In my previous post, I tried to relate the discussion of accounting identities to the familiar circular-flow diagram with injections into and leakages out of the flows of income, expenditure and output. My hopes that framing the discussion in terms of injections and leakages, with investment viewed as an injection into, and savings as a withdrawal out of, the flows of income and expenditure would help clarify my position about accounting identities were disappointed, as defenders of those accounting identities were highly critical of the injections-leakages analogy, launching a barrage of criticism at my argument that the basic macroeconomic model of income determination should not be understood in terms of the income-expenditure or the investment-savings identities.

I think that criticism of the injections-leakages analogy was, for the most part, misplaced and a based on a misunderstanding of what I have been aiming to do, but much of the criticism was prompted by my incomplete or inadequate explanation of my reasoning. So, before continuing with my summary of Lipsey’s essay on the subject, on which this series is based, I need to address at least some of the points that have been made by my (and Lipsey’s) various critics. In the course of doing so, I believe it will be helpful if I offer a revised version of Lipsey’s Table 1, which I reproduced in part III of this series.

First, I am not saying that the standard accounting identities are wrong. Definitions are neither right nor wrong, but they may be useful or not useful depending on the context. In everyday conversation, we routinely ascribe one of many possible meanings to particular words used by selecting one of the many possible definitions as that which is most likely to make an entire sequence of words – a phrase, a clause, or a sentence – meaningful. Our choice of which definition to use is generally determined by the context in which the word appears. Choosing one definition over another doesn’t mean that others are not valid, just that the others would not work as well or at all in the context in which the word in question appears. Working with an inappropriate definition in a given context can lead, as we all know from personal experience, to confusion, misunderstanding and error. Defining savings and investment to be equal in every state of the world is certainly possible, and doing so is not invalid, but doing so is not necessarily useful in the context of formulating a macroeconomic theory of income determination.

There are two reasons why defining savings and investment to be identically equal in all states of the world is not useful in a macroeconomic theory of income. First, if we define savings and investment (or income and expenditure) to be identically equal, we can’t solve, either algebraically or graphically, the system of equations describing the model for a unique equilibrium. According to the model, aggregate expenditure is assumed to be a function of income, but if income and expenditure are identical, expenditure is simply identical to itself, so the system of equations described by the model collapses onto the 45-degree line representing the expenditure-income identity.

Second, even if we interpret the equality of income and expenditure as an ex ante equilibrium condition, while asserting that identity between income and expenditure must always hold ex post, the ex post definitional equality tells us nothing about the adjustment process that restores equilibrium when, owing to some parameter change that disturbs a pre-existing equilibrium, the ex ante equilibrium condition does not hold. For a dynamic adjustment path to take the model from one equilibrium to another via a sequence of discrete adjustments, the model must incorporate some lags. Without lags, the adjustment would be instantaneous, and the model would move from its old equilibrium to a new equilibrium in one fell swoop. But in the course of a sequence of partial adjustments, savings and investment will typically have to be defined by the model so that they are not equal, and this will be reflected in the implied course of savings and investment if the model is worked out period-by-period. Or if you were to observe the Phillips machine (a hydraulic macroeconomic model built by A. W. Phillips of Phillips Curve fame) in action, you could actually see that the savings and investment flows were of unequal magnitudes as machine responded to a change in the settings and moved from one hydraulic equilibrium to another.

It is a common mistake, and the primary object of Richard Lipsey’s scorn in his essay, to attribute causal significance to the savings-investment identity, as if it were the force of the identity itself that guided the dynamic adjustment, when, in reality, the identity, which can always be recovered if one does all the necessary accounting and classifies all the transactions according to the accounting conventions, is irrelevant to the adjustment path. Doing the accounting does not explain how the model moves from the old to a new equilibrium; it just assures us that nothing has been omitted from a final description of what has happened. Rather, the causal mechanism driving the adjustment process can be described using the intuitive idea that income changes because there are injections (in the form of investment) into the income and expenditure flows and leakages (in the form of savings) out of those flows, and when the injections and leakages are unequal in magnitude, the discrepancy between the injections and the leakages causes a corresponding change in the income and expenditure flows.

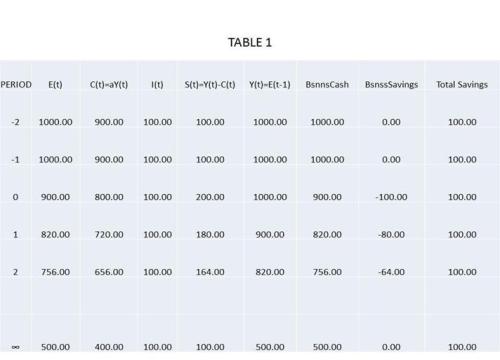

One commenter pointed out that, even in the numerical example (taken from Lipsey’s essay) that I gave in my earlier post, the sequence of adjustments preserved the definitional equality between savings and investment and income and expenditure, even though the verbal explanation of the adjustment process showed that the equality of savings and investment required a rather forced interpretation of the meaning of savings: the difference between the cash balance expected at the end of a period and the actual cash balance at the end of the period. This peculiar interpretation of savings and its equality with investment reflected the way that Lipsey chose to introduce a lag between expenditure and income into the model: by assuming that income was disbursed by businesses to households at the end of the period in which households provide services to businesses. The income received at the end of one period is then used to finance consumption expenditures and savings in the following period.

I should have pointed out that if one made the trivial adjustment in the expenditure-income lag, so that incomes earned in one period are not at the end of the current period, but at the beginning of the following period, then income and expenditure and savings and investment would not remain equal over the course of the adjustment from the old to the new equilibrium. The sequence of adjustments under the alternative assumption is shown in Table 1 below.

Of course, if we assume that there is a one-period lag between expenditure and income, one could define something called total savings, which would be household savings plus business savings, where business savings is defined as the difference between cash held by businesses at the end of the current period and cash held by businesses at the end of the previous period. And total savings is identically equal to investment. However, it is important to bear in mind that from the point of view of the simple income-expenditure model, the relevant causal variable in determining equilibrium is not total savings, but household savings.

Why do I say that household savings, not business savings, is the relevant causal factor in determining equilibrium income in the simple income-expenditure model? The reason should be obvious: the solution for equilibrium in the simple income-expenditure model is Y = A/(1 – MPC), where A represents the autonomous component of consumption plus planned investment by business firms and MPC is the marginal propensity to consume by households, so that (1 – MPC) is the marginal propensity to save (MPS) . . . by households!

In this setup, business savings is a pure residual adjusting to make up the difference between household savings and investment. When household savings exceeds investment, businesses accumulate their holdings of cash, and when investment is greater than household saving, businesses reduce their accumulate cash. The operation of the banking system might be relevant at this point, but that analysis would take this discussion to a whole new level, which I am not going to get started on at this point.

I will close at this point by just saying that I think that I have provided an answer to the following comment on my previous post asking what is gained by introducing an alternative set of definitions of saving and investment under which savings and investment are equal only in equilibrium, but not otherwise:

But let’s just say you have a system of accounts where definitions are different and saving is different from investment. I can do a mathematical transformation to a new set of variables in which standard identities hold. What is the point of writing so much? Absolutely nothing.

