In this installment of my series on Richard Lipsey’s essay “The Foundations of the Theory of National Income,” I am going to focus on a single issue: what inferences about reality are deducible from a definition about the meaning of the terms used in a scientific theory? In my first installment I listed seven common statements about the basic Keynesian income-expenditure model that are found in most textbooks. The first concerned the confusion between the equality of investment and saving (or between income and expenditure) as an equilibrium condition and a definitional identity. Interpreting the equality of savings and investment as an identity essentially means collapsing the entire model onto the 45-degree line and arbitrarily choosing some point on the 45-degree line as the solution of the model.

That nonsensical interpretation of the simple Keynesian cross is obviously unsatisfactory, so, in an effort to save both the definitional identity of savings and investment and the equality of investment and savings as an equilibrium condition, the textbooks have introduced a distinction between ex ante and ex post in which savings and investment are defined to be identically equal ex post, but planned (ex ante) savings may differ from planned (ex ante) investment, their equality being the condition for equilibrium.

Now, to be fair, it is perfectly legitimate to define an equilibrium in terms of plan consistency, and to say that the inconsistency of the plans occasions a process of readjustment in the plans, and that it is the readjustment in the plans which leads to a new equilibrium. The problem with the textbook treatment is that it draws factual inferences about the adjustment process to a disequilibrium in which planned saving is not equal to planned investment from the definitional identity between ex post savings and ex post investment. In particular, the typical textbook treatment infers that in a disequilibrium with planned savings not equal to planned investment, the adjustment process is characterized by unplanned positive or negative investment (inventory accumulation or decumulation) corresponding to the gap between planned savings and planned investment. Identifying a gap between planned saving and planned investment with unplanned inventory accumulation or decumulation, as textbook treatments of the income expenditure model typically do, is logically unfounded.

Again, I want to be careful, I am not saying that unplanned inventory accumulation or decumulation could not occur in response to a difference gap between planned savings and planned investment, or even that such unplanned inventory accumulation or decumulation is unlikely to occur. What I am saying is that the definitional identity between ex post savings and ex post investment does not imply that such inventory accumulation or decumulation takes place and certainly not that the amount by which inventories change is necessarily equal to the gap between planned savings and planned investment.

Richard Lipsey made the key point in his comment on my previous post:

The main issue in this whole discussion is, I think, can we use a definitional identity to rule out an imaginable state of the universe. The answer is “No”, which is why Keynes was wrong. The definitional identity of S ≡ I tells us nothing about what will happen if agents wish to save a different amount from what agents wish to invest.

Here is how Lipsey put it in his 1972 essay:

The error in this interpretation lies in the belief that the identity E ≡ Y can tell us what can and cannot happen in the world. If it were possible that a definitional identity could rule out certain imaginable events, then such a definitional identity would be an informative statement having empirical content! If it is a genuine definitional identity (which follows from our use of words and is compatible with all states of the universe) then it is only telling us that we are using E and Y to refer to the same thing, and this statement no more allows us to place restrictions on what happens in the world than does the statement that we are not using E and Y to refer to the same thing.

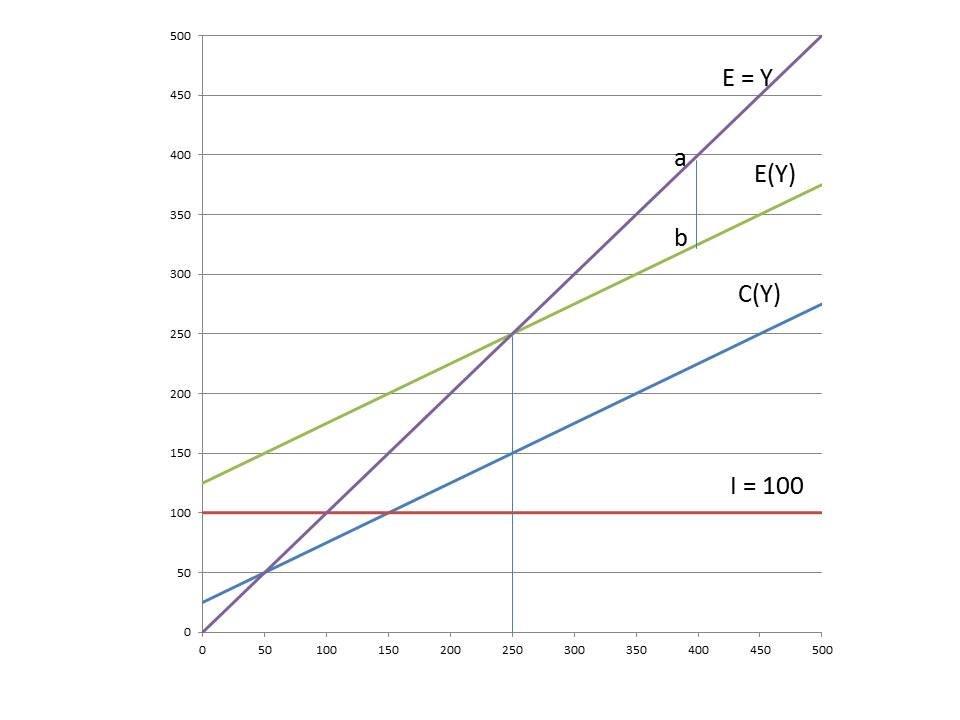

Lipsey illustrated the problem using the simple Keynesian cross diagram. To make the discussion a bit easier to follow, I am going to refer to my own slightly altered version (using a specific numerical example) of the familiar diagram. Setting investment (I) equal to 100 and assuming the following consumption function

C = 25 + .5Y

We can easily solve for an equilibrium income of 250 corresponding to the intersection of the expenditure function with the 45-degree line.

