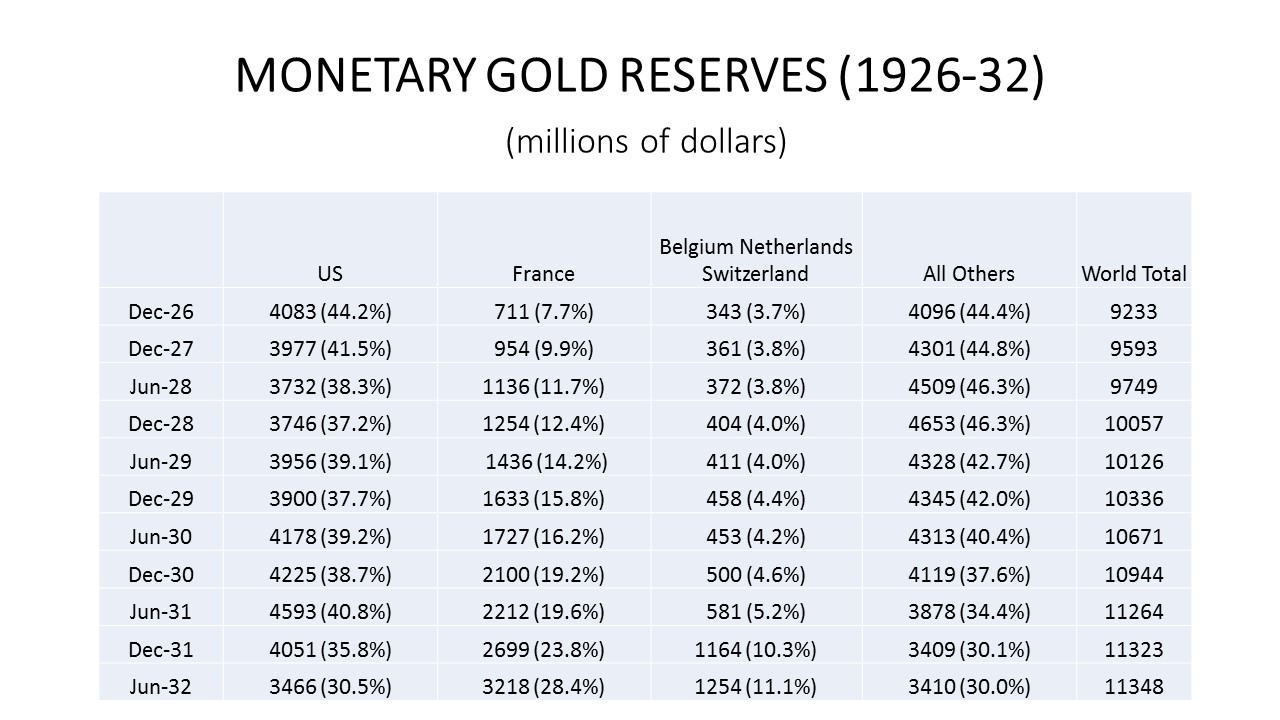

I find this minimal adjustment by Friedman of his earlier position in the Monetary History totally unsatisfactory. Why do I find it unsatisfactory? To begin with, Friedman makes vague references to unnamed but “important subtleties” in Moreau’s memoir that he was unable to appreciate before reading the 1991 translation. There was nothing subtle about the gold accumulation being undertaken by the Bank of France; it was massive and relentless. The table below is constructed from data on official holdings of monetary gold reserves from December 1926 to June 1932 provided by Clark Johnson in his important book Gold, France, and the Great Depression, pp. 190-93. In December 1926 France held $711 million in gold or 7.7% of the world total of official gold reserves; in June 1932, French gold holdings were $3.218 billion or 28.4% of the world total.

What was it about that policy that Friedman didn’t get? He doesn’t say. What he does say is that he would not alter his previous judgment that the US was responsible “for the initiation of a worldwide contraction.” The only change he would make would be to say that France, as well as the US, contributed to the vulnerability of the international financial system to unspecified disturbances, because of a failure to follow “gold-standard rules.” I will just note that, as I have mentioned many times on this blog, references to alleged “gold standard rules” are generally not only unhelpful, but confusing, because there were never any rules as such to the gold standard, and what are termed “gold-standard rules” are largely based on a misconception, derived from the price-specie-flow fallacy, of how the gold standard actually worked.

What was it about that policy that Friedman didn’t get? He doesn’t say. What he does say is that he would not alter his previous judgment that the US was responsible “for the initiation of a worldwide contraction.” The only change he would make would be to say that France, as well as the US, contributed to the vulnerability of the international financial system to unspecified disturbances, because of a failure to follow “gold-standard rules.” I will just note that, as I have mentioned many times on this blog, references to alleged “gold standard rules” are generally not only unhelpful, but confusing, because there were never any rules as such to the gold standard, and what are termed “gold-standard rules” are largely based on a misconception, derived from the price-specie-flow fallacy, of how the gold standard actually worked.

