A couple of weeks ago, I wrote a post chiding John Taylor for his habitual verbal carelessness. As if that were not enough, Taylor, in a recent talk at the IMF, appearing on a panel on monetary policy with former Fed Chairman Ben Bernanke and the former head of the South African central bank, Gill Marcus, extends his trail of errors into new terrain: historical misstatement. Tony Yates and Paul Krugman have already subjected Taylor’s talk to well-deserved criticism for its conceptual confusion, but I want to focus on the outright historical errors Taylor blithely makes in his talk, a talk noteworthy, apart from its conceptual confusion and historical misstatements, for the incessant repetition of the meaningless epithet “rules-based,” as if he were a latter-day Homeric rhapsodist incanting a sacred text.

Taylor starts by offering his own “mini history of monetary policy in the United States” since the late 1960s.

When I first started doing monetary economics . . ., monetary policy was highly discretionary and interventionist. It went from boom to bust and back again, repeatedly falling behind the curve, and then over-reacting. The Fed had lofty goals but no consistent strategy. If you measure macroeconomic performance as I do by both price stability and output stability, the results were terrible. Unemployment and inflation both rose.

What Taylor means by “interventionist,” other than establishing that he is against it, is not clear. Nor is the meaning of “bust” in this context. The recession of 1970 was perhaps the mildest of the entire post-World War II era, and the 1974-75 recession was certainly severe, but it was largely the result of a supply shock and politically imposed wage and price controls exacerbated by monetary tightening. (See my post about 1970s stagflation.) Taylor talks about the Fed’s lofty goals, but doesn’t say what they were. In fact in the 1970s, the Fed was disclaiming responsibility for inflation, and Arthur Burns, a supposedly conservative Republican economist, appointed by Nixon to be Fed Chairman, actually promoted what was then called an “incomes policy,” thereby enabling and facilitating Nixon’s infamous wage-and-price controls. The Fed’s job was to keep aggregate demand high, and, in the widely held view at the time, it was up to the politicians to keep business and labor from getting too greedy and causing inflation.

Then in the early 1980s policy changed. It became more focused, more systematic, more rules-based, and it stayed that way through the 1990s and into the start of this century.

Yes, in the early 1980s, policy did change, and it did become more focused, and for a short time – about a year and a half – it did become more rules-based. (I have no idea what “systematic” means in this context.) And the result was the sharpest and longest post-World War II downturn until the Little Depression. Policy changed, because, under Volcker, the Fed took ownership of inflation. It became more rules-based, because, under Volcker, the Fed attempted to follow a modified sort of Monetarist rule, seeking to keep the growth of the monetary aggregates within a pre-determined target range. I have explained in my book and in previous posts (e.g., here and here) why the attempt to follow a Monetarist rule was bound to fail and why the attempt would have perverse feedback effects, but others, notably Charles Goodhart (discoverer of Goodhart’s Law), had identified the problem even before the Fed adopted its misguided policy. The recovery did not begin until the summer of 1982 after the Fed announced that it would allow the monetary aggregates to grow faster than the Fed’s targets.

So the success of the Fed monetary policy under Volcker can properly be attributed to a) to the Fed’s taking ownership of inflation and b) to its decision to abandon the rules-based policy urged on it by Milton Friedman and his Monetarist acolytes like Alan Meltzer whom Taylor now cites approvingly for supporting rules-based policies. The only monetary policy rule that the Fed ever adopted under Volcker having been scrapped prior to the beginning of the recovery from the 1981-82 recession, the notion that the Great Moderation was ushered in by the Fed’s adoption of a “rules-based” policy is a total misrepresentation.

But Taylor is not done.

Few complained about spillovers or beggar-thy-neighbor policies during the Great Moderation. The developed economies were effectively operating in what I call a nearly international cooperative equilibrium.

Really! Has Professor Taylor, who served as Under Secretary of the Treasury for International Affairs ever heard of the Plaza and the Louvre Accords?