What happens if we posit that the system is at a disequilibrium point, say Y = 400. The usual interpretation is that at Y = 400, planned (ex ante) investment is less than savings and planned (ex ante) expenditure is less than income. Because, actual (ex post) investment is identically equal to savings and because actual (ex post) expenditure is identically equal to income, unplanned investment must occur to guarantee that the investment-savings identity is satisfied. The amount of unplanned investment is shown on the graph as the vertical distance between the expenditure function (E(Y)) at Y = 400 and the 45-degree line at Y = 400. This distance is shown in my diagram as the vertical distance between the points a and b on the diagram, and it is easy to check that the distance corresponds to a value of 75.

What happens if we posit that the system is at a disequilibrium point, say Y = 400. The usual interpretation is that at Y = 400, planned (ex ante) investment is less than savings and planned (ex ante) expenditure is less than income. Because, actual (ex post) investment is identically equal to savings and because actual (ex post) expenditure is identically equal to income, unplanned investment must occur to guarantee that the investment-savings identity is satisfied. The amount of unplanned investment is shown on the graph as the vertical distance between the expenditure function (E(Y)) at Y = 400 and the 45-degree line at Y = 400. This distance is shown in my diagram as the vertical distance between the points a and b on the diagram, and it is easy to check that the distance corresponds to a value of 75.

So the basic textbook interpretation of the Keynesian cross is using the savings-investment identity to derive a proposition about the behavior of the economy in disequilibrium. It is saying that an economy in disequilibrium with planned investment less than planned savings adjusts to the disequilibrium through unplanned inventory accumulation (unplanned investment) that exactly matches the difference between planned saving and planned investment. But it is logically impossible for a verbal identity (between savings and investment) — an identity that can never be violated in any actual state of the world — to give us any information about what actually happens in the world, because whatever happens in the world, the identity will always be satisfied.

Recall erroneous propositions 2, 3 and 4, listed in part I of this series:

2 Although people may try to save different amounts from what people try to invest, savings can’t be different from investment; realized (ex post) savings necessarily always equals realized (ex post) investment.

3 Out of equilibrium, planned savings do not equal planned investment, so it follows from (2) that someone’s plans are being disappointed, and there must be either unplanned savings or dissavings, or unplanned investment or disinvestment

4 The simultaneous fulfilment of the plans of savers and investors occurs only when income is at its equilibrium level just as the plans of buyers and sellers can be simultaneously fulfilled only at the equilibrium price.

If realized (ex post) savings necessarily always equals realized (ex post) investment, that equality is the result of how we have chosen to define those terms, not because of people actually are behaving, e.g., by unwillingly accumulating inventories or failing to save as much as they had intended to. However people behave, the identity between savings and investment will be satisfied. And whether savers and investors are able to fulfill their plans or are unable to do so cannot possibly be inferred from a definition that says that savings and investment mean the same thing.

In several of his comments on my recent posts, Scott Sumner has cited the professional consensus that savings and investment are defined to be equal. I am not so sure that there is really a consensus on that point, because I don’t think that most economists have thought carefully about what the identity actually means. But even if there is a consensus that savings is identical to investment, no empirical implication follows from that definition. But typical textbook expositions, and I think even Scott himself when he is not being careful, do use the savings-investment identity to make inferences about what actually happens in the real world.

In the next installment, I will go through a numerical example that shows, based on a simple lagged adjustment between consumption and income (household consumption in this period being a function of income in the previous period), that planned savings and planned investment can be realized and unequal in the transition from one equilibrium to another.

PS I apologize for having been unable to respond to a number of comments to previous posts. I will try to respond in the next day or two.

David: I’m on board with you and Richard so far. Inventories might not even exist, if goods are services like haircuts, or are only produced after the order to buy them is placed.

I will wait for Part 3.

LikeLike

“But it is logically impossible for a verbal identity (between savings and investment) — an identity that can never be violated in any actual state of the world — to give us any information about what actually happens in the world, because whatever happens in the world, the identity will always be satisfied.”

True. Good point. But your entire post (and the last one) reads as if nothing can be gained out of learning accounting identities.

It is also true that economists confuse accounting identities for behavioural relations but nonetheless they are important.

The reason is that economic concepts are accounting concepts. If one has no respect for accounting, one can simply build vague theories.

LikeLike

I would put this, we can define S to be equal to I, S(t) to be equal to I(t) and empirically determine S(t0) and I(t0) to be equal to x, but cannot say anything from this about what S(t1) and I(t1) are or will be.

LikeLike

“The definitional identity of S ≡ I tells us nothing about what will happen if agents wish to save a different amount from what agents wish to invest.”

That about nails the nothingness aspect to it. But the identity does tell you something about one feature of the process of adjustment and how it must look close up. Specifically, the iterative steps toward the future state must satisfy the accounting identity at all times. And any model for that process must be consistent with that. I’d be surprised if Keynes didn’t understand that. But a lot of economists probably don’t – because they don’t know accounting.

And fulfillment of a plan requires those iterations over time. So while the identity can’t tell you anything about why it must happen, it tells you how it must happen if it happens in the sense of adhering to the identity at all times.

So I think the objection is backwards. It’s not that it tells you what must happen, but how it must happen. Identities are constraints of coherency on modeling.

