In a recent post, John Cochrane, responding to an earlier post by Nick Rowe about Neo-Fisherism, has tried to explain why raising interest rates could plausibly cause inflation to rise and reducing interest rates could plausibly cause inflation to fall, even though almost everyone, including central bankers, seems to think that when central banks raise interest rates, inflation falls, and when they reduce interest rates, inflation goes up.

In his explanation, Cochrane concedes that there is an immediate short-term tendency for increased interest rates to reduce inflation and for reduced interest rates to raise inflation, but he also argues that these effects (liquidity effects in Keynesian terminology) are transitory and would be dominated by the Fisher effects if the central bank committed itself to a permanent change in its interest-rate target. Of course, the proviso that the central bank commit itself to a permanent interest-rate peg is a pretty important qualification to the Neo-Fisherian position, because few central banks have ever committed themselves to a permanent interest-rate peg, the most famous attempt (by the Fed after World War II) to peg an interest rate having led to accelerating inflation during the Korean War, thereby forcing the peg to be abandoned, in apparent contradiction of the Neo-Fisherian view.

However, Cochrane does try to reconcile the Neo-Fisherian view with the standard view that raising interest rates reduces inflation and reducing interest rates increases inflation. He suggests that the standard view is strictly a short-run relationship and that the way to target inflation over the long-run is simply to target an interest rate consistent with the desired rate of inflation, and to rely on the Fisher equation to generate the actual and expected rate of inflation corresponding to that nominal rate. Here’s how Cochrane puts it:

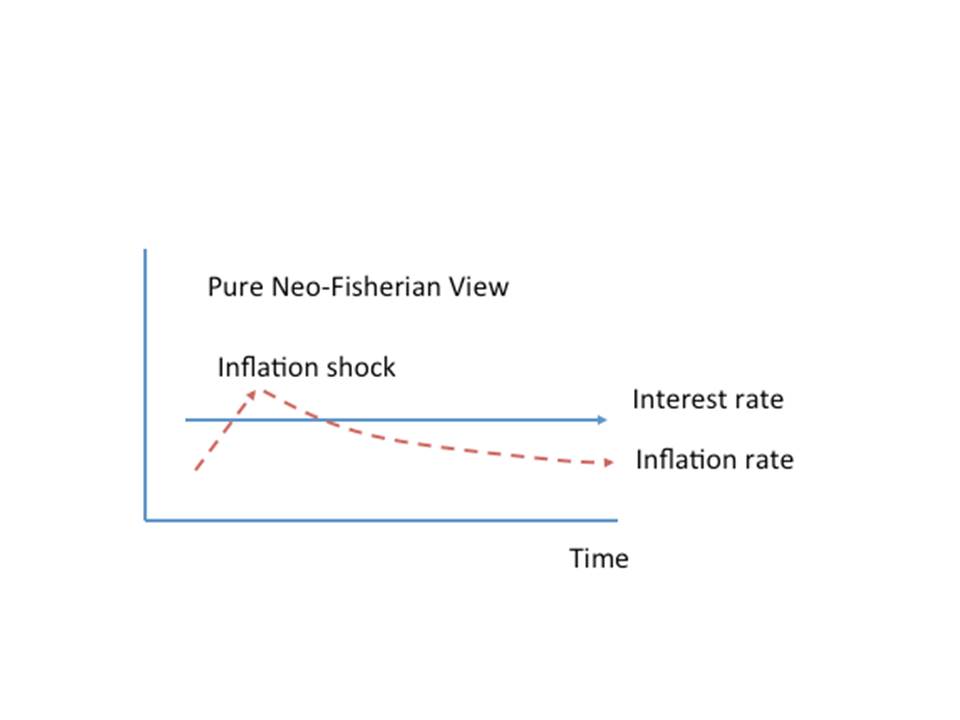

We can put the issue more generally as, if the central bank does nothing to interest rates, is the economy stable or unstable following a shock to inflation?

For the next set of graphs, I imagine a shock to inflation, illustrated as the little upward sloping arrow on the left. Usually, the Fed responds by raising interest rates. What if it doesn’t? A pure neo-Fisherian view would say inflation will come back on its own.

Again, we don’t have to be that pure.

