The New York Times finally caught on today that the gold bubble is bursting, months after I had alerted the blogosphere. But even though I haven’t received much credit for scooping the Times, I am still happy to see that word that the bubble has burst is spreading.

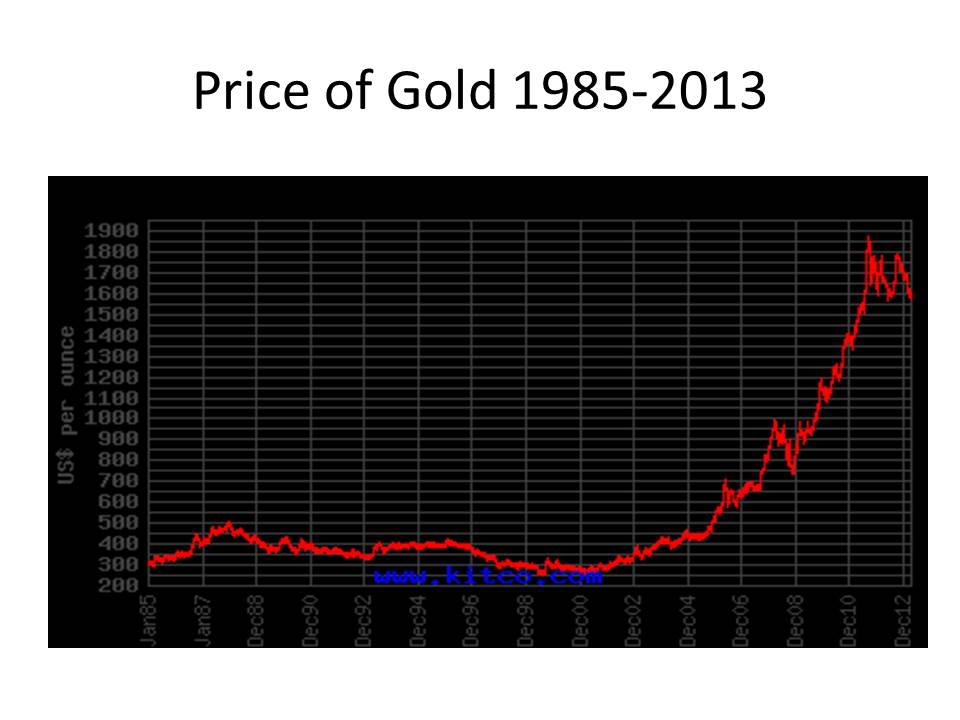

Gold, pride of Croesus and store of wealth since time immemorial, has turned out to be a very bad investment of late. A mere two years after its price raced to a nominal high, gold is sinking — fast. Its price has fallen 17 percent since late 2011. Wednesday was another bad day for gold: the price of bullion dropped $28 to $1,558 an ounce.

It is a remarkable turnabout for an investment that many have long regarded as one of the safest of all. The decline has been so swift that some Wall Street analysts are declaring the end of a golden age of gold. The stakes are high: the last time the metal went through a patch like this, in the 1980s, its price took 30 years to recover.

What went wrong? The answer, in part, lies in what went right. Analysts say gold is losing its allure after an astonishing 650 percent rally from August 1999 to August 2011. Fast-money hedge fund managers and ordinary savers alike flocked to gold, that haven of havens, when the world economy teetered on the brink in 2009. Now, the worst of the Great Recession has passed. Things are looking up for the economy and, as a result, down for gold. On top of that, concern that the loose monetary policy at Federal Reserve might set off inflation — a prospect that drove investors to gold — have so far proved to be unfounded.

And so Wall Street is growing increasingly bearish on gold, an investment that banks and others had deftly marketed to the masses only a few years ago. On Wednesday, Goldman Sachs became the latest big bank to predict further declines, forecasting that the price of gold would sink to $1,390 within a year, down 11 percent from where it traded on Wednesday. Société Générale of France last week issued a report titled, “The End of the Gold Era,” which said the price should fall to $1,375 by the end of the year and could keep falling for years.

