Ben Bernanke held a press conference today at the conclusion of the FOMC meeting held yesterday and today. The stock market had risen by almost 2 percent on Monday and Tuesday, apparently in hopes that Bernanke would have something encouraging to say about Fed policy. They were obviously disappointed. The accompanying chart shows how the S&P 500 has fluctuated since last Thursday, the sharp drop today coincided with Bernanke’s press conference.

What was so disturbing to the markets? Well, Bernanke’s press conference triggered some sharp movements in the bond markets. The yield on the 10-year Treasury jumped by 13 basis points to 2.33%. I don’t have a chart of the intra-day fluctuation, but I am pretty sure almost all of the movement occurred after the press conference started. Meanwhile the yield on the 10-year TIPS jumped 15 basis points, from 0.14% to 0.29%, implying a 2-basis-point drop in the breakeven TIPS spread, to 2.04%. A two-basis-point change in inflation expectations is not very remarkable. So it seems that what drove the increase in yield was the increase in the real rate. But one has to be careful in identifying the TIPS spread with the real rate of interest, especially when one sees sudden changes in the market, changes that could reflect factors other than the real rate of interest, such as illiquidity in the TIPS market or increasing uncertainty about future inflation, even though expected inflation is not changing much.

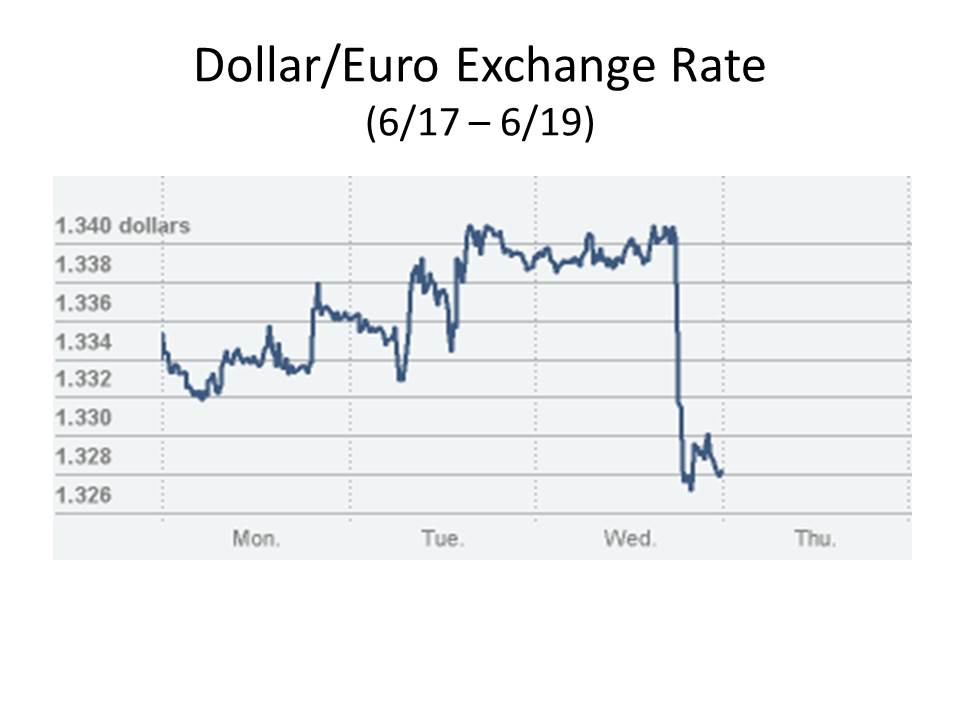

Let’s look at two other markets that moved sharply after Bernanke started talking this afternoon. The chart below shows the movement of dollar/euro exchange rate since Monday. The dollar weakened slightly on Monday and Tuesday and Wednesday morning, but as soon as Bernanke got started the dollar shot up against the euro.

That should not necessarily be construed as a vote of confidence in Bernanke, even though it apparently pleased Bernanke et al. to think that the sharp run-up in the value of the dollar in August 2008 was a sign of confidence that Fed policy to keep inflation expectations anchored was working. It is hard to interpret today’s sharp increase in the value of the dollar as anything but an expectation of future tightening of monetary policy by the Fed. But then why did inflation expectations fall by only 2 basis points?

Another market that is supposed to be sensitive to inflation expectations is gold, though in my view the demand for gold is too irrational to provide any usable information about expectations. But I will suspend my disbelief in the rationality of gold traders for the time being to note that the price of gold has just fallen to a new low for the year, dropping below $1340 an ounce or almost 3% since yesterday. A fall in the value of gold is consistent with an increase in real interest rates or with a decline in inflation expectations, so take your pick.

Some people have suggested that declining inflation expectations and rising real interest rates are manifestations of a positive supply shock, also reflected in declining commodity prices. A positive supply shock would have provided the Fed with an opportunity to relax monetary policy further without risk of raising inflation or inflation expectations from current levels, which already are well below the Fed’s announced 2% target. If continued Fed easing was what the markets had been anticipating earlier in the week, reflected in a gently falling dollar exchange rate, even with inflation expectations stable or falling, then Bernanke’s announcement today constituted a tightening of policy relative to expectations. The tightening drove up the dollar and caused a further, albeit small, decline in inflation expectations. (But I should note that this interpretation depends on what may be an oversimplified identification of the TIPS spread with inflation expectations.)

At any rate, I don’t think that we have a clear understanding of what is driving markets at this point. Markets still seem to be in confusion. Today’s movements in the markets were sudden and sharp, but they were also fairly modest. A one or two percent movement in markets is hardly a major event. Nevertheless, by displaying an unseemly haste to withdraw the very modest monetary stimulus that the Fed has begrudgingly provided, Bernanke may have given the markets a bit of scare, reminding them how indifferent central bankers have been to the ongoing disaster of the Little Depression. The markets did not panic, but we may be flying into turbulence. Keep your seat belts fastened.

David, I agree with you. And yes, the market moves were not ‘outstanding’ because the news was not so surprisng.It´s being dished out incrementally with some ‘bells and whistles’ in the form of ‘soothing words’ attached. After all, it´s been going on for five years and the acutness of the pain ended 4 years ago.

LikeLike

When, oh when, will the Fed learn that the markets and the economy love QE.

Since when is it a crime to print money and monetize federal debt? If no inflation results, then why not continue? This may be a rare opportunity.

Or it may be the new norm.

In any event the Fed should think about expanding QE, not contracting.

LikeLike

Intra day of the 10 yr yield:

https://pbs.twimg.com/media/BNJihQECMAA5S2_.png:large

LikeLike

Does ZIRP have traction under these conditions? What is the impact iyo of the interest paid on excess reserves by the fed?

LikeLike