The New York Times finally caught on today that the gold bubble is bursting, months after I had alerted the blogosphere. But even though I haven’t received much credit for scooping the Times, I am still happy to see that word that the bubble has burst is spreading.

Gold, pride of Croesus and store of wealth since time immemorial, has turned out to be a very bad investment of late. A mere two years after its price raced to a nominal high, gold is sinking — fast. Its price has fallen 17 percent since late 2011. Wednesday was another bad day for gold: the price of bullion dropped $28 to $1,558 an ounce.

It is a remarkable turnabout for an investment that many have long regarded as one of the safest of all. The decline has been so swift that some Wall Street analysts are declaring the end of a golden age of gold. The stakes are high: the last time the metal went through a patch like this, in the 1980s, its price took 30 years to recover.

What went wrong? The answer, in part, lies in what went right. Analysts say gold is losing its allure after an astonishing 650 percent rally from August 1999 to August 2011. Fast-money hedge fund managers and ordinary savers alike flocked to gold, that haven of havens, when the world economy teetered on the brink in 2009. Now, the worst of the Great Recession has passed. Things are looking up for the economy and, as a result, down for gold. On top of that, concern that the loose monetary policy at Federal Reserve might set off inflation — a prospect that drove investors to gold — have so far proved to be unfounded.

And so Wall Street is growing increasingly bearish on gold, an investment that banks and others had deftly marketed to the masses only a few years ago. On Wednesday, Goldman Sachs became the latest big bank to predict further declines, forecasting that the price of gold would sink to $1,390 within a year, down 11 percent from where it traded on Wednesday. Société Générale of France last week issued a report titled, “The End of the Gold Era,” which said the price should fall to $1,375 by the end of the year and could keep falling for years.

Granted, gold has gone through booms and busts before, including at least two from its peak in 1980, when it traded at $835, to its high in 2011. And anyone who bought gold in 1999 and held on has done far better than the average stock market investor. Even after the recent decline, gold is still up 515 percent.

But for a generation of investors, the golden decade created the illusion that the metal would keep rising forever. The financial industry seized on such hopes to market a growing range of gold investments, making the current downturn in gold felt more widely than previous ones. That triumph of marketing gold was apparent in an April 2011 poll by Gallup, which found that 34 percent of Americans thought that gold was the best long-term investment, more than another other investment category, including real estate and mutual funds.

It is hard to know just how much money ordinary Americans plowed into gold, given the array of investment vehicles, including government-minted coins, publicly traded commodity funds, mining company stocks and physical bullion. But $5 billion that flowed into gold-focused mutual funds in 2009 and 2010, according to Morningstar, helped the funds reach a peak value of $26.3 billion. Since hitting a peak in April 2011, those funds have lost half of their value.

“Gold is very much a psychological market,” said William O’Neill, a co-founder of the research firm Logic Advisors, which told its investors to get out of all gold positions in December after recommending the investment for years. “Unless there is some unforeseen development, I think the market is going lower.”

The smart money is getting out fast.

Investment professionals, who have focused many of their bets on gold exchange-traded funds, or E.T.F.’s, have been faster than retail investors to catch wind of gold’s changing fortune. The outflow at the most popular E.T.F., the SPDR Gold Shares, was the biggest of any E.T.F. in the first quarter of this year as hedge funds and traders pulled out $6.6 billion, according to the data firm IndexUniverse. Two prominent hedge fund managers who had taken big positions in gold E.T.F.’s, George Soros and Louis M. Bacon, sold in the last quarter of 2012, according to recent regulatory filings.

“Gold was destroyed as a safe haven, proved to be unsafe,” Mr. Soros said in an interview last week with The South China Morning Post of Hong Kong. “Because of the disappointment, most people are reducing their holdings of gold.”