Granted, gold has gone through booms and busts before, including at least two from its peak in 1980, when it traded at $835, to its high in 2011. And anyone who bought gold in 1999 and held on has done far better than the average stock market investor. Even after the recent decline, gold is still up 515 percent.

But for a generation of investors, the golden decade created the illusion that the metal would keep rising forever. The financial industry seized on such hopes to market a growing range of gold investments, making the current downturn in gold felt more widely than previous ones. That triumph of marketing gold was apparent in an April 2011 poll by Gallup, which found that 34 percent of Americans thought that gold was the best long-term investment, more than another other investment category, including real estate and mutual funds.

It is hard to know just how much money ordinary Americans plowed into gold, given the array of investment vehicles, including government-minted coins, publicly traded commodity funds, mining company stocks and physical bullion. But $5 billion that flowed into gold-focused mutual funds in 2009 and 2010, according to Morningstar, helped the funds reach a peak value of $26.3 billion. Since hitting a peak in April 2011, those funds have lost half of their value.

“Gold is very much a psychological market,” said William O’Neill, a co-founder of the research firm Logic Advisors, which told its investors to get out of all gold positions in December after recommending the investment for years. “Unless there is some unforeseen development, I think the market is going lower.”

The smart money is getting out fast.

Investment professionals, who have focused many of their bets on gold exchange-traded funds, or E.T.F.’s, have been faster than retail investors to catch wind of gold’s changing fortune. The outflow at the most popular E.T.F., the SPDR Gold Shares, was the biggest of any E.T.F. in the first quarter of this year as hedge funds and traders pulled out $6.6 billion, according to the data firm IndexUniverse. Two prominent hedge fund managers who had taken big positions in gold E.T.F.’s, George Soros and Louis M. Bacon, sold in the last quarter of 2012, according to recent regulatory filings.

“Gold was destroyed as a safe haven, proved to be unsafe,” Mr. Soros said in an interview last week with The South China Morning Post of Hong Kong. “Because of the disappointment, most people are reducing their holdings of gold.”