The point of course is that by defining savings and investment so that they are equal only in equilibrium, we now have a system of two linear equations in two unknowns that can be solved for a unique solution, something that cannot be done if savings and investment are identically equal. Second, when we have defined savings and investment so that they can be unequal, but define their equality to be a condition of equilibrium, we can write the following dynamic relationships characterizing the system:

dY/dt = 0 <=> I = S

dY/dt > 0 <=> I > S

dY/dt < 0 <=> I < S

where I and S are defined under the behavioral assumptions in this example as actual investment by businesses and saving by households. The precise definition of I and S would depend, in each particular case, on the specific behavioral assumptions about the underlying lag structure of the model for that particular case. The definitional equality of total savings and investment has no causal significance, but simply reflects the fact that total savings is defined in such a way that it must equal investment.

The definitional equality of savings and investment, as Scott Sumner has observed, is exactly analogous to the quantity identity MV ≡ PY, when V is treated not as the reciprocal of the amount of money demanded as a fraction of income — which is to say as a measurable magnitude understood to be a function of specifiable independent variables — but simply as a residual whose value, by definition, must always be identically equal to PY/M. The quantity identity, lacking being consistent with all possible states of the world, because V is defined not as an independent variable, but as a mere residual. The quantity identity is therefore of no use in describing the dynamic process of adjustment to a change in the quantity of money or what in telling us what are the causes of such a process.

UPDATE (3/29/15): In writing a response to Jamie’s comment, I realized that in the third paragraph after the table above, I misstated the relationship between business savings and the difference between investment and household savings. I have made the correction, and apologize for not being more careful.

This was stated much more simply & effectively by Marriner Eccles, in 1938

https://fraser.stlouisfed.org/scribd/?item_id=465651&filepath=/docs/historical/eccles/077_03_0002.pdf#scribd-open

LikeLike

There are two reasons why defining savings and investment to be identically equal in all states of the world is not useful in a macroeconomic theory of income.

Your definition of saving please?

First, if we define savings and investment (or income and expenditure) to be identically equal, we can’t solve, either algebraically or graphically, the system of equations describing the model for a unique equilibrium

This is simply wrong. It’s hilarious.

LikeLike

To be even clearer, your posts simply read:

“Accounting is wrong”.

But that’s not the end. You attempt to hedge your posts by also claiming “accounting is right”, so that nobody can accuse you of claiming “accounting is wrong”.

But all your posts simply read: “accounting is wrong”.

LikeLike

Ramanan:

“This is simply wrong. It’s hilarious.”

I don’t think so. The post is a clear explanation of two ways in which variables can be equal, only one of which is useful.

Your comment, on the other hand, is so empty that it can only inform us that you failed to understand the post.

LikeLike

I continue to think that part of the confusion stems from what was at least a plausible (early) 19th century argument, which, in fact, I believe “classical” economists made.

Divide the economy into two groups, “workers” and “capitalists.” *Assume* that workers spend their entire income on consumption. And that “capitalists” spend part of their income on consumption and “save” the rest–but that their saving is in the form of reinvestment in their businesses. In this case, saving *is* investment.

As soon as we have “workers” who save, and “capitalists” who do things other than run businesses, the act of saving becomes separated from the act of acquiring new capital goods. And for some reason in thinking about national income accounting, some people never got past the first stage.

LikeLike

+1 to what elwailly said.

LikeLike

David: for your fault 😉 I’m reading a lot about this topic. I think that the nuclear problem is the break of Keynes from de classical theory of “natural” interest rate that equate saving & investment.

More frequently than not, economist & politics more or less classics (including MM) confound the account identity with the equilibrium condition of S=I thanks to the interes rate adjusted to the “natural rate”. So, an increase in saving would be followed by an increase in investment.

Thank you for your clever post!

LikeLike

I think part of the problem here is that you are thinking of savings as a causal factor. That is indeed problematic if savings and investment are identically equal. It is better to think of the propensity to save as the causal factor and savings as an outcome.

LikeLike

Roger Erickson, Thanks for the link. I took a quick look, but the document is a 25-page speech., which seems to be mainly a defense of the government’s attempt to stimulate the economy in the 1930s under FDR. So I would appreciate it if you could point me to a particular passage that addresses the point that I was trying to make, however inadequately.

elwailly, Thanks very much for your response to an unpleasant comment that I had decided not to respond to myself.

Don, An interesting idea, but I am not so sure that classical writers believed that all funds invested in businesses were generated by the profits accruing to the owners of existing businesses. But I haven’t read much of the classical writers on interest and what I have read was read decades ago, so I am not going to say that you are wrong.

Rob, Thanks.

Miguel, I’m glad that these posts have been of interest to you. You are certainly right that Keynes introduced the savings investment identity as an alternative to neo-classical theory of interest, and wanted to use it to reject the idea that rate of interest adjusts to equate savings and investment. That got him into a huge muddle, which Hawtrey, Robertson, Haberler, and Lutz immediately criticized him for. For some reason the savings investment identity was reintroduced into the macroeconomics textooks in the 1950s by Samuelson, among others, and led to the confusion that Lipsey tried to dispel in his wonderful essay.

LikeLike

“I don’t think so. The post is a clear explanation of two ways in which variables can be equal, only one of which is useful.

Your comment, on the other hand, is so empty that it can only inform us that you failed to understand the post.”

elwailly,

Going by your argument everything in the internet is right: either the author or some supporter says “this post is clear, you fail to understand”. What an argument!!

LikeLike

I have a post here

Nothing new. Just a record of the quote “we can’t solve” (!!!) and a quote by Tobin.

LikeLike

David–I’m not sure that classical economists believed all funding for investment came from retained earnings; I do think they used that as a plausible simplification. (And that’s the problem with plausible simplifications, I think.)

LikeLike

As I’ve said before, this debate is predominantly about definitions of terms.

In Table 1, as you point out, the column I (t) and the column Total Savings are identical in every period. Hence, the identity holds if you use those columns. On the other hand, the column I (t) does not equal the column S (t). It is only possible to have a sensible conversation on identities if definitions and assumptions are properly documented.

In your latest example,

I (Business) = S (Households) + S (Business) = S (Whole economy)

In earlier discussions, you appeared to be assuming that S (Business) was zero i.e. there was no retained profit and no operational business loss. In that case,

S (Business) = 0

As a result,

I (Business) = S (Households) = S (Whole economy)

This is entirely consistent. When S (Business) equals 0, it doesn’t matter whether you define S to be S (Households) or S (Whole economy). If S (Business) does not equal zero, it does matter. You must use S (Whole economy) for the identity to hold.

This problem has got nothing to do with time lags and it’s got nothing to do with whether you can solve a particular set of equations. You appear to have solved your equations even though I = S (Whole economy) in every period in your example. The problem is about definitions and assumptions.

The root cause of the ambiguity in this debate can be traced back to that fact that the context diagram you included near the start of your Bathtubs post is not fit for the purpose of helping to define the vocabulary you are using in your posts. For example, there is no injection corresponding to household spending in the diagram. Also, there is only one saving, so the diagram does not support the separate discussion of business saving and household saving.

I agree that it makes sense to focus on S (Households) in your period by period calculations. The Business Cash column is, effectively, dead money. Businesses will not spend money unless they believe that it will contribute to sales but, by not distributing it to households in dividends, businesses prevent anyone else from spending it either.

LikeLike

“You appear to have solved your equations even though I = S (Whole economy) in every period in your example.”

Nice point Jamie. Nice comment overall.

