I wasn’t planning to post today, but I just saw (courtesy of the New York Times) a classic example of the economic prejudice wrapped in high-minded sloganeering that I talked about yesterday. David Rocker, founder and former managing general partner of the hedge fund Rocker Partners, proclaims that he is in favor of a free market.

The worldwide turbulence of recent days is a strong indication that government intervention alone cannot restore the economy and offers a glimpse of the risk of completely depending on it. It is time to give the free market a chance. Since the crash of 2008, governments have tried to stimulate their economies by a variety of means but have relied heavily on manipulating interest rates lower through one form or other of quantitative easing or simply printing money. The immediate rescue of the collapsing economy was necessary at the time, but the manipulation has now gone on for nearly seven years and has produced many unwanted consequences.

In what sense is the market less free than it was before the crash of 2008? It’s not as if the Fed before 2008 wasn’t doing the sorts of things that are so upsetting to Mr. Rucker now. The Fed was setting an interest rate target for short-term rates and it was conducting open market purchases (printing money) to ensure that its target was achieved. There are to be sure some people, like, say, Ron Paul, that regard such action by the Fed as an intolerable example of government intervention in the market, but it’s not something that, as Mr. Rucker suggests, the Fed just started to do after 2008. And at a deeper level, there is a very basic difference between the Fed targeting an interest rate by engaging in open-market operations (repeat open-market operations) and imposing price controls that prevent transactors from engaging in transactions on mutually agreeable terms. Aside from libertarian ideologues, most people are capable of understanding the difference between monetary policy and government interference with the free market.

So what really bothers Mr. Rucker is not that the absence of a free market, but that he disagrees with the policy that the Fed is implementing. He has every right to disagree with the policy, but it is misleading to suggest that he is the one defending the free market against the Fed’s intervention into an otherwise free market.

When Mr. Rucker tries to explain what’s wrong with the Fed’s policy, his explanations continue to reflect prejudices expressed in high-minded sloganeering. First he plays the income inequality card.

The Federal Reserve, waiting for signs of inflation to change its policies, seems to be looking at the wrong data. . . .

Low interest rates have hugely lifted assets largely owned by the very rich, and inflation in these areas is clearly apparent. Stocks have tripled and real estate prices in the major cities where the wealthy live have been soaring, as have the prices of artwork and the conspicuous consumption of luxury goods.

Now it may be true that certain assets like real estate in Manhattan and San Francisco, works of art, and yachts have been rising rapidly in price, but there is no meaningful price index in which these assets account for a large enough share of purchases to generate a significant inflation. So this claim by Mr. Rucker is just an empty rhetorical gesture to show how good-hearted he is and how callous and unfeeling Janet Yellen and her ilk are. He goes on.