My goal in this post was not to engage in more Friedman bashing. What I wanted to do was to clarify the underlying causes of Friedman’s misunderstanding of what caused the Great Depression. But I have to admit that sometimes Friedman makes it hard not to engage in Friedman bashing. So let’s examine another passage from Friedman’s foreward, and see where that takes us.

Another feature of Moreau’s book that is most fascinating . . . is the story it tells of the changing relations between the French and British central banks. At the beginning, with France in desperate straits seeking to stabilize its currency, [Montagu] Norman [Governor of the Bank of England] was contemptuous of France and regarded it as very much of a junior partner. Through the accident that the French currency was revalued at a level that stimulated gold imports, France started to accumulate gold reserves and sterling reserves and gradually came into the position where at any time Moreau could have forced the British off gold by withdrawing the funds he had on deposit at the Bank of England. The result was that Norman changed from being a proud boss and very much the senior partner to being almost a supplicant at the mercy of Moreau.

What’s wrong with this passage? Well, Friedman was correct about the change in the relative positions of Norman and Moreau from 1926 to 1928, but to say that it was an accident that the French currency was revalued at a level that stimulated gold imports is completely — and in this case embarrassingly — wrong, and wrong in two different senses: one strictly factual, and the other theoretical. First, and most obviously, the level at which the French franc was stabilized — 125 francs per pound — was hardly an accident. Indeed, it was precisely the choice of the rate at which to stabilize the franc that was a central point of Moreau’s narrative in his memoir, a central drama of the tale told by Moreau, more central than the relationship between Norman and Moreau, being the struggle between Moreau and his boss, the French Premier, Raymond Poincaré, over whether the franc would be stabilized at that rate, the rate insisted upon by Moreau, or the prewar parity of 25 francs per pound. So inquiring minds can’t help but wonder what exactly did Friedman think he was reading?

The second sense in which Friedman’s statement was wrong is that the amount of gold that France was importing depended on a lot more than just its exchange rate; it was also a function of a) the monetary policy chosen by the Bank of France, which determined the total foreign-exchange holdings held by the Bank of France, and b) the portfolio decisions of the Bank of France about how, given the exchange rate of the franc and given the monetary policy it adopted, the resulting quantity of foreign-exchange reserves would be held.

Let’s follow Friedman a bit further in his foreward as he quotes from his own essay “Should There Be an Independent Monetary Authority?” contrasting the personal weakness of W. P. G. Harding, Governor of the Federal Reserve in 1919-20, with the personal strength of Moreau:

Almost every student of the period is agreed that the great mistake of the Reserve System in postwar monetary policy was to permit the money stock to expand very rapidly in 1919 and then to step very hard on the brakes in 1920. This policy was almost surely responsible for both the sharp postwar rise in prices and the sharp subsequent decline. It is amusing to read Harding’s answer in his memoirs to criticism that was later made of the policies followed. He does not question that alternative policies might well have been preferable for the economy as a whole, but emphasizes the treasury’s desire to float securities at a reasonable rate of interest, and calls attention to a then-existing law under which the treasury could replace the head of the Reserve System. Essentially he was saying the same thing that I heard another member of the Reserve Board say shortly after World War II when the bond-support program was in question. In response to the view expressed by some of my colleagues and myself that the bond-support program should be dropped, he largely agreed but said ‘Do you want us to lose our jobs?’

The importance of personality is strikingly revealed by the contrast between Harding’s behavior and that of Emile Moreau in France under much more difficult circumstances. Moreau formally had no independence whatsoever from the central government. He was named by the premier, and could be discharged at any time by the premier. But when he was asked by the premier to provide the treasury with funds in a manner that he considered inappropriate and undesirable, he flatly refused to do so. Of course, what happened was that Moreau was not discharged, that he did not do what the premier had asked him to, and that stabilization was rather more successful.

Now, if you didn’t read this passage carefully, in particular the part about Moreau’s threat to resign, as I did not the first three or four times that I read it, you might not have noticed what a peculiar description Friedman gives of the incident in which Moreau threatened to resign following a request “by the premier to provide the treasury with funds in a manner that he considered inappropriate and undesirable.” That sounds like a very strange request for the premier to make to the Governor of the Bank of France. The Bank of France doesn’t just “provide funds” to the Treasury. What exactly was the request? And what exactly was “inappropriate and undesirable” about that request?