LikeLike

David,

I don’t think either of us is going to succeed in convincing the other on this, so I’m just going to say that I think we agree on what I believe is the most important point here, being that accounting identities tell us nothing about behaviour. In particular, it is wrong to conclude that investment levels can be deduced by considering saving behaviour alone, regardless of how these terms are defined. Also that we cannot deduce equilibrium conditions simply from accounting definitions, nor can we say what happens out of equilibrium. Finally, and perhaps least obviously, that if terms are defined so that they are identically equal, it makes no sense to ask what mechanism it is that ensures they are equal.

LikeLike

Nick,

Finally, and perhaps least obviously, that if terms are defined so that they are identically equal, it makes no sense to ask what mechanism it is that ensures they are equal.

I think it does make sense. Perhaps the question should be asked differently. From a purely mathematical and modeling point of view, it seems it makes no sense to ask what mechanism it is that the variables in an identity are equal. We just use them as input to our model and hence that itself is an explanation of their truth.

However, from an economic viewpoint, it is not so satisfying as one is still left with a question as to how it is that they are equal. One one hand we have economic units making decisions on capital formation and on the other we have units making decisions on saving. How is it that saving = investment always?

Neoclassical authors typically use the price mechanism for everything. So interest rate in this example (with the rate of interest as “price”). They always use the price mechanism for everything. Keynes argued all this is wrong and went on to show how the story is wrong in everything.

Here’s Joan Robinson on this:

“For purposes of theoretical argument we are interested in causal relationships, which depend on behavior based on expectations, ex ante, whereas the statistics necessarily record what happened ex-post… An ex-post accounting identity, which records what has happened over, say, the past year, cannot explain causality; rather it shows what has to be explained. Keynes’ theory did not demonstrate that the rate of saving is equal to the rate of investment, but explained through what mechanism the equality is brought about.”

My view about all this is exactly opposite of Glasner: accounting identities are revelations.

LikeLike

I agree with Nick on “Finally, and perhaps least obviously, that if terms are defined so that they are identically equal, it makes no sense to ask what mechanism it is that ensures they are equal.’

In David’s example it is the behavioral assumption about consumers spending a % of income, and businesses always investing $100, while correctly anticipating consumption that drives the model (and allows one to track the series of adjustment that occurs when the behavioral assumption about consumption changes from 90% to 80% of Y).

“Total Savings” is just a derived value entirely dependent upon the other values driven by the behavioral assumption and will always equal I , and doesn’t add much to the narrative.

My only quibble is this. David could have named “Total Savings” as “Savings” (S) to keep the accounting geeks happy, and used a different term (“saved Income?”) for his S , and driven the same results with less scope for terminology nit-picking that has hindered and confused the discussion IMO.

LikeLike

To summarize a different view:

If one is opposed to national income accounting as the measurement foundation for a model of national income determination, there’s little hope for a coherent result in simulating a real world process that gets routinely measured using real world accounting entries. Cost accounting for expenditures sums up to what factors of production earn as income. If one denies that, then you deny the role of cost accounting and income accounting.

Actual expenditure equals actual income.

In the simplified 2 sector model, the measured quantity of actual investment equals actual saving.

In that context, I think the national income determination model you portray is incorrect from the outset– even before getting to the bathtub model.

The model that I understand is based on the idea of planned expenditure versus actual expenditure and income, the latter two being equivalent in measure, as portrayed on the 45 degree line. The model is based on planned injections and implied withdrawals (leakages) of potentially differing value – not actual injections and actual withdrawals of differing value, because the latter are always equivalent.

The actual economy is always on the 45 degree line.

Consider the simplified two sector model (4 sectors is an easy extension once the basic logic of the identity issue is understood).

On that line, C + I = C + S, and actual injections I equal actual withdrawals S.

The reason for the 45 degree line is that it depicts the relationship between two different things that have the same quantitative measurement in a monetary economy – expenditures on real goods and services on the y axis and income earned in the monetary unit on the x axis.

The planned expenditure line represents planned expenditure as a function of income. Its lesser slope than the 45 degree line reflects the fact that MPC < 1. The line starts at the level of autonomous injections on the Y axis and with a lower slope than 45 degrees intersects the 45 degree line at the equilibrium point where actual E equals actual Y.

Points on such a planning line other than the single point at its intersection with the 45 degree line represent plans for expenditure that are a function of actual income on the x axis, but that do not coincide with corresponding actual expenditure, which must be equal to actual income. Therefore, these non-intersection points are all unrealizable as plans corresponding to their coordinates.

The intersection of the planned expenditure line with the 45 degree line is a potential equilibrium, where planned expenditure equals actual expenditure and income. Plans can be realized at that point. And it is the only point where plans can be realized according to the assumed expenditure function.

Depending on context, the 45 degree line can also depict the economy at points of disequilibrium – for example, when the planned expenditure line suddenly rises or falls from its previous equilibrium level.

For example, suppose the economy starts at an equilibrium point where planned expenditure intersects with the 45 degree line. Suppose planned expenditure then suddenly drops down from there. In the two sector model, this could reflect a planned reduction in investment relative to the counterfactual of no planned reduction in current investment levels. The actual economy is still on the 45 degree line but is now in disequilibrium. The intersection point of the new planned expenditure with the 45 degree line represents a potential future equilibrium point, down to the left and toward the origin of the 45 degree line. Using that new lower potential intersection and equilibrium as a reference point, planned expenditure would fall short of current actual income at income higher levels higher than at that reference point. In the simplified model, planned investment is less than current saving, and so planned injections are less than actual current withdrawal levels.

Actual S and I will always be equal in the two sector model (more generally, actual injections and withdrawals will always be equal), as the economy proceeds toward a new equilibrium point based on the impetus of planned expenditure. With the subsequent “implementation” of the plan to reduce investment, the behavior of actual injections and withdrawals begins to get traction and this is reflected in the continuous satisfaction of the identity. When actual I is reduced relative to the counterfactual of an unchanged I, it follows that actual S and therefore actual Y must decline by the same amount – because of the inviolable accounting identity that portrays how a reduction in I reduces factor income by the same quantity. And as investment is reduced, the multiplier starts to work in reverse, as actual declining incomes result in reduced consumption as well. Depending on the pattern of the actual implementation of the plan, the economy will gradually work its way down to the new equilibrium point (unless otherwise disturbed) through iterative shrinking of I and S and C and Y, until planned E equals actual E and actual Y once again.

Non-equilibrium planning points can never be realized because they are off the 45 degree line. All planning points away from the 45 degree line can only be in effect the wishful plans of planners who do not incorporate the inevitable knock-on income effects of realizing their plans to change expenditures.

This sort of model does not depict a circulating flow of actual injections and actual withdrawals where the two are not equal. There is no such model. Actual injections are always equal to actual leakages. The model instead depicts such differences only in the context of plans for injections and leakages that can never be realized as they are depicted away from that 45 degree line.

Yet a circulating flow of different actual injections and actual withdrawals is exactly what you have described in this series. That is impossible.

It is incorrect, and that is why your bathtub model doesn’t work from the get go.