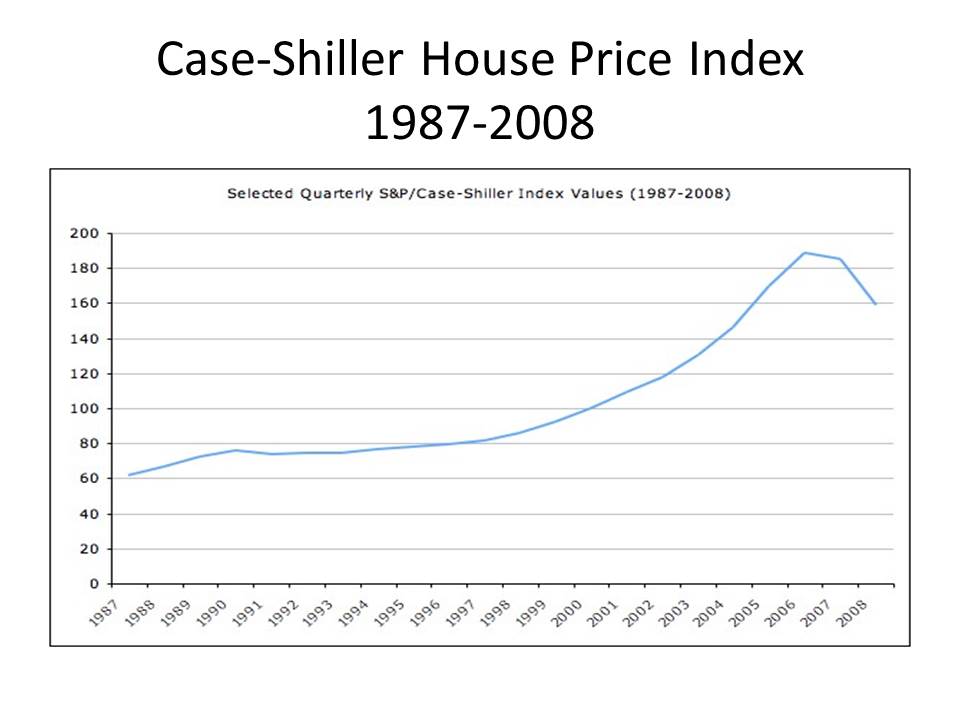

And if you happen to think that the nearly $400 an ounce drop in the price of gold since it peaked in 2011 is no big deal, have a look at these two graphs. The first is the Case-Shiller house price index from 1987 to 2008. The second is the price of gold from 1985 to 2013.

Of course now that it is semi-official that the gold bubble has burst, isn’t it time to start looking for someone to blame it on? I mean we blamed Greenspan and Bernanke for the housing bubble, right. There must be someone (or two, or three) to blame for the gold bubble.

Juliet Lapidos, on the editorial page editor’s blog of the Times, points an accusing finger at Ron Paul, dredging up quotes like this from the sagacious Congressman.

As the fiat money pyramid crumbles, gold retains its luster. Rather than being the barbarous relic Keynesians have tried to lead us to believe it is, gold is, as the Bundesbank president put it, ‘a timeless classic.’ The defamation of gold wrought by central banks and governments is because gold exposes the devaluation of fiat currencies and the flawed policies of government. Governments hate gold because the people cannot be fooled by it.

Fooled by gold? No way.

But the honorable Mr. Paul is surely not alone in beating the drums for gold. If he were still alive, it would have been nice to question Murray Rothbard about his role in feeding gold mania. But we still have Rothbard’s partner Lew Rockwell with us, maybe we should ask him for his take on the gold bubble. Indeed, inquiring minds want to know: what is the Austrian explanation for the gold bubble?

I don’t know what the Austrian explanation for the gold bubble bursting is, but I’d blame it on a gradual improvement in expected returns on investment.

When expected returns are falling or negative, it makes sense to hoard commodities with low storage costs rather than bearing a negative/worsening return on capital. Gold prices will rise. As gold and other commodity prices are now falling, I wonder if this an indication of an underlying improvement in expected returns, which would diminish the attractiveness of buying and holding storable commodities.

LikeLike

To me, I am not sure about the extent of overvaluation of gold. There might be, in part, a case of overshooting in a largely rational scramble for higher rates of return because of the problem of the zero lower bound. At least that’s an explanation that makes sense to me. David, do you believe this is a potentially valid viewpoint? Good post!

LikeLike

Really, the gold bubble burst? is there a gold bubble? It is the first time in history I think, that a bubble is as accurate predicts. Central bank assets have tripled in five years and they stop not, on the contrary, look at Japan. It is not the price of gold that goes up but the fiat money that continuously devalue.

LikeLike

As the fiat money pyramid crumbles, Bitcoin retains its luster. Rather than being the barbarous relic Keynesians have tried to lead us to believe it is, Bitcoin is, as the Bundesbank president put it, ‘a timeless classic.’ The defamation of Bitcoin wrought by central banks and governments is because Bitcoin exposes the devaluation of fiat currencies and the flawed policies of government. Governments hate Bitcoin because the people cannot be fooled by it.

LikeLike

What a relief. People might actually feel safe wearing jewelry again, without having to hire bodyguards to do so.

LikeLike

JP, In an equilibrium model of the value of gold, its value, like that of any storable good, is inversely related to the real rate of interest. So you are describing an equilibrium relationship not a bubble.

Julian, Thanks. I’m not sure. To me it just seems that gold, which is almost totally useless, with huge stockpiles just waiting to be dumped on the market is just about the worst store of value I could imagine, which I guess makes it an ideal investment for someone with the mental capacity of Ron Paul.