I have to say again that I have not read Moreau’s memoir, so I can’t state flatly that there is no incident in Moreau’s memoir corresponding to Friedman’s strange account. However, Jacques Rueff, in his preface to the 1954 French edition (translated as well in the 1991 English edition), quotes from Moreau’s own journal entries how the final decision to stabilize the French franc at the new official parity of 125 per pound was reached. And Friedman actually refers to Rueff’s preface in his foreward! Let’s read what Rueff has to say:

The page for May 30, 1928, on which Mr. Moreau set out the problem of legal stabilization, is an admirable lesson in financial wisdom and political courage. I reproduce it here in its entirety with the hope that it will be constantly present in the minds of those who will be obliged in the future to cope with French monetary problems.

“The word drama may sound surprising when it is applied to an event which was inevitable, given the financial and monetary recovery achieved in the past two years. Since July 1926 a balanced budget has been assured, the National Treasury has achieved a surplus and the cleaning up of the balance sheet of the Bank of France has been completed. The April 1928 elections have confirmed the triumph of Mr. Poincaré and the wisdom of the ideas which he represents. The political situation has been stabilized. Under such conditions there is nothing more natural than to stabilize the currency, which has in fact already been pegged at the same level for the last eighteen months.

“But things are not quite that simple. The 1926-28 recovery from restored confidence to those who had actually begun to give up hope for their country and its capacity to recover from the dark hours of July 1926. . . . perhaps too much confidence.

“Distinguished minds maintained that it was possible to return the franc to its prewar parity, in the same way as was done with the pound sterling. And how tempting it would be to thereby cancel the effects of the war and postwar periods and to pay back in the same currency those who had lent the state funds which for them often represented an entire lifetime of unremitting labor.

“International speculation seemed to prove them right, because it kept changing its dollars and pounds for francs, hoping that the franc would be finally revalued.

“Raymond Poincaré, who was honesty itself and who, unlike most politicians, was truly devoted to the public interest and the glory of France, did, deep in his heart, agree with those awaiting a revaluation.

“But I myself had to play the ungrateful role of representative of the technicians who knew that after the financial bloodletting of the past years it was impossible to regain the original parity of the franc.

“I was aware, as had already been determined by the Committee of Experts in 1926, that it was impossible to revalue the franc beyond certain limits without subjecting the national economy to a particularly painful readaptation. If we were to sacrifice the vital force of the nation to its acquired wealth, we would put at risk the recovery we had already accomplished. We would be, in effect, preparing a counterspeculation against our currency that would come within a rather short time.

“Since the parity of 125 francs to one pound has held for long months and the national economy seems to have adapted itself to it, it should be at this rate that we stabilize without further delay.

“This is what I had to tell Mr. Poincaré at the beginning of June 1928, tipping the scales of his judgment with the threat of my resignation.” [my emphasis]

So what this tells me is that the very act of personal strength that so impressed Friedman about Moreau was not about some imaginary “inappropriate” request made by Poincaré (“who was honesty itself”) for the Bank to provide funds to the treasury, but about whether the franc should be stabilized at 125 francs per pound, a peg that Friedman asserts was “accidental.” Obviously, it was not “accidental” at all, but it was based on the judgment of Moreau and his advisers (including two economists of considerable repute, Charles Rist and his student Pierre Quesnay) as attested to by Rueff in his preface, of which we know that Friedman was aware.

Just to avoid misunderstanding, I would just say here that I am not suggesting that Friedman was intentionally misrepresenting any facts. I think that he was just being very sloppy in assuming that the facts actually were what he rather cluelessly imagined them to be.

Before concluding, I will quote again from Friedman’s foreword:

Benjamin Strong and Emile Moreau were admirable characters of personal force and integrity. But in my view, the common policies they followed were misguided and contributed to the severity and rapidity of transmission of the U.S. shock to the international community. We stressed that the U.S. “did not permit the inflow of gold to expand the U.S. money stock. We not only sterilized it, we went much further. Our money stock moved perversely, going down as the gold stock went up” from 1929 to 1931. France did the same, both before and after 1929.

Strong and Moreau tried to reconcile two ultimately incompatible objectives: fixed exchange rates and internal price stability. Thanks to the level at which Britain returned to gold in 1925, the U.S. dollar was undervalued, and thanks to the level at which France returned to gold at the end of 1926, so was the French franc. Both countries as a result experienced substantial gold inflows. Gold-standard rules called for letting the stock of money rise in response to the gold inflows and for price inflation in the U.S. and France, and deflation in Britain, to end the over-and under-valuations. But both Strong and Moreau were determined to preven t inflation and accordingly both sterilized the gold inflows, preventing them from providing the required increase in the quantity of money. The result was to drain the other central banks of the world of their gold reserves, so that they became excessively vulnerable to reserve drains. France’s contribution to this process was, I now realize, much greater than we treated it as being in our History.