Second, it certainly appears that your objection to income accounting as the basis for a model of national income determination stems from a lack of familiarity with flow of funds accounting – and implicitly an apparent lack of familiarity with each of income accounting, flow of funds accounting, and balance sheet accounting and the role that each of those financial statement types play in understanding the measurement of economic and financial outcomes. Because what has been proposed is an attempt in effect to convert in some way income accounting to a kind of flow of funds accounting in order to establish some sort of measurement foundation that captures “lags”. But this entirely ignores a standard flow of funds accounting framework that already exists and that is normally used in capturing such cash flow timing differences as a normal complement to income accounting. And ironically, in attempting to create a home grown version of flow of funds accounting, the argument becomes reliant on this customized version of accounting in an attempt to explain behavior. But the behavioral piece comes not from any first order accounting choice. Rather in the model it comes from the marginal propensity to consume assumption and the autonomous injection factors that are built into the planned expenditure equation. It does not come from an attempted bespoke conversion of income accounting to flow of funds accounting, and nor for that matter does it come from the accepted normal accounting system framework.

Flow of funds accounting is already an established standard accounting framework that complements income accounting and helps explain the cash flow nuances that complement income accounting. The primary accounting tool that underpins a national income determination model obviously has to be the accounting tool that measures income – not flow of funds. Flow of funds information is complementary to this, and is easily incorporated into any logical explanation about how behavior unfolds into actual economic transactions.

Third, the criticism that accounting does not explain behavior (or as Sumner puts it that one does not reason from an accounting identity) is certainly valid in cases where that mistake is actually made. For example, within the economics profession, this seemed to have been the case when Krugman wrote his “Dark Age of Macro” post in respect of the reasoning of some members of the Chicago school. But this criticism is also the straw man that the economics profession habitually trots out as a more general indictment of the role and importance of accounting. That sort of generalized attitude is an ignorant reflex from the profession and nothing more. Those who understand the connection between accounting and economics obviously know that accounting does not explain behavior. One has to be ignorant of the role of measurement not to understand that. But as the foundation measurement system for realized economic and financial events, it also constrains the nature of the path of feasible economic outcome in the future. It doesn’t determine them, but it does constrain the characteristic of their path in its own way and shapes the feasibility of what those outcomes can end up looking like in the future – if they materialize in fact. So this fact is tremendously important in forecasting – and in planning – and in risk management.

Fourth, I have no idea how you come to the conclusion that the intersection of the expenditure planning function with the 45 degree line does not determine a unique solution. That conclusion seems to have something to do with a characterization of the expenditure planning function as a function that depicts events that actually happen rather than those which are planned. It is beyond me how one can think that this is not a system of simultaneous equations that determines a unique economy point on the 45 degree line.

Fifth, the issue of the differentiation of saving as between households and businesses is really of minor concern in context. Model the saving nexus of the two sectors as the alternative of assuming a full distribution of earnings as dividends to households – or model it as separate business sector saving and make some reasonable adjustment to the interpretation of MPC as necessary. This is just not a substantive issue for this topic. The required flexibility in interpretation is easy compared to some of the other issues in debate.

The Lipsey/Glasner transformation draws from one part of an established accounting framework (income accounting) in an attempt to construct by implication a hybrid version of a second piece that already exists (flow of funds accounting) and which already works very effectively as part of an interconnected accounting system with several different required parts. This tendency to reinvent something that already exists and works very well seems to be a creative impulse that is quite widespread in the economics blogosphere.

LikeLike

Ramanan,

“I think it does make sense.”

Totally agree

As in Robinson’s “rather it shows what has to be explained”

It’s an accounting mechanism

A form of mathematics after all

LikeLike

Ramanan,

I picked my words carefully. I did not want to exclude the possibility that some form of explanation might be useful in showing how the equality arises from the data.

However, it makes no sense to me to ask, for example, whether it is changes in interest rates or changes in income levels that makes savings equal investment. They are equal for no other reason than we have defined them that way. No mechanism is necessary.

But of course that is not to say that we cannot ask what happens if people’s desire to save or invest changes. And we can talk about what mechanism might reconcile these desires.

It’s like with supply and demand. We can ask what makes the amount people want to buy equal to the amount others want to sell. But we don’t bother asking what makes the quantity actually purchased equal to the quantity actually sold.

LikeLike

Nick,

Agree, my point was that these questions are perhaps not the best worded. But their intuition in the question posed has a point, whether or not their actual proposed solution is right or wrong.

“It’s like with supply and demand. We can ask what makes the amount people want to buy equal to the amount others want to sell”

Yes that’s a nice way to say it. It’s just that other people word it as if the two sides of the identity are somehow not equal at some times, diverge from each other and made equal and things such as that. Some understand that identities are always true but have some other variables such as planned and so on. What the assumed mechanism before Keynes arrived (and still with most economists) is that if people want to save more, interest rates change (perhaps instantaneously) so that investment also rises with saving. But Keynes showed how the causality is from investment to saving and that output is changing while things such as propensity to consume changes and his mechanism is different.

So my point was that there’s still some right intuition (at least at the level of posing a question, although the answer may be wrong) even though it is not the best worded usually.

LikeLike

JKH,

I suspect I may be missing something basic here but I don’t understand “This sort of model does not depict a circulating flow of actual injections and actual withdrawals where the two are not equal. There is no such model. Actual injections are always equal to actual leakages”.

I’m imagining a very simple and unrealistic model were each period investment is funded by newly created money (injections) and people save each period by putting some of their income under the bed (withdrawals). If $100 new dollar bills were printed each period and injected via investment spending and $200 leaked out by being put under the bed, why isn’t this a net leakage ? ( you could define savings as defined by the difference between income and consumption, and guaranteed to be $200 in this simple model no matter what assumptions are made about consumption, but that doesn’t seem to provide an explanation for the decline in income caused by the apparent leakage).

Similarly for the bath tub model. if you take the volume of water in the bath to be income in a given period, and have an input pipe that delivers 100 gallons each period, and an outlet that initially drains 10% of the water each period, then you will start with an equilibrium of 1000 gallons. If you change the outflow from 10% of total content to 20% then the water will drain until you get to a new equilibrium of 500 gallons. In this case outflow exceed inflows until the new equilibrium is reached. Defining S to be the difference between total content minus water that didn’t flow out gives you an equality between S and I (inflow) but not an intuitively very helpful one.

I suppose you could say that the bathtub must be part of larger model where the leakages must go somewhere so are not really lost but that just seems to be dodging the issue which is about explaining the volume of water in the bathtub.

LikeLike

Miguel, I can’t speak for other MMs, but I certainly don’t believe an increase in saving would be “followed by” an increase in investment. Nor do I believe an increase in saving causes an increase in investment. Rather some third factor causes both S and I to change, simultaneously.

And I certainly don’t believe the so-called Wicksellian “natural rate” has any bearing on any of this.

LikeLike

Rob R.

Suppose the central bank does “currency QE” by swapping currency for bonds with private sector counterparty firm F.

Firm F buys newly manufactured capital good from firm G using currency to pay.

Firm G is a fully vertically integrated firm that pays labor and capital the full cost of goods sold using currency. It pays out dividends to its owners.

Labor and the owners hide the currency under the mattress.

The price of the investment good equals what is paid out as income to the factors of production. Other things equal the economy must save all of that income – because no new consumption goods have been produced that can be purchased – only investment goods.

Investment equals saving.

Injections equal withdrawals.

The QE production of currency has nothing to do with the issue at hand. That’s because it is a flow of funds event but not an income event.