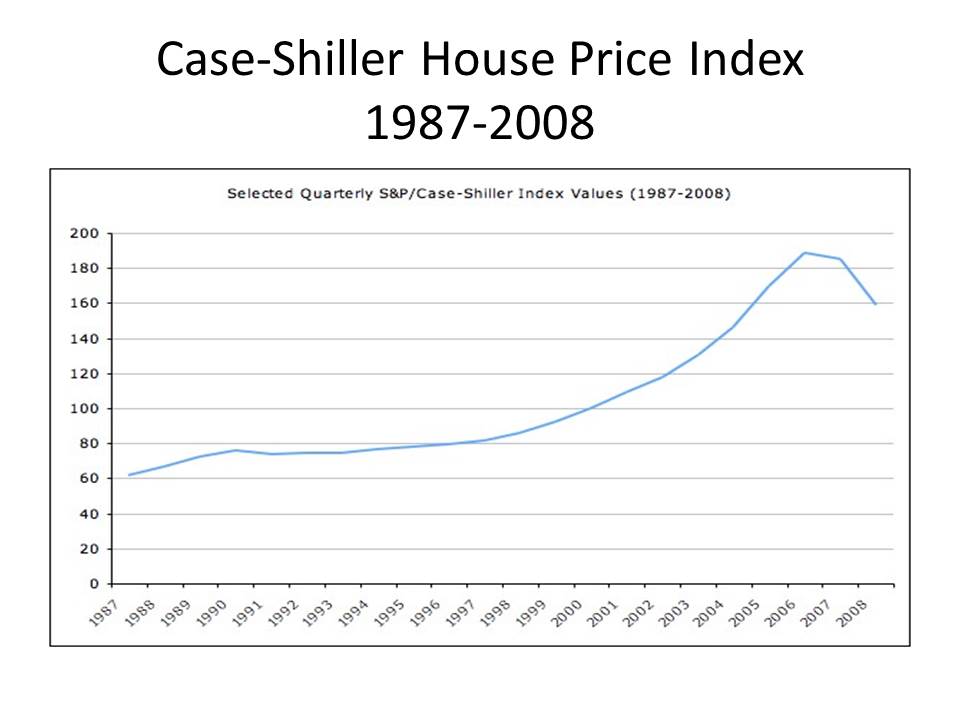

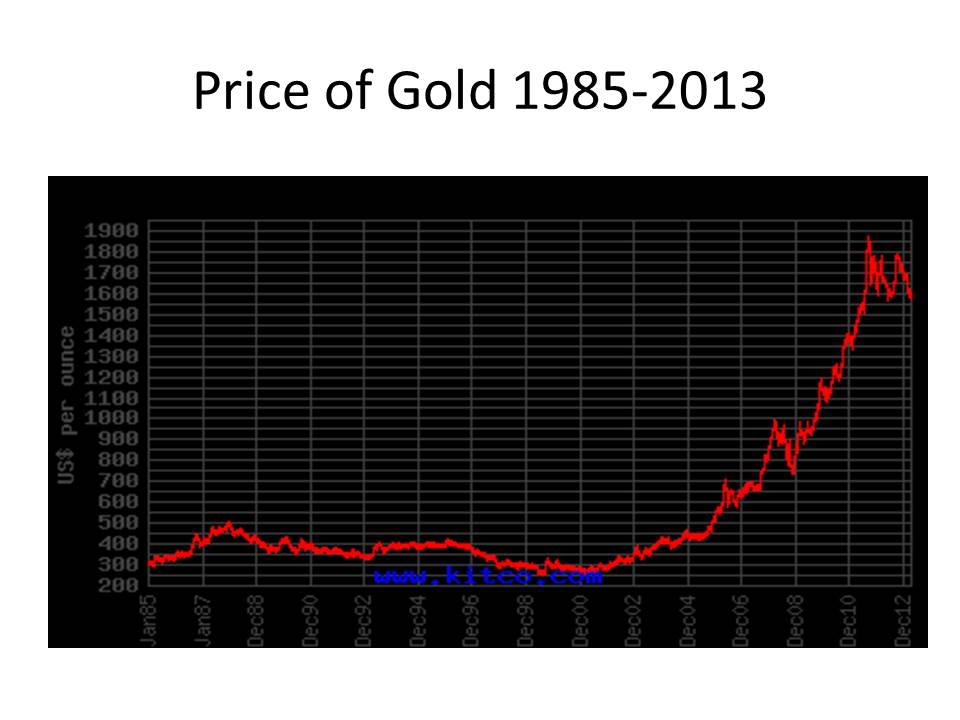

And if you happen to think that the nearly $400 an ounce drop in the price of gold since it peaked in 2011 is no big deal, have a look at these two graphs. The first is the Case-Shiller house price index from 1987 to 2008. The second is the price of gold from 1985 to 2013.

Of course now that it is semi-official that the gold bubble has burst, isn’t it time to start looking for someone to blame it on? I mean we blamed Greenspan and Bernanke for the housing bubble, right. There must be someone (or two, or three) to blame for the gold bubble.

Juliet Lapidos, on the editorial page editor’s blog of the Times, points an accusing finger at Ron Paul, dredging up quotes like this from the sagacious Congressman.

As the fiat money pyramid crumbles, gold retains its luster. Rather than being the barbarous relic Keynesians have tried to lead us to believe it is, gold is, as the Bundesbank president put it, ‘a timeless classic.’ The defamation of gold wrought by central banks and governments is because gold exposes the devaluation of fiat currencies and the flawed policies of government. Governments hate gold because the people cannot be fooled by it.

Fooled by gold? No way.

But the honorable Mr. Paul is surely not alone in beating the drums for gold. If he were still alive, it would have been nice to question Murray Rothbard about his role in feeding gold mania. But we still have Rothbard’s partner Lew Rockwell with us, maybe we should ask him for his take on the gold bubble. Indeed, inquiring minds want to know: what is the Austrian explanation for the gold bubble?