Pascal, As I write this, gold is down $65 since yesterday, crashing through the $1500 barrier.

negativeinterest, You certainly have a way with words.

Becky, Your worries are over!

LikeLike

On the Fox News channel, advertisers want to sell you gold coins. On every other channel, advertisers want to buy your gold jewelry.

I’m not sure what to conclude from that, other than the gold price increase has been good for middlemen.

LikeLike

I actually assumed the last sentence was a rhetorical question – and a masterful one at that!

LikeLike

David,

Thanks for the response. I’m just thinking that the perceived probability of the “release” of those large reserved may be very low. That, to the extent that there is any rational reason to acquire gold as an asset, it would probably mostly be because of expected yields from rising market values. I think investors have gotten it very, very wrong, but I think it may be at least partially be because of the zero-lower bound… People searching for what they think promises relatively safe returns… I think the price of gold has been far too high for this purpose. I thought this could be an area of agreement. To my way of thinking, if the Fed does the kind of easing that is needed to restore monetary equilibrium in a Wicksellian/NeoWicksellian sense, high values of gold may temporarily be expected, but should decline along with bond prices and maybe even stock prices, if their values are in part determined by a desperate scramble for returns on investment (although there would be countervailing tendencies).

LikeLike

Julian, The problem I have with your story is that I see a real disconnect between the absence of good profit opportunities and the quest for profits. You can’t just wish profits into existence, which is what saying that people don’t have any profitable investment opportunities to pub the their spare cash so instead they bid up the price of gold to ridiculous heights. That’s taking Keynes’s beauty contest theory of asset markets two or three steps beyond where even Keynes was willing to take it. And I say this as someone who is very far from being a devote of the efficient markets hypothesis. But I also don’t think that you can simply assume that investors as a class are a bunch of idiots. I don’t think that’s what you want to do, but somehow it sounds a bit like that to my ear.

LikeLike

Let me withdraw what I said about stocks… I looked at the latest data on corporate bond yields, gold prices, the stock exchange indices (s&p 500 and dow jones) and it makes me feel like recovery may be in the offing… Rising corporate bond yields, declining gold value, rising stock market… The thing abt stocks, as far as I am concerned, is that relative booms in stocks can be facilitated by a recovery, but also a search for yields in a low-interest market which is dominated by the zlb (at least that’s a starting pt).

LikeLike

I think the “who’s to blame ?” question is brilliant.

LikeLike

I guess what I’m trying to express, which I think is being misread is that there is a compression of the yield curve and the rate of return differentials between higher risk and lower risk investment is likewise compressing. Is that clearer?

LikeLike

I’m sorry if the tone of the last comment may seem negative, I should have said that maybe I am not expressing myself well. My apologies.

LikeLike

I suspect the column’s sentiments are a tad bit premature. Gloating might be in order after the Fed removes its support for buying in excess of 80% of new government debt issuance monthly and after we see the economy show improvement unaided by government supports for housing sales.

LikeLike

The US constitutes 4% of the gold market, India and China consume 20%. Then when the India government starts restricting gold imports, by all means lets blame US politicians.

LikeLike

Many fathers with daughter’s to get marry will have a sigh of relief

LikeLike

Max, Sounds like advertisers know where the suckers are.

Ravi, It was rhetorical, thanks.

Julian, I don’t disagree with you that rising stock prices can be an indicator of expectations of a recovery. I don’t see how low interest rates can raise stock prices very much unless investors are also expecting increased profits.

Robert, Thanks.

Otiose, Was I gloating? Anyway what does any of that have to do with the price of gold?

G3V, I wasn’t blaming US politicians for the rise in the price of gold. I was pointing out that there are those who claim that the dollar is being debased and gold is the only or best way to avoid losing one’s savings.

Mathews, Good for the fathers and the daughters.