Perhaps accounting can be viewed as a required mini-equilibrium underlying the process of equilibrium more conventionally understood.

LikeLike

Hi David,

This is a nice series. I don’t know if you will find this convincing, but “identities” like E ≡ Y seem to actually be closer to information equilibrium relationships (a signal in a fluctuation in E shows up in Y). When the system is not in equilibrium, the equality doesn’t hold:

http://informationtransfereconomics.blogspot.com/2015/03/theories-of-identities-are-nonsensical.html

Imagine sending sound waves through water, singing as a humpback whale. In still water, this is really straightforward, and your signal in (your song) equals your signal out (the song received by other whales). But in the non-equilibrium case of turbulent, even frothy, water (or temperature gradients) your signal can be changed, diminished or even washed out completely.

LikeLike

“If realized (ex post) savings necessarily always equals realized (ex post) investment, that equality is the result of how we have chosen to define those terms, not because of people actually are behaving, e.g., by unwillingly accumulating inventories or failing to save as much as they had intended to.”

I have no problem with this. It is clear to me that if you define savings and investment so that they are identically equal, it’s meaningless to ask what mechanism brings them into equality. The problem I have is that I can’t see how redefining the terms so that they might be unequal tells you anything more about what their values might be. You still need a theory of what is going on, and your theory either stacks up or doesn’t, regardless of how you define your terms.

LikeLike

JKH has nice points.

David, while what you say is true, accounting identities must hold for every state of the world, it isn’t true for the model world with a given set of behavioural assumptions. So accounting identities have to be added in the equations of the model. These are constraints. So it reduces future possibilities possible without those identities.

And this is not a trivial point. Most of the times economists are making some accounting errors.

In the end models should have emphasis on the accounting identities because otherwise the model will produce non-possible states of the world

LikeLike

Agree with Ramanan obviously.

Accounting is a constraint on coherent economic modeling – that is if there is any interest in modeling a projected state that is something other than an incoherent fantasy.

The definition of saving as a residual is fundamental to the logic of it. There is no other coherent way of doing it in a monetary economy, although the blogosphere is famous for trying. The equivalence is essentially a mathematical measurement of something that is real and something that is monetary / financial where the two must connect tightly for the system to be intelligent.

And investment and saving are definitely different “things” because real investment is different from monetary or financial forms of saving.

The equivalence is purely quantitative in the sense of monetary measurement – not existential as in the equation of real and monetary.

Finally, the constraint shows up in the real world in many ways – for example, banks model their balance sheets going forward for expectation and risk assessment around that expectation. Accounting coherence in what the model projects is essential. It is in this way that the ex ante / ex post debate is a total straw man put up by the economics profession as it struggles to deal with this issue – where it struggles at all when it is not outright rejecting its relevance, which is the most common treatment. Accounting coherence is not just an ex post exercise – it is an ex ante requirement for projected future states of the world.

P.S.

Applying the debate to IS-LM, I think the IS curve should just be called the I curve.

Nice series of posts btw.

LikeLike

“What happens if we posit that the system is at a disequilibrium point, say Y = 400. The usual interpretation is that at Y = 400, planned (ex ante) investment is less than savings and planned (ex ante) expenditure is less than income.”

This to me is an incredibly illogical set up and interpretation. Being “at” disequilibrium makes no sense. The system is never “at disequilibrium” when agents are making stepwise decisions to transact – for example, to add to investment – and when those transactions change actual GDP and GDI. Agents execute plans and the results follow the accounting identity. That means the iterative results are always on the relevant 45 degree line (which is in effect superfluous). It’s just that the line shifts (still superfluous) with each investment transaction.

This planned/unplanned stuff is the problem. The awkward cross diagram is just a way of depicting the result of the assumed path of actual GDP and GDI according to the equation and the assumed starting point. But it’s a terrible conflation of a graphical depiction of a projected end result with the underlying algebra that forces the implied result. Simple algebra without the graph is a much better way of illustrating the result. The use of the term “disequilibrium” just reflects some presumed algebra that hasn’t yet worked itself out through iterative activity.

LikeLike

“In particular, the typical textbook treatment infers that in a disequilibrium with planned savings not equal to planned investment, the adjustment process is characterized by unplanned positive or negative investment (inventory accumulation or decumulation) corresponding to the gap between planned savings and planned investment.”

I really don’t understand the emphasis on inventories, particularly in the context of your example. If additional investment is forthcoming through inventory accumulation, that becomes a contractionary influence – which would decrease income rather than move it to 400. An expansionary effect would result from increased productive fixed investment– which would increase income. The new investment would generate new saving with the associated multiplier effect. The “planning” effect that moves income to 400 comes from investment expenditure planning (“autonomous injection” planning).

LikeLike

JKH,

I’d put it differently. In my view, economic systems are always in disequilibrium, because things change faster than the system can adjust. But accounting identities hold whether the system is in equilibrium or not.

I read the paragraph you quote as being about what happens when firms produce 400 of output (expecting to be able to sell that), and when combined consumption expenditure and fixed capital formation turns out to be less than that.

LikeLike

“If it were possible that a definitional identity could rule out certain imaginable events, then such a definitional identity would be an informative statement having empirical content!”

Ironically, it does rule out those uncountable imaginable events where the economic thinker is not acknowledging the accounting constraints that must underpin any viable projection.

LikeLike

Nick,

I find the notion of permanent disequilibrium to be reasonable as a concept but somewhat useless as a terminological distinction when it means there is

never an equilibrium. The language is unreasonable.

