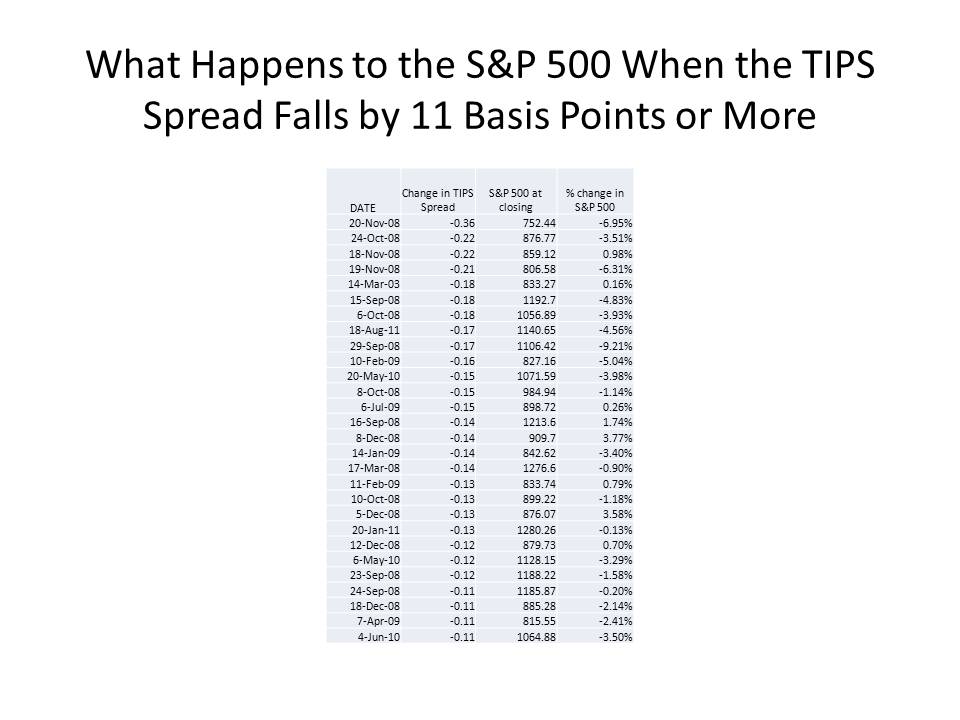

On August 18, I did a post after the S&P 500 fell by 4.6% to 1140.65, observing that inflation expectations as reflected in the breakeven TIPS spread on constant-maturity 10-year Treasuries fell by a whopping 18 basis points from 2.17% to 1.99%. I also provided a table showing that in 26 instances in which inflation expectations (measured by the 10-year constant maturity TIPS spread) had fallen by 11 basis points or more in a single day since September 2008, 17 had been associated with a decline of more than 1% in the S&P 500. Today, the TIPS spread fell by 15 basis points from 1.86% to 1.71% while the S&P 500 fell by 3.2%. (For an explanation of the theory behind this relationship and for a description of the econometric evidence supporting it, see my paper here and an earlier post on this blog.) Inflation expectations are now at their lowest point in over a year just about the time that Chairman Bernanke and other Fed officials began signalling that they were concerned about the dangers of deflation. The S&P 500 is now barely above its low for 2011, and only about 7-8% above its level in August 2010 just before the Fed moved to ease deflationary fears.

Josh Hendrickson provides a good explanation for why the Fed’s feeble moves to flatten the yield curve are irrelevant to the problem now staring us in the face: price level expectations are not high enough to make capacity-expanding investment worthwhile. Even though profits are high at current levels of output, businesses have no confidence that they can sell increased output at prices that will generate a return on investment. They therefore hold on to their cash hoards, investing only in projects that reduce their costs without expanding capacity, carefully limiting the hiring of new workers, lest they have to lay them off later because of insufficient demand.

And with inflation expectations dropping like a stone, Professor John Taylor can think of nothing better than to admonish the Fed for even mentioning that it has a mandate to promote full employment in addition to ensuring price stability.

[F]or most of the 1980s and 1990s — starting when Paul Volcker became chairman — the Fed stressed the goal of price stability in its actions. The result was much lower unemployment than before or since.

Sorry to be pedantic, but what exactly does Professor Taylor mean when he says “the Fed stressed the goal of price stability in its actions?” I know actions speak louder than words, but is Professor Taylor saying that inflation was lower under Paul Volcker’s chairmanship than it is now? I don’t think so! Even after the 1981-82 recession, the average rate of inflation was higher under Chairman Volcker than it has been since 2008 (see here). Is he saying that the Fed under Chairman Volcker was aiming (and, evidently, missing) at a lower rate of inflation than the Fed is now? Well since the Fed did not even have an explicit inflation target under Chairman Volcker while the current inflation target is 2% or a bit less, I can’t see how that is possible, though I would love to hear Professor Taylor’s explanation. But perhaps Professor Taylor, in his wisdom, knows how to infer something else from his “reading” of the Fed’s “actions” under Chairman Volcker? Or perhaps Professor Taylor knows how to compare Chairman Volcker’s body language to Chairman Bernanke’s body language. Or maybe Professor Taylor is playing to a certain audience that likes to hear a respected academic economist bash the Fed? But I can’t imagine who could possibly be in that audience. I must be hallucinating.