LikeLike

Don, Just out of curiosity, which classical economists are you referring to when you say they used the assumption that all funding for investment came from retained earnings?

Jamie, You said:

“This problem has got nothing to do with time lags and it’s got nothing to do with whether you can solve a particular set of equations. You appear to have solved your equations even though I = S (Whole economy) in every period in your example. The problem is about definitions and assumptions.”

Actually, it has everything to do with time lags, because the period by period adjustment described by the table depends on the assumption that households receive the income earned only at the beginning of the period after it was earned. That is why, if you check the expenditure (E) column and the income (Y) column, you will see that beginning with period 0, expenditure is less than income in each period..

“The root cause of the ambiguity in this debate can be traced back to that fact that the context diagram you included near the start of your Bathtubs post is not fit for the purpose of helping to define the vocabulary you are using in your posts. For example, there is no injection corresponding to household spending in the diagram. Also, there is only one saving, so the diagram does not support the separate discussion of business saving and household saving.”

There is no injection corresponding to household spending because household spending is derived from the incomes earned by households, so it is a constituent part of the circular flow. It is household saving that leaks out of the flow. It is possible that household consumption could suddenly increase, but unless the increase was so large that households were dissaving rather than saving, it would still not be a net injection into the circular flow from the household sector. You are correct that there is only one savings leakage shown in circular flow diagram in my earlier post. The reason is that households, having changed their marginal propensity to save out of income from .1 to .2, are the only source of the increased leakage out of the circular flow. Perhaps as a result of my own misstatement (now corrected) in the third paragraph after the table, you seem to be confused about the role of business firms in this process. All they are doing is letting their total cash balance at the end of each period go down compared to what it was in the previous period. So their saving is going from 0 in the initial equilibrium to a negative number exactly equal in size (but of opposite sign) to the increase in household savings. So there is only one leakage out of the circular flow (the leakage through household savings). There is an ex post adjustment in savings reflecting the willingness of businesses to allow their cash balance at the end of the period to decline in response to the reduction in consumption spending by households. But that reduction in cash holdings represents not a real leakage, but a (strictly bookkeeping) injection(!) (i.e., a negative leakage).

“I agree that it makes sense to focus on S (Households) in your period by period calculations. The Business Cash column is, effectively, dead money. Businesses will not spend money unless they believe that it will contribute to sales but, by not distributing it to households in dividends, businesses prevent anyone else from spending it either.”

Thank you for your acknowledgment that it is household saving that explains what is going on this example. But again you seem to be treating the negative savings by businesses as if it were a separate and independent leakage in its own right, when all that is happening is that end of each period in the adjustment process they wind up holding less money than they held at the end of the previous period. So where is the dead money that they are not distributing to households in dividends that they are preventing anyone else from spending when their cash holdings are diminishing all through the adjustment process?

I would also point out to you that in each period the following relationship holds: the change in expenditure from the previous period equals the negative of the difference between savings in the current period and savings in the previous equilibrium. Thus E(-1) – E(0) = 900 – 1000 = -100, and S(0) – S(-1) = 100. So it is only household savings that has any effect on changes in expenditure and income. Business savings in each period is merely a reflection of the change in expenditure in that period, i.e., business savings is a residual effect that has no influence on the change in expenditure, rather it is the result of the change in expenditure which is the direct result of the change in household savings.

Nick, I agree with all your conclusions but one. I believe that my tables show that it is possible to say what happens out of equilibrium (i.e., what happens in the model out of equilibrium) if we specify with sufficient precision what behavior assumptions we are making about the agents and about the lag structure.

Rob, I think that whatever it is that is causing the very negative reactions to my posts by some commenters, it would not have been assuaged by renaming the variables as you suggest. But I don’t have any problem with your terminology.

More responses to come

LikeLike

In reviewing this comment, I found that before my next to last response to various passages from JKH’s comment above, I somehow quoted the wrong passage. I have crossed out the incorrect passage and inserted the passage to which I meant to respond. I apologize to JKH for this inadvertent error.

JKH, Thanks for your comment/reply to my post.

You said:

“Cost accounting for expenditures sums up to what factors of production earn as income.”

In my example, with a one-period lag between expenditure and income, income exceeds expenditure in every period starting with period 0 when the MPC falls from .9 to .8. It is possible to equalize income and expenditure, in my example, but only by adding the entirely notional decrease in business savings (caused by the increase in household savings) to income in each period starting with period 0. If you wish to make such an adjustment, that is fine with me, but you cannot say that the reduction in business saving plays a causal role in process. It is a pure residual effect in an adjustment process that is independent of any action taken by business firms.

You said:

“The model that I understand is based on the idea of planned expenditure versus actual expenditure and income, the latter two being equivalent in measure, as portrayed on the 45 degree line.”

This is one possible way of understanding the income-expenditure model, which is commonly presented in the textbooks. The expenditure curve represents desired or planned expenditures as a function of income, and equilibrium occurs when actual expenditures equal planned expenditures. The problem with this version of the model arises when one attempts to explain what happens when planned expenditures don’t equal actual expenditures and what mechanisms operate to bring planned and actual expenditures into alignment. The idea that there is a real world mechanism operating to ensure that a definitional equality is realized is problematic, and I see nothing in your comment that dispels that difficulty.

You said:

“The planned expenditure line represents planned expenditure as a function of income. . . . The line starts at the level of autonomous injections on the Y axis and with a lower slope than 45 degrees intersects the 45 degree line at the equilibrium point where actual E equals actual Y.

“The intersection of the planned expenditure line with the 45 degree line is a potential equilibrium, where planned expenditure equals actual expenditure and income. Plans can be realized at that point. And it is the only point where plans can be realized according to the assumed expenditure function.”

Why do you say that the intersection of the planned expenditure line with the 45-degree line is a potential equilibrium rather than an actual equilibrium? What prevents that point of intersection from being an actual equilibrium? Is it possible for plans not to be realized? If so, how would you represent a non-equilibrium situation in the Keynesian cross framework? Is it a point on the 45-degree line? Is it a point of intersection between an expenditure line and the 45-degree line? If it is not, how does one go about finding which point on the 45-degree line the economy is at?

You said:

“[S]uppose the economy starts at an equilibrium point where planned expenditure intersects with the 45 degree line. Suppose planned expenditure then suddenly drops down from there. In the two sector model, this could reflect a planned reduction in investment relative to the counterfactual of no planned reduction in current investment levels. The actual economy is still on the 45 degree line but is now in disequilibrium.”

You say that the economy is still on the 45-degree line at the moment at which the expenditure line shifts downward? I would like to know which expenditure line it is on. Are you saying that it is still on the old expenditure line, or on some new expenditure line? By what method do you determine which expenditure line the economy is on when it is not in equilibrium?

You said:

“The intersection point of the new planned expenditure with the 45 degree line represents a potential future equilibrium point, down to the left and toward the origin of the 45 degree line. Using that new lower potential intersection and equilibrium as a reference point, planned expenditure would fall short of current actual income at income higher [sic] levels higher than at that reference point. In the simplified model, planned investment is less than current saving, and so planned injections are less than actual current withdrawal levels.”

