Ever the optimist, I was hoping that yesterday’s immediate, sharply negative, reaction to the FOMC statement and Ben Bernanke’s press conference was only a mild correction, not the sign of a major revision in expectations. Today’s accelerating slide in stock prices, coupled with continuing rises declines in bond prices, across the entire yield curve, shows that the FOMC, whose obsession with inflation in 2008 drove the world economy into a Little Depression, may now be on the verge of precipitating yet another downturn even before any real recovery has taken place.

If 2008-09 was a replay of 1929-30, then we might be headed back to a reprise of 1937, when a combination of fiscal austerity and monetary tightening, fed by exaggerated, if not irrational fears of inflation, notwithstanding the absence of a full recovery from the 1929-33 downturn, caused a second downturn, nearly as sharp as that of 1929-30.

Nothing is inevitable. History does not have to repeat itself. But if we want to avoid a repeat of 1937, we must avoid repeating the same stupid mistakes made in 1937. Don’t withdraw – or talk about withdrawing — a stimulus that isn’t even generating the measly 2% inflation that the FOMC says its targeting, even while the unemployment rate is still 7.6%. And as Paul Krugman pointed out in his blog today, the labor force participation rate has barely increased since the downturn bottomed out in 2009. I reproduce his chart below.

Bernanke claims to be maintaining an accommodative monetary policy and is simply talking about withdrawing (tapering off), as conditions warrant, the additional stimulus associated with the Fed’s asset purchases. That reminds me of the stance of the FOMC in 2008 when the Fed, having reduced interest rates to 2% in March, kept threatening to raise interest rates during the spring and summer to counter rising commodity prices, even as the economy was undergoing, even before the onset of the financial crisis, one of the fastest contractions since World War II. Yesterday’s announcement, making no commitment to ensure that the Fed’s own inflation target would be met, has obviously been understood by the markets to signal the willingness of the FOMC to tolerate even lower rates of inflation than we have now.

