Robert Waldmann has been criticizing my arguments for the importance of monetary policy in accounting for both the 2008 downturn and the weakness of the subsequent recovery. He raises interesting issues which I think warrant a response. In my previous response to Waldmann, I closed with the following paragraph:

I think that the way to pick out changes in monetary policy is to look at changes in inflation expectations, and I think that you can find some correlation between changes in monetary policy, so identified, and employment, though it is probably not nearly as striking as the relationship between asset prices and inflation expectations. I also don’t think that operation twist had any positive effect, but QE3 does seem to have had some. I am not familiar with the study by the San Francisco Fed economists, but I will try to find it and see what I can make out of it. In the meantime, even if Waldmann is correct about the relationship between monetary policy and employment since 2008, there are all kinds of good reasons for not rushing to reject a null hypothesis on the basis of a handful of ambiguous observations. That wouldn’t necessarily be the calm and reasonable thing to do.

Waldmann replied as follows on his blog:

Get the null on your side is my motto (I admit it). You follow this. You suggest that your hypothesis is the hull hypothesis then abuse Neyman and Person by implying that we can draw interesting conclusions from failure to reject the null. Basically the sentence which includes the word “null” is the assertion that we should assume you are right and I am wrong until I offer solid proof. To be briefer, since we are working in social science, you are asking that I assume you are right. This is not an ideal approach to debate.

I ask you to review your sentence which contains the word “null” and reconsider if you really believe it. The choice of the null should be harmless (it is an a priori choice without a prior). How about we make the usual null hypothesis that an effect is zero. Can you reject the null that monetary policy since 2009 has had no effect ? At what confidence level is the null rejected ? Did you use a t-test ? an f-test ? “null” is a technical term and I ask again if you would be willing to retract the sentence including the word “null”.

First, I was careless in identifying my hypothesis that monetary policy is an important factor with the “null” hypothesis. The convention in statistical testing is to identify the null hypothesis as alternative to the hypothesis being tested. What I meant to say was that even if the evidence is not sufficient to reject the null hypothesis that monetary policy is ineffective, there may still be good reason not to reject the alternative or maintained hypothesis that monetary policy is effective. In the real world, there is ambiguity. Evidence is not necessarily conclusive, so we accept for the most part that there really are alternative ways of looking at the world and that, as a practical matter, we don’t have sufficient evidence to reject conclusively either the null or the maintained hypothesis. With the relatively small numbers of observations that we are working with, statistical tests aren’t powerful enough to reject the null with a high level of confidence, so I have trouble accepting the standard statistical model of hypothesis testing in this context.

But even aside from the paucity of observations, there is a deeper problem which is that, as Karl Popper the arch-falsificationist was among the first to point out, observations are not independent of the underlying theory. We use the theory to interpret what we are observing. Think of Galileo, he was confronted with people telling him that the theory that the earth is travelling around a stationary sun is obviously refuted by the clear evidence that the earth is stationary and that it is the sun that is moving in the sky. Galileo therefore had to write a whole book in which he explained, using the Copernican theory, how to interpret the apparent evidence that the earth is stationary and the sun is moving. By doing so, Galileo didn’t prove that the earth-centric model was wrong, he simply was able to show that what his opponents regarded as conclusive empirical validation of their theory was not conclusive, inasmuch as the Copernican theory was able to interpret the supposedly contradictory evidence in a manner that is consistent with the premises of the Copernican theory. As Kuhn showed in the Structure of Scientific Revolutions, the initial astronomical evidence was more supportive of the Ptolomaic hypothesis than of the Copernican hypothesis. It was only because the Copernicans didn’t give up prematurely that they eventually gathered sufficient evidence to overwhelm the opposition.

Waldmann continues:

using expected inflation to identify monetary policy is only a valid statistical procedure if one is willing to assume that nothing else affects expected inflation. If you think that say OPEC ever had any influence on expected inflation, then you can’t use your identifying assumption. In particular TIPS breakevens can be fairly well fit (not predicted because not out of sample) using lagged data other than data on what the FOMC did.

again I refer to

http://www.angrybearblog.com/2013/02/inflation-expectations-and-lagged.html

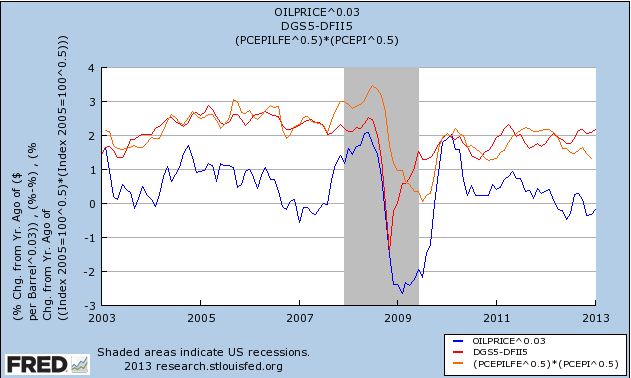

[Here is the chart to which Waldmann refers.]

(legend here red is the 5 year TIPS breakeven or expected inflation, Blue is the change over the *past* year of the price of a barrel of oil times 0.1 plus 1.6, green is the geometric mean of the change over the *past year* of the personal consumption deflator and the personal consumption minus food and energy deflator.

Again, I don’t think formal statistical modeling is the issue here, because the data are neither sufficient in quantity nor unambiguous in their interpretation. The data are what they are, and if we cannot parse out what has been caused by OPEC and what has been caused by the Fed, we have to accept the ambiguity and not pretend that it doesn’t exist just so to impose an identifying assumption. I would also make what I would have thought is an obvious observation that since 2007 the causality between the price of oil and the state of the economy has been going in both directions, and any statistical model that takes the price of oil as exogenous is incredible.

I don’t see how anyone could look at this graph and then claim we can identify monetary policy by the TIPS breakeven. That is only valid if nothing but monetary policy affects inflation expectations.

I don’t understand that. Why, if monetary policy accounts for 50% of the variation in inflation expectations is it not valid to use the TIPS spread to identify monetary policy? We may have to make some plausible assumptions about when there were supply-side disturbances or add some instrumental variables, but I don’t see why we would want to ignore monetary policy just because factors other than monetary policy may be affecting inflation expectations.

Similarly in 1933 monetary policy wasn’t the only thing that changed. I understand that there was considerable policy reform in the so called “first hundred days. ” The idea that we can identify the effect of monetary policy by looking at the USA in 1933 is based on the assumption that Roosevelt did nothing else. This is not reasonable.

Sure he did other things, but you can’t seriously mean that government spending increased in the first 100 days by an amount sufficient to account for the explosion in output from April to July. I would concede that other things that Roosevelt did may have also helped restore confidence, but I don’t see how you can deny that the devaluation of the dollar was at or near the top of the list of economic actions taken in the first 4 months of his Presidency.

But I think we can detect the effect of recent monetary policy on TIPS breakevens if we agree that it (including QE) is working principally through forward guidance. There should be quick effects on asset prices when surprising shifts are announced. QE 4 (December 2012) was definitely a surprise. The TIPS spread barely moved (within the range of normal fluctuations). I think the question is settled. I do not think it is optimal to ignore daily data when you have it and treat same quarter as the same instant. Some prices are sticky and some aren’t. Bond prices aren’t.

What makes you so sure that QE4 was a surprise. I think that there was considerable disappointment that there was no increase in the inflation target, just a willingness to accept some slight amount of overshooting (2.5%) before applying the brakes as long as unemployment remains over 6.5%. Ambiguity reins supreme.