After my previous post comparing the neoclassical synthesis in its various versions to the mind-body problem, there was an interesting Twitter exchange between Steve Randy Waldman and David Andolfatto in which Andolfatto queried whether Waldman and I are aware that there are representative-agent models in which the equilibrium is not Pareto-optimal. Andalfatto raised an interesting point, but what I found interesting about it might be different from what Andalfatto was trying to show, which, I am guessing, was that a representative-agent modeling strategy doesn’t necessarily commit the theorist to the conclusion that the world is optimal and that the solutions of the model can never be improved upon by a monetary/fiscal-policy intervention. I concede the point. It is well-known I think that, given the appropriate assumptions, a general-equilibrium model can have a sub-optimal solution. Given those assumptions, the corresponding representative-agent will also choose a sub-optimal solution. So I think I get that, but perhaps there’s a more subtle point that I’m missing. If so, please set me straight.

But what I was trying to argue was not that representative-agent models are necessarily optimal, but that representative-agent models suffer from an inherent, and, in my view, fatal, flaw: they can’t explain any real macroeconomic phenomenon, because a macroeconomic phenomenon has to encompass something more than the decision of a single agent, even an omniscient central planner. At best, the representative agent is just a device for solving an otherwise intractable general-equilibrium model, which is how I think Lucas originally justified the assumption.

Yet just because a general-equilibrium model can be formulated so that it can be solved as the solution of an optimizing agent does not explain the economic mechanism or process that generates the solution. The mathematical solution of a model does not necessarily provide any insight into the adjustment process or mechanism by which the solution actually is, or could be, achieved in the real world. Your ability to find a solution for a mathematical problem does not mean that you understand the real-world mechanism to which the solution of your model corresponds. The correspondence between your model may be a strictly mathematical correspondence which may not really be in any way descriptive of how any real-world mechanism or process actually operates.

Here’s an example of what I am talking about. Consider a traffic-flow model explaining how congestion affects vehicle speed and the flow of traffic. It seems obvious that traffic congestion is caused by interactions between the different vehicles traversing a thoroughfare, just as it seems obvious that market exchange arises as the result of interactions between the different agents seeking to advance their own interests. OK, can you imagine building a useful traffic-flow model based on solving for the optimal plan of a representative vehicle?

I don’t think so. Once you frame the model in terms of a representative vehicle, you have abstracted from the phenomenon to be explained. The entire exercise would be pointless – unless, that is, you assumed that interactions between vehicles are so minimal that they can be ignored. But then why would you be interested in congestion effects? If you want to claim that your model has any relevance to the effect of congestion on traffic flow, you can’t base the claim on an assumption that there is no congestion.

Or to take another example, suppose you want to explain the phenomenon that, at sporting events, all, or almost all, the spectators sit in their seats but occasionally get up simultaneously from their seats to watch the play on the field or court. Would anyone ever think that an explanation in terms of a representative spectator could explain that phenomenon?

In just the same way, a representative-agent macroeconomic model necessarily abstracts from the interactions between actual agents. Obviously, by abstracting from the interactions, the model can’t demonstrate that there are no interactions between agents in the real world or that their interactions are too insignificant to matter. I would be shocked if anyone really believed that the interactions between agents are unimportant, much less, negligible; nor have I seen an argument that interactions between agents are unimportant, the concept of network effects, to give just one example, being an important topic in microeconomics.

It’s no answer to say that all the interactions are accounted for within the general-equilibrium model. That is just a form of question-begging. The representative agent is being assumed because without him the problem of finding a general-equilibrium solution of the model is very difficult or intractable. Taking into account interactions makes the model too complicated to work with analytically, so it is much easier — but still hard enough to allow the theorist to perform some fancy mathematical techniques — to ignore those pesky interactions. On top of that, the process by which the real world arrives at outcomes to which a general-equilibrium model supposedly bears at least some vague resemblance can’t even be described by conventional modeling techniques.

The modeling approach seems like that of a neuroscientist saying that, because he could simulate the functions, electrical impulses, chemical reactions, and neural connections in the brain – which he can’t do and isn’t even close to doing, even though a neuroscientist’s understanding of the brain far surpasses any economist’s understanding of the economy – he can explain consciousness. Simulating the operation of a brain would not explain consciousness, because the computer on which the neuroscientist performed the simulation would not become conscious in the course of the simulation.