Conversely, from that standpoint, accounting identities are in permanent equilibrium, since every economic event can be represented as an accounting event.

“I read the paragraph you quote as being about what happens when firms produce 400 of output (expecting to be able to sell that), and when combined consumption expenditure and fixed capital formation turns out to be less than that.”

I don’t understand that. How can inventory accumulation alone increase output (to 400) from the counterfactual without the inventory accumulation? That seems to be the starting premise.

LikeLike

My general interpretation of both KC and IS-LM as graphs is that all points other than the intersection are meaningless in both cases.

And the meaninglessness in both cases is due to conflict with accounting identities that can only be realized at the intersection.

Which leads to the question – what is the purpose of presenting these things in graphical form?

And my answer is – there isn’t any.

It should be done through algebra alone.

And the meaning of the KC is really one of projected expenditure mix – investment plus consumption in the basic model.

(At a level of much greater generality, this is a sort of income statement analogue to optimal asset mix when there is an overriding portfolio constraint.)

And the type of constraining equation that you present for the desired expenditure mix can be easily solved as you have done.

Solving the equation does not violate accounting identities.

Trying to interpret graphs that are not required in the first place leads to some pretty weird misunderstandings though.

So I don’t agree with Lipsey’s list.

It looks to me like all of that depends on interpreting a graph that is incoherent in all but one of its points.

But the graph is not required to make sense of the basic KC conclusion – which is that of projected expenditure mix based on an algebraic equation of “expenditure and income portfolio balance” – and nothing more than that.

LikeLike

There is something troubling me about the logic here and the only way I can describe how it feels to a non-economist is to use an analogy from another subject with scientific theories – chemistry.

Consider the following steps in the thought process of a chemist

Step 1: Observe the world. Note the existence of hydrogen, oxygen and water.

Step 2: Create precise definitions for these terms and how they are used. For example, in order to be precise, separate definitions are required for an atom of oxygen and a molecule of oxygen.

Step 3: Observe the world some more and play about with it a little. Note that hydrogen and oxygen can sometimes be transformed into water.

Step 4: Develop an accounting identity theory concerning hydrogen and oxygen combining to form water. (It is an accounting identity because the number of atoms is conserved in any reaction).

Step 5: Challenge the rest of the world to find an exception to the identity. Can water be produced from elements other than hydrogen and oxygen? Can hydrogen and oxygen combine to form anything other than water? If exceptions are found update the theory.

In contrast, what is happening here seems to be more like:

Step 1: Define an accounting identity concerning the relationship between hydrogen and oxygen combining to form water.

Step 2: Observe the world. Note that in some circumstances hydrogen and oxygen do, indeed, combine to form water.

Step 3: Decide that observing the world has added no additional information over and above the identity.

Step 4: Worry that there might be some exceptions to the identity in some other “imaginable state of the universe”.

The problem with this logic starts with the first step. The first step is just an assumption. However, it is then used as though it were a fundamental truth.

When you talk about the “definitional identity of savings and investment” you are assuming what you need to prove. If I observe the world I will note the existence of investment and saving as different things. In my car manufacturing example from the previous thread, the car manufacturer invests in materials and labour and then transforms that investment into an investment in unsold cars. Unsold cars are demonstrably not the same type of thing as the monetary savings accrued by the rest of the economy from selling the materials and labour to the car manufacturer.

If I observe the world some more, and think about the rules of accounting, I might then come up with a theory that says ‘saving = investment’. I might then challenge others to find counter-examples to this theory. However, that is not what you are doing.

The key thing here would be to find a counter-example where saving does not equal investment. That may be what you intend to do in your next post. I look forward to reading your counter-example. However, I am dubious that you can do that without breaking the rules of accounting or without mis-using a term such as ‘investment’.

LikeLike

JKH,

I’m not saying there never could be an equilibrium. Just that in practice, even if there is at least one equilibrium, it changes faster than the economy can adjust to it. So the actual state never catches up with the target. I’m not talking about a situation where the economy remains in a stationary disequilibrium state.

With regard to the example, it’s just the way I read it, but it didn’t occur to me that this was a situation where income had for some reason changed from an equilibrium of 250 to a disequilibrium of 400. I hadn’t analysed it in great detail, but I’d just assumed it was a situation, for example, where income had been at an equilibrium of 400 for some time and then suddenly, and unbeknownst to firms, households changed their spending habits to consume less for any given income level.

LikeLike

Nick,

On the second point:

“The amount of unplanned investment is shown on the graph as the vertical distance between the expenditure function (E(Y)) at Y = 400 and the 45-degree line at Y = 400.”

That corresponds to an increase in investment from 100 to 175 which combined with the consumption multiplier effect then increases Y from 250 to 400.

(the total Y change of 150 is a 75 change in investment + .5 x (400 – 250) = 75 change in consumption)

– or maybe I’m still misunderstanding this

LikeLike

Nick,

Looking at that example in your way, I think the economy would move from an initial equilibrium at 400 to a sudden disequilibrium at 400 which would prod an inventory accumulation of 75.

That would be consistent with a story of eventual contraction as that inventory was worked off over time.

But that scenario increases investment initially from a level of 175 (corresponding to equilibrium Y at 400) to 250 – the original equilibrium fixed investment of 175 plus inventory accumulation of 75 in lieu of sales.

Yet to move back to a Y equilibrium of 250, investment has to return to a level of 100. That corresponds to a total reduction of 150 consisting of a reversal of the inventory increase and a contraction in fixed investment.

I guess I still don’t get how this is described.