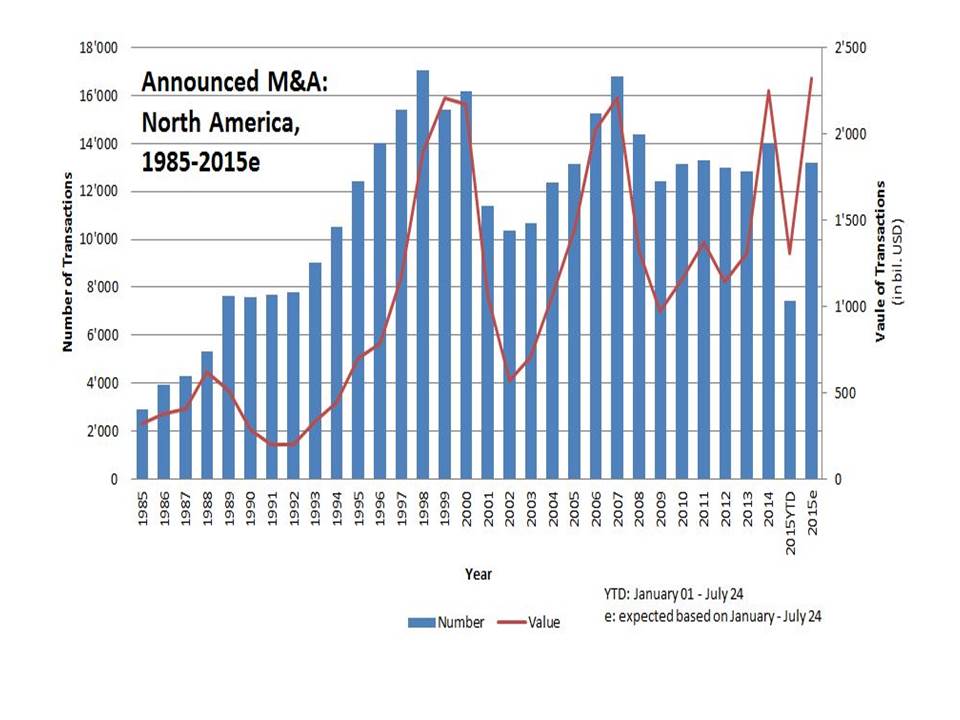

Cheap financing has led to a boom in speculative activity, and mergers and acquisitions. Most acquisitions are justified by “efficiencies” which is usually a euphemism for layoffs. Valeant Pharmaceuticals International, one of the nation’s most active acquirers, routinely fires “redundant” workers after each acquisition to enhance reported earnings. This elevates its stock, with which it makes the next acquisition. With money cheap, corporate executives have used cash flow to buy back stock, enhancing the value of their options, instead of investing for the future. This pattern, and the fear it engenders, has added to downward pressure on employment and wages.

Actually, according to data reported by the Institute for Mergers and Acquisitions and Alliances displayed in the accompanying chart, the level of mergers and acquisitions since 2008 has been consistently below what it was in the late 1990s when interest rates were over 5 percent and in 2007 when interest rates were also above 5 percent.

And if corporate executives are using cash flow to buy back stock to enhance the value of their stock options instead of making profitable investments that would enhance share-holder value, there is a serious problem in how corporate executives are discharging their responsibilities to shareholders. Violations of management responsibility to their shareholders should be disciplined and the legal environment that allows executives to disregard shareholder interests should be reformed. To blame the bad behavior of corporate executives on the Fed is a total distraction.

And if corporate executives are using cash flow to buy back stock to enhance the value of their stock options instead of making profitable investments that would enhance share-holder value, there is a serious problem in how corporate executives are discharging their responsibilities to shareholders. Violations of management responsibility to their shareholders should be disciplined and the legal environment that allows executives to disregard shareholder interests should be reformed. To blame the bad behavior of corporate executives on the Fed is a total distraction.

Having just attributed a supposed boom in speculative activity and mergers and acquisitions to the Fed’s low-interest rate policy, Mr. Rucker, without batting an eye, flatly denies that an increase in interest rates would have any negative effect on investment.

The Fed should raise rates in September. The focus on a quarter-point change in short rates and its precise date of imposition is foolishness. Expected rates of return on new investments are typically well above 10 percent. No sensible businessman would defer a sound investment because short-term rates are slightly higher for a few months. They either have a sound investment or they don’t.

Let me repeat that. “Expected rates of return on new investment are typically well above 10 percent.” I wonder what Mr. Rucker thinks the expected rate of return on speculative activity and mergers and acquisitions is.

But, almost despite himself, Mr. Rucker is on to something. Some long-term investment surely is sensitive to the rate of interest, but – and I know that this will come as a rude shock to adherents of Austrian Business Cycle Theory – most investment by business in plant and equipment depends on expected future sales, not the rate of interest. So the way to increase investment is really not by manipulating the rate of interest; the way to increase investment is to increase aggregate demand, and the best way to do that would be to increase inflation and expected inflation (aka nominal GDP and expected nominal GDP).