LikeLike

Prof. Glasner,

Perhaps I am confused on that point, but I was thinking that, in effect, one could imagine that, with limited investment opportunities because entrepreneurs are not terribly interested in investing in a future economy which they expect to remain depressed considerably into the future (like, say, 2020, as an example). With that limitation, but a lot of liquidity out there (liquidity trap conditions), interest rates would plunge because of a rush for relatively safe financial products (treasuries, highly rated corporate paper, etc.). It occurs to me it may even make perceived “safe stocks” seem attractive investments. The risk premia seem to have been considerably less than what is typical. As I see it, the flip side of this may be an apparent boom in the stock market. I admit the idea seems odd, but I wonder whether it might be possible and maybe even a feature of the not-so-distant past. I guess I have to add a caveat, that the same feature might be present if irrational pessimism caused a deeper decline in stocks than was called for in the “crash” phase of our lesser depression.

LikeLike

Can I propose a suspect to be vilified on the main square of the global village for the gold bubble?

I’d like to nominate traders. If you look at your graph, at the same moment as gold starts its price hike around 2005, there is also the apparition of short-lived peaks which were absent before. Where can this volatility come from? Traders!

Plenty of economists will be all too keen to testify on this type of findings.

LikeLike

Regarding the report from the South China Morning Post on George Soros…the Institute for New Economic Thinking was in Hong Kong for its annual conference, and the SCMP didn’t report on it!

Hong Kong’s primary English-language newspaper covers Soros’s remarks on markets, and yet it can’t (or won’t) cover Soros’s little venture at reforming the study of economics and the economics profession?

It’s depressing.

As for the gold bubble, well, haven’t gold prices rise and fell more than once already in the past five or so years? I remember reading somewhere that gold prices rocketed during the global financial crisis of 2007/2008 (and they stayed at pretty high levels when Lehman Brothers went under), but eventually, as monetary and fiscal actions taken by government were enacted to stabilise the economic situation, gold prices eventually fell.

Of course, I could be wrong…

LikeLike

Julian, What I am having trouble with is the idea that just because the interest rate is low (reflecting pessimism) the corresponding asset valuation of expected cash flows from assets is not necessarily irrational. So just pointing out that low interest rates increase asset values does not show that there is a bubble, even if asset values will fall once interest rates rise (that is, unless expected cash flow increase by even more than interests rates rise). So to show a bubble, you have to show that somehow anticipated cash flow are irrationally high. I don’t think that your argument really addresses that issue.

Max, I am not a great fan of traders, but I don’t think that traders on their own are capable of creating a bubble, there have to be people out there willing to hold the assets being traded.

Blue Aurora, I think that I read on Bloomberg today that gold has risen in price for 12 consecutive years.

LikeLike

There’s an old saying about an ounce of gold being able to buy high-end business attire in all cultures and times…that suggests gold should be about $800-$1100 (Armani). It’ s a great storehouse of value considering that, but that doesn’t mean it’s immune to speculative bubbles.

LikeLike

Prof. Glasner,

What I tried to say (you can judge whether I did or didn’t) was that the natural interest rate (Wicksellian/neowicksellian/new keynesian) could be lower than is achievable by the market. Investment is insufficient to satisfy market equilibrium with respect to savings. I suppose if you want to argue that the liquidity trap condition also entails a bubble in bonds, etc., you can, but I don’t see that my suggestion is not just a possible outcome in liquidity trap conditions.

LikeLike

People who understand the fundamentals are not scared at all. What put an end to Golds last run in 1980 was Fed interest rates staying above 10% for six and a half years straight, to stop the decline of the dollar, with rates climbing above 15% for a third of that time.

You know it is time to sell your gold when the Fed funds rate is 10%+ and the economy doesn’t implode. Of course anyone who does any research on the subject knows that the Fed has painted itself into a corner. If it keeps rates low forever, the inflation will eventually become painfully obvious to everyone and there will be an eventual run on the dollar. If the Fed raises rates to even 4%, all the major banks go bust as the money they make holding 10 year treasuries turn to massive losses. With the Fed no longer buying new bonds, the Federal government is also forced to default on its debts. Either outcome means gold goes up against fiat currencies.