LikeLike

JKH,

Yes, I understood it as a change from an equilibrium at 400 to a disequilibrium at 400, which then led to other things happened.

But, no, I hadn’t necessarily envisaged that planned investment was previously 175. In fact I’d imagined something more like an original consumption function of, say, C = 100 + 0.5Y, and then households deciding to consume less.

I should point out that I’m not necessarily endorsing this analysis. My point here is really that it works the way it works regardless of how you define terms, but defining income and expenditure so that they are identically equal is not only conventional but very useful.

LikeLike

“My point here is really that it works the way it works regardless of how you define terms, but defining income and expenditure so that they are identically equal is not only conventional but very useful.”

Agree 100 per cent.

LikeLike

Nick R., Thanks. Good to know you are on board. Makes me feel more secure.

Ramanan, No empirical information can be learned about what the real world, because as a number of commenters have pointed out, whatever happens in the real world, there is an accounting category to which a corresponding entry can be made, so that all accounting identities are satisfied.

Lord, I think that that is correct.

JKH, When you say that “the iterative steps toward the future state must satisfy the accounting identity at all times,” you are not describing any feature of the real adjustment process, because whatever happens the accounting definition will still hold. There is no possible state of the world in which the accounting identity is violated. It’s just a question of calling things by their right accounting names. So accounting identities place no restriction on what people actually do or the adjustment process that they follow. Hence, they provide us no information about how the world operates. Adhering to the identity is not a restriction on what people do it is imposed by the way accountants define their terms.

Jason, Thanks, glad you like it. Unfortunately, I still haven’t figured out what information transfer economics is all about. Sorry.

Nick E., I agree. No definition ensures that you get to the right answer. You need to formulate a theory of adjustment. The point of this post is that an accounting identity is not a theory of adjustment, and the attempt to use an accounting identity to derive a theory of adjustment from the simple income- expenditure model involves a misunderstanding.

JKH, Why do you think that the mathematical identity between a graphical representation and an algebraic representation of the same functional forms is any weaker than an accounting identity?

Whenever you look at a disequilibrium situation, there is an implicit assumption that there was some parametric change that causes a pre-existing equilibrium to be unsustainable. The only parameters in the simple model we are looking at are the vertical intercept (25) of the consumption function, the slope of the consumption function (0.5) , and the fixed level of investment spending (100). The question is whether such a parametric change causing a change in consumption and saving by households would necessarily be matched by an equal change in investment at every point along the adjustment path from the old equilibrium to the new one. It is entirely possible to imagine that the change takes place without any accumulation of inventories and no change in planned investment, in which case the only change is in saving.

Jamie, JKH and Nick E., A counterexample, taken from Lipsey’s essay, is precisely what I am going to offer in my next post. So stay tuned.

LikeLike

David,

“When you say that “the iterative steps toward the future state must satisfy the accounting identity at all times,” you are not describing any feature of the real adjustment process, because whatever happens the accounting definition will still hold.”

I am referring to the economist’s description of the adjustment process – not the adjustment process itself. The economist’s description of the process reflects the observation of the process. The description should convey useful information in the form of coherent accounting. If the description is wrong, then information has been lost. I think accounting coherence is a deeply embedded aspect of this entire discussion and important to the information about it.

“Why do you think that the mathematical identity between a graphical representation and an algebraic representation of the same functional forms is any weaker than an accounting identity?”

It is weaker when the relationship between graphical and algebraic representations is in fact not an identity, which I believe to be the case here.

The algebraic representation is a solution in two simultaneous equations of the form:

E = Y

E = a + bY

That is fine, and there is only one solution, which determines the functional value of E = Y.

But the “corresponding” graphical depiction is wrong as a visualization of the simultaneous equation result.

E = Y is fine as the 45 degree line

But E = a + bY is wrong as a graph in the form of another line

Instead, I would suggest the following:

Define:

E* = a + bY AND E* = E

That defines the corresponding “graph” not as a line but as a point

All points on the line defined by E = a + bY are irrelevant to the Keynesian cross, except for this one point

i.e. the cross is not the intersection of two lines, but the intersection of a line with a point

LikeLike

David,

You responded in a comment to an observation by Scott Sumner and a VERY good question from Ken Duda at your previous post.

“Scott and Ken, Here is what, I think, you are missing. I am defining income as a flow of money from firms to households. My payment of $1.98 for a cup of coffee is a flow of money from a household to a firm. The $1.98 sits in the Barnes & Noble cash box when I make a payment, it does not reach households until wages and other factor payments are made and dividends are paid.”

I’ve already said this, but the problem with your response is that it confuses income accounting with flow of funds accounting. This is ALL about accounting mode differentiation.

With income accounting, that $ 1.98 will be reflected as an apportioning of costs between payments for the cost of goods sold, payments for various administrative expenses, payments to labor, and payments to capital, including equity.

Added up at the macro level, it is income accounting that forces the equivalence between expenditures and income.

It DOESN’T matter when the actual cash payments are made. Timing differences where relevant by spanning different accounting periods are captured in flow of funds accounting. And your point above is about timing differences.

The fact that timing differences exist doesn’t mean that equivalence can’t be proven. That is the very PURPOSE of income accounting.

Every business entity of substance has 3 different types of financial statements: income statement, balance sheet, and sources and uses of funds (which is flow of funds at the macro level). There is a reason for the existence of these different types. And it is to answer questions such as Den Duda posed prior to your response above. His question can be answered very easily by relating national income to flow of funds (I won’t do that here but I can certainly provide it on request).