{kind=link}

{kind=link}

Not to defend Taylor, but don’t you think what he means is that FOMC minutes seldom mentioned full employment? I have no idea if this is true, and don’t think it would support Taylor’s claims if it were (much more sensible to think that success at maintaining full employment leads to not talking about the goal, rather than vice versa) but it seems like a perfectly meaningful thing to say, that doesn’t require reading anyone’s body language.

LikeLike

David,

Your wrote, “businesses have no confidence that they can sell increased output at prices that will generate a return on investment.”

IMO, this view is fundamentally wrong. Margins are at peak. The next dollar of output, if sold, would doubtless provide a decent margin and ROI. Perhaps something a bit lower than peak, but still quite robust.

The problem is not margins or return on investment; rather, it is the uncertainty regarding demand for the additional output. Inflation might, theoretically, boos that demand, but that relationship is much more tenuous than that between prices, margins, returns and investment spending.

I keep seeing a tendency to want to make 2011 seem like a lesser version of 1932. It is understandable, but in my view incorrect.

LikeLike

I am not certain there was lower unemployment under Volcker. It seems to me his Friedmanesque monetarism of clamping down on the money supply created unemployment on a scale not seen until today.

re previous comment: IMO you are exactly right. Businesses have no confidence they can sell their output at a profit. If they did, they would invest and sell. Hard to argue that one.

LikeLike

demand side,

I think you misunderstood my comment. I am arguing that the problem is not prices — deflation — but a lack of volume demand. In contrast to the GD when deflation caused prices to fall much more than input costs, in this recovery margins have expanded significantly. Prices are not the problem.

The question is, would prices collapse if businesses tried to sell more output, such that margins would be squeezed? I think this is the implication of what David is saying, and I don’t see how businesses worry that this is the problem.

LikeLike

The standard assumption is that in modern capitalist economies, firms are imperfectly competitive and normally produce on the flat section of the cost curve. (Finding firms operating on upward sloping supply curves in the real world is exceptionally difficult, except in situations like all-out mobilization in wartime.) The profit-maximizing price for such a firm does not vary with its level of output.

Instead, the firm sets its price at a markup, determined by the price-elasticity of demand, over its (fixed) marginal cost; it then sells as much as it can at that price. If that level of output puts it at the high end of normal capacity utilization (i.e. approaching the increasing-cost portion of the supply curve) then it invests to increase capacity, *if* financing is available.

So if we see low levels of business investment (which is debatable right now) then it is sensible to ask if they are low because of lack of demand, or because of lack of financing. But margins are not informative either way. It’s perfectly possible for investment to be demand-constrained when margins are high, or for firms to be investing more to meet greater demand even when margins are falling. It all depends on how the price-elasticity of demand changes with the output level, and there’s no reason to have strong priors on that either way.

LikeLike

Perhaps I do not understand. If I hear you saying that trying to sell more would not reduce margins, I disagree. Margins increased on account of aggressive cost-cutting on the labor front. If they reverse this cost-cutting (well, they have little choice, at least to reduce the rate of reduction), and don’t sell it, margins have to come down. Other input prices have gone up. See the recent National Economics Club presentation by Chad Mountray, chief economist at NAM. Producer prices are driven up by higher commodity prices. He says explicitly that these are squeezing margins. It could be that refinancing from the largesse of the Fed has reduced costs, that could well be. I don’t know about that. That would certainly allow margins to go up.

If you are saying that they could increase output and find more demand, I don’t follow.

I am very sure that producers have made this calculation, whether they could increase output and what would happen to margins. I am very much sure they made the high-profit choice.

LikeLike

As long as the Fed persists in keeping to their inflation / unemployment targeting, shouldn’t they at least pick a number for the inflation target and a lambda?

They would then try to minimize: delta-inflation + lambda * delta-unemployment (or perhaps square the deltas)

Wouldn’t that be a pretty big improvement compared to what we have today?

LikeLike

JW On this blog you are allowed — perhaps not encouraged, but certainly allowed — to defend Taylor. You are right that Taylor was drawing on the absence of references to the dual mandate in the Volcker era. But in the Volcker era, the Fed’s goals were totally opaque except that obviously the whole point of Volcker’s monetary policy was to bring inflation down regardless of the effect on employment. However, clearly at some point before achieving price stability, or even a rate of inflation as low as the current rate, much less the current expected rate, the Fed declared victory and eased up its policy (actually stopped trying to target the monetary aggregates). I was reading Taylor very strictly. He said the Fed under Volcker “stressed the goal of price stability in its actions.” And I still don’t understand how you can make senses of the statement. It’s just a nonsense statement.

David, demand side and JW That was a helpful discussion for me at least in clarifying the microeconomic assumptions underlying an analysis of current investment decisions by business. The way to think about is that businesses don’t want to commit to expanding capacity (and this especially true in a risky macro environment) until they are pretty sure that they are operating near capacity. That’s probably also true for hiring substantial numbers of new workers. Would increasing inflation expectations make much difference in their decisions to expand capacity? Maybe not by itself, but combined with other demand expanding effects of increased inflation expectations, maybe so.

LikeLike