This is not at all clear. You are implying, but not actually saying that the economy is somehow moving down the 45-degree line from the old equilibrium to “the new lower potential intersection and equilibrium as a reference point.” What “reference point” might mean in this context is completely unclear, a reference point to whom? To households, to businesses, or to the modeler? Does that reference point affect anyone’s behavior in the model in the transition from the old to the new equilibrium? If so, how? You say that planned expenditure would fall short of current actual income at income levels higher than at the reference point. So? What is the implication of planned expenditure being less than actual income for the transition from the old to the new equilibrium? What is happening to actual expenditure when the economy is in transition? Or are you saying that the transition is instantaneous? I don’t understand.

You said:

“Actual S and I will always be equal in the two sector model (more generally, actual injections and withdrawals will always be equal), as the economy proceeds toward a new equilibrium point based on the impetus of planned expenditure.”

You are asserting that actual injections and withdrawals are always equal in the transition from the old to the new equilibrium even though you just explained that planned expenditure falls short of current actual income during that transition. By what mechanism is actual investment made equal to actual savings even though planned investment is less than planned savings?

You said:

“With the subsequent “implementation” of the plan to reduce investment, the behavior of actual injections and withdrawals begins to get traction and this is reflected in the continuous satisfaction of the identity.”

What does “subsequent implantation” mean? The expenditure curve has just shifted. How long after the expenditure curve shifts does the plan get implemented?

What does it mean for “the behavior of actual injections and withdrawals to begin to get traction?” How long does it take for the process of getting traction – what “getting traction” can possibly mean in this context I have no clue – to be completed? If the process of “getting traction” is not instantaneous, but is nevertheless essential to continuous satisfaction of the identity – otherwise why even mention it in this context? – why is it that the identity is satisfied when the process of “getting traction” is only beginning?

You said:

“When actual I is reduced relative to the counterfactual of an unchanged I, it follows that actual S and therefore actual Y must decline by the same amount – because of the inviolable accounting identity that portrays how a reduction in I reduces factor income by the same quantity.”

Here you simply assert that a reduction in investment causes an actual reduction in savings because of an “inviolable accounting identity” without explaining (insofar as I can tell) how the “inviolable accounting identity” induces any change in the behavior of actual savers. Do you believe that the decline in savings occurs with or without a change in the behavior of savers. If you believe that the behavior of savers does change, please explain to me how their behavior has changed and how that change is related to an “inviolable accounting identity?”

You said:

“And as investment is reduced, the multiplier starts to work in reverse, as actual declining incomes result in reduced consumption as well.”

You seem to be positing a one-time reduction in planned investment. You then assert that there is an instantaneous reduction in savings as a result “because of [an] inviolable accounting identity.” You then posit that the multiplier starts to work in reverse, with declining incomes causing reduced consumption.” Well, with the MPC < 1, declining incomes cause reduced savings as well as reduced consumption. So, according to you, savings keep falling during the transition from the old to the new equilibrium, even though savings fell immediately along with investment when the old equilibrium was disturbed, and the fall in savings exactly matched the fall in investment. And now, according to your own description, savings, having already fallen as much as investment fell, continue to fall because income is now falling toward the new equilibrium, even though the fall in investment, by assumption, has stopped.

You said:

“Depending on the pattern of the actual implementation of the plan, the economy will gradually work its way down to the new equilibrium point (unless otherwise disturbed) through iterative shrinking of I and S and C and Y, until planned E equals actual E and actual Y once again.”

You have provided no explanation at all of the adjustment process, merely a vague and, as far as I can tell, self-contradictory description of what happens based on a supposed “inviolable accounting identity.”

You said:

“Non-equilibrium planning points can never be realized because they are off the 45 degree line. All planning points away from the 45 degree line can only be in effect the wishful plans of planners who do not incorporate the inevitable knock-on income effects of realizing their plans to change expenditures.”

Why is a point on the 45-degree line, but off the planned expenditure any more realizable than a point on the planned expenditure line, but off the 45-degree line?

You said:

“This sort of model does not depict a circulating flow of actual injections and actual withdrawals where the two are not equal. There is no such model.”

Actually there is; it is right in front of you in the table above, and you have not said a word to disprove it even though you keep asserting that an inviolable accounting identity requires that savings and investment, and leakages and injections, are necessarily equal.

You said:

“

This sort of model does not depict a circulating flow of actual injections and actual withdrawals where the two are not equal. There is no such model. Actual injections are always equal to actual leakages. The model instead depicts such differences only in the context of plans for injections and leakages that can never be realized as they are depicted away from that 45 degree line.”“I have no idea how you come to the conclusion that the intersection of the expenditure planning function with the 45 degree line does not determine a unique solution. That conclusion seems to have something to do with a characterization of the expenditure planning function as a function that depicts events that actually happen rather than those which are planned. It is beyond me how one can think that this is not a system of simultaneous equations that determines a unique economy point on the 45 degree line.”

If one distinguishes between planned expenditure and actual expenditure, I agree that the simple income expenditure model can be solved for a unique equilibrium. The problem arises when one interprets the expenditure function in the Keynesian cross naively as an expenditure function without distinguishing between planned and actual expenditure. Lipsey makes this point very clearly in his essay, and if I have not been clear enough in making that point, I apologize. However, the distinction between planned and actual expenditure solves only the first of the seven problems listed by Lipsey with using the savings investment identity as if it were the mechanism by which the equality between planned and actual expenditure is actually achieved.

You said:

“Fifth, the issue of the differentiation of saving as between households and businesses is really of minor concern in context. Model the saving nexus of the two sectors as the alternative of assuming a full distribution of earnings as dividends to households – or model it as separate business sector saving and make some reasonable adjustment to the interpretation of MPC as necessary. This is just not a substantive issue for this topic. The required flexibility in interpretation is easy compared to some of the other issues in debate.”

What does “saving nexus of the two sectors” mean? The MPC is perfectly well defined. Where in the basic Keynesian model with which we are dealing is there a corresponding magnitude for business saving. As I have already explained above and in my earlier response to Jamie, business saving in this case is simply a notional bookkeeping entry of opposite sign to the additional saving undertaken by households. It is not the result of any behavioral decision taken by businesses. It is only a reflection of the reduction in consumption spending imposed on business by the desire of households to increase their savings.

LikeLike

“business saving in this case is simply a notional bookkeeping entry of opposite sign to the additional saving undertaken by households. It is not the result of any behavioral decision taken by businesses.”

There’s a strange notion people have that some accounting entries “are just book-keeping entries”, as if there is some degree of book-keeping-ness or something which you can assign to various entries.

Anyway, opposite sign? What’s that? And no, it is not correct to say that business saving is not the result of any behavioural decision taken by businesses. Businesses decide to distribute the amount of dividends and retained earning is the result of that.

LikeLike

David,

Thanks for your very thorough response to my comment.

I will return later with an example that puts some meat on those bones.

LikeLike

JKH 2.0

David,

I’d like to make several comments further to your last response. I’ll do this in stages.

First , I’d like to describe my interpretation of the K multiplier.

After that, the application of the K multiplier to the K cross.

At both of these steps I will be mapping the economic ideas to income accounting.

I’ll try to get more specific on the Lipsey/Glasner approach sometime after that. The generics of how I interpret all this seem to be getting in the way of doing that though. The 40,000 foot level is a prerequisite when approaches are so different.

LikeLike

2.1

(I will not be responding directly to your questions in this comment or the one that follows. These two comments are a basis for how I approach the subject. I hope this will be useful. After that, I’ll try to address some of the questions you put to me in that context.)