At a larger scale, the definitions of income, saving, and investment are all income accounting measures. They are NOT flow of funds concepts. How money moves around is entirely superseded by the technique of income accounting. And that’s how the equivalence of expenditure and income is established at the macro level.

Double entry bookkeeping is the basis for national income accounting, and it is what forces equivalence when swept up at the macro level. DEB is not a mere “convention”. It is the result of some mathematical logic that was first brought to bear in India I believe, sometime around the 7th century.

It’s time for the economics profession to catch up.

LikeLike

David, You said:

“But typical textbook expositions, and I think even Scott himself when he is not being careful, do use the savings-investment identity to make inferences about what actually happens in the real world.”

If you keep making this claim then you’ll eventually need to provide an example. I doubt you will find one.

Other than this single sentence, I like the post. The ex ante/ex post adjustment process that Keynesians often talk about is unhelpful. However I’m not qualified to talk about what the Keynesian cross textbook writers have in mind when they draw the Keynesian cross diagram. It’s such a painfully lame theory that it makes my hair hurt just to think about it.

LikeLike

Assume that savings and investment are both different words for “that part of output that is not consumed in the current period”.

Once you have this definition it is quite possible to define “planned investment” and “planned savings” independently . It then becomes an interesting exercise to work out how the actual level of savings/investment is derived from a starting point where planned investment and planned savings differ.

Starting from a point where savings/investment, and planned investment and planned savings are all equal. People decide to consumer less. What happens next depends upon your model.

In a traditional model with inventories the decision to consume less will not necessarily immediately effect output. The increase in planned savings will be realized (at least in the short term) and result in actual savings/investment increasing above planned investments (via inventory buildup). This will then affect planned investment. Then there will be an iterative process to realign planned investment and planned savings with actual savings/investment.

As Nick Rowe says, you can have models where inventories do not even exist. In these models the increase in planned savings has an immediate effect on output. The effect on savings/investment would depend upon how the decrease in consumption affects both the book value of existing capital and the production of new capital.

LikeLike

From the standpoint of algebraic construction, the following sequence makes no sense to me:

…………………………………………………………………………

E = E(Y) + A

and the expenditure-income accounting identity

E ≡ Y.

An accounting identity provides no independent information about the real world, because there is no possible state of the world in which the accounting identity does not hold. It therefore adds no new information not contained in the expenditure function. So the equilibrium level of income and expenditure must be determined on the basis of only the expenditure function. But if the expenditure function remains as is, it cannot be solved, because there are two unknowns and only one equation. To solve the equation we have to make a substitution based on the accounting identity E ≡ Y. Using that substitution, we can rewrite the expenditure function this way.

E = E(E) + A

If the expenditure function is linear, we can write it as follows:

E = bE + A,

which leads to the following solution:

E = A/(1 – b).

That solution tells us that expenditure is a particular number, but it is not a functional relationship between two variables representing a theory, however naïve, of household behavior; it simply asserts that E takes on a particular value.

Thus treating the equality of investment and savings as an identity turns the simply Keynesian theory into a nonsense theory.

………………………………………………………………….

The appropriate form in my view is more like this:

E = A + bY

E ≡ Y

A is a parameter that is constructed from the sum of the assumed autonomous factors (the consumption intercept, investment, government spending, and net exports)

b is the consumption slope

This is a system in two simultaneous equations that can be solved

The viability of the expenditure function is constrained by the expenditure/income identity

Because of that, the expenditure function has no applicable meaning except on the 45 degree line

I find the notion that an identity provides no information to be utterly bizarre

It is essential to knowing how the expenditure function is constrained in the real world – it is necessary to solve for the value of the expenditure function in the model and knowing precisely where it is applicable

E and Y are different in substance but equivalent in value

They are made different in substance because such separation is required in a monetary system in which financial intermediation exists

They are made quantitatively equivalent through double entry bookkeeping

The logic of that is watertight

Bill Woolsey summarized it well in comments somewhere

LikeLike

It you define Expenditure and Income as 2 words for the same thing and you then have a chart with a 45 degree line representing this identity, and a line tracking E(Y) then it is nonsensical to talk about ever being away from the equilibrium point. No adjustment process could be described because none could ever be needed.

However while you are always at the point where E(Y) crosses the 45 degree line you could be at a point where planned E != actual E/Y. And it would be interesting to describe an adjustment process to bring these 2 into line, and this would probably involve things like inventory adjustments etc.

It may be more useful to have the 45 degree line representing a (non-definitional) equality between planned E and actual E/Y. You could then be at a point where actual Y/E is greater than planned E. You could then describe a process showing how both actual E/Y and planned E change and get to the equilibrium point where the lines cross.

LikeLike

Can you imagine a physicist claiming that the conservation of momentum and the conservation of energy can tell us nothing about the world, because they are identities? Really?

When Lipsey says, “The main issue in this whole discussion is, I think, can we use a definitional identity to rule out an imaginable state of the universe. The answer is “No”, which is why Keynes was wrong,” he is mistaken. In fact, identities eliminate almost all imaginable states of the universe.

LikeLike

JKH, There are physical conservation laws, and there are accounting identities. Physical conservation laws cannot be violated because doing so would involve creating something out of nothing. The equality of purchases and sales is akin to a conservation law because a purchase and a sale involves a transfer of the same item. Investment and savings are not physically the same thing and savers and investors are not the same people, so there is no reason to believe that planned saving and planned investment are equal, and you can’t just invoke an accounting identity to explain how it is that realized investment and realized saving are always equal.