Many neuroscientists and other materialists like to claim that consciousness is not real, that it’s just an epiphenomenon. But we all have the subjective experience of consciousness, so whatever it is that someone wants to call it, consciousness — indeed the entire world of mental phenomena denoted by that term — remains an unexplained phenomenon, a phenomenon that can only be dismissed as unreal on the basis of a metaphysical dogma that denies the existence of anything that can’t be explained as the result of material and physical causes.

I call that metaphysical belief a dogma not because it’s false — I have no way of proving that it’s false — but because materialism is just as much a metaphysical belief as deism or monotheism. It graduates from belief to dogma when people assert not only that the belief is true but that there’s something wrong with you if you are unwilling to believe it as well. The most that I would say against the belief in materialism is that I can’t understand how it could possibly be true. But I admit that there are a lot of things that I just don’t understand, and I will even admit to believing in some of those things.

New Classical macroeconomists, like, say, Robert Lucas and, perhaps, Thomas Sargent, like to claim that unless a macroeconomic model is microfounded — by which they mean derived from an explicit intertemporal optimization exercise typically involving a representative agent or possibly a small number of different representative agents — it’s not an economic model, because the model, being vulnerable to the Lucas critique, is theoretically superficial and vacuous. But only models of intertemporal equilibrium — a set of one or more mutually consistent optimal plans — are immune to the Lucas critique, so insisting on immunity to the Lucas critique as a prerequisite for a macroeconomic model is a guarantee of failure if your aim to explain anything other than an intertemporal equilibrium.

Unless, that is, you believe that real world is in fact the realization of a general equilibrium model, which is what real-business-cycle theorists, like Edward Prescott, at least claim to believe. Like materialist believers that all mental states are epiphenomenous, and that consciousness is an (unexplained) illusion, real-business-cycle theorists purport to deny that there is such a thing as a disequilibrium phenomenon, the so-called business cycle, in their view, being nothing but a manifestation of the intertemporal-equilibrium adjustment of an economy to random (unexplained) productivity shocks. According to real-business-cycle theorists, such characteristic phenomena of business cycles as surprise, regret, disappointed expectations, abandoned and failed plans, the inability to find work at wages comparable to wages that other similar workers are being paid are not real phenomena; they are (unexplained) illusions and misnomers. The real-business-cycle theorists don’t just fail to construct macroeconomic models; they deny the very existence of macroeconomics, just as strict materialists deny the existence of consciousness.

What is so preposterous about the New-Classical/real-business-cycle methodological position is not the belief that the business cycle can somehow be modeled as a purely equilibrium phenomenon, implausible as that idea seems, but the insistence that only micro-founded business-cycle models are methodologically acceptable. It is one thing to believe that ultimately macroeconomics and business-cycle theory will be reduced to the analysis of individual agents and their interactions. But current micro-founded models can’t provide explanations for what many of us think are basic features of macroeconomic and business-cycle phenomena. If non-micro-founded models can provide explanations for those phenomena, even if those explanations are not fully satisfactory, what basis is there for rejecting them just because of a methodological precept that disqualifies all non-micro-founded models?

According to Kevin Hoover, the basis for insisting that only micro-founded macroeconomic models are acceptable, even if the microfoundation consists in a single representative agent optimizing for an entire economy, is eschatological. In other words, because of a belief that economics will eventually develop analytical or computational techniques sufficiently advanced to model an entire economy in terms of individual interacting agents, an analysis based on a single representative agent, as the first step on this theoretical odyssey, is somehow methodologically privileged over alternative models that do not share that destiny. Hoover properly rejects the presumptuous notion that an avowed, but unrealized, theoretical destiny, can provide a privileged methodological status to an explanatory strategy. The reductionist microfoundationalism of New-Classical macroeconomics and real-business-cycle theory, with which New Keynesian economists have formed an alliance of convenience, is truly a faith-based macroeconomics.