The following is my interpretation of the Keynesian multiplier. The basics should be straightforward. But the result of mapping the mathematical process to national income accounting is rather surprising. I first thought of this some time ago and at that point hadn’t seen it in any textbook. That doesn’t necessarily mean it’s wrong – especially considering the somewhat loose connection between economics and financial accounting. I’m also guessing that Godley and Lavoie may have touched on this sort of reconciliation and a whole lot more in their book, although I don’t recall seeing this exact piece when I read it.

So consider an investment injection of quantity 100 with an MPC of 2/3.

The usual math produces a total delta effect of:

Y = I + C = 100 + 200 = 300

I think of this as the leveraging of an investment injection with consumption flowing from the income that is created for the factors of investment good production. The real world process may be more complicated, but I’ve always thought of the multiplier as intuitively reasonable, even if oversimplified. I can’t see why it should be fundamentally wrong as an idea about economics.

But here are some income accounting implications of the economic effect:

First, the investment injection creates income that accrues to the factors of production – labor and capital. This works through cost accounting. The price at which the investment good is sold covers all costs – including the cost of capital. That said, the price may not cover the theoretical “hurdle rate” for the cost of capital. But that is a technical detail. The equity holders earn some sort of actual residual return, positive or negative. So in the more general sense, the actual cost of capital is accounted for.

So the investment injection creates an equivalent amount of income.

Consider the effect at the moment the income is fully accrued to the factors of production – before anything else happens. That amount of income must be saved by the macroeconomy – other things equal. We know this because no new consumer goods or services are produced in this initial standalone scenario of a new investment injection. Therefore, given that saving in the generic sense is income not used to purchase consumer goods and services, this new income created by an assumed investment injection must be saved in the first instance.

So at this incipient stage before the multiplier process starts, S equals I. That’s before the marginal propensity to consume or save is in motion.

One’s eyes may roll at this point, since the operation of the MPC includes the complementary MPS, and the MPS is a saving function that also operates as the multiplier iterates with successive waves of income creation and consumption.

So one may ask – how can these apparently opposing ideas be reconciled – the contention that S equals I at a point when the multiplier saving dynamic hasn’t even started?

The investment injection results in an equivalent quantity of income and saving as described earlier. I think you question this off the top while I have claimed it must be the case. But please suspend disbelief for purposes of what I want to describe next, because given that assumed starting point, this should at least reinforce the idea that S = I at all times following that same assumption for the investment injection.

So now assume that the first round of the multiplier math works and there is an initial consumption burst of quantity 66, representing the MPC effect on the income of 100 that was just newly created.

And correspondingly there is new saving of 33.

A pertinent question then is how this gets reflected in income accounting.

As a simplification, assume that the factors of the investment good production who received the new income of 100 are the ones who spend the 66.

So the economy has earned 100 in its factors of investment good production capacity and has now spent 66 in its MPC capacity.

Recall that at the investment injection stage considered on its own, before the multiplier starts to work, the economy saved 100.

Then, in the first stage of the multiplier, the economy spent 66 on consumption. For simplicity of exposition, I’ve assumed those who initially saved were the ones who then spent (I.e. the factors of investment production) But no more income has been assumed to be earned by them. So they have dissaved 66 in the second stage. At the same time, those who produced the 66 of consumer goods have earned 66 as factors of production for those consumer goods. But the consumer goods they produced have been purchased. So there are no remaining consumer goods for them to purchase with their income of 66. And that means they have saved 66.

Therefore, the net saving result of the first round of the multiplier effect is 0.

Thus an MPS of 1/3 has resulted in 0 incremental saving for the macroeconomy. That is because the opening saving of 100 by the factors of production for the investment good has only been redistributed as cumulative saving as between 33 for the investment good producion factors and 66 for the consumer good production factors. So the amount of cumulative S still equals the amount of original S, which equals I. And the important observation is that the entire quantity of saving was created originally and at the outset as equivalent to the income earned by the factors of the investment good production.

Each successive round of the multiplier features a similar combination of equal dissaving and saving.

The result is that cumulative saving remains constant at 100 from the outset and I = S remains in tact always.

The important point is that an original investment injection associated with a Keynesian multiplier process accounts for all the macroeconomic saving to come out of that process, and the MPS fallout of the MPC sequence accounts for none of it.

Tomorrow I’ll write out my interpretation of how the multiplier algebra translates to the Keynesian cross geometry.

P.S.

My motivation in part for writing this out was this section of your previous response:

” You seem to be positing a one-time reduction in planned investment. You then assert that there is an instantaneous reduction in savings as a result “because of [an] inviolable accounting identity.” You then posit that the multiplier starts to work in reverse, with declining incomes causing reduced consumption.” Well, with the MPC < 1, declining incomes cause reduced savings as well as reduced consumption. So, according to you, savings keep falling during the transition from the old to the new equilibrium, even though savings fell immediately along with investment when the old equilibrium was disturbed, and the fall in savings exactly matched the fall in investment. "

My explanation above is framed in the generic expansionary mode but applies readily to the previous contractionary example on which you commented. The injection and consumption multiplier just work in reverse. I'll return to that contractionary example with my next comment on the application of this to the Keynesian cross.

LikeLike

2.2

This is my follow up comment regarding the multiplier and the Keynesian cross. But before getting to that, it occurred to me that I would be able to transform your table 1 and the story that it tells into conventional financial accounting. Instead of modifying standard income accounting as you have done, I will be able to present an integrated treatment of your story using balance sheet, income, and flow of funds accounting. I think I can do this, but it’s going to take several days to think through how to do that in a reasonably concise and understandable way.

It may make more sense following that to return to some of the more specific questions in your last comment.

I’m not sure how interested you are at this point, but with your permission I’d like to use this space to develop my response to your series further. I will assume that is OK unless you interject at some point. This is something I’m interested in for purposes of my own satisfaction at least.

Anyway, here is what I suggested yesterday. It is a brief explanation adapting the multiplier to the Keynesian cross with standard income accounting. I want to emphasize this description has nothing to do with explaining behavioral motivation. It is the adaptation of algebra to geometry using accounting. Pending my planned reformulation of your table 1 using standard accounting, suspending judgement on my stubborn quantitative equating of expenditure and income and of investment and saving is always an option.

Here is my interpretation of the Keynesian cross, using the previous multiplier discussion as the basis. I’ll return to the first example of an investment contraction to keep continuity with the scenario you have already responded to.

Assume the economy is at an alleged equilibrium point – at the intersection of a planned expenditure line with the 45 degree line.

Suppose planned investment falls by 100. Again, assume MPC = 2/3.

The scenario is one in which investment will be 100 lower than its previous level (bearing in mind we are referring to the level of investment flows here).

Using comparable logic as in my previous comment, that means that both I and S drop by 100 at the outset. There is that much less investment injected and saving created as a result of the economy not operating at a counterfactual level of activity equal to its previous pace.

So expenditure drops by 100 – and that considered just on its own can be represented by a direct vertical drop from the previous equilibrium point down to the planning line.

But as I have said before, such a point is unrealizable in fact, because it lies off the 45 degree line. And that corresponds to the fact that I of 100 generates S of 100 (or in this case a decline in I from previous levels means a decline in S from previous levels). So what happens is that instead of landing on that 100 vertical drop down point, the economy combines (in measured effect) that move with a second move horizontally to the left, where it lands on the 45 degree line at a point where both E and Y have declined by 100. This simply reflects the fact that I = S at all times as described in my previous comment (which again I realize is a contentious supposition for purposes of the broader discussion).