You are free to interpret the algebraic equation that relates expenditure to income as a point if you like, but you have provided no mathematical or economic basis for doing so. The equation clearly defines a line not a point.

I don’t say that accountants can’t consistently define income, I’m just saying that for purposes of a theory of income and how it changes, the categories of national income accounting may not be the most useful way of formulating a theory. The way that a business firm defines income is not necessarily the way that a household determines what its income is. The household may only consider income to be received when the payment is actually made.

Scott, I’m sorry if I have misrepresented your position:

Explain to me please what you meant by this statement on your econolog blog which got me started on this series of posts:

In the standard national income accounting, gross domestic income equals gross domestic output. In the simplest model of all (with no government or trade) you have the following identity:

NGDI = C + S = C + I = NGDP (it also applies to RGDI and RGDP)

Because these two variables are identical, any model that explains one will, ipso facto, explain the other.

Rob, I prefer not to assume that savings and investment are both different words for “that part of output that is not consumer in the current period.” That is a fine definition of investment, but the people who decide how much to save are deciding how much of their disposable income not to consume in the current period. In deciding how much of their income they plan not to consume, they have no idea what total output is going to be.

JKH, The expenditure function is a notional construct. Just because only one point on the function corresponds to the actual solution of the model does not mean that the function is meaningless except at the point of intersection with the 45-degree line. If that were the case, how could you talk about the effect of a parameter change on equilibrium?

Rob, See my next post, which I am about to post.

Min, Conservation laws are identities because they embody an assumption about how the world works, namely you can’t create something out of nothing. The identity follows from the assumption about how the world works. Accounting identities may also embody some deeper assumption about how the world works, for example purchases equal sales, but it is not clear to me that the savings equals investment identity is an identity of that character.

LikeLike

David,

Given my particular interest in your approach to your subject in this series (I imagine not many do approach it), I appreciate your patience with so many comments. And I look forward to your next post in the series.

It seems very reasonable that physical conversation laws cannot be violated.

I agree investment and saving are not the same thing and have also said so a number of times in my comments.

But in a coherent (macroeconomic) accounting framework, the quantity of investment must the same as the quantity of saving. This holds for realized outcomes ex post and FEASIBLE planned outcomes ex ante. In other words, viable ex ante forecasts are constrained by the same accounting identities that measure realized ex post outcomes.

This also goes to the very meaning of algebra.

A = B does not mean that A and B are the same thing in algebra. It means they are different things that feature the same numerical measure in context. I’m surprised this is coming up as a point.

I agree there is no reason to believe that planned saving and planned investment are equal, but I think this is best qualified in the sense of aggregating up individual plans.

I disagree that you can’t just invoke an accounting identity to explain how it is that realized investment and realized saving are always equal. This is the consequence of a coherent accounting framework.

I agree that the algebraic equation that relates planned expenditure to income is a line, but there is only one point on that line that is realizable, which is the point on the 45 degree line. That planned expenditure line has to shift (i.e. change) for other points on the 45 degree line to be realizable. And that is a contradiction in terms of the alleged range of applicability of the given line. So the line is a non-line in terms of viable outcomes for actual expenditure and income. The line must itself change (i.e. shift) to achieve any other outcome.

I personally believe that macroeconomics requires coherent accounting foundations, and that business and household accounting need to be consistent from a macroeconomic application perspective. There is no reason why this can’t be achieved. Whether households view their own accounting framework in quite the same way as a coherent macroeconomic framework is a second order concern. That sort of disparity can be wrapped up into a behavioral model. But it shouldn’t be confused with the required integrity of accounting foundations for measuring outcomes for the entire economy.

A parameter change changes the expenditure “line”. The planned expenditure line will drop with a reduction in “aggregate demand”. This is a new line. That has the likely effect of pulling down actual expenditure as you point out in your inventory accumulation example I believe. But the effect occurs on the 45 degree line. It can’t be anywhere else. The visible “gap” between the two lines that is intended to portray inventory accumulation does not correspond to any realized point away from the 45 degree line – because there are no such points. Moreover, that static gap portrayal does not capture the dynamic which overtakes it – which is that of rolling down the 45 degree line instead of remaining in such a depicted state of inventory accumulation.

My own interpretation of that quote from Scott S as you state it: I see no problem. That’s just explaining the outcome of a model whose feasible outcomes are properly vetted by required accounting identities. That doesn’t mean reasoning from an accounting identity. It means explaining a model outcome in total that happens to be coherent and therefore feasible with respect to accounting foundations. Big difference.

Perhaps one may view accounting identities as laws of mathematical conservation.

LikeLike

David, The meaning is very simple. An identity tells us nothing about the causal process that explains changes in either side of the equation. Nothing at all. You seemed to suggest I believe it does, as when people (erroneously) argue that the equation of exchange shows that more M must lead to higher prices, or when people erroneously claim that more G must lead to more Y.

I never, ever, make that sort of idiotic argument. Instead I argue that IF, and I emphasize IF, you define S and I to be equal, by defining S to be the funds spent on investment, then any explanation of changes in S is, ipso facto, an explanation of changes in I. I can’t imagine anyone disagreeing with that proposition. It’s logic 101.

I can understand someone claiming that S=I is not a useful definition, that they’d prefer not to define them in such a way that they are equal, and that seems to be your position. That’s fine. If we define saving as you prefer, then any explanation of a change in savings is NOT an explanation of a change in investment. Again, that’s logic 101.