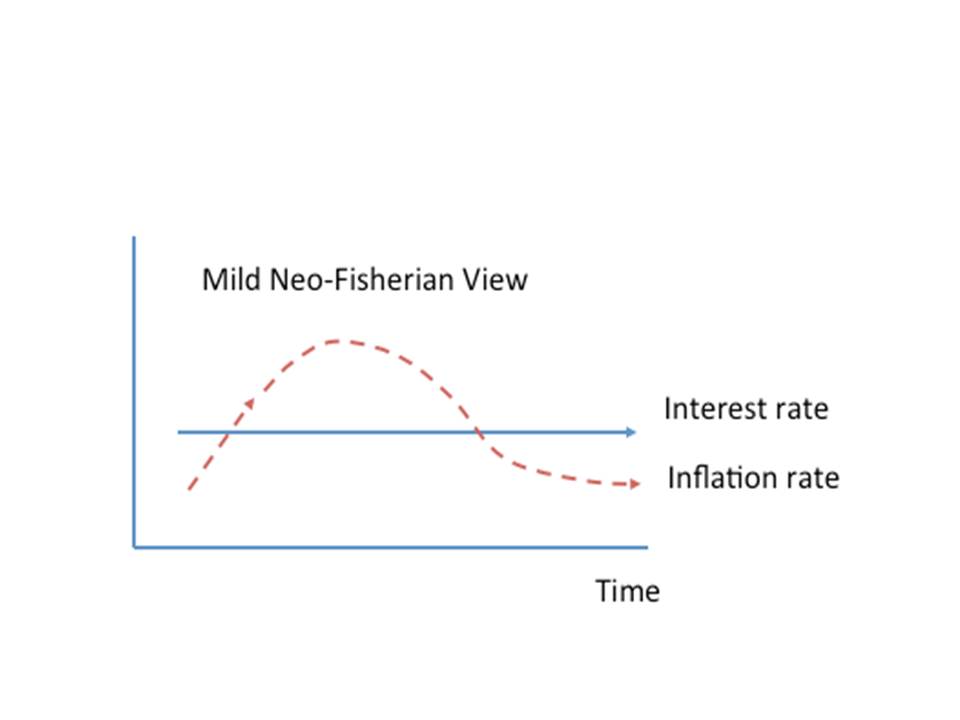

The milder view allows there may be some short run dynamics; the lower real rates might lead to some persistence in inflation. But even if the Fed does nothing, eventually real interest rates have to settle down to their “natural” level, and inflation will come back. Mabye not as fast as it would if the Fed had aggressively tamed it, but eventually.