And so what has really happened from the standpoint of the KC geometry is that the economy has slid directly down the 45 degree line as a result of this discrete drop in both investment and saving.

This happens in steps representable by discrete accounting. Common sense suggests that a “plan” can consist of a series of such discrete steps – in which case there is a ratcheting of reduced investment injections down the 45 degree line – or a plan can consist of a single discrete step depending on the scale or on the preference for stepwise analysis. The single discrete step is the clearest way to analyse the accounting record for the economics.

As in my previous example depicting economic expansion, such a discrete investment step occurs logically prior to knock-on consumption multiplication, which in this case will be a multiplied contraction from the unchanged level of the counterfactual.

Similar steps can be visualized for the operation of the multiplier in reverse. The first wave in which income has dropped by 100 results in 66 less consumption expenditure with that much less income created and so on. The economy falls down the 45 degree line in stages. At each stage a simple vertical drop in expenditure is precluded by the fact that income has also declined, which directs the net result back to the 45 degree line. One can visualize successive falls down the 45 degree line in this way. And note that the economy remains above the planned expenditure curve all the way down until it finally converges to the intersection of the planning line with the 45 degree line. That is the point where the multiplier effect finally exhausts itself mathematically because new iterations of forgone income have become vanishingly small. And comparable to the expansion version I described before, there is no additional reduction in macroeconomic saving beyond the initial drop associated with the investment reduction, notwithstanding the dynamic operation of the MPS in reverse.

LikeLike

JKH,

Just to let you know that I am still reading and trying to follow along.

You logic sees to be: Investment spending will always lead to income that cannot be consumed since investment spending by definition does not generate consumer goods. So investment always equals savings.

Likewise consumption spending, as it can be seen as spending from previously accumulated savings, will always be both dis-savings and dis-investment.

So applying this logic to David’s model:

In year 1 there will be 100 of I and S and no consumption so Y= 100

In year 2 there will again be 100 I and S, but people will spend 90% of the 100 they earned (saved) in year 1 so Y= 190

Y will then multiply up with people always spending 90% of the previous year Y until we reach an equilibrium of y=$1000, which is David’s staring point (and he brings Y forward a year).

Then from equilibrium people decide they want to consume only 80% of the previous years Y, which then causes Y to multiply down to the new equilibrium of Y=500.

David defines S as “Y-C” (where Y is E from the previous period) and based on that definition he uses dY/dt = 0 I = S as an equilibrium condition.

Using (my interpretation of ) your version of David’s model, you could rename David’s S as a new variable called UY (Unspent Income = Last Years Y – this years C) , and draw the conclusion that in equilibrium dY/dt = 0 I = UY.

Is above correct ?

LikeLike

Rob R.

Thanks for following and your question.

I’m attempting to put together a comment that compares David’s approach with more conventional accounting.

There are a lot of moving pieces, so that’s going to take longer than I had first anticipated.

At this point I hope to have that done no later than sometime on Monday.

I think it will be effective for me to look at your comment more closely after I’m done with that. And I’ll try and respond then.

LikeLike

Dear

I fully agreed that these accounting identities are faulty :

1. GDI = C + I = C+ S = GDP

2. GDP = C + I + G + (X – M) = GDI = C + S + T (used in MMR and MMT)

But the NIPA foundation is really based on these accounting identities:

1. GDP = C + I + NX (net exports)

= C + S – NR (net income receipts from foreign)

2 S – I = NX + NR = balance of current account

Most people missed the meaning and definition of saving S in NIPA, which is “non-consumed” spending from income. Investment (I) is not considered as consumed spending.

In NIPA accounting, saving S just measures the return of investments (both domestic and foreign) while investment I measures the cost of investment.

Detailed NIPA accounts and the relationships of accounting items are here

http://www.bea.gov/national/pdf/nipa_primer.pdf.

LikeLike

JKH and Bob R.

I believe that we are using different definitions and meanings of S(savings) in the discussions. In my previous post, I referred to one pdf file about USA NIPA T economic accounting methodology for your reference.

In economic accounting, sector T-accounting tables 2, 3 and 4 (public, business and personal) define a balance item called sector saving.

LHS = “consumed” spending items + saving

RHS = income items

Please note that investments are not recorded in “consumed” spending items in table. Sector investments and savings are compared in domestic capital account table 6.

LikeLike

The meanings of negative saving numbers (S < 0) and (S – I) < 0 in NIPA accounts Note that: S(saving) is used to measure the RETURN of investment. I is used to measure the COST of investment and it must be non-negative number.

(a) S < 0

Sector saving S can be a negative number in NIPA accounts since it is defined as sector income less "consumed" spending items. In USA, government saving is often a negative number. Sector ROI (Return of Investment) has not yet cover sector CFC (Consumption of Fixed Capital).

(b) S-I < 0

Gross saving (total ROI from public and private sectors) has not yet cover domestic investment (I)

Since S and balance of current account can be negative numbers, "S=I" is described in NIPA investment and saving account (table 6 in NIPA guide) by this way: RHS = LHS

RHS = net domestic saving + CFC = gross domestic saving(S)

LHS = gross domestic investment (I) + balance of current account (NX+NR)

Thus, the confusion of "S=I" comes from following sources from incorrectly using the NIA accounting items.

1. The definition of S.

In NIPA, I is not considered as "consumed" spending since S is a

smart way to measure RO(I)

2. The definition of I

In NIPA, I is used to measure gross domestic investment

3. NIPA T-accounting is based on money flow conservation laws, not

based on supply-demand equilibrium cross. In temporal logic (http://en.wikipedia.org/wiki/Temporal_logic), the accounting identities mean "ALL" operator: ALL t such that LHS(t) = RHS(t) in NIPA T-accounts

Note that, the supply-demand equilibrium cross is based on "EXIST" or "FUTURE" operator. IMO, behavioral and equilibrium math equations in current economic models make axiomatic economic theorems for "mechanizing" human economic behaviors. This is the problem of our economic models, far from reality.

LikeLike

2.3

This is my comment discussing how standard accounting works for the lag model presented in the post.

There are 2 aspects to the discussion – the structure of the economic scenario and model with lagged payments of income, and the accounting.

The scenario is that an economy produces output with corresponding expenditure E but delays the payment of income Y until the next accounting period.

I’m going to refer to standard accounting for Y as Y and the methodology used in the post as LGY (i.e. “Lipsey – Glasner income” ).

Then:

E ( t ) = Y ( t )

E ( t ) = LGY ( t +1)

Standard accounting recognizes income in the time period in which it is earned.

LGY accounting recognizes income in the time period in which it is paid in cash.

Consider the point in table 1 where the MPC propensity factor drops from .9 to .8.

The economy starts to contact.

In the first iteration, E is 900 ( 100 I + 800 C ) but LGY is 1000.

Household saving is shown to be 200.

Here is how standard accounting handles that:

First, a real world example. Suppose a US corporation listed on a stock exchange reports its financial results at the end of each calendar quarter. And suppose it pays its employees once a month. But for each month’s work it pays them at the start of the next month.

Then there is no way that this corporation would report it’s December 31 financial results without showing a liability on its balance sheet for the employee compensation earned in December but not yet paid by December 31.