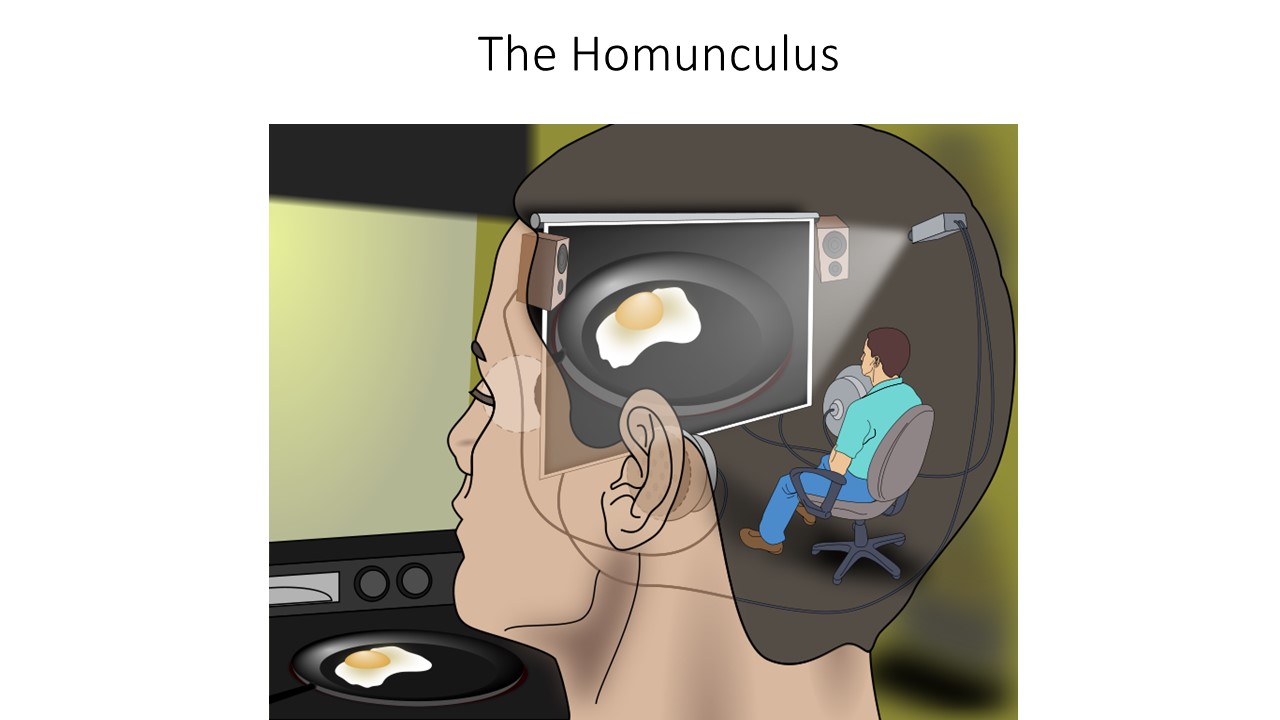

The remarkable similarity between the reductionist microfoundational methodology of New-Classical macroeconomics and the reductionist materialist approach to the concept of mind suggests to me that there is also a close analogy between the representative agent and what philosophers of mind call a homunculus. The Cartesian materialist theory of mind maintains that, at some place or places inside the brain, there resides information corresponding to our conscious experience. The question then arises: how does our conscious experience access the latent information inside the brain? And the answer is that there is a homunculus (or little man) that processes the information for us so that we can perceive it through him. For example, the homunculus (see the attached picture of the little guy) views the image cast by light on the retina as if he were watching a movie projected onto a screen.

But there is an obvious fallacy, because the follow-up question is: how does our little friend see anything? Well, the answer must be that there’s another, smaller, homunculus inside his brain. You can probably already tell that this argument is going to take us on an infinite regress. So what purports to be an explanation turns out to be just a form of question-begging. Sound familiar? The only difference between the representative agent and the homunculus is that the representative agent begs the question immediately without having to go on an infinite regress.

PS I have been sidetracked by other responsibilities, so I have not been blogging much, if at all, for the last few weeks. I hope to post more frequently, but I am afraid that my posting and replies to comments are likely to remain infrequent for the next couple of months.