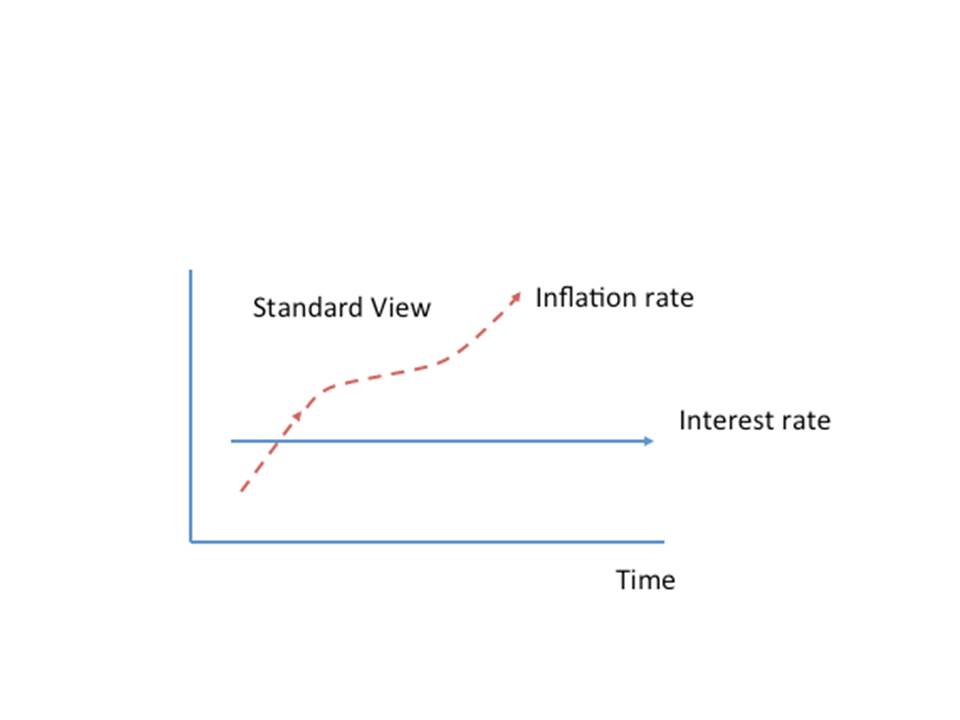

By contrast, the standard view says that inflation is unstable. If the Fed does not raise rates, inflation will eventually careen off following the shock.

Now this really confuses me. What does a shock to inflation mean? From the context, Cochrane seems to be thinking that something happens to raise the rate of inflation in the short run, but the persistence of increased inflation somehow depends on an underlying assumption about whether the economy is stable or unstable. Cochrane doesn’t tell us what kind of shock to inflation he is talking about, and I can imagine only two possibilities, either a nominal shock or a real shock.

Let’s say it’s a nominal shock. What kind of nominal shock might Cochrane have in mind? An increase in the money supply? Well, presumably an increase in the money supply would cause an increase in the price level, and a temporary increase in the rate of inflation, but if the increase in the money supply is a once-and-for-all increase, the system must revert, after a temporary increase, back to the old rate of inflation. Or maybe, Cochrane is thinking of a permanent increase in the rate of growth in the money supply. But in that case, why would the rate of inflation come back on its own as Cochrane suggests it would? Well, maybe it’s not the money supply but money demand that’s changing. But again, one would normally assume that an appropriate change in central-bank policy could cope with such a scenario and stabilize the rate of inflation.

Alright, then, let’s say it’s a real shock. Suppose some real event happens that raises the rate of inflation. Well, like what? A supply shock? That raises the rate of inflation, but since when is the standard view that the appropriate response by the central bank to a negative supply shock is to raise the interest-rate target? Perhaps Cochrane is talking about a real shock that reduces the real rate of interest. Well, in that case, the rate of inflation would certainly rise if the central bank maintained its nominal-interest-rate target, but the increase in inflation would not be temporary unless the real shock was temporary. If the real shock is temporary, it is not clear why the standard view would recommend that the central bank raise its target rate of interest. So, I am sorry, but I am still confused.

Now, the standard view that Cochrane is disputing is actually derived from Wicksell, and Wicksell’s cycle theory is in fact based on the assumption that the central bank keeps its target interest rate fixed while the natural rate fluctuates. (This, by the way, was also Hayek’s assumption in his first exposition of his theory in Monetary Theory and the Trade Cycle.) When the natural rate rises above the central bank’s target rate, a cumulative inflationary process starts, because borrowing from the banking system to finance investment is profitable as long as the expected return on investment exceeds the interest rate on loans charged by the banks. (This is where Hayek departed from Wicksell, focusing on Cantillon Effects instead of price-level effects.) Cochrane avoids that messy scenario, as far as I can tell, by assuming that the initial position is one in which the Fisher equation holds with the nominal rate equal to the real plus the expected rate of inflation and with expected inflation equal to actual inflation, and then positing an (as far as I can tell) unexplained inflation shock, with no change to the real rate (meaning, in Cochrane’s terminology, that the economy is stable). If the unexplained inflation shock goes away, the system must return to its initial equilibrium with expected inflation equal to actual inflation and the nominal rate equal to the real rate plus inflation.

In contrast, the Wicksellian assumption is that the real rate fluctuates with the nominal rate and expected inflation unchanged. Unless the central bank raises the nominal rate, the difference between the profit rate anticipated by entrepreneurs and the rate at which they can borrow causes the rate of inflation to increase. So it does not seem to me that Cochrane has in any way reconciled the Neo-Fisherian view with the standard view (or at least the Wicksellian version of the standard view).

PS I would just note that I have explained in my paper on Ricardo and Thornton why the Wicksellian analysis (anticipated almost a century before Wicksell by Henry Thornton) is defective (basically because he failed to take into account the law of reflux), but Cochrane, as far as I can tell, seems to be making a completely different point in his discussion.