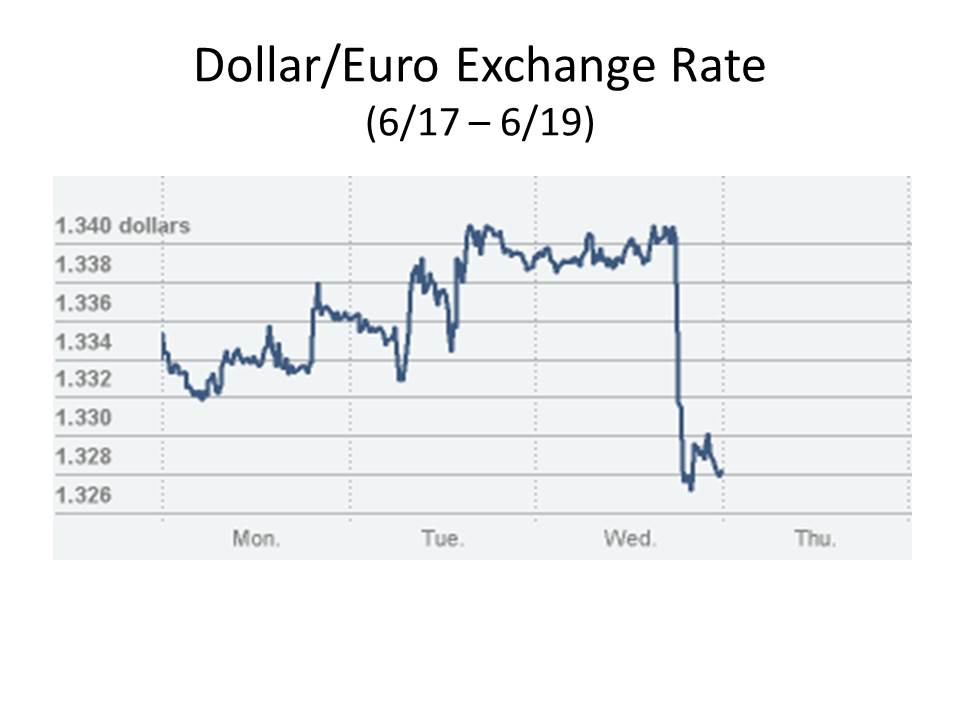

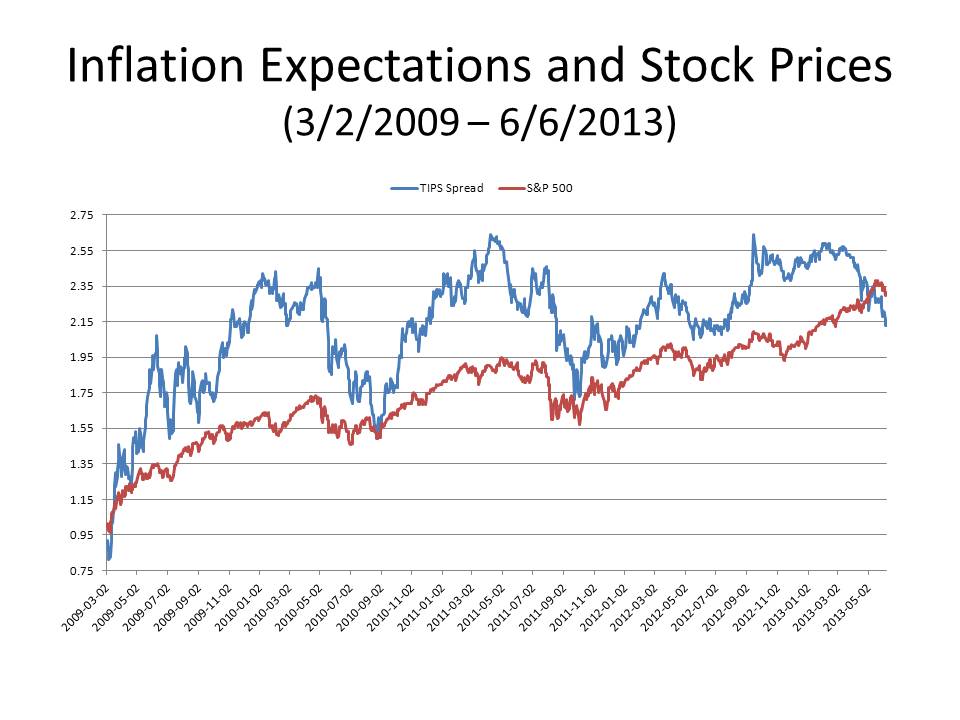

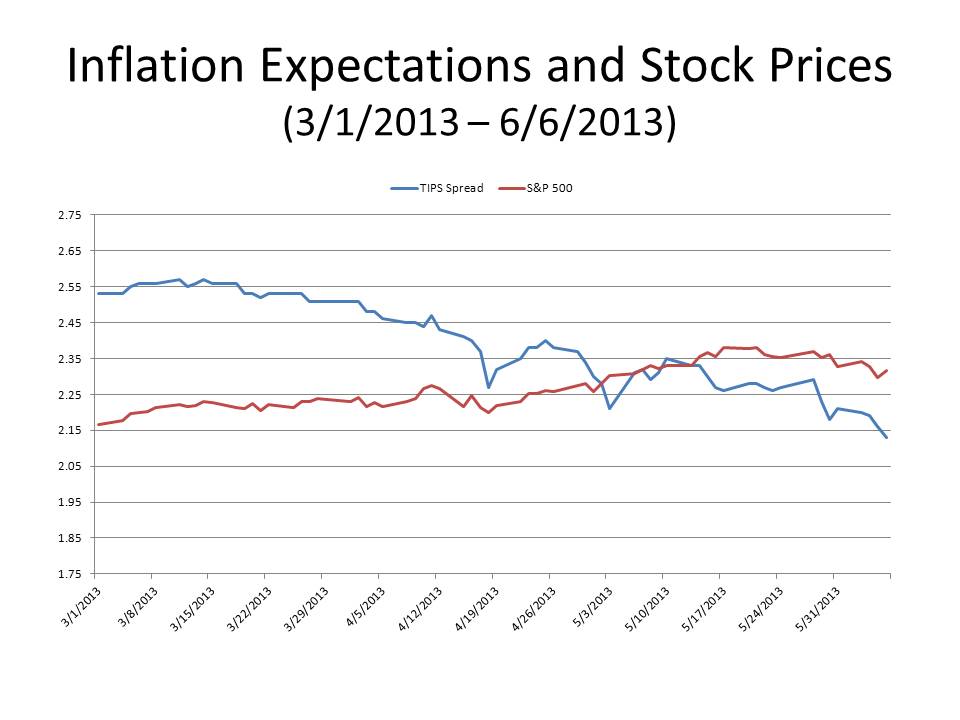

In my post yesterday, I observed that the steep rise in nominal and real interest rates (at least as approximated by the yield on TIPS) was accompanied by only a very modest decline in inflation expectations (as approximated by the TIPS spread). Well, today, nominal and real interest rates (as reflected in TIPS) rose again, but with the breakeven 10-year TIPS spread falling by 9 basis points, to 1.95%. Meanwhile, the dollar continued to appreciate against the euro, supporting the notion that the markets are reacting to a perceived policy change, a change in exactly the wrong direction. Oh, and by the way, the price of gold continued to plummet, reaching $1280 an ounce, the lowest in almost three years, nearly a third less than its 2011 peak.

But for a contrary view, have a look at theeditorial (“Monetary Withdrawal Symptom”) in Friday’s Wall Street Journal, as well as an op-ed piece by an asset fund manager, Romain Hatchuel, (“Central Banks and the Borrowing Addiction”). Both characterize central banks as drug pushers who have induced hundreds of millions, if not billions, of people around the world to become debt addicts. Hatchuel sees some deep significance in the fact that total indebtedness has, since 1980, increased as fast as GDP, while from 1950 to 1980 total indebtedness increased at a much slower rate.

Um, if more people are borrowing, more people are lending, so the mere fact that total indebtedness has increased faster in the last 30 years than it did in the previous 30 years says nothing about debt addiction. It simply says that more people have been gaining access to credit markets in recent years than had access to credit markets in the 1950s, 1960s and 1970s. If we are so addicted to debt, how come real interest rates are so low? If a growing epidemic of debt addiction started in 1980, shouldn’t real interest rates have been rising steadily since then? Guess what? Real interest rates have been falling steadily since 1982. The Wall Street Journal strikes (out) again.