These sharp drops just flush out the speculators, who were getting tired of gold not climbing while the inflation driven stock market was reaching new highs. We’ve seen this time and time again in the last 12+ years in gold. Anyone with a brain is not buying gold with the expectation that they’re gonna be able to sell it in 6 months. You’re buying it for 10+ years down the road or for when the crash hits.

Yea it does suck to be on the lifeboat while people are still partying on the sinking ship, but when it starts to take the final plunge, you’ll be glad you didn’t try to time the market.

LikeLike

Ah, gold. It fevers the brain, enfeebles logic, makes imbeciles out of otherwise stalwart men.

My grandfather once said to me, maybe 50 years ago, “Remember, son, all gold is fool’s gold.”

Still true.

The value of gold is set by some incalculable metric deep inside the latest buyer’s cortex. An ounce of gold is worth a well-made suit—a definition fat enough to drive an 18-wheeler through. How well made? and where? Three-piece?

An ounce of gold is worth so much in oil—except when it is not. And why is natural gas not connected to gold?

Imagine a nation that thinks itself rich, with gold in the vaults. Then it turns out to be lead-plated, the real stuff stolen. So the nation is poor.

Really? The nation has the infrastructure, the educated population, the workforce, the technology, but now it is poor, terrorists stole all the gold and ran away to Wazi-doodoo-stan.

Catastrophe!

LikeLike

mark, Interesting.

Julian, In a liquidity trap the rate of interest consistent with full employment is less than the market rate of interest. But the reason that there is a liquidity trap is that entrepreneurial expectations are very pessimistic. An economic recovery is likely to be associated with more optimistic expectations, so the whole situation is difficult to model in terms that are consistent with the dichotomy between rational and irrational expectations that underlies the analysis of a bubble.

Benjamin Allen Whetham, Thanks for spelling it all out for me. You are as much a speculator as the short-term investor. You are speculating that other people will eventually increase their demand for gold, not because of any service that gold provides, but because they will think that gold will increase in value.

Benjamin Cole, Gold has very little fundamental value, it is a perfect example of Keynes’s beauty contest theory of asset values.

LikeLike

No way that Gold will go down all the way. This movement is because central bankers cannot allow Gold getting to high. This is why they manipulate the price of Gold. I would argue the smart money should be buying Gold right now like crazy. Because now we can get it for a discount. Just take a look at central banks like Russia or China they have been stockpiling Gold for years. There is no way that they will sell any of it. This Gold story just shows that some huge force wants us to believe that we should sell Gold. Don’t fall into it. Instead buy like crazy. Don’t trust fiat currency it will ruin you.

LikeLike

Tas, I sure hope you aren’t following the terrible advice that you are giving to others.

LikeLike

When you look at the price of gold historically, price movements have always experienced ups and downs. The reason why the recent price fall has caused such stir is because it’s the lowest we’ve seen in years. But does that mean that the gold burble has burst? Perhaps this is just another fluctuation in prices. I think that if you are looking for an investment vehicle that will generate some quick cash, gold is not the best option to go for.

LikeLike

Fon, Well, it’s true that the price of gold tends to fluctuate a lot, but the fluctuation in the price of gold is greater than the fluctuation in the price of real estate. So if everyone is ready to say that there is a real estate price bubble, why not say that there was a gold price bubble. So my post was aimed as much at the idea of a bubble as at gold. I don’t say that there are never bubbles, I am just saying that the term is applied pretty loosely. Having said all that, I would add that the services provided by gold are so meager compared to those provided by, say, houses that I have difficulty ascribing attributing any substantial value to gold except from an expectation that it will have a high future value. And i don’t know what rational (fundamental) basis there is for expecting that it will have a future value above the value generated by its current (minimal) real service flow.

LikeLike