These two paragraphs are full of misconceptions; I will try to clarify and correct them. First Friedman refers to “the U.S. shock to the international community.” What is he talking about? I don’t know. Is he talking about the crash of 1929, which he dismissed as being of little consequence for the subsequent course of the Great Depression, whose importance in Friedman’s view was certainly far less than that of the failure of the Bank of United States? But from December 1926 to December 1929, total monetary gold holdings in the world increased by about $1 billion; while US gold holdings declined by nearly $200 million, French holdings increased by $922 million over 90% of the increase in total world official gold reserves. So for Friedman to have even suggested that the shock to the system came from the US and not from France is simply astonishing.

Friedman’s discussion of sterilization lacks any coherent theoretical foundation, because, working with the most naïve version of the price-specie-flow mechanism, he imagines that flows of gold are entirely passive, and that the job of the monetary authority under a gold standard was to ensure that the domestic money stock would vary proportionately with the total stock of gold. But that view of the world ignores the possibility that the demand to hold money in any country could change. Thus, Friedman, in asserting that the US money stock moved perversely from 1929 to 1931, going down as the gold stock went up, misunderstands the dynamic operating in that period. The gold stock went up because, with the banking system faltering, the public was shifting their holdings of money balances from demand deposits to currency. Legal reserves were required against currency, but not against demand deposits, so the shift from deposits to currency necessitated an increase in gold reserves. To be sure the US increase in the demand for gold, driving up its value, was an amplifying factor in the worldwide deflation, but total US holdings of gold from December 1929 to December 1931 rose by $150 million compared with an increase of $1.06 billion in French holdings of gold over the same period. So the US contribution to world deflation at that stage of the Depression was small relative to that of France.

Friedman is correct that fixed exchange rates and internal price stability are incompatible, but he contradicts himself a few sentences later by asserting that Strong and Moreau violated gold-standard rules in order to stabilize their domestic price levels, as if it were the gold-standard rules rather than market forces that would force domestic price levels into correspondence with a common international level. Friedman asserts that the US dollar was undervalued after 1925 because the British pound was overvalued, presuming with no apparent basis that the US balance of payments was determined entirely by its trade with Great Britain. As I observed above, the exchange rate is just one of the determinants of the direction and magnitude of gold flows under the gold standard, and, as also pointed out above, gold was generally flowing out of the US after 1926 until the ferocious tightening of Fed policy at the end of 1928 and in 1929 caused a sizable inflow of gold into the US in 1929.

In thrall to the crude price-specie-flow fallacy, Friedman erroneously assumes that inflation rates under the gold standard are governed by the direction and size of gold flows, inflows being inflationary and outflows deflationary. That is just wrong; national inflation rates were governed by a common international price level in terms of gold (and any positive or negative inflation in terms of gold) and whether prices in the local currency were above or below their gold equivalents, market forces operating to equalize the prices of tradable goods. Domestic monetary policies, whether or not they conformed to supposed gold standard rules, had negligible effect on national inflation rates. If the pound was overvalued, there was deflationary pressure in Britain regardless of whether British monetary policy was tight or easy, and if the franc was undervalued there was inflationary pressure in France regardless of whether French monetary policy was tight or easy. Tightness or ease of monetary policy under the gold standard affects not the rate of inflation, but the rate at which the central bank gained or lost foreign exchange reserves.

However, when, in the aggregate, central banks were tightening their policies, thereby tending to accumulate gold, the international gold market would come under pressure, driving up the value of gold relative goods, thereby causing deflationary pressure among all the gold standard countries. That is what happened in 1929, when the US started to accumulate gold even as the insane Bank of France was acting as a giant international vacuum cleaner sucking in gold from everywhere else in the world. Friedman, even as he was acknowledging that he had underestimated the importance of the Bank of France in the Monetary History, never figured this out. He was obsessed, instead with relatively trivial effects of overvaluation of the pound, and undervaluation of the franc and the dollar. Talk about missing the forest for the trees.

Of course, Friedman was not alone in his cluelessness about the Bank of France. F. A. Hayek, with whom, apart from their common belief in the price-specie-flow fallacy, Friedman shared almost no opinions about monetary theory and policy, infamously defended the Bank of France in 1932.

France did not prevent her monetary circulation from increasing by the very same amount as that of the gold inflow – and this alone is necessary for the gold standard to function.

Thus, like Friedman, Hayek completely ignored the effect that the monumental accumulation of gold by the Bank of France had on the international value of gold. That Friedman accused the Bank of France of violating the “gold-standard rules” while Hayek denied the accusation simply shows, notwithstanding the citations by the Swedish Central Bank of the work that both did on the Great Depression when awarding them their Nobel Memorial Prizes, how far away they both were from an understanding of what was actually going on during that catastrophic period.