Paul Volcker is a big man, 6 feet 7 inches tall. He is also a great man — truly great. Appointed chairman of the Federal Reserve Board in 1979 after his predecessor, the unfortunate G. William Miller, obviously out of his depth, had to be replaced to avoid a collapse of confidence in the dollar. A consensus quickly formed that only one man, Paul Volcker, then President of the New York Federal Reserve Bank, could restore the confidence of the nation and the rest of the world in the US monetary system. Facing double-digit inflation, Volcker immediately took the steps needed to bring inflation down, raising interest rates and slowing monetary expansion, precipitating a recession in the process, a recession intensified by rapidly rising oil prices in the wake of the Iranian Revolution that brought the Ayatollah Khomeini to power. However, the year was 1980, and Jimmy Carter, desperately seeking reelection, demanded a relaxation of monetary policy, forcing Volcker to subordinate monetary policy to Carter’s political requirements. After Carter lost the election anyway, Ronald Reagan, who had pledged to bring inflation under control, gave Volcker a blank check to do whatever was necessary to reduce — but not eliminate — inflation. And so he did, but it wasn’t pretty. Interest rates skyrocketed to the highest levels in US history, unemployment rising above 10 percent for the first time since the Great Depression. But Volcker, notwithstanding almost universal condemnation, held fast, and in the end gained vindication for his courageous anti-inflation stance. In the annals of central banking, there are few, if any, figures that loom any larger than Paul Volcker.

So when Paul Volcker writes a column in the New York Times, warning against any increase in the Fed’s inflation target as a means of hastening our painfully slow recovery (if we can even call it that) from the Little Depression of 2008-09, his opinion cannot be dismissed lightly.

There is great and understandable disappointment about high unemployment and the absence of a robust economy, and even concern about the possibility of a renewed downturn. There is also a sense of desperation that both monetary and fiscal policy have almost exhausted their potential, given the size of the fiscal deficits and the already extremely low level of interest rates.

So now we are beginning to hear murmurings about the possible invigorating effects of “just a little inflation.” Perhaps 4 or 5 percent a year would be just the thing to deal with the overhang of debt and encourage the “animal spirits” of business, or so the argument goes.

It’s not yet a full-throated chorus. But remarkably, at least one member of the Fed’s policy making committee recently departed from the price-stability script.

The siren song is both alluring and predictable. Economic circumstances and the limitations on orthodox policies are indeed frustrating. After all, if 1 or 2 percent inflation is O.K. and has not raised inflationary expectations — as the Fed and most central banks believe — why not 3 or 4 or even more? Let’s try to get business to jump the gun and invest now in the expectation of higher prices later, and raise housing prices (presumably commodities and gold, too) and maybe wages will follow. If the dollar is weakened, that’s a good thing; it might even help close the trade deficit. And of course, as soon as the economy expands sufficiently, we will promptly return to price stability.

Well, good luck.