LikeLike

JKH, Thanks for your interest in this series, and I appreciate your challenging questions that are forcing me to think hard about the issues that you are raising.

You say that you agree that savings and investment are not the same thing, but assert that they must have the same numerical value. I am not sure how to interpret that. One dollar and one hundred cents are not the same thing, but they do necessarily have the same value. In your view is the identity between savings and investment of the same character as the identity between one dollar and one hundred cents? If not, how would you characterize the difference?

Obviously A = B allows A and B to be different, but we are talking about A ≡ B, not A = B. The question is whether the investment and saving are potentially different, but equal in equilibrium, or whether they are identically equal so that there is no possible state of affairs in which they are not equal.

In a system of simultaneous equations, the only possible solution occurs at the point of intersection of all the lines. No other point is viable as a solution. That doesn’t mean that the lines have no meaning anywhere except at the point of intersection.

Scott, I don’t believe that I have ever seen savings defined as “funds spent on investment.” Saving is usually defined as “unspent income.” The question is how is it that unspent income winds up being identically equal to “funds spent on investment.” As far as I can tell “funds spent on investment” is the definition of investment. Now in the world of microeconomics, we do say that purchases are identical with sales. That is because there is an identity between purchases and sales that is implied by the definitions of purchase and sale, which are reciprocal activities. So it would make sense to say that if you explain the changes in purchases you have ipso facto explained the changes in sales. But certainly that would not be the same as saying that if you explain the change in quantity demanded you have explained the change in quantity supplied. I would hope you would agree that explaining the change in quantity demanded does not explain the change in quantity supplied. But I don’t believe that most people (or most economists) believe that the equality between investment and savings is directly entailed by the definition of either saving or investing in the same way that equality between purchases and sales is entailed by the definition of purchasing and selling.

LikeLike

David, Textbooks define S=I as an identity. I don’t know what else to say other than you are wrong. Now that may not be the way you’d like to see it defined, but an identity is a definition.

LikeLike

Scott, Yes textbooks do define investment and savings as an identity, but they also describe the equality of income and savings as an equilibrium condition. How can the equality of saivngs and investment be both an identity and an equilibrium condition? In ordinary English, savings has a meaning that is distinct from investment, so obviously there is some unclarity in the way these terms are being used by economists and by ordinary people. I am trying to work through this unclarity and come up with a way of understanding the different meanings that we attach to savings and investment. You seem to think that the savings-investment identity takes precedence and that nothing else matters, because that’s what it says in the textbooks. Why are you being so deferential to the textbooks?

LikeLike

I’m being deferential because I find the identity definition far more useful than the alternative. And for exactly the same reason that I find the MV=PY identity version more useful than the MV=PY theory version. It simplifies thinking about the economy, so you can focus on the essentials. Suppose we accept the theory version of MV = PY. Then you need to model M, V and the discrepancy. In the identity version you just have to model M and V, to explain NGDP.

As far as I know GDI = GDP is also viewed as an identity–at least that’s how I’ve always seen it presented. And the reason is simple, if S=I is an identity, then ipso facto C + S = C + I is also an identity.

LikeLike

Scott, You said:

“Suppose we accept the theory version of MV = PY. Then you need to model M, V and the discrepancy. In the identity version you just have to model M and V, to explain NGDP.”

Forgive me, but I don’t understand this at all. If I have a monetary theory of NGDP — and, despite your disclaimer, I believe that you do, as well — I am saying that NGDP in some loose sense are causally related to M and V, so that if I can know or can predict what happens to M and V, I can predict (approximately) what will happen to NGDP. My theory of NGDP may be right or wrong (or somewhere in between), but it has empirical content. It could be refuted by the observed movements of M, V and NGDP. So it has some explanatory power.

But if all you are working with is the identity that MV is equal, by definition, to NGDP, you have no basis for making any causal inference about NGDP from changes in M or V. No possible observation could ever refute the identity, because V is defined as NGDP divided by M.

In a monetary theory of NGDP, V is modeled. In the MV = PY identity, V is not modeled; it is a residual.

Milton Friedman would be spinning in his grave if he could hear you saying that. The idea that making a MV=PY an irrefutable identity rather than a refutable theory with empirical content would have flabbergasted him. (Actually, I am kind of flabbergasted, myself, at the thought that I am invoking Friedman to make a point in a disagreement with you. What is this world coming to?)

You said:

“GDI = GDP is also viewed as an identity–at least that’s how I’ve always seen it presented. And the reason is simple, if S=I is an identity, then ipso facto C + S = C + I is also an identity.”

Actually, I think the derivation usually goes in the other direction. GDI and GDP (alternatively E and Y) are defined to be always equal, and the identity of savings and investment follows from the ncome-expenditure identity. But that’s just a quibble. The substantive point is that in the identity approach, I and S are not treated as independently measurable quantities, so the theory has no empirical content. There is no way any prediction about I or S or E or Y could ever be refuted, just as the quantity identity cannot be refuted if V is treated as a residual rather than as an independently observable and measurable magnitude.

LikeLike

@Scott, David

Maybe this adds to the discussion: The identity approach would imply that the measures of GDP and GDI would have not only the same value, but the same errors — the measured data from which GDI was constructed would be exactly the measured data from which GDP is constructed if it is an identity. The equilibrium condition approach allows them to have independent errors, since they aren’t constructed from the exact same measurements.

In the former case (constructed from same measurements) there is no content (empirical or theoretical), in the latter there is:

http://research.stlouisfed.org/fred2/graph/?g=14Rb

LikeLike