The Plaza Accord or Plaza Agreement was an agreement between the governments of France, West Germany, Japan, the United States, and the United Kingdom, to depreciate the U.S. dollar in relation to the Japanese yen and German Deutsche Mark by intervening in currency markets. The five governments signed the accord on September 22, 1985 at the Plaza Hotel in New York City. (“Plaza Accord” Wikipedia)

The Louvre Accord was an agreement, signed on February 22, 1987 in Paris, that aimed to stabilize the international currency markets and halt the continued decline of the US Dollar caused by the Plaza Accord. The agreement was signed by France, West Germany, Japan, Canada, the United States and the United Kingdom. (“Louvre Accord” Wikipedia)

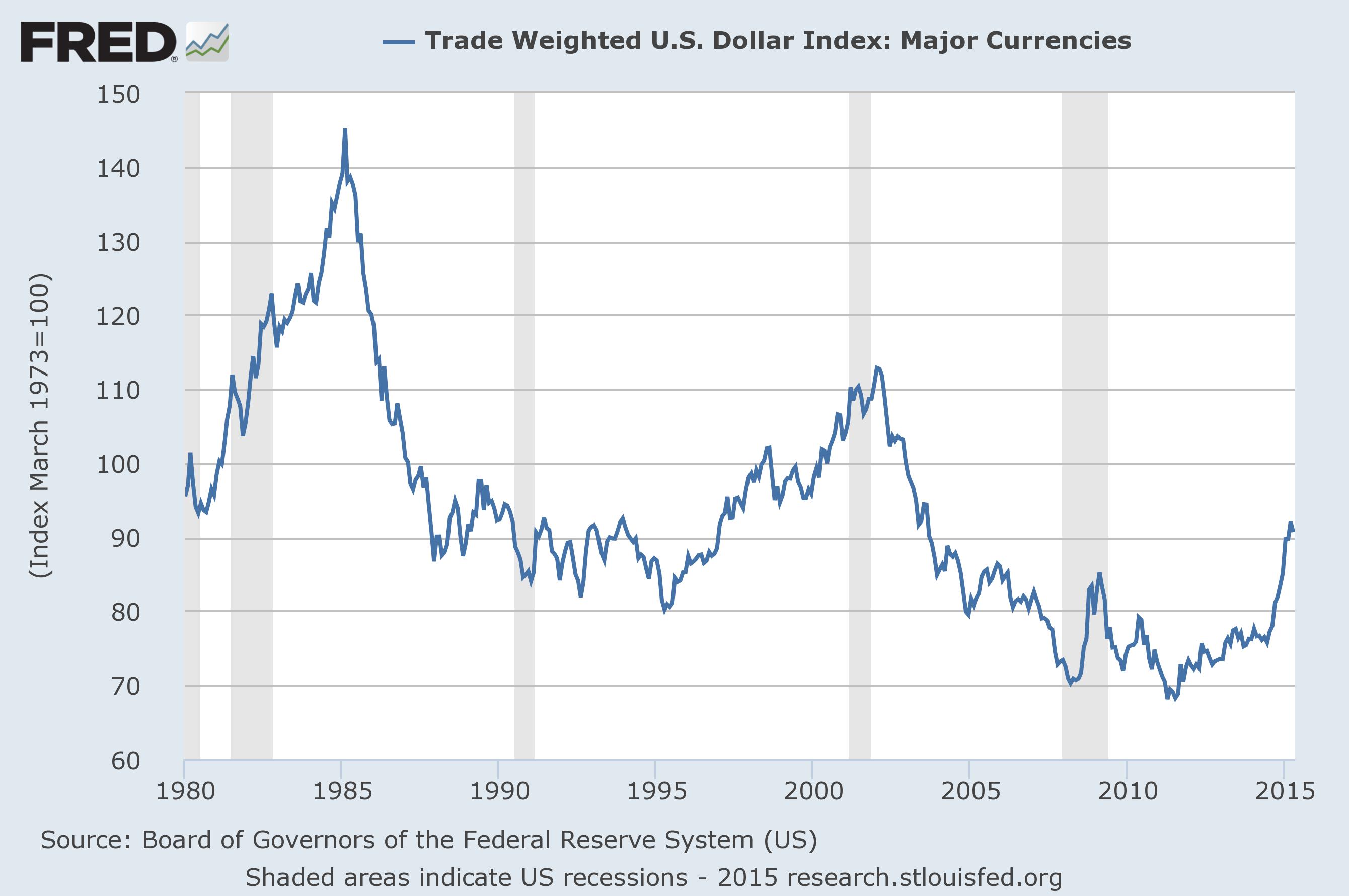

The chart below shows the fluctuation in the trade weighted value of the US dollar against the other major trading currencies since 1980. Does it look like there was a nearly international cooperative equilibrium in the 1980s?

But then there was a setback. The Fed decided to hold the interest rate very low during 2003-2005, thereby deviating from the rules-based policy that worked well during the Great Moderation. You do not need policy rules to see the change: With the inflation rate around 2%, the federal funds rate was only 1% in 2003, compared with 5.5% in 1997 when the inflation rate was also about 2%.

Well, in 1997 the expansion was six years old and the unemployment rate was under 5% and falling. In 2003, the expansion was barely under way and unemployment was rising above 6%.

I could provide other dubious historical characterizations that Taylor makes in his talk, but I will just mention a few others relating to the Volcker episode.

Some argue that the historical evidence in favor of rules is simply correlation not causation. But this ignores the crucial timing of events: in each case, the changes in policy occurred before the changes in performance, clear evidence for causality. The decisions taken by Paul Volcker came before the Great Moderation.

Yes, and as I pointed out above, inflation came down when Volcker and the Fed took ownership of the inflation, and were willing to tolerate or inflict sufficient pain on the real economy to convince the public that the Fed was serious about bringing the rate of inflation down to a rate of roughly 4%. But the recovery and the Great Moderation did not begin until the Fed renounced the only rule that it had ever adopted, namely targeting the rate of growth of the monetary aggregates. The Fed, under Volcker, never even adopted an explicit inflation target, much less a specific rule for setting the Federal Funds rate. The Taylor rule was just an ex post rationalization of what the Fed had done by instinct.

Another point relates to the zero bound. Wasn’t that the reason that the central banks had to deviate from rules in recent years? Well it was certainly not a reason in 2003-2005 and it is not a reason now, because the zero bound is not binding. It appears that there was a short period in 2009 when zero was clearly binding. But the zero bound is not a new thing in economics research. Policy rule design research took that into account long ago. The default was to move to a stable money growth regime not to massive asset purchases.

OMG! Is Taylor’s preferred rule at the zero lower bound the stable money growth rule that Volcker tried, but failed, to implement in 1981-82? Is that the lesson that Taylor wants us to learn from the Volcker era?

Some argue that rules based policy for the instruments is not needed if you have goals for the inflation rate or other variables. They say that all you really need for effective policy making is a goal, such as an inflation target and an employment target. The rest of policymaking is doing whatever the policymakers think needs to be done with the policy instruments. You do not need to articulate or describe a strategy, a decision rule, or a contingency plan for the instruments. If you want to hold the interest rate well below the rule-based strategy that worked well during the Great Moderation, as the Fed did in 2003-2005, then it’s ok as long as you can justify it at the moment in terms of the goal.

This approach has been called “constrained discretion” by Ben Bernanke, and it may be constraining discretion in some sense, but it is not inducing or encouraging a rule as a “rules versus discretion” dichotomy might suggest. Simply having a specific numerical goal or objective is not a rule for the instruments of policy; it is not a strategy; it ends up being all tactics. I think the evidence shows that relying solely on constrained discretion has not worked for monetary policy.

Taylor wants a rule for the instruments of policy. Well, although Taylor will not admit it, a rule for the instruments of policy is precisely what Volcker tried to implement in 1981-82 when he was trying — and failing — to target the monetary aggregates, thereby driving the economy into a rapidly deepening recession, before escaping from the positive-feedback loop in which he and the economy were trapped by scrapping his monetary growth targets. Since 2009, Taylor has been calling for the Fed to raise the currently targeted instrument, the Fed Funds rate, even though inflation has been below the Fed’s 2% target almost continuously for the past three years. Not only does Taylor want to target the instrument of policy, he wants the instrument target to preempt the policy target. If that is not all tactics and no strategy, I don’t know what is.