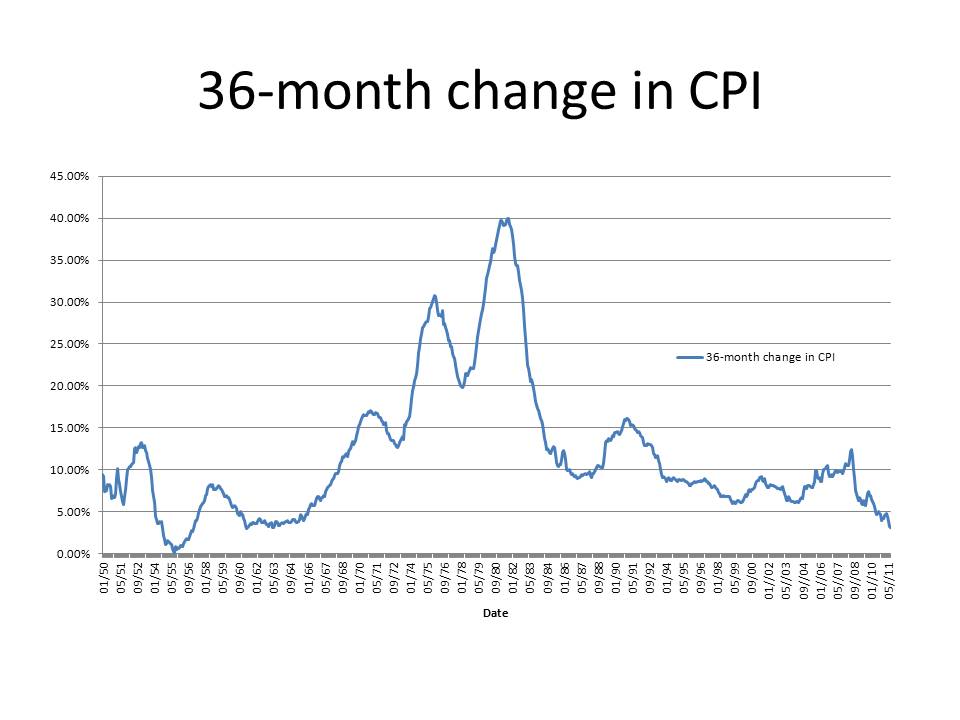

Some mathematical models spawned in academic seminars might support this scenario. But all of our economic history says it won’t work that way. I thought we learned that lesson in the 1970s. That’s when the word stagflation was invented to describe a truly ugly combination of rising inflation and stunted growth.

Well, I am not ashamed to admit to being somewhat overawed and intimidated by Paul Volcker. So I am going to call on Mark Twain to respond to Mr. Volcker on my behalf. “We should be careful,” Mr. Twain observes, “to get out of an experience all the wisdom that is in it — not like the cat that sits on a hot stove lid. She will never sit down on a hot lid again — and that is well; but also she will never sit down on a cold one anymore.“

What Mark Twain meant was that history alone can’t teach us anything. To learn anything from history, we need a theory to explain why history worked out as it did. The cat doesn’t have a theory, so she learns the wrong lesson: don’t sit down on a stove lid. But, with the benefit of a theory, we know that the lesson that the cat ought to have learned was: don’t sit down on a hot stove lid.

Paul Volcker is a practical man. That was one of his great strengths as a central banker, but it can also be a weakness when his practical instinct leads him to take an overly simplified – dare I say, simplistic – view of a complicated economic disorder. Mr. Volcker knows from experience how terribly difficult it is to eradicate, or even reduce, inflationary expectations after they have become embedded in the psychological fabric of an economy. Lacking a theory of how inflation might be an essential element of a recovery from a recession in which profit and demand expectations have become deeply pessimistic, Mr. Volcker assumes that every inflation is of exactly the same type as the one with which he had to contend in the early 1980s. Like the cat, he thinks that every lid is hot.

Well, that wasn’t quite fair. Mr. Volcker is not like the cat. He acknowledges that there may be “mathematical models spawned in academic seminars” in which inflation could be essential, or at least very conducive, to a recovery. But, as a practical man, he cannot bring himself to take seriously the esoteric mathematical models supporting such a scenario. The condescending reference to mathematical models and academic seminars, however, betrays Mr. Volcker’s own anti-theoretical bias, because one doesn’t need a mathematical model to see how inflation could promote recovery. That conclusion is a straightforward implication of straightforward macroeconomics that has been understood for at least a century. The question is whether we should take the risk that if we use inflation to get a recovery going, we will become hopelessly hooked on inflation, like someone experimenting with drugs becoming addicted after his first fix, or the risk that our slow, faltering recovery is really a reflection of deep structural problems immune to the stimulus of inflation.

Furthermore, Mr. Volcker’s view of economic history seems to be focused almost exclusively on the 1970s, which is understandable, but not necessarily practical. It would also be worth paying attention to March 1933, when FDR, taking office with an economy seemingly unable to recover from the Great Depression, prices having fallen 30% or more since 1929, suspended the gold standard and announced a goal of restoring the US price level to where it had been in 1926. By devaluing the dollar, Roosevelt produced a rapid rise in prices (wholesale price rose 14 percent from April to July 1933), triggering the fastest recovery in US history, industrial output increasing by over 70% from April to July while the Dow Jones average nearly doubled.

So, yes, Mr. Volcker, history shows that inflation can produce a recovery. Maybe we need to learn from it.

{kind